Semiconductor Manufacturing Equipment Market Size Analysis:

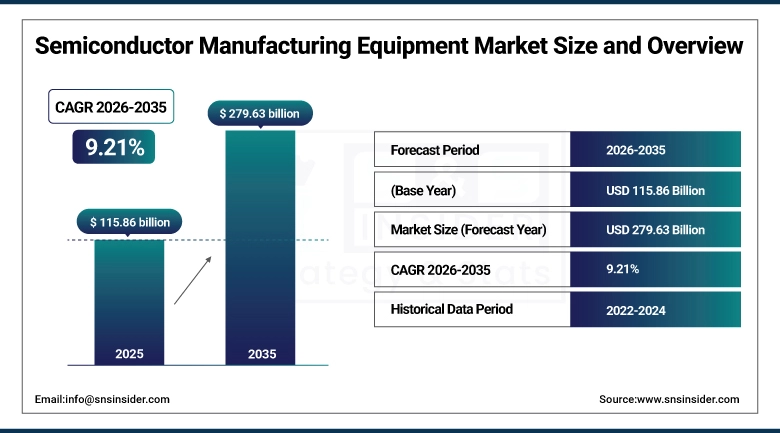

The Semiconductor Manufacturing Equipment Market size was valued at USD 115.86 Billion in 2025 and is projected to reach USD 279.63 Billion by 2035, growing at a CAGR of 9.21% during 2026–2035.

The growth of the Semiconductor Manufacturing Equipment Market is fueled by the increasing demand for advanced semiconductor chips in AI, 5G, automotive, and data center applications. Increasing investments in semiconductor fabrication plants and government support for local semiconductor production also fuel the growth of the Semiconductor Manufacturing Equipment Market. Ongoing improvements in lithography, miniaturization, and wafer processing technologies are also contributing factors to the growth of the Semiconductor Manufacturing Equipment Market. In addition, the rise of consumer devices and high-performance computing, as well as the shift to advanced semiconductor packaging and 3D technologies, is accelerating the adoption of semiconductor manufacturing equipment worldwide.

Semiconductor Manufacturing Equipment Market Size and Forecast:

-

Market Size in 2025: USD 115.86 Billion

-

Market Size by 2035: USD 279.36 Billion

-

CAGR: 9.21% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Semiconductor Manufacturing Equipment Market - Request Free Sample Report

Semiconductor Manufacturing Equipment Market Key Trends:

-

Advanced EUV Lithography: Increasing adoption for smaller nodes and higher chip performance.

-

AI-Driven Manufacturing: Integration of AI for process optimization and yield improvement.

-

Advanced Packaging: Growth of 2.5D/3D packaging and chiplet architectures.

-

Rising Fab Investments: Expansion of semiconductor fabs across global regions.

-

Inspection & Metrology Demand: Greater focus on precision and defect control.

-

Automation & Smart Factories: Adoption of Industry 4.0 and fully automated production lines.

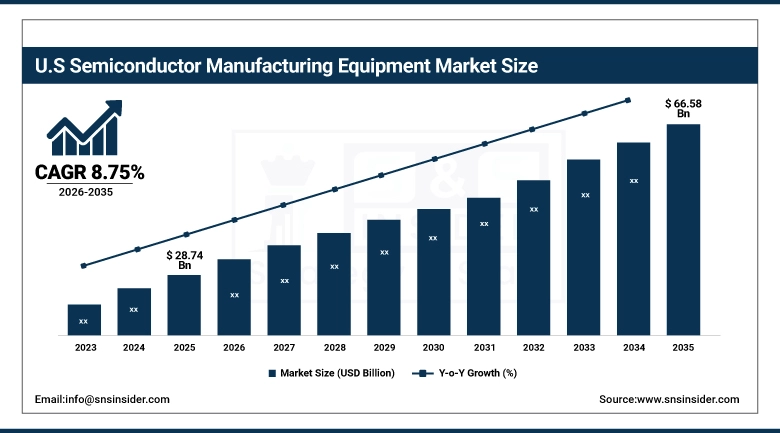

U.S. Semiconductor Manufacturing Equipment Market Size Outlook:

The U.S. Semiconductor Manufacturing Equipment Market was valued at USD 28.74 Billion in 2025 and is projected to reach USD 66.58 Billion by 2035, growing at a CAGR of 8.75% during 2026–2035. Growth in the U.S. semiconductor manufacturing equipment market is driven by CHIPS Act investments, expansion of domestic fabs, rising AI and HPC demand, technological advancements, and supply chain localization initiatives.

Semiconductor Manufacturing Equipment Market Key Drivers:

-

Rising Demand for Advanced Semiconductor Chips and Fab Expansion

The Semiconductor Manufacturing Equipment market is also driven by the increasing need for advanced semiconductor chip technology for AI, 5G, automotive, and high-performance computing. The rapid growth of semiconductor fabrication plants, also known as semiconductor fabs, in the Asia Pacific and North American regions is also boosting the Semiconductor Manufacturing Equipment market. Estimates suggest that over 60% of investments are being made in advanced node manufacturing, reflecting the growth rate. Government policies to support semiconductor manufacturing are also fueling the growth of the Semiconductor Manufacturing Equipment market.

Semiconductor Manufacturing Equipment Market Key Restraints:

-

High Capital Investment and Complex Manufacturing Processes

The market faces limitations in its growth due to the high capital requirements for the equipment used in the manufacturing of semiconductors, as well as the complexities involved in the fabrication of the materials. It requires billions of dollars to establish a fab for the manufacturing of semiconductors, which hampers the entry of new companies into the industry. Research has shown that about 40% of the companies face difficulties in entering the industry due to the high capital requirements and the complexities involved in the fabrication of the materials.

Semiconductor Manufacturing Equipment Market Key Opportunities:

-

Advancements in Advanced Packaging and AI-Driven Manufacturing

Significant opportunities exist due to advancements in advanced packaging technologies such as 2.5D and 3D integration, as well as AI-driven manufacturing processes. These advancements improve chip efficiency and scalability, creating a need in next-generation equipment. According to industry reports, investment in advanced packaging is growing by over 12% annually. In addition, there is increased interest in automation, smart fabs, as well as expansion in emerging markets such as India and Southeast Asia. These factors provide long-term growth opportunities for industry players.

Semiconductor Manufacturing Equipment Market Segments:

-

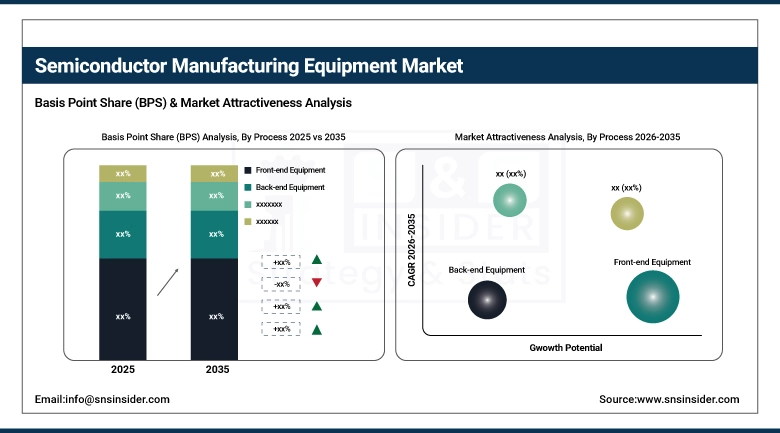

By Process: In 2025, Front-end Equipment dominated with 58% share; Packaging Equipment fastest growing segment during 2026–2035

-

By Equipment Type: In 2025, Lithography Equipment dominated with 32% share; Deposition Equipment fastest growing segment during 2026–2035

-

By Application: In 2025, Semiconductor Fabrication Plants/Foundries dominated with 55% share; Testing & Inspection fastest growing segment during 2026–2035

-

By End User: In 2025, Consumer Electronics dominated with 38% share; Automotive fastest growing segment during 2026–2035

By Process: Front-End Equipment Leads as Packaging Equipment Expands Rapidly

Front-end equipment has the largest share in the market due to the criticality of the wafer fabrication process, which includes equipment like lithography, etching, and deposition. This process is critical in the performance of the chips. This process requires highly advanced and capital-intensive equipment. The ongoing process of reducing the node size and improving the efficiency of the chips also increases the demand for front-end equipment, thus maintaining the leading position in the market.

The packaging equipment market is growing rapidly due to the increasing use of advanced packaging technologies like 2.5D and 3D integration. With the increasing complexity of the chips, the role of the packaging equipment has also become critical in the performance enhancement and miniaturization of the chips. The increasing demand for high-performance computing and AI chips has accelerated the growth of the packaging equipment market.

By Equipment Type: Lithography Equipment Leads as Deposition Equipment Expands Rapidly

The equipment segment of lithography is the largest due to the necessity of this equipment in defining the pattern on the semiconductor wafer. This makes it the most critical and costly step in the semiconductor fabrication process. The shift to extreme ultraviolet (EUV) lithography for the latest technology nodes has raised the stakes and the level of investments in this technology by the leading semiconductor companies.

The deposition equipment market is growing at a tremendous rate due to the rise in the requirement of thin layers in the latest semiconductor devices. Technologies like CVD and ALD are becoming popular due to the requirement of precise layering of materials in the latest semiconductor devices.

By Application: Semiconductor Fabrication Plants/Foundries Lead as Testing & Inspection Expand Rapidly

The semiconductor fabrication plants and foundries hold the largest share of the market, as these are the major users of the equipment used in the manufacturing process of semiconductor chips on a large scale. The rise in the construction and expansion of semiconductor fabrication plants globally, with the support of government policies.

The market for testing and inspection is also growing rapidly due to the increasing complexity of semiconductor devices and the need for precise and defect-free devices.

By End User: Consumer Electronics Lead as Automotive Expands Rapidly

Consumer electronics lead in this market segment due to the large demand for semiconductors in gadgets such as smartphones, laptops, and wearables. High product turnover and innovations in this segment, along with increasing global consumption, contribute to the demand for semiconductor manufacturing equipment.

The automotive segment is growing rapidly, especially due to the increasing number of semiconductors in modern vehicles for electric vehicles, ADAS, infotainment systems, and autonomous driving. The increasing number of electric and autonomous vehicles is contributing to the growth of this segment due to increasing demand for semiconductors.

Semiconductor Manufacturing Equipment Market Regional Analysis:

Asia-Pacific Semiconductor Manufacturing Equipment Market Insights:

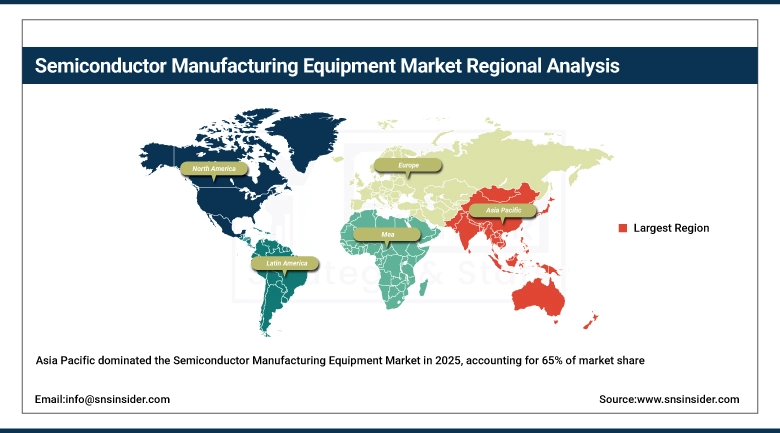

Asia Pacific held the highest regional revenue share of the global Semiconductor Manufacturing Equipment Market in 2025, i.e., 65%. The region’s dominance can be attributed to the fact that the region has some of the major semiconductor manufacturing centers like China, Taiwan, South Korea, and Japan. High investment in fabs, a strong electronics manufacturing infrastructure, and a growing demand for consumer electronics and automotive semiconductors boost the region’s dominance in the global Semiconductor Manufacturing Equipment Market during 2026-2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Semiconductor Manufacturing Equipment Market Insights:

In terms of regional revenue, North America semiconductor manufacturing equipment market in 2025 accounts for approx. 22%. North America is expanding, driven by robust government support, including the CHIPS Act, investments in domestic semiconductor fabrication facilities, and demand for high-end chips in AI, data centers, and defense. With most of the global leading semiconductor manufacturers present in North America, it is a natural destination for semiconductor manufacturing equipment.

Europe Semiconductor Manufacturing Equipment Market Insights:

The Europe Semiconductor Manufacturing Equipment market is growing steadily due to rising investments in semiconductor manufacturing, high semiconductor demand in the automotive industry, and favorable government policies. Europe is focusing on advanced technologies and automotive electronics, and government initiatives to boost semiconductor manufacturing and independence are also driving the Europe Semiconductor Manufacturing Equipment market. Research institutions and semiconductor companies are also joining hands to boost innovation in the field of semiconductors and driving the Europe Semiconductor Manufacturing Equipment market.

Latin America Semiconductor Manufacturing Equipment Market Insights:

The Latin America Semiconductor Manufacturing Equipment market is growing steadily and is being driven by the gradual growth of the electronics manufacturing industry in the region. In addition to this, the growing adoption of semiconductor-based technologies and the increase in foreign investments in the region are also driving the Semiconductor Manufacturing Equipment market in Latin America. The improving infrastructure in the region and the growing need for consumer electronics are also boosting the Semiconductor Manufacturing Equipment market in Latin America.

Middle East & Africa (MEA) Semiconductor Manufacturing Equipment Market Insights:

The Middle East & Africa Semiconductor Manufacturing Equipment Market is growing gradually. This growth can be attributed to the increase in digitalization, growing need for electronics, and increased investments in technology infrastructure. The Middle East & Africa region is aiming to build diversified economies and develop capabilities in semiconductors. In addition, government initiatives, international collaborations, and investments in advanced technologies are also projected to boost the Middle East & Africa Semiconductor Manufacturing Equipment Market during the forecast period of 2026-2035.

Semiconductor Manufacturing Equipment Market Competitive Landscape:

Tokyo Electron Limited is one of the major semiconductor manufacturing equipment companies that focus on high-end wafer fabrication equipment such as deposition tools, etching tools, cleaning tools, and lithography tools. The company mainly concentrates on process technology innovations for high-end chips and next-generation semiconductor applications.

-

In 2025, Tokyo Electron Limited expanded its advanced deposition and etching solutions portfolio to support 2nm and below semiconductor nodes, enhancing precision, yield, and efficiency for leading chip manufacturers.

ASML is a global leader in lithography equipment and is best known for its extreme ultraviolet (EUV) lithography systems used in advanced semiconductor manufacturing. ASML is a key enabler for the development of cutting-edge semiconductors, serving leading global semiconductor foundries.

-

In 2025, ASML introduced next-generation High-NA EUV lithography systems, significantly improving resolution and enabling further miniaturization of semiconductor devices for advanced computing and AI applications.

Semiconductor Manufacturing Equipment Companies are:

-

ASML

-

Hitachi High-Tech Corporation

-

EV Group

-

Advanced Dicing Technologies

-

Evatec

-

FormFactor

-

Lam Research Corporation

-

KLA Corporation

-

Advantest

-

Plasma-Therm

-

Nordson

-

QP Technologies

-

Modutek

-

Daifuku

-

Canon

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 115.86 Billion |

| Market Size by 2035 | USD 279.63 Billion |

| CAGR | CAGR of 9.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Process (Front-end Equipment, Back-end Equipment, Packaging Equipment) • By Equipment Type (Lithography Equipment, Etching Equipment, Deposition Equipment) • By Application (Semiconductor Fabrication Plants/Foundries, Semiconductor Electronics Manufacturing, Testing & Inspection) • By End User (Consumer Electronics, Automotive, Telecommunications) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Tokyo Electron Limited, ASML, Hitachi High-Tech Corporation, EV Group, Advanced Dicing Technologies, Evatec, Nikon Corporation, FormFactor, Lam Research Corporation, KLA Corporation, Advantest, Plasma-Therm, Nordson, QP Technologies, Modutek, Daifuku, Canon. |

Frequently Asked Questions

Ans: The Semiconductor Manufacturing Equipment Market is expected to grow at a CAGR of 9.21% during 2026–2035.

Ans: The Semiconductor Manufacturing Equipment Market size was valued at USD 115.86 Billion in 2025 and is projected to reach USD 279.63 Billion by 2035.

Ans: The key drivers of the Semiconductor Manufacturing Equipment Market include rising demand for advanced semiconductors (AI, 5G, automotive), increasing fab investments, technological advancements, and government support for domestic chip production.

Ans: The Front-end Equipment segment dominated the Semiconductor Manufacturing Equipment Market during the projected period.

Ans: Asia-Pacific dominated the Semiconductor Manufacturing Equipment Market in 2025.

Get in Touch