Server AI Chip Market Report Scope & Overview:

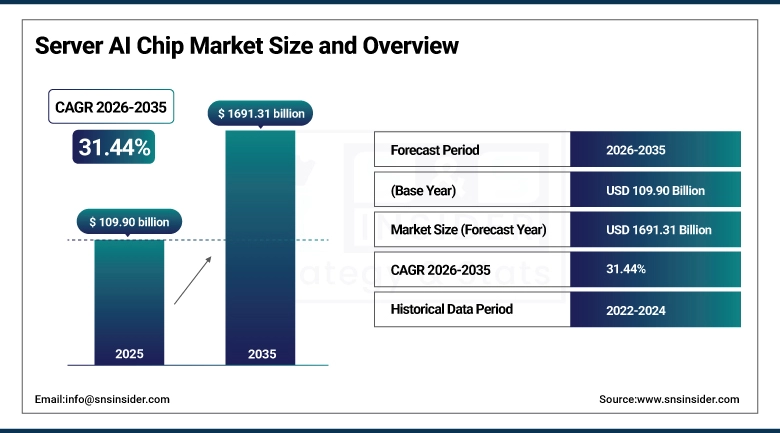

The Server AI Chip Market size was valued at USD 109.90 Billion in 2025 and is projected to reach USD 1691.31 Billion by 2035, growing at a CAGR of 31.44% during 2026–2035.

The Server AI Chip market is experiencing healthy growth due to increased demand for domestic AI semiconductor development to support regions that are reducing reliance on banned or lack of access to advanced GPUs. Organizations are moving more resources in-house to design AI chips and build a scalable data center infrastructure to scale large language models to support cloud computing and enterprise AI workloads. Such a shift is driving increased adoption of ASIC-based and custom AI server chips, further enhancing regional AI ecosystems and heightening competition between regional and global semiconductor companies, while also helping spur broader deployments of high-performance AI servers at scale across hyperscale and telecom data center environments.

On November 28, 2025, Baidu is emerging as a leading AI chip player in China through its Kunlunxin unit, strengthening domestic semiconductor capabilities to address rising AI chip shortages and reduce reliance on foreign suppliers, while expanding its role in AI infrastructure, cloud computing, and large-scale data center deployments.

Market Size and Growth Forecast:

-

Market Size in 2025: USD 109.90 Billion

-

Market Size by 2035: USD 1691.31 Billion

-

CAGR: 31.44% (from 2026 to 2035)

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Server AI Chip Market - Request Free Sample Report

Server AI Chip Market Trends Highlights:

-

Rapid expansion driven by hyperscale data centers and growing AI workloads such as generative AI, machine learning, and large language models

-

Strong shift toward GPU, ASIC, and custom AI server chips to improve performance, efficiency, and scalability in AI computing infrastructure

-

Increasing investments from cloud providers and semiconductor companies in AI-optimized data center architectures

-

Rising adoption of high-bandwidth memory (HBM) and advanced packaging technologies to support high-performance AI processing

-

Growing focus on energy-efficient AI server chips to address power consumption and thermal management challenges

-

Intensifying competition among global players, including GPU manufacturers, cloud hyperscalers, and emerging AI chip developers

U.S. Server AI Chip Market Size Outlook:

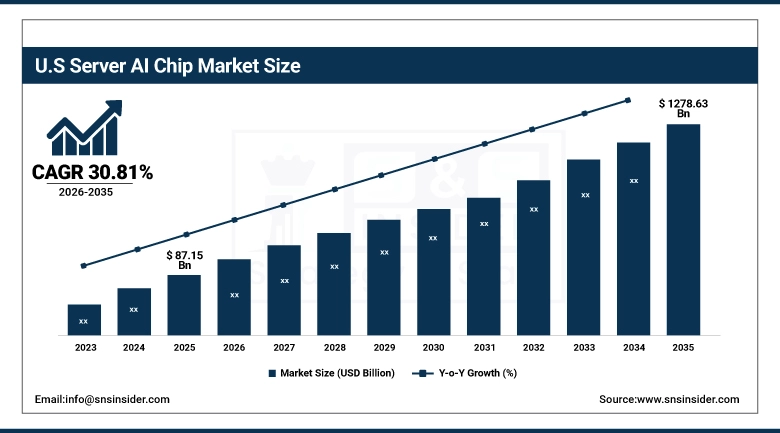

The U.S. Server AI Chip Market size was valued at USD 87.15 Billion in 2025 and is projected to reach USD 1278.63 Billion by 2035, growing at a CAGR of 30.81% during 2026–2035, growing rapidly driven by the rapid growth of the hyperscale data centers, adoption of Generative AI, demand for high-performance computing infrastructure, migrating of AI workloads in the cloud environment, advancements in GPU and ASIC-based server chips, strong investments from leading semiconductor companies and cloud companies, strengthening the overall AI server ecosystem.

Market Drivers: Stronger Global Controls and Secure Supply Chains Driving Server AI Chip Market Growth

Increasing stringency in the enforcement of export control regulations on related technology collaterals to high-performance computing infrastructure has been found to accelerate the Server AI Chip Market at a large extent. Rising limitations on higher AI server hardware are forcing semiconductor groups, cloud carriers, as well as device integrators to get extra secure and compliant and stick to extra vigilant deliver chain practices. Datacenter management is requiring AI chips with traceability, verified supply chains and managed deployments of GPU- and ASIC based servers, and this is creating a new demand-driven acceleration of this trend. Consequently, we see more emphasis on governance, risk mitigation and regulated growth of AI data center infrastructure around the globe.

On March 26, 2026, The U.S. Department of Justice indicted three men for allegedly conspiring to illegally export AI servers containing NVIDIA GPUs via intermediaries via illegal means, the indictment reflects the ongoing enforcement actions against the circumvention of bans on high-performance computing hardware transfers around the globe to new international markets, which is also re-iterate strict compliance requirements for advanced AI chip supply chains.

Market Restraints: Structural and Operational Barriers Limiting Server AI Chip Industry Expansion

Despite a healthy demand for AI-enabled data centers, the Server AI Chip Industry is subject to certain restraints that might hinder the overall growth when it comes to services provided. The high R&D and production costs of high-end AI processors (GPUs, custom ASICs) are putting tremendous financial pressure on semiconductor manufacturers. This dual-level restriction in scalability is compounded by supply chain constraints in advanced node fabrication and high-bandwidth memory availability. Moreover, as AI server infrastructure consumes more power and requires effective thermal management, operational complexity and costs rise. Increased geopolitical tensions and bans on advanced chips exports also complicate global supply chains, preventing smooth distribution and rapid adoption in some areas.

Market Opportunities: Strengthening Compliance and Secure Deployment in the Server AI Chip Market

The Server AI Chip Market is increasingly focused on secure deployment frameworks and controlled distribution of high-performance AI processors used in data centers and cloud infrastructure. Increased focus on compliance obligations are bolstering the demand for traceable and reliable AI server chips with governance capabilities. Notably, this shift is helping both semiconductor companies and cloud providers foster supply chain transparency and proper utilization of AI computing resources in worldwide hyperscale ecosystem, ultimately fortifying the stability and trust of the entire server AI chip marketplace.

On April 2, 2026, Singapore authorities launched an investigating a suspected case of export fraud where servers provided by Dell Technologies were allegedly misledgered as being for a different end user ultimately receiving the servers from the UK via intermediaries. The case relates to fears that US servers possibly carrying advanced Nvidia chips intended for artificial-intelligence applications had been misused, triggering a scrutiny of the lessoned compliance with international export control rules.

Server AI Chip Market Segment Highlights:

-

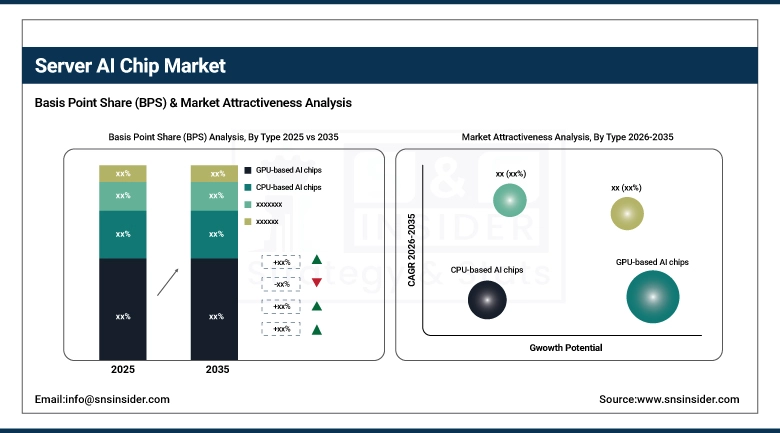

By Type: Dominant – GPU-based AI chips (44.60% in 2025 → 34.20% in 2035); Fastest-Growing – ASIC-based AI chips (18.10% in 2025 → 38.70% in 2035)

-

By Technology: Dominant – Deep Learning Chips (34.80% in 2025 → 41.80% in 2035); Fastest-Growing – Natural Language Processing (NLP) Chips (12.60% in 2025 → 17.20% in 2035)

-

By Application: Dominant – Computer Vision (22.40% in 2025 → 26.80% in 2035); Fastest-Growing – NLP (18.70% in 2025 → 24.60% in 2035)

-

By End-User: Dominant – Data Centers (38.60% in 2025 → 42.30% in 2035); Fastest-Growing – Automotive (16.70% in 2025 → 19.60% in 2035)

By Type: GPU-based AI Chips (Dominant) and ASIC-based AI Chips (Fastest-Growing)

GPU-based AI chips dominate the market owing to their strong parallel processing capability, high flexibility, and extensive use across AI training and inference workloads in data centers, cloud platforms, and advanced computing applications. In contrast, ASIC-based AI chips are becoming the fastest-growing segment, driven by significantly better energy performance, high level of workload specificity and widespread use in edge AI devices, autonomous systems, and next-gen hyperscale AI infrastructure.

By Technology: Deep Learning Chips (Dominant) and Natural Language Processing (NLP) Chips (Fastest-Growing)

The technology segment is dominated by Deep Learning chips as they possess superior capacity for handling complicated neural network computations, high efficiency for training Large Scale AI models, and a broad deployment footprint across enterprise AI and cloud workloads. Conversely, NLP chips are are the fastest growing segment for reasons that stem from the growing demand for conversational AI, more affordable virtual assistants, real-time language translation and generative AI applications, which are rapidly being adopted across the consumer and enterprise ecosystems.

By Application: Computer Vision (Dominant) and NLP (Fastest-Growing)

Computer vision leads the application segment due to its extensive use in image recognition, surveillance systems, autonomous vehicles, and industrial automation, supported by continuous advancements in AI-enabled visual processing. Meanwhile, NLP is the fastest-growing application segment as organizations increasingly adopt AI-driven chatbots, sentiment analysis tools, and language-based automation solutions across customer service, healthcare, and enterprise communication platforms.

By End-User: Data Centers (Dominant) and Automotive (Fastest-Growing)

Data centers dominate the end-user segment owing to their central role in AI model training, cloud computing, and large-scale data processing infrastructure supporting global digital transformation. In contrast, the automotive segment is the fastest-growing end-user category due to rapidly-growing integration of AI chips in autonomous driving systems, advanced driver-assistance systems (ADAS) and in-vehicle infotainment solutions thus accelerating the transition towards intelligent mobility.

Server AI Chip Market Regional Highlights:

-

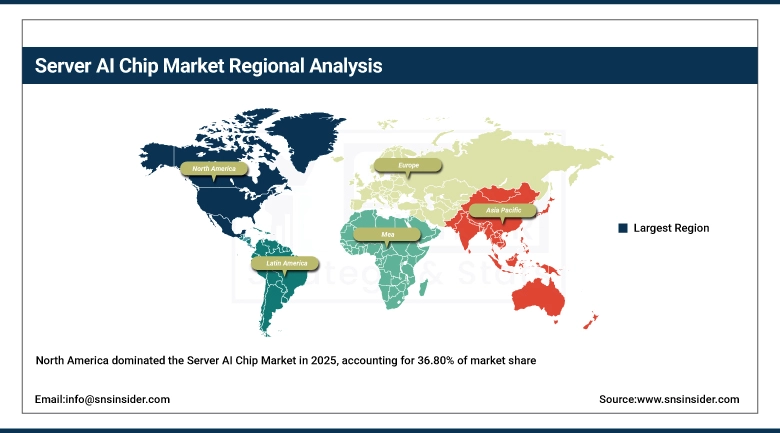

North America (Dominant – 36.80% in 2025 → 33.10% in 2035, CAGR 30.05%)

-

Asia-Pacific (Fastest-Growing – 28.90% in 2025 → 34.80% in 2035, CAGR 33.88%)

-

Europe (21.70% → 19.60%, CAGR 30.10%)

-

Latin America (6.40% → 6.80%, CAGR 32.24%)

-

Middle East & Africa (6.20% → 5.70%, CAGR 30.34%)

North America Server AI Chip Market Insights:

North America is the dominating region in the Server AI Chip market due to the strong presence of leading technology companies, advanced data center infrastructure, and early adoption of AI-driven computing solutions. The region benefits from significant investments in hyperscale cloud platforms, high-performance computing, and continuous innovation in AI chip design by major players such as NVIDIA, AMD, Intel, and leading cloud service providers. Additionally, strong government support for semiconductor development and robust R&D capabilities further strengthen its market leadership position globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Server AI Chip Market Insights:

The robust growth in the U.S. Server AI Chip market is driven by a fast-paced AI adoption landscape and consistent hyperscale data center expansion, as well as leadership in semiconductor innovation, rising demand for cloud computing, and sizeable investment in AI infrastructure.

Asia-Pacific Server AI Chip Market Insights:

Asia-Pacific is the highest growing region in Server AI Chip market as it has fast digital transformation, growing number of ultra large scale of data center, and rising adoption of AI in business sectors like it, telecommunication and manufacturing. The rapid growth of Asian markets is being driven by strong government policies supporting semiconductor development in many Asian countries including China, Japan and South Korea, increasing demand for cloud computing applications, and cloud investment from global mega-tech companies. Asia-Pacific market growth is bolstered by the increasing demand for high-performance computing and low-cost AI infrastructure.

China Server AI Chip Market Insights:

Rapid AI infrastructure expansion, government semiconductor initiatives, enterprise data center deployment at large scale and rapidly growing demand from cloud computing and hyperscale technology companies are some of the major factors that are driving growth in the Server AI Chip industry in China.

Europe Server AI Chip Market Insights:

The adoption of AI technology across enterprises in Europe has been gaining traction with stable growth in EMEA Server AI Chip Industry fueled by strong regulatory support for digital transformation coupled with investments in cloud infrastructure and high-performance computing. Automotive AI, industrial automation and research-focused AI applications also chips are found as the ones harvesting the benefits of the region. Moreover, partnerships between tech enterprises and governmental programs for bolstering semiconductor resources are aiding to a consistent growth of market in major economies of Europe.

Germany Server AI Chip Market Insights:

The Server AI Chip Industry in Germany is one of the largest in the region, aided by its strong industrial infrastructure, current adoption of advanced AI use cases in the automotive industry, development efforts on the data center side, and large investments on the national level in high performance computing and technology sectors relevant to semiconductor manufacturing..

Latin America Server AI Chip Market Insights:

Latin America Server AI Chip have steady high growth due to growing digitalization, rise in cloud computing activities and increasing data center infrastructure in key regions i.e. Brazil and Mexico. Increasing demand for artificial intelligence-integrated applications in sectors like banking and telecom, along with e-commerce is also contributing in market growth. Several factors, including gradual Internet penetration, technology infrastructure investments by foreign firms, and government polices directing electronic modernization, are driving the progressive adoption of advanced AI chip technologies.

Brazil Server AI Chip Market Insights:

The expanding coverage of cloud, increasing investments in data centres, and the demand for AI-based applications alongside the improvements in the digital transformation of a few end-user industries like the banking, telecom, and e-commerce industries are fuelling the growth of the Brazil server AI Chip Industry.

Middle East & Africa Server AI Chip Market Insights:

The Middle East & Africa Server AI Chip Industry is steadily growing by expanding digital infrastructure, data center capacity, and use of cloud computing and AI technologies. Regional transformation is being led through smart city initiatives and government-led digitalization programs in countries including the UAE, Saudi Arabia, and South Africa. Steady but nascent market growth is also backed by increased need for advanced analytics, automation, and high-performance computing in various sectors..

United Arab Emirates (UAE) and Saudi Arabia Server AI Chip Market Insights:

UAE and Saudi Arabia are the two most dominating countries, with UAE on top with relatively more mature data center infrastructure, stronghold on cloud investments and faster uptake of AI powered digital transformation programs such as smart cities and government digital services.

Server AI Chip Market Competitive Landscape:

NVIDIA (Founded 1993) interactive graphic graphics processing unit (GPUs), AI accelerators, and high-performance computing technology. The company is a leader in AI server chips, data center infrastructure, and accelerated computing, powering cloud, generative AI, autonomous systems, and advanced machine learning workloads worldwide.

-

On March 31, 2026, NVIDIA invested USD 2 billion in Marvell Technology to strengthen collaboration in AI infrastructure, focusing on enabling easier deployment of custom AI chips integrated with advanced networking gear and CPUs, highlighting the accelerating competition and ecosystem expansion in AI server chip development.

Intel (Founded 1968) is a global semiconductor company specializing in the design and manufacturing of processors, chipsets, and computing technologies. It plays a key role in data center and AI server infrastructure through its Xeon processor family, enabling high-performance computing, workload orchestration, and scalable solutions for enterprise and cloud-based applications.

-

On March 2026, Intel announced that its Xeon 6 processors will be used as host CPUs to orchestrate NVIDIA’s DGX Rubin NVL8 AI servers, acting as the central control layer for managing GPU coordination, memory, security, and system throughput in large-scale AI data center infrastructure.

Server AI Chip Companies are:

-

NVIDIA

-

Advanced Micro Devices (AMD)

-

Intel

-

Broadcom

-

Marvell Technology

-

Samsung Electronics

-

SK hynix

-

Micron Technology

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

Microsoft

-

Google

-

Meta Platforms

-

Tencent Cloud

-

Baidu

-

Huawei Technologies

-

Cerebras Systems

-

Graphcore

-

Tenstorrent

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 109.90 Billion |

| Market Size by 2035 | USD 1691.31 Billion |

| CAGR | CAGR of 31.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type(GPU-based AI chips, CPU-based AI chips, ASIC-based AI chips and Others) • By Technology(Machine Learning (ML) Chips, Deep Learning Chips, Natural Language Processing (NLP) Chips, Computer Vision Chips and Others) • By Application(Natural Language Processing (NLP), Computer Vision, Robotics & Automation, Recommendation Systems, Predictive Analytics and Others) • By End-User(Data centers, Healthcare, Automotive, Retail and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation; Advanced Micro Devices (AMD); Intel Corporation; Qualcomm Incorporated; Broadcom Inc.; Marvell Technology Group Ltd.; Samsung Electronics Co., Ltd.; SK hynix Inc.; Micron Technology, Inc.; Taiwan Semiconductor Manufacturing Company (TSMC); Amazon Web Services (AWS); Microsoft Corporation; Google LLC (Alphabet Inc.); Meta Platforms, Inc.; Tencent Cloud; Baidu, Inc.; Huawei Technologies Co., Ltd.; Cerebras Systems; Graphcore Ltd.; Tenstorrent Inc. |

Frequently Asked Questions

North America dominated the Server AI Chip Market in 2025.

The “GPU-based AI chips” segment dominated during the projected period.

Rapid growth in AI workloads, expansion of data centers, increasing demand for high-performance computing, cloud adoption, and advancements in GPU/ASIC/TPU architectures are the key drivers of the Server AI Chip Market.

The Market was valued at USD 109.90 Billion in 2025 and is projected to reach USD 1691.31 Billion by 2035.

The Market is expected to grow at a CAGR of 31.44% during 2026–2035.

Get in Touch