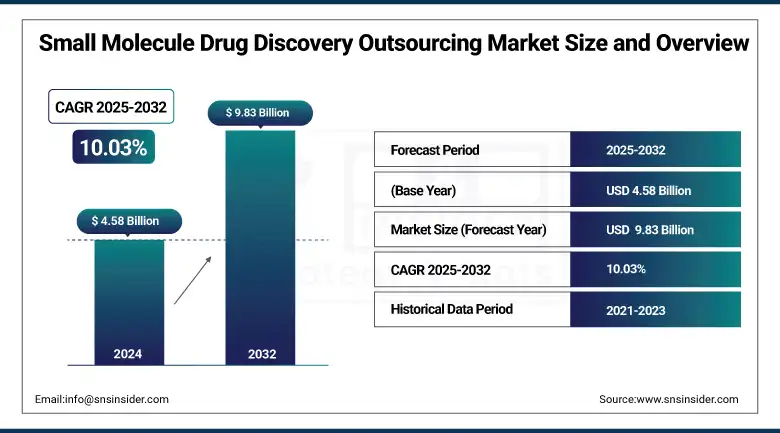

Small Molecule Drug Discovery Outsourcing Market Report Scope & Overview:

The small molecule drug discovery outsourcing market size was valued at USD 4.58 billion in 2024 and is expected to reach USD 9.83 billion by 2032, growing at a CAGR of 10.03% over 2025-2032.

The small molecule drug discovery outsourcing market trends are associated with factors such as the increasing cost of pharmaceutical R&D, sponsors' focus on core competencies, and rising complexities in the drug discovery process. Pharmaceuticals and biotech firms are outsourcing early discovery programs (such as target identification, lead optimization, and preclinical development) more and more to Contract Research Organizations (CROs) to speed development and drugs to market and to enhance cost effectiveness.

In Jan 2024, AION Labs received investment from AstraZeneca, Merck, and Pfizer, and launched AI-driven small molecule discovery startups, including ProPhet (for targeted protein degradation) and TenAces, signifying profound innovation in early-stage outsourcing models.

To Get more information On Small Molecule Drug Discovery Outsourcing Market - Request Free Sample Report

The requirement for outsourcing is reiterated by the transformation to AI applications in virtual screening, predictive modeling, and in silico drug design. Globally, the research and development (R&D) investment in pharmaceuticals exceeded USD 244 billion in 2023, with a significant amount committed to small-molecule research. Also, regulatory easing and faster FDA approvals for therapies based on small molecules (accounting for more than 60% of new drug approvals in 2023) are aiding the small molecule drug discovery outsourcing market. The supply-side capacity is growing very briskly in low-cost markets, such as India and China, and the top CROs are running at 80%-90% capacity utilization, meaning that the industry will always depend on partners for help on discovery.

In September 2023, Merck KGaA expanded its relationship with AI drug discovery player Exscientia, aiming to accelerate pipeline delivery in oncology and immunology, underscoring the increasingly important role of AI in outsourced discovery.

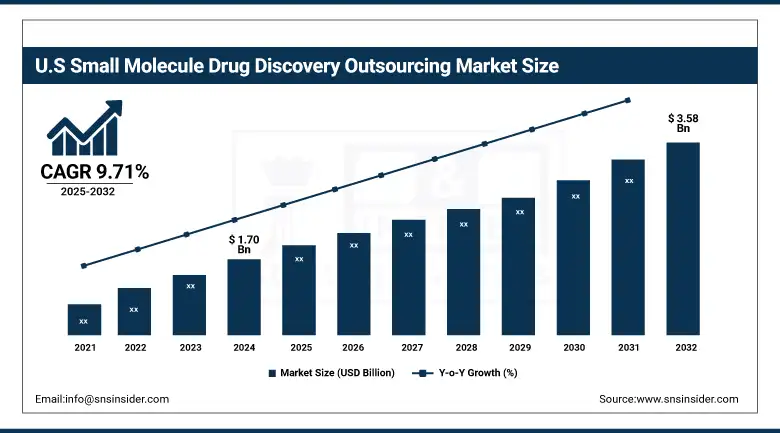

The U.S. small molecule drug discovery outsourcing market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 3.58 billion by 2032, growing at a CAGR of 9.71% over 2025-2032.

The U.S. was the leading country in the North American small molecule drug discovery outsourcing market in 2024, with more than 65% of the regional market share, driven by high discovery project volumes, strong presence of leading CROs, such as Charles River and LabCorp, and significant federal research funding totaling over USD 49 billion by 2023 (NIH). The country's government offers incentives, and biotech alliances are on the rise. Attention to AI-driven discovery, early IND-enabling studies, and regulatory clarity from the FDA are drivers for regional concentration. North America is known to have a significant presence in the precision medicine and oncology discovery of small molecules, and as a result, it has a major share of the industry.

Market Dynamics:

Drivers:

-

Investment Trends, Technological Innovations, Regulatory Backing, and Increasing Demand from Pharmaceutical Companies Propel Market Growth

The small molecule drug discovery outsourcing market growth is driven by the growth in pharmaceutical R&D spending, increasing need for faster results and reduced overheads, and growth in complex pharmaceutical products in the R&D pipeline.

In 2023, global pharma R&D spend is over USD 244 billion and grew by more than 6% of that spend is on small molecule therapeutics. A growing number of pharmaceutical powerhouses are turning to CRO collaborations for cost-efficient drug discovery, particularly in oncology, neurology, and anti-infectives. The trend is driven in large part by the increasing importance of fragment-based drug discovery (FBDD) and structure-based drug design, for which niche CROs can provide extensive expertise.

Moreover, AI-derived tools are also fueling early-stage discovery companies, such as INSILIICO Medicine, which has submitted more than 30 AI-generated preclinical candidates in less than 3 years. On the regulatory front, authorities, such as the U.S. FDA and EMA are proactively promoting the fast-track and/or orphan drug designations of small-molecule-based drugs, which accelerate their translation into clinics. The number of out-licensing transactions is on the rise, including AbbVie’s multi-target discovery deal with HotSpot Therapeutics in 2023, signaling the growing importance of innovation brought into the company from the outside. With sponsors further paring back their internal discovery pipelines to adopt siloed outsourcing models, the market should see a boost from a combination of expanded capacity at CROs and increased investment in discovery-enabling platforms.

Restraints:

-

Quality Concerns, Fragmented Service Ecosystems, and Regulatory Compliance Burdens Hamper the Market Expansion

There are some factors that are challenging the growth of the small molecule drug discovery outsourcing market, such as issues regarding the quality of the information and the protection of the data, which do not meet expectations when the capital is invested. Small biotechs and early-stage pharmaceuticals report difficulties with reproducibility and batch-to-batch variability by collaborating with piecemeal CRO ecosystems. Additionally, the regulatory environment is becoming more complicated, with the U.S. FDA and the EMA both raising the bar for data traceability, bioanalytical validations, and Good Laboratory Practices (GLP), which place a more onerous burden on the sponsor’s compliance obligations. In a 2023 Deloitte poll, 41% of developers said that regulatory synchronization with CROs was a top risk when working with outsourced projects.

Moreover, the partial deployment of AI platforms in mid- and low-tier CROs is posing a bottleneck for tech-enabled discovery with a seamless rollout and it is restraining the full cycle innovation. It is not just the loss of programming time, but the additional pressure of a reduced workforce (in medicinal chemistry and DMPK domains in particular), which has an impact on the delivery schedule. Lastly, increased geopolitical risks and IP-related issues in places including China and Russia are leading sponsors to rethink their outsourcing strategy, with demand moving out of these higher-risk and lower-cost regions into higher-priced yet stable geographies, which may prove a short-term challenge of scalability for the market.

Segmentation Analysis:

By Workflow

By 2024, lead identification & candidate optimization became the leading workflow, which holds around 32% of the overall small molecule drug discovery outsourcing market share due to its significance in the process of converting validated targets into druggable leads. This stage requires time-consuming medicinal chemistry and SAR (Structure–Activity Relationship) studies, the latter of which is outsourced to a greater extent due to resource requirements and in light of the availability of specialized CRO (Contract Research Organization) resources.

The fastest growth workflow segment is targeting validation & functional informatics, propelled by greater incorporation of bioinformatics, CRISPR, and functional genomics platforms. The trend in the more recent AI-driven target analysis and the requirement for mechanistic understanding is driving growth in this early phase position.

By Service

Chemistry services accounted for the largest market share in 2024, and it is also expected to remain the leading services category during the forecast period, driven by high demand for hit-to-lead optimization, synthetic route development, and custom synthesis services. This stranglehold has been reinforced by the degree of medicinal chemistry capabilities available at the leading CROs.

Among the service segments, the DMPK and toxicology screening services (of Others) are expected to grow the fastest as companies consider an early evaluation of ADME properties and safety profiles to avoid any late-stage failures. Mounting regulatory pressure is also driving preliminary toxicological profiling.

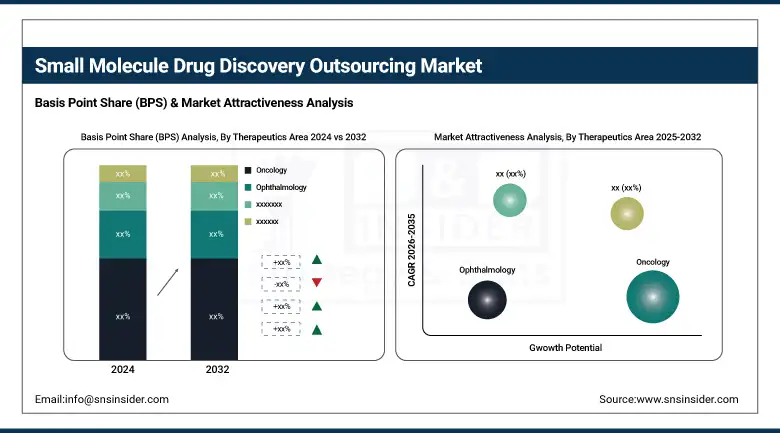

By Therapeutics Area

The therapeutic area segmentation in 2024 oncology dominated, accounting for almost 38% owing to a high number of oncology pipelines and small-molecule-based mechanisms (kinase inhibition and DNA-interacting agents). Increased investment, expedited regulatory roads, and precision-based oncology vehicles also contribute to contracts in this space.

The fastest growing segment is the central nervous system (CNS), centering on the increasing frequency of neurodegenerative diseases and the discovery of small molecules for new CNS receptors and pathways. Approaches, such as BBB-penetrant molecules and neuroinflammation modulators are driving this expansion.

By End-Use

Pharmaceutical & biotechnology companies continued to be the largest end-user segment in 2024, accounting for around 72% of the overall small molecule drug discovery outsourcing market share as they are increasingly outsourcing discovery activities to minimize fixed R&D and shorten development timeframes. Big pharma companies are placing more and more emphasis on long-term discovery partnerships with CROs to improve pipelines.

The academic institutes segment is fastest-growing end-use segment, with government funded research increasingly as well as cross institution research coordinated by CROs. The academic laboratories are actively working with external partners to develop further the translational research from basic discovery through to early preclinical proof of concept.

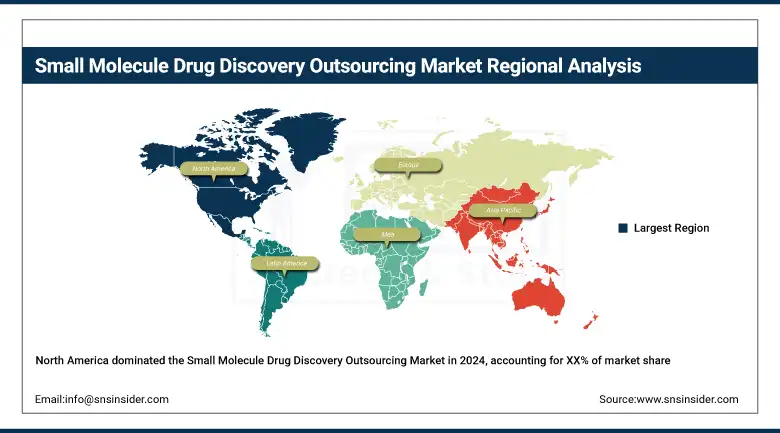

Regional Analysis:

North America led the small molecule drug discovery outsourcing market in 2024 primarily because of its developed infrastructure, leading pharmaceutical companies, and steady expansion of R&D spending.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe accounted for the second-largest share in the small molecule drug discovery outsourcing market in 2024, due to regulatory harmonization (EMA), academic-industry partnerships, and growing biopharma investments. Germany has been the biggest driver, benefiting from strong government support and public-private partnership, but the U.K. was a fast-catcher post-Brexit, owing to the initiatives to encourage CRO working and AI-powered drug discovery. European CROs enhance fragment-based discovery and DMPK profiling with new capabilities. The continent also experienced growth in oncology and rare disease research initiatives, especially in France and Spain. Not only does Europe hold a strong supply (CRO capacity) but also demand, particularly in therapeutic innovation and early-stage clinical trials, contributing to the growth of the overall small molecule drug discovery outsourcing market.

Asia Pacific is the fastest-growing region in the small molecule drug discovery outsourcing market due to the cost-effective CRO services, increasing biotech presence, and strategic government initiatives to support pharmaceutical R&D. The Chinese market is the largest regional market, contributing to more than 45% of the APAC share, tapped by firms WuXi AppTec and Pharmaron, which have expanded their medicinal chemistry, biology, and IND-enabling studies operations. India is growing the fastest on the back of its robust chemistry service experience, substantial skilled talent base, and growing number of FDA/EMA qualified facilities. Both nations are seeing ample VC in discovery-stage biotech. Japan and South Korea are also adopting AI-enabled discovery pipelines. Increasing prevalence of diseases, competitive cost-effectiveness, and regulatory harmonization with ICH guidelines drive the small molecule drug discovery outsourcing market in APAC.

Key Players:

Prominent small molecule drug discovery outsourcing companies operating in the market include WuXi AppTec, Pharmaceutical Product Development LLC (PPD), Charles River Laboratories, Laboratory Corporation of America Holdings (Covance), Eurofins Scientific, Evotec SE, Curia (Albany Molecular Research Inc.), GenScript Biotech, Pharmaron Beijing Co., Ltd., Syngene International Ltd., Dalton Pharma Services, Oncodesign Services, Jubilant Biosys Ltd., Domainex Ltd., Merck & Co., Inc., QIAGEN N.V., Dr. Reddy’s Laboratories Ltd., TCG Lifesciences Pvt. Ltd., Aurigene Pharmaceutical Services, and Medpace Inc.

Recent Developments:

In June 2025, AstraZeneca announced a strategic collaboration with China’s CSPC Pharmaceuticals, involving a USD 110 million upfront investment and a potential USD 5.2 billion total deal. The partnership focuses on applying CSPC's AI-driven discovery platform to small-molecule therapeutics for chronic and immunological diseases.

In May 2025, Novo Nordisk entered a collaboration and licensing agreement with U.S. biotech Septerna, investing over USD 200 million upfront and a deal value of up to USD 2.2 billion. The pact targets the development of oral small-molecule treatments for obesity, diabetes, and cardiometabolic diseases.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.58 billion |

| Market Size by 2032 | USD 9.83 billion |

| CAGR | CAGR of 10.03% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Workflow (Target Identification & Screening, Target Validation & Functional Informatics, Lead Identification & Candidate Optimization, Preclinical Development, Others [Hit-to-Lead Studies, In Silico Modeling / Computational Drug Design]) • By Service (Chemistry Services, Biology Services, Others [DMPK Services, Toxicology Screening Services]) • By Therapeutics Area (Respiratory System, Pain and Anesthesia, Oncology, Ophthalmology, Hematology, Cardiovascular, Endocrine, Gastrointestinal, Immunomodulation, Anti-infective, Central Nervous System, Dermatology, Genitourinary System, Others [Rare/Orphan Diseases, Autoimmune Disorders, Metabolic Disorders]) • By End Use (Pharmaceutical & Biotechnology Companies, Academic Institutes, Others [Contract Research Organizations (CROs), Research Institutions, Non-Profit Research Foundations]) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | WuXi AppTec, Pharmaceutical Product Development LLC (PPD), Charles River Laboratories, Laboratory Corporation of America Holdings (Covance), Eurofins Scientific, Evotec SE, Curia (Albany Molecular Research Inc.), GenScript Biotech, Pharmaron Beijing Co., Ltd., Syngene International Ltd., Dalton Pharma Services, Oncodesign Services, Jubilant Biosys Ltd., Domainex Ltd., Merck & Co., Inc., QIAGEN N.V., Dr. Reddy’s Laboratories Ltd., TCG Lifesciences Pvt. Ltd., Aurigene Pharmaceutical Services, and Medpace Inc. |

Frequently Asked Questions

Technologies such as AI, machine learning, and cloud-based platforms are enabling faster hit identification, predictive modeling, and improved success rates. These advancements are shortening discovery timelines and increasing the attractiveness of outsourcing early drug development stages.

North America is the dominant region due to the presence of global CROs and pharma giants. However, Asia Pacific—led by China and India—is the fastest-growing region, driven by cost-effective services, skilled labor, and expanding R&D capabilities.

Oncology leads the market, accounting for the highest share due to the extensive number of pipeline programs and high R&D investments. CNS and immunology are also rapidly growing therapeutic areas, particularly in AI-driven small molecule discovery.

Chemistry services—especially medicinal chemistry, custom synthesis, and lead optimization—hold the largest market share, while DMPK and toxicology screening services are witnessing the fastest growth due to rising emphasis on early safety profiling and regulatory compliance.

The market is driven by rising pharmaceutical R&D costs, growing complexity of early-stage drug discovery, rapid adoption of AI and computational modeling, increasing demand for faster time-to-market, and cost-efficiencies offered by outsourcing to CROs in Asia-Pacific and Eastern Europe.

Get in Touch