Slide Stainer Market Report Scope & Overview:

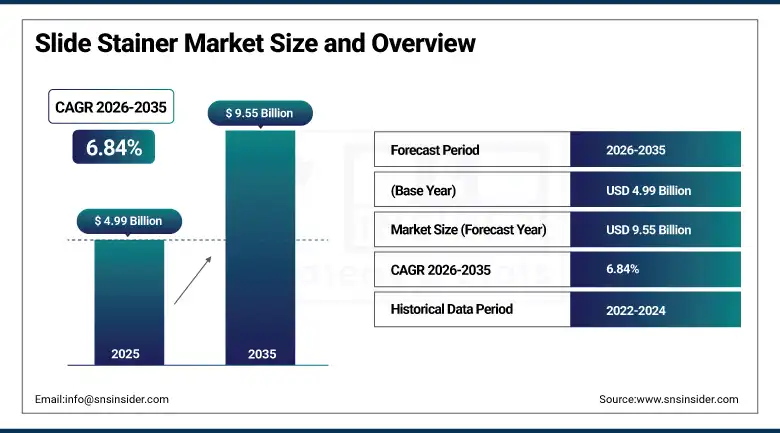

The Slide Stainer Market was valued at USD 4.99 Billion in 2025 and is expected to reach USD 9.55 Billion by 2035, growing at a CAGR of 6.84% from 2026–2035.

Slide stainers are laboratory instruments that apply chemical dyes and staining solutions to histological tissue sections and cytological preparations mounted on glass microscope slides, rendering the biological structures, cellular components, and molecular targets visible under light microscopy with the contrast and specificity that morphological assessment and biomarker detection in clinical pathology and research microscopy require. The commercial significance of slide staining technology rests on its foundational position in the diagnostic pathology workflow, where tissue staining is the non-negotiable prerequisite for every histological diagnosis across surgical pathology, cancer grading, and infectious disease tissue diagnosis whose clinical management decisions depend on the morphological and molecular information that stained tissue sections reveal to pathologists.

In January 2025, Roche Diagnostics gained U.S. FDA clearance for its VENTANA DP 600 high-volume slide scanner as part of its Roche Digital Pathology Dx system, a 240-slide stainer that enhances diagnostic speed and image quality while expanding Roche's digital pathology portfolio and strengthening its position in advanced cancer diagnostics. The clearance reflected the progressive integration of slide staining with digital pathology image capture and AI-powered analysis whose workflow combination creates a continuous tissue preparation-to-diagnosis workflow that improves pathology laboratory throughput, diagnostic consistency, and remote consultation capability beyond what conventional slide staining with manual microscopy review provides.

Market Size and Forecast

-

Market Size in 2026E: USD 5.33 Billion

-

Market Size by 2035: USD 9.55 Billion

-

CAGR: 6.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Slide Stainer Market - Request Free Sample Report

Slide Stainer Market Trends

-

Automated slide stainers are increasingly replacing manual staining methods to improve laboratory efficiency, consistency, and throughput.

-

Integration of digital pathology and AI-powered image analysis is enabling more streamlined and data-driven diagnostic workflows.

-

Rising adoption of immunohistochemistry (IHC) staining is supporting precision oncology and companion diagnostic testing applications.

-

Demand for eco-friendly, low-toxicity staining reagents is growing due to environmental and laboratory safety requirements.

-

Compact and point-of-care slide stainers are expanding access to advanced pathology diagnostics in smaller laboratories and emerging markets.

The U.S. Slide Stainer Market Outlook

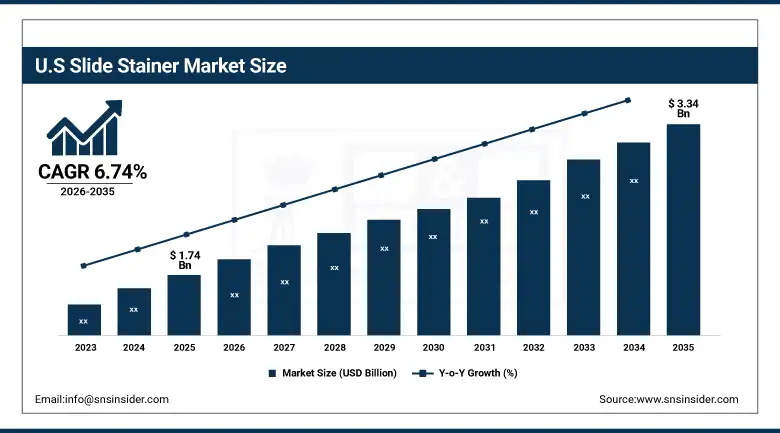

The U.S. Slide Stainer Market was valued at approximately USD 1.74 Billion in 2025 and is expected to reach approximately USD 3.34 Billion by 2035, growing at a CAGR of approximately 6.74%. North America dominated the slide stainer market in 2023, driven by the world's most extensive clinical pathology infrastructure, high cancer diagnosis rates creating large histopathology testing volumes, and government initiatives including NIH cancer research funding that sustains advanced diagnostic technology investment.

The United States slide stainer market is driven by the combination of high cancer incidence creating large surgical pathology tissue processing volumes. The expanding companion diagnostic IHC testing requirement of precision oncology practice, and the regulatory environment whose College of American Pathologists laboratory accreditation standards for staining reagent validation, quality control, and result documentation create compliance-driven investment in automated staining platforms whose process control and documentation capabilities exceed what manual staining can provide. The U.S. pathology laboratory consolidation trend, where independent reference laboratories and hospital laboratory outreach programmes are progressively consolidating surgical pathology volume into large high-throughput facilities. This creates commercial conditions that favour high-capacity automated staining platform investment whose economies of scale improve with throughput concentration.

In October 2023, Biocare Medical announced a partnership with EmeritusDX, a CAP-accredited and CLIA-certified laboratory, to integrate its IntelliPATH FLX Automated Slide Stainer into the laboratory's IHC diagnostic workflow. The integration optimised staining speed and precision while supporting Biocare's broad IHC antibody and detection kit menu, demonstrating the growing commercial importance of automated staining platform and reagent ecosystem co-development partnerships whose combined value proposition for clinical laboratory customers creates purchasing decision alignment between instrument and consumable selection.

Slide Stainer Market Segment Analysis

-

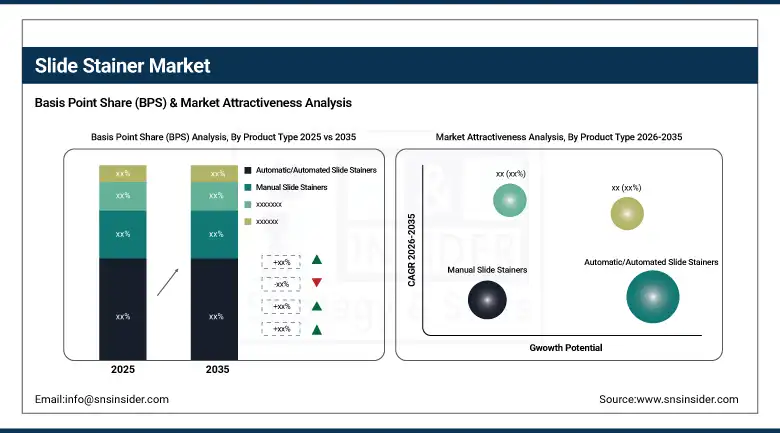

By Product Type, automated slide stainers segment dominated the slide stainer market with approximately 52.4% share in 2025, while the automated slide stainers segment is also the fastest growing segment.

-

By Technique, hematoxylin & eosin staining segment dominated the slide stainer market in 2025, while the immunohistochemistry segment is the fastest growing technique driven by companion diagnostic testing expansion and precision oncology biomarker assessment demand.

-

By Component, reagents & kits segment dominates through its recurring consumable procurement model, while the instruments segment represents the foundational capital equipment whose automation capability drives laboratory productivity improvement.

-

By End User, hospitals & diagnostics laboratories segment dominated the slide stainer market with approximately 34% share in 2025, while research laboratories are growing as oncology, pathology, and biomarker research programmes expand histological analysis requirements.

By Product Type, automated stainers dominate, semi-automatic serves mid-volume

Automated slide stainers retained the dominant product type position with approximately 52.4% of the slide stainer market in 2025. Their commercial primacy reflects the compelling operational economics of automated staining in high-volume clinical pathology settings where manual staining's labour intensity, throughput limitation, reagent consistency variability, and documentation burden create operational and quality disadvantages that automated platforms systematically address. Automated staining platforms including Leica Biosystems' BOND RX and ST5010, Dako (Agilent) OMNIS and PT Link, Roche Ventana Discovery Ultra and ULTRA, and Sakura Tissue-Tek SMART series. These provide programmable staining protocol management, closed-loop reagent dispensing, temperature-controlled incubation, and automated slide transport whose integration creates reproducible staining outcomes across the full volume of clinical slides that busy pathology departments process daily.

By End User, hospitals & diagnostic laboratories dominate, research grows

Hospitals and diagnostic laboratories retained the dominant end user position with approximately 34% of the slide stainer market in 2025. Their commercial leadership reflects the concentration of surgical pathology specimen processing, clinical cytology preparation, and diagnostic IHC testing in hospital-based and reference laboratory pathology departments whose tissue processing volumes create the highest per-facility slide staining demand of any end user category. The progressive consolidation of surgical pathology services into large reference laboratories and hospital outreach laboratory programmes creates commercial conditions that favor automated staining platform investment whose throughput capacity and consistency advantages improve with increasing slide volume concentration at fewer, larger facilities.

Research laboratories are growing as oncology, translational pathology, and biomarker research programmes whose tissue-based analysis requirements extend well beyond routine H&E morphology into multiplexed IHC, spatial transcriptomic preparation, and novel biomarker staining whose experimental diversity creates demand for flexible staining platform capability that research-grade automated stainers with open-protocol programming capability provide above what clinically validated fixed-protocol instruments offer.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Slide Stainer Market Insights

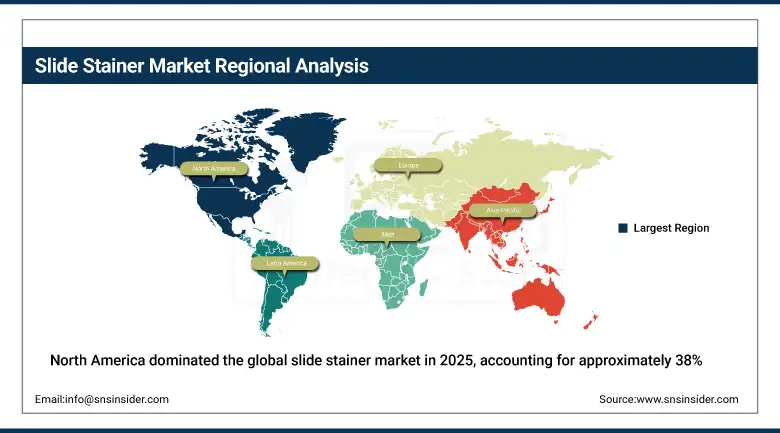

North America dominated the global slide stainer market in 2025, accounting for approximately 38% of the total market share. This is driven by the world's most extensive clinical pathology infrastructure, the highest cancer diagnosis rates among major economies, and the largest companion diagnostic IHC testing programme. The United States accounts for approximately 82.5% of North American revenues through its large surgical pathology volume, the commercial concentration of major slide stainer manufacturers including Leica Biosystems, Sakura Finetek, and Thermo Fisher Scientific whose North American headquarters sustain regional market development, and the NIH-funded cancer research infrastructure whose tissue analysis requirements create consistent academic research laboratory staining platform procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Slide Stainer Market Insights

Europe held a significant share of the global slide stainer market in 2025. Germany, France, the United Kingdom, Italy, and Spain are the leading national markets whose universal healthcare cancer care programmes, advanced histopathology services, and academic pathology research infrastructure create consistent diagnostic and research staining demand. Germany accounts for approximately 28.5% of European revenues through its large clinical pathology infrastructure, the commercial presence of Leica Biosystems (Danaher) whose Nussloch headquarters sustains a major European slide stainer manufacturing and development base, and the comprehensive university hospital research programme whose translational pathology research creates premium instrument procurement.

The United Kingdom's NHS pathology network, France's large hospital sector, and the academic oncology research programmes of German and Swiss universities each create consistent slide stainer demand. The European Companion Diagnostics programme expansion under EMA regulatory framework is progressively mandating IHC biomarker testing whose validated automated staining platform requirements create growing IHC instrument procurement across European oncology centres.

Asia Pacific Slide Stainer Market Insights

Asia Pacific is the fastest-growing regional slide stainer market, driven by expanding healthcare infrastructure investment, growing cancer diagnosis rates as lifestyle and dietary changes increase cancer incidence across the region's rapidly urbanizing populations, and the progressive automation of clinical pathology workflows whose efficiency improvement imperative is creating systematic manual-to-automated staining transition. China accounts for approximately 38.5% of Asia Pacific revenues through its rapidly expanding hospital network, the growing pathology service quality investment driven by medical reform programmes, and the government's cancer prevention and early detection initiatives whose tissue diagnostic infrastructure investment includes automated staining platform procurement.

Japan and South Korea contribute premium regional demand through their advanced pathology infrastructure, high automated staining penetration in hospital pathology departments, and the growing companion diagnostic IHC testing programmes of their oncology care systems. India and Southeast Asian markets are growing rapidly as pathology laboratory modernization, increasing cancer diagnosis volumes, and growing healthcare quality investment create systematic progression from manual to automated staining workflows.

MEA & Latin America Slide Stainer Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its world-class hospital infrastructure, the advanced diagnostic pathology services at major Dubai and Abu Dhabi teaching hospitals, and the government's healthcare quality improvement programme whose diagnostic technology investment includes automated histopathology equipment. Saudi Arabia's hospital expansion and growing oncology programme create increasing slide stainer demand.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its large public and private hospital pathology infrastructure, the growing cancer diagnosis volumes whose tissue specimen processing creates large automated staining demand, and the expanding research laboratory network at institutions including FMUSP and UNIFESP whose oncology research programmes create academic slide stainer procurement.

Market Dynamics

Growth Drivers: Rising global cancer incidence driving histopathology testing volumes and companion diagnostic IHC automation requirements creating systematic adoption of automated slide staining platforms

The slide stainer market's growth is structurally driven by the rising global cancer burden, whose WHO projection of 29.9 million new cancer cases annually by 2040 creates proportionally growing surgical pathology specimen volumes that automated staining platforms must process, and the precision oncology revolution's companion diagnostic IHC testing requirements that create mandatory automated staining adoption in oncology pathology departments. Each new cancer patient diagnosed requires histological tissue confirmation and grading whose H&E staining is the foundational diagnostic procedure, and each cancer patient managed with targeted therapy requires companion diagnostic IHC biomarker assessment whose validated automated staining platform requirement progressively converts pathology departments to automated IHC staining infrastructure.

Restraints: High capital cost of advanced automated slide staining platforms and reagent exclusivity creating total cost of ownership barriers for smaller clinical laboratories

Advanced automated immunohistochemistry staining platforms from leading manufacturers including Leica Biosystems BOND series, Roche Ventana ULTRA, and Agilent OMNIS each represent capital investments of USD 100,000 to USD 400,000 per system whose procurement justification requires annual slide volume validation that smaller laboratories and hospitals whose pathology departments process below threshold throughput cannot achieve economically. The reagent exclusivity arrangements between automated IHC platform manufacturers and their proprietary antibody and detection kit ecosystems create ongoing consumable procurement commitments at above-generic-market pricing that compounds the capital cost of platform adoption into a total cost of ownership calculation that constrains adoption at cost-sensitive laboratories in both developed and developing healthcare markets.

Opportunities: Digital pathology integration creating connected staining-to-imaging workflows and emerging market laboratory automation representing the highest-growth commercial frontiers

The integration of automated slide staining with whole slide imaging and AI-powered pathological analysis creates a connected tissue preparation-to-diagnosis workflow whose combined capability substantially exceeds the sum of individual technology component values. Each laboratory that deploys integrated automated staining and digital pathology infrastructure creates a tissue analysis workflow whose slide throughput, diagnostic consistency, remote consultation capability, and AI-assisted pattern recognition collectively deliver operational and clinical quality improvements that sustain investment in premium platform procurement. Emerging market clinical laboratory automation investment, where rapidly growing hospital networks in China, India, Brazil, and Southeast Asia are systematically transitioning from manual to automated pathology laboratory workflows, creates a large and rapidly expanding market for automated slide staining platforms.

Recent Developments:

-

2025: Roche Diagnostics received FDA clearance for the VENTANA DP 600 high-volume slide scanner integrating with the Digital Pathology Dx system, combining automated slide staining with high-throughput digital image capture to create a connected tissue preparation-to-digital-diagnosis workflow enhancing pathology laboratory throughput and diagnostic quality.

-

2023: Biocare Medical partnered with EmeritusDX laboratory to integrate its IntelliPATH FLX Automated Slide Stainer into a CAP-accredited IHC diagnostic workflow, optimising staining speed and precision while demonstrating the commercial value of automated platform and reagent ecosystem co-development partnerships.

-

2023: Leica Biosystems launched its BOND Prime automated IHC staining platform incorporating continuous specimen loading for uninterrupted staining workflow, enabling 24-hour automated IHC staining operation that substantially increases throughput compared to batch-processed platform predecessors serving high-volume oncology pathology programmes.

Slide Stainer Market Key Players are:

-

F. Hoffmann-La Roche Ltd.

-

Danaher Corporation (Leica Biosystems)

-

Agilent Technologies, Inc.

-

Thermo Fisher Scientific Inc.

-

Sakura Finetek Japan Co., Ltd.

-

Merck KGaA

-

BioGenex Laboratories, Inc.

-

General Data Healthcare, Inc.

-

ELITechGroup

-

Biocare Medical, LLC

-

CellPath Ltd.

-

A. Menarini Diagnostics S.r.l.

-

StatLab Medical Products, Inc.

-

Histo-Line Laboratories S.r.l.

-

SLEE Medical GmbH

-

MEDITE Medical GmbH

-

Diapath S.p.A.

-

Amos Scientific Pty Ltd.

-

Dakewe (Shenzhen) Medical Equipment Co., Ltd.

-

Intelsint S.r.l.

Slide Stainer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.99 Billion |

| Market Size by 2035 | USD 9.55 Billion |

| CAGR | CAGR of 6.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Manual Slide Stainers, Semi-Automatic Slide Stainers, Automatic/Automated Slide Stainers) • By Technique (Hematoxylin & Eosin Staining, Immunohistochemistry, Special Staining, Cytology Staining, Others) • By Component (Instruments, Reagents & Kits, Others) • By End User (Hospitals & Diagnostics Laboratories, Research Laboratories, Pharmaceutical & Biotechnology Companies, Academic Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F. Hoffmann-La Roche Ltd., Danaher Corporation (Leica Biosystems), Agilent Technologies, Inc., Thermo Fisher Scientific Inc., Sakura Finetek Japan Co., Ltd., Merck KGaA, BioGenex Laboratories, Inc., General Data Healthcare, Inc., ELITechGroup, Biocare Medical, LLC, CellPath Ltd., A. Menarini Diagnostics S.r.l., StatLab Medical Products, Inc., Histo-Line Laboratories S.r.l., SLEE Medical GmbH, MEDITE Medical GmbH, Diapath S.p.A., Amos Scientific Pty Ltd., Dakewe (Shenzhen) Medical Equipment Co., Ltd., and Intelsint S.r.l. |

Frequently Asked Questions

The Slide Stainer Market is expected to grow at a CAGR of 6.84% from 2026 to 2035.

The Slide Stainer Market was valued at USD 4.99 Billion in 2025.

Rising cancer incidence, increasing demand for histopathology and companion diagnostic testing, growing adoption of automated pathology workflows, expanding digital pathology integration are driving the Slide Stainer Market.

The Automated Slide Stainers segment dominated the Slide Stainer Market with approximately 52.4% share in 2025 through its superior throughput, consistency, and documentation capabilities for high-volume clinical pathology operations.

North America dominated the Slide Stainer Market in 2025, with the United States accounting for approximately 82.5% of North American revenues.

Get in Touch