Smart Connected Assets and Operations Market Analysis & Overview:

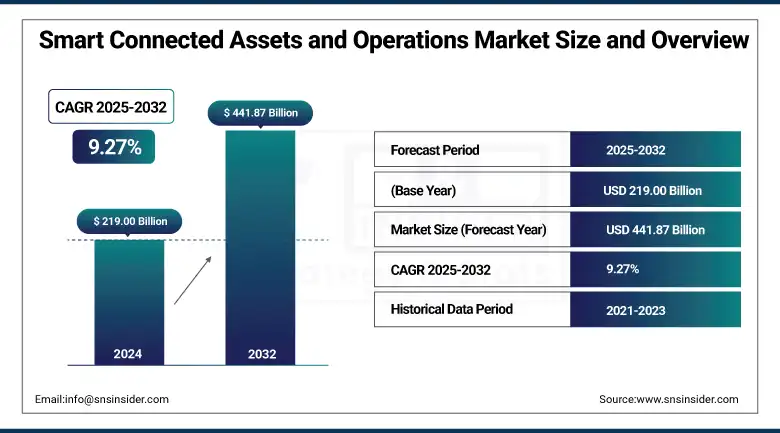

Smart Connected Assets and Operations Market was valued at USD 219.00 billion in 2024 and is expected to reach USD 441.87 billion by 2032, growing at a CAGR of 9.27% from 2025-2032.

The Smart Connected Assets and Operations Market is growing as a result of the increasing adoption of IoT technology, the increasing demand for real-time asset monitoring; increased operational efficiency, and predictive maintenance. The digital transformation taking place in diverse industries and the inherent need for diminished downtime and reduced operational costs are also fueling the market.

To Get more information On Smart Connected Assets and Operations Market - Request Free Sample Report

Implementing predictive maintenance can lead to up to 12% savings over scheduled repairs, reduce maintenance costs by 30%, and eliminate breakdowns by 70%.

Industrial Internet of Things (IIoT) technologies have helped industrial companies reduce downtime by up to 20% and maintenance costs by around 25-30% through predictive maintenance and real-time monitoring.

Furthermore, Siemens reports that IoT-based asset management can improve operational efficiency by up to 30% and reduce unplanned downtime by up to 50% in manufacturing plants using their MindSphere IoT platform.

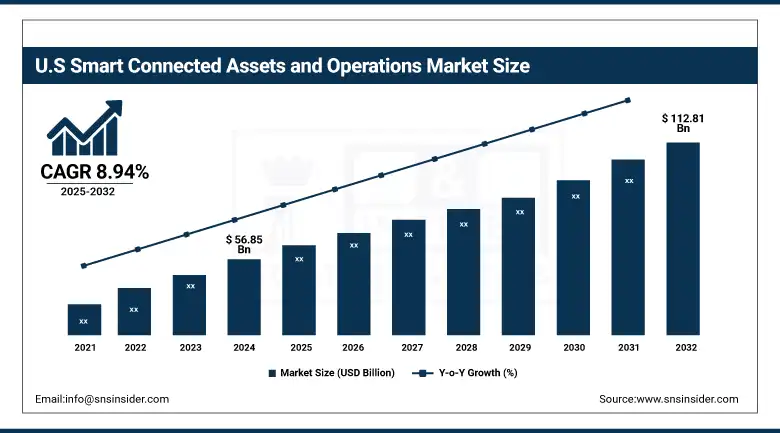

U.S. Smart Connected Assets and Operations Market was valued at USD 56.85 billion in 2024 and is expected to reach USD 112.81 billion by 2032, growing at a CAGR of 8.94% from 2025-2032.

The factors driving U.S. market growth include widespread adoption of IoT, increased investment in smart infrastructure, rising demand for asset management in real-time, and a focus on improving operational efficiency and reducing maintenance costs within the manufacturing, logistics, and energy industries.

The U.S. government has recognized the potential of IoT technologies, with the DIGIT Act emphasizing IoT's role in generating new economic activity across various sectors, including transportation, energy, agriculture, manufacturing, and healthcare.

Additionally, the U.S. Department of Transportation announced $54 million in grant awards for 34 projects across 22 states, focusing on advanced smart community technologies to improve transportation efficiency and safety.

Smart Connected Assets and Operations Market Dynamics

Drivers

-

Widespread adoption of IoT and AI technologies in industrial ecosystems boosts demand for smart connected assets and operations platforms.

IoT and AI are changing industrial asset management by using smart sensors and predictive analytics, along with real-time monitoring, in order to minimize downtime and better productivity in operations and logistics. IoT and AI allow for cloud computing as well as edge intelligence to increase connectivity and automation to support smart predictions and real-time decision-making. With these technologies to optimize resource utilization, businesses can future-proof their operations and reduce costs. As a result, there is an accelerating demand for smart connected assets across industries.

According to the U.S. Department of Energy, implementing predictive maintenance can deliver a 35% to 45% reduction in equipment downtime, highlighting the substantial impact of these technologies on operational efficiency.

Siemens' MindSphere platform leverages AI and IoT to optimize maintenance efficiency, enabling companies to transform data into productive business insights and reduce unplanned downtime.

Meanwhile, GE Vernova’s Asset Performance Management (APM) software has shown measurable outcomes, with customers like Navigator achieving 7.2% cost savings in just 90 days and projecting a 12.8% annual reduction in maintenance costs.

Restraints

-

Data security risks and concerns about system vulnerabilities limit confidence in adopting connected assets and operations platforms at scale.

The growing use of connected devices and cloud systems increases the cyber threat surface area, creating concerns about unauthorized access, breaches of data, and manipulation of systems. This is particularly concerning in the energy, manufacturing, and transport sectors as disruptions can have serious implications. Compliance with data protection and security requires significant investments. Organizations are hesitant to routinely adopt smart connected technologies without firm, guaranteed protections in place as cyber threats continue to evolve.

In 2024, ransomware remained the most significant cyber threat to U.S. critical infrastructure, with complaints to the FBI's Internet Crime Complaint Center (IC3) increasing by 9% from 2023. The IC3 also received 859,532 cybercrime complaints in the same year, with reported losses surpassing USD 16.6 billion marking a 33% rise over the previous year.

Further amplifying concern, a whitepaper by Palo Alto Networks and Siemens revealed that approximately 62% of exploit triggers in operational technology (OT) networks stemmed from vulnerabilities that were 6 to 10 years old, underscoring the dangers posed by aging systems in industrial environments.

Opportunities

-

Expanding role of edge computing and 5G connectivity unlocks new capabilities for real-time monitoring and responsive asset management.

With the combination of edge computing and 5G networks, ultra-low latency, faster data processing, and scalable connectivity options are now available to smart systems. This will allow for near-real-time insight and responsiveness for critical assets in autonomous transport, oil and gas, smart utilities, etc. 5G can accommodate even more devices with the same performance by allowing connections from each device that use low, and potentially, no latency. This has significantly transformed the market for hyper-connected devices enabling vendors, integrators, and industries, to all see growth opportunities in hyper-connected freedom and intelligence.

According to Intel, 67% of manufacturers cited improving employee productivity as the top motivating factor for adopting edge AI, with nearly half aiming to reduce operational costs. For instance, at Audi's Neckarsulm plant in Germany, edge computing enhanced weld inspections by 100 times with a latency of 18 milliseconds, and reduced labor costs by 30% to 50%.

Challenges

-

Lack of standardization across platforms and protocols impedes seamless integration and slows progress toward fully interoperable smart operations.

Despite rapid progress, the smart connected assets remain fragmented with competing platforms, protocols, and data standards. This lack of uniformity creates major integration challenges, particularly for companies with diverse or global assets, hindering data consolidation, workflow automation, and scalability. Without universal frameworks, implementation costs rise, and dependence on vendor-specific solutions limits flexibility and upgrades. Until industry-wide standards are established, achieving interoperable, scalable connected operations will continue to be a costly, persistent challenge.

Smart Connected Assets and Operations Market Segment Analysis

By Industry

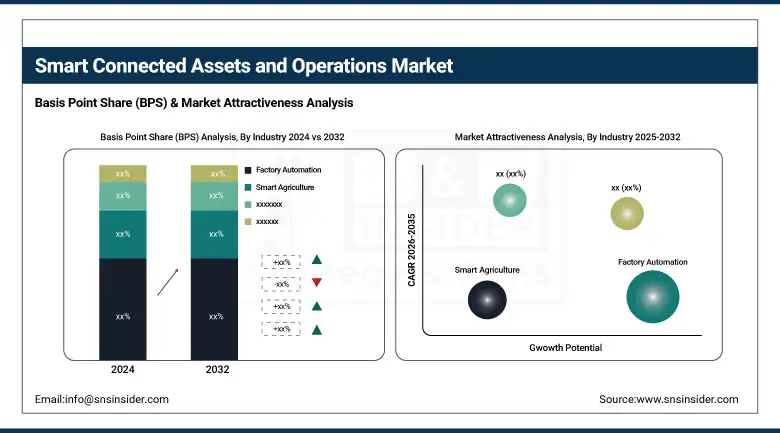

Factory automation led the Smart Connected Assets and Operations Market in 2024 with a 31% revenue share because of widespread implementations of industrial IoT, robotics, and real-time monitoring solutions, contributing to operational efficiency, reducing unproductive downtime, and proactive maintenance - all must-haves in manufacturing. The demand for ultra-flexible, automated, and scalable production environments has led to high factory automation solution adoption rates.

Smart agriculture is projected to grow at the fastest CAGR of 11.53% from 2025 to 2032, with food demand rising globally, shortages of labor, and advancements pushing for sustainable farming practices. The integration of IoT devices, drones, and analytics provides increased yield forecast accuracy, soil monitoring, and resource optimization, making connected devices more critical in modernizing agricultural activities and improving food productivity overall.

By Module

The hardware segment held the largest revenue share of 46% in 2024, primarily due to the extensive use of sensors, controllers, and edge devices that are crucial for enabling connected operations. These physical components are the backbone of smart infrastructure, allowing for real-time data collection and asset management, which are essential for driving IoT-based automation across various industries.

The APM (Asset Performance Management) software and platform segment is expected to grow at a CAGR of 10.57% from 2025 to 2032, driven by an increasing need for predictive analytics, maintenance optimization, and operational insights. These platforms empower businesses to minimize equipment failures, prolong asset lifespan, and enhance overall efficiency through data-driven decision-making, making them more essential in today’s smart industrial ecosystems.

Smart Connected Assets and Operations Market Regional Outlook

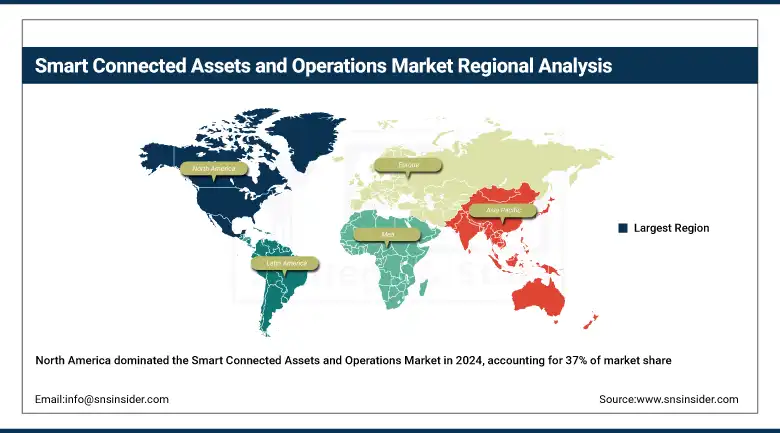

North America accounted for the highest revenue share of 37% in 2024, due to the early embrace of Industry 4.0 technologies, a solid digital infrastructure, and hefty investments in smart manufacturing and industrial IoT. The U.S. and Canada are at the forefront of automation efforts and research and development, backed by a well-established network of technology providers. This strong foundation cements the region's position as a leader in deploying connected assets and optimizing smart operations.

Get Customized Report as per Your Business Requirement - Enquiry Now

The U.S. dominated the Smart Connected Assets and Operations Market due to strong industrial digitization, advanced infrastructure, and early adoption of IoT technologies.

Asia Pacific is projected to grow at the fastest CAGR of 10.94% from 2025 to 2032, driven by swift industrialization, the rise of smart city projects, and increasing investments in digital transformation across countries. Government backing for automation, a growing need for operational efficiency, and the integration of IoT in manufacturing and agriculture are all contributing to the rapid expansion of smart connected assets and operations in this region.

China is dominating the Smart Connected Assets and Operations Market in Asia Pacific due to large-scale industrial automation, government support, and rapid IoT technology adoption.

Europe holds a significant position in the Smart Connected Assets and Operations Market, driven by strong regulatory support for digital transformation, widespread adoption of automation technologies, and growing investments in sustainable industrial practices across major economies like Germany and France.

Germany is dominating the Smart Connected Assets and Operations Market in Europe due to its advanced manufacturing sector, strong automation focus, and Industry 4.0 leadership.

In the Smart Connected Assets and Operations Market, the Middle East & Africa and Latin America are experiencing steady growth driven by infrastructure modernization, smart city initiatives, and increasing investments in automation across energy, mining, and manufacturing sectors.

Key Players

IBM Corporation, General Electric (GE), Siemens AG, Schneider Electric, Rockwell Automation, Inc., Honeywell International Inc., ABB Ltd., Cisco Systems, Inc., PTC Inc., SAP SE and others.

Recent Developments:

-

In June 2024, Honeywell launched Connected Power, enabling buildings to monitor and control plug-level energy usage, reducing waste and enhancing safety.

-

In January 2024, Honeywell and NXP Semiconductors announced a collaboration to integrate AI-enabled processors into building management systems, enhancing energy efficiency and autonomy.

-

In 2024, SAP expanded Joule's capabilities with collaborative AI agents, automating complex business workflows and enhancing productivity across financial and dispute management tasks.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 219.00 Billion |

| Market Size by 2032 | USD 441.87 Billion |

| CAGR | CAGR of 9.27% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Module(Hardware, APM software & platform, Service) • By Industry(Automotive & Transportation, Energy & Power, Healthcare, Smart Agriculture, Factory Automation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | IBM Corporation, General Electric (GE), Siemens AG, Schneider Electric, Rockwell Automation, Inc., Honeywell International Inc., ABB Ltd., Cisco Systems, Inc., PTC Inc., SAP SE |

Frequently Asked Questions

North America dominated with a 37% revenue share in 2024, driven by early Industry 4.0 adoption and strong digital infrastructure in the U.S. and Canada.

Factory automation led with a 31% revenue share in 2024 due to heavy integration of IoT, robotics, and predictive maintenance in manufacturing.

Growth is driven by IoT adoption, real-time asset monitoring, predictive maintenance, and demand for operational efficiency across industrial sectors.

The market was valued at USD 219.00 billion in 2024, reflecting strong global momentum toward industrial digitization and automation.

The market is projected to grow at a CAGR of 9.27% from 2025 to 2032, reaching USD 441.87 billion by 2032.

Get in Touch