Specialty Tapes Market Analysis & Overview:

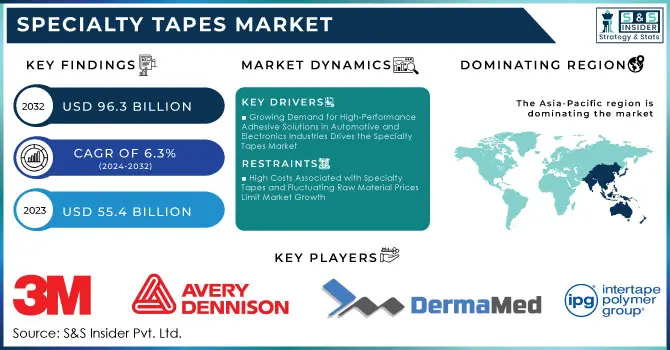

Specialty Tapes Market was valued at USD 62.60 billion in 2025 and is expected to reach USD 115.32 billion by 2035, growing at a CAGR of 6.3% from 2026-2035.

The Specialty Tapes Market around the world is experiencing considerable growth because of rising demand in automotive, electronics, packaging, and construction sectors. The rise in use of innovative adhesive systems, such as double-sided and high-end tapes, enables light weight, strength, and efficiency. Moreover, increasing industrial automation, application in the medical sector, and need for bonding products in manufacturing operations are other factors driving the growth of this market.

Get More Information on Specialty Tapes Market - Request Sample Report

Specialty Tapes Market Size and Forecast

- Market Size in 2025: USD 62.60 Billion

- Market Size by 2035: USD 115.32 Billion

- CAGR: 6.3% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2022–2024

Specialty Tapes Market Trends

- Rising demand for advanced bonding, insulation, and sealing solutions is driving the specialty tapes Specialty Tapes Market.

- Growing adoption across automotive, construction, electronics, and healthcare sectors is boosting Specialty Tapes Market growth.

- Expansion of industrial manufacturing and packaging activities is fueling product deployment.

- Increasing focus on high-performance tapes with temperature resistance, chemical stability, and adhesion strength is shaping adoption trends.

- Advancements in acrylic, PTFE, foam, and conductive tape technologies are enhancing functionality and durability.

- Rising need for lightweight, energy-efficient, and sustainable materials is supporting Specialty Tapes Market expansion.

- Collaborations between tape manufacturers, OEMs, and end-use industries are accelerating innovation and global adoption.

U.S. Specialty Tapes Market was valued at USD 18.2 billion in 2025 and is expected to reach USD 33.5 billion by 2035, growing at a CAGR of 6.29% from 2026-2035.

Growth in the Specialty Tapes market of the United States is being supported by an increase in demand in the automobile, electronics, and construction industries; the automation of industries; and the use of innovative adhesives that provide increased performance.

Specialty Tapes Market Growth Drivers:

-

Growing Demand for High-Performance Adhesive Solutions in Automotive and Electronics Industries Drives the Specialty Tapes Market

The growing demand for better-performing adhesives in the automotive and electronics industries is driving the growth in the specialty tapes market. The automotive industry, in particular, is using specialty tapes extensively in place of other bonding processes to ensure that they are lighter and stronger. In the same vein, the growing demand for lighter and fuel-efficient cars is making it essential for manufacturers to use specialty tapes instead of other adhesives, ensuring that there is a lower carbon footprint but retaining the strength of these vehicles. Also, the electronics industry has started using specialty tapes widely in bonding processes because of the small size of these electronic products. Specialty tapes make it easier for designers to make their products lighter and more compact, thereby improving their efficiency and durability.

Specialty Tapes Market Restraints:

-

High Costs Associated with Specialty Tapes and Fluctuating Raw Material Prices Limit Market Growth

Despite the various advantages that specialty tapes provide to businesses, high pricing coupled with the variability in raw material pricing is a major constraint to market growth. Specialty tapes typically utilize innovative materials and adhesives, making production more expensive than regular tapes. Sectors with restricted budgets, such as SMEs, may experience difficulties implementing these costly measures even though they have numerous advantages. Moreover, specialty tape raw materials, including acrylics, silicones, and foams, have variable prices, which may be affected by various market forces, such as supply chain issues and policy changes. This pricing issue may hinder profitability, hence limiting the production of cheaper specialty tapes.

Specialty Tapes Market Opportunities:

-

Increasing Focus on Sustainable and Eco-Friendly Adhesive Technologies Creates Growth Opportunities in the Specialty Tapes Market

Increasing importance given to environmental sustainability presents a new avenue for the development of environmentally friendly specialty tapes. In light of increasing pressures on industries to cut down on their carbon footprints and adhere to environmental regulations, many players have been introducing specialty tapes that can be recycled or are biodegradable. Bio-adhesives are becoming popular as they provide environmentally sustainable solutions without compromising performance requirements in the industrial world. Moreover, water and solvent-free adhesives are increasingly being used due to their environmental advantages in terms of lower emission of toxic substances. Specialty tapes can play an important role in the environmentally sensitive packaging industry as well as the healthcare industry.

Specialty Tapes Market Segment Analysis

By Resin Type

The acrylic category held the lead position in the specialized tapes market with a market share of 40% in the year 2025. Acrylic tapes are highly favored by many industries because of their adhesive nature, strength, and excellent UV resistance ability. They are ideal for exterior use and hence very common in sectors such as the construction sector and the automotive industry, where there are extreme weather conditions. The flexibility of the acrylic tapes has enabled them to bond surfaces effectively and thus become popular even in the packaging and labeling industries.

By Backing Material

Polyvinyl Chloride (PVC) held a major market share as the leading backing material used in specialty tapes in 2025, capturing approximately 35% of the total market share. PVC tapes exhibit excellent flexibility, durability, and moisture and chemical resistance, making them ideal materials for insulations and sealers. Due to their high degree of durability and insulation capabilities, PVC tapes are widely employed in the electrical industry as well as the automotive industry for insulation and protection purposes. Due to these unique features of PVC, coupled with its adhesive characteristics and ability to bond to different surfaces, PVC tapes have remained a leading material choice.

By End-use Industry

In 2025, the electrical and electronics industry held the largest share of the specialty tapes market. Specialty tapes are indispensable when it comes to electronics, as they are used as insulators and for thermal management in various gadgets such as cell phones, laptops, and computers. With the increasing need among consumers for sophisticated and small-sized electronics, the importance of specialty tapes cannot be underestimated. The electronics industry employs specialty tapes during the assembly of electronics and ensures reliable adhesion, thus confirming their importance in the market.

Specialty Tapes Market Regional Analysis

Asia Pacific Specialty Tapes Market Insights

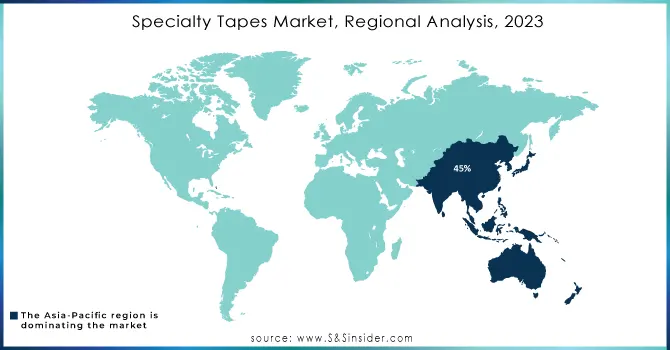

Asia-Pacific held the largest market share of the global specialty tapes market with a market share of 45% in 2025. The reason behind the dominance of the Asia-Pacific region lies in its established manufacturing and industrial presence in areas including electronics, automotive, and healthcare, in countries including China, Japan, and South Korea. Specialty tapes have an important application in the electronics industry where they can be used in assembling processes and as an insulator for managing heat in electronics. In addition to this, there is an increasing demand for specialty tapes in applications such as bonding and sealing in the automotive industry.

North America Specialty Tapes Market Insights

The North American region has been identified as the fastest-growing region within the specialty tapes market, growing at a CAGR of about 7.5%. The fast growth of the region can be attributed to an increase in demand from industries such as healthcare, automotive, and construction in the United States. Specialty tapes are being utilized more in the production of wearables in the healthcare industry. There has been increased activity in the construction industry within the United States, leading to an increased need for high-quality adhesives.

Europe Specialty Tapes Market Insights

Europe Specialty Tapes Market Growth is attributed to increasing demand in various applications, namely automotive, electronics, healthcare, and construction. Adoption of high-performance tapes, pressure sensitive tapes, and green tapes is driving the growth of this market. Innovations in terms of advanced production techniques, as well as tapes for insulation and protection purposes, improve productivity in industries. Strict regulations and sustainability programs have encouraged the use of environment friendly tapes. Key players are concentrating on product differentiation, network expansion, and strategic collaborations.

Middle East & Africa and Latin America Specialty Tapes Market Insights

The Middle East & Africa and Latin America Specialty Tapes Market will see growth in the coming years because of increasing industrialization and automobile production. The increasing need for efficient and customized tapes is driving the growth of this market. These tapes can be single-layered or double-layered and can offer protection from various elements. There will be a greater emphasis on technology and product innovation in these regions by industry players.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Specialty Tapes Market Competitive Landscape:

Avery Dennison Corporation

Avery Dennison Corporation was established in 1935 and specializes in the production of labels, packaging, and special tapes. Its products serve industries such as retailing, healthcare, logistics, and industrial use. With an emphasis on sustainable growth, Avery Dennison continually invests in researching and developing environmentally friendly products, adhesive technologies, and label systems that improve productivity and efficiency for their customers worldwide.

- June 2026 – Avery Dennison Performance Tapes issued an official bonding study press release highlighting adhesive performance of its Core Series specialty tape portfolio when bonding to Rogers Poron industrial polyurethane materials.

LINTEC Corporation

LINTEC Corporation was founded in 1926. It is a Japanese adhesive producer that produces tapes, labels, and other adhesive products for a variety of industries like electronics, automotive, health care, and logistics. LINTEC specializes in developing innovative products focusing on high performance and reliability, while also taking environmental issues into account. LINTEC invests heavily in R&D to develop products that address current industry requirements while promoting recycling and environmentally friendly production methods around the globe.

- March 2025 – LINTEC launched a removable labelstock with low environmental-impact hot-melt adhesive for easier application and recycling-friendly labeling.

Key Players

-

3M (VHB Tape, Double-Sided Tape, Electrical Insulation Tape)

-

Avery Dennison Corporation (EcoFriendly Adhesive Tapes, Reflective Tapes, Labeling Tapes)

-

Berry Global Inc. (Polypropylene Tapes, Double-Sided Tapes, Packaging Tapes)

-

DermaMed Coatings Company, LLC (Medical Adhesive Tapes, Silicone Foam Tapes, Hypoallergenic Tapes)

-

ECHOtape (Masking Tapes, Double-Sided Tapes, HVAC Tapes)

-

Intertape Polymer Group (Paper Masking Tape, Duct Tape, Filament Tape)

-

LINTEC Corporation (Label Stock, Protective Films, Specialty Adhesive Tapes)

-

Lohmann GmbH & Co. (Bonding Tapes, Medical Tapes, Automotive Tapes)

-

NICHIBAN Co., Ltd (Medical Tape, General-Purpose Tape, Masking Tape)

-

NITTO DENKO CORPORATION (Electrical Insulation Tape, Double-Sided Tape, Protective Film)

-

Saint-Gobain (High-Performance Tapes, Duct Tapes, Protective Tapes)

-

Scapa Group Plc (Medical Adhesive Tapes, Industrial Tapes, Specialty Masking Tapes)

-

Specialty Tapes Manufacturing (STM) (Foam Tapes, Custom Adhesive Tapes, Surface Protection Tapes)

-

Tesa Tapes Private Limited (Double-Sided Tapes, Packaging Tapes, Specialty Adhesive Tapes)

-

Adchem Corporation (Double-Sided Foam Tapes, Transfer Tapes, Adhesive Tapes)

-

Essentra plc (Filament Tapes, Label Tapes, Packing Tapes)

-

Rogers Corporation (High-Performance Foam Tapes, Specialty Adhesive Tapes, Thermal Management Tapes)

-

Shurtape Technologies, LLC (Duct Tape, Painter's Tape, Gaffer Tape)

-

Sika AG (Construction Tapes, Adhesive Tapes, Sealing Tapes)

-

Toyochem Co., Ltd (Pressure-Sensitive Adhesive Tapes, Electrical Tapes, Specialty Tapes)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 62.60 Billion |

| Market Size by 2035 | US$ 115.32 Billion |

| CAGR | CAGR of 6.3% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Resin Type (Acrylic, Silicone, Rubber, Others) •By Backing Material (Polyvinyl Chloride (PVC), Polypropylene, Woven/ Non- woven, PET, Paper, Foam, Others) •By End-Use Industry (Electrical & Electronics, Automotive, Healthcare & Hygiene, Building & Construction, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | 3M, Tesa Tapes Private Limited, Avery Dennison Corporation, Scapa Group Plc, Berry Global Inc., Lohmann GmbH & Co., DermaMed Coatings Company, LLC, ECHOtape, LINTEC Corporation, Intertape Polymer Group, Saint-Gobain, NICHIBAN Co., Ltd, Specialty Tapes Manufacturing (STM), NITTO DENKO CORPORATION and other key players |

Frequently Asked Questions

Ans: The Specialty Tapes Market is expected to grow at a CAGR of 6.3% from 2026 to 2035.

Ans: The Specialty Tapes Market was valued at USD 62.60 billion in 2025.

Ans: Growing Demand for High-Performance Adhesive Solutions in Automotive and Electronics Industries Drives the Specialty Tapes Market.

Ans: The Electrical & Electronics segment dominated the Specialty Tapes Market in 2025.

Ans: Asia Pacific dominated the Specialty Tapes Market in 2025.

Get in Touch