Storage in Big Data Market Report Scope & Overview:

The Storage in Big Data Market was valued at USD 66.18 billion in 2025 and is expected to reach USD 330.99 billion by 2035, growing at a CAGR of 17.57% from 2026 to 2035.

Rising volumes of structured and unstructured data from enterprises, IoT devices, cloud platforms, and digital services are accelerating demand for scalable big data storage solutions. Organizations increasingly adopt cloud storage, software-defined storage, and advanced data management tools to support analytics, AI, and real-time decision-making, while regulatory data retention requirements and cybersecurity needs further boost long-term storage investments.

For instance, Amazon Web Services (AWS) reported that global data creation reached 181 zettabytes by the end of 2025, projected to hit 230–240 zettabytes in 2026, with 74% of enterprises storing over 5 PB of unstructured data a 57% increase since 2024.

Microsoft Azure noted that IoT devices generate 79 zettabytes annually by 2025, prompting 80% of enterprises to adopt hyperscale cloud storage for analytics workloads.

Market Size and Forecast:

-

Market Size in 2025: USD 66.18 Billion

-

Market Size by 2035: USD 330.99 Billion

-

CAGR: 17.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Storage in Big Data Market - Request Free Sample Report

Storage in Big Data Market Trends

-

Rising data generation from IoT, social media, and enterprise applications is driving the storage in big data market.

-

Growing adoption of cloud storage, hybrid architectures, and high-performance storage solutions is boosting market growth.

-

Expansion across BFSI, healthcare, IT, and telecommunications sectors is fueling deployment.

-

Increasing focus on data security, scalability, and real-time analytics is shaping adoption trends.

-

Advancements in NVMe, SSDs, distributed storage, and object storage technologies are enhancing performance and efficiency.

-

Rising need for cost-effective and energy-efficient storage solutions is supporting market expansion.

-

Collaborations between storage solution providers, cloud vendors, and enterprises are accelerating innovation and global adoption.

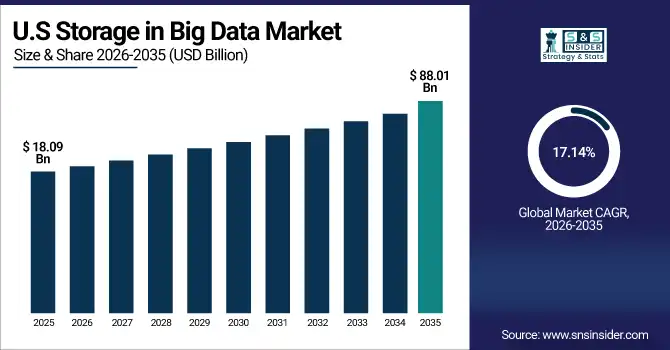

U.S. Storage in Big Data Market was valued at USD 18.09 billion in 2025 and is expected to reach USD 88.01 billion by 2035, growing at a CAGR of 17.14% from 2026-2035.

Rapid growth in enterprise data volumes, expanding cloud adoption, and rising use of AI and analytics are driving demand for scalable storage. Increasing IoT deployment, regulatory data retention needs, and modernization of legacy infrastructure further support sustained market expansion.

Storage in Big Data Market Growth Drivers:

-

Increasing data generation across enterprises and growing requirement for advanced analytics and data-driven decision-making

The massive growth of enterprise data from social media, IoT devices, and transactional systems fuels the need for advanced storage solutions. Organizations require robust platforms to store, manage, and retrieve large volumes of structured, semi-structured, and unstructured data. Big data analytics relies on secure and high-performance storage to derive actionable insights and optimize operations. Industries such as BFSI, IT, manufacturing, and healthcare increasingly adopt storage solutions for predictive analytics, customer insights, and operational efficiency. The escalating volume, variety, and velocity of data globally continue to drive the demand for storage in big data solutions, fueling market expansion.

For example, Google Cloud reports that 97% of companies budget for big data analytics, with 74% relying on data warehouses for AI workloads processing petabyte-scale datasets.

U.S. Department of Commerce data shows BFSI sectors store 40% more transactional data annually, enabling 25% faster fraud detection via real-time storage.

IBM highlights manufacturing firms adopting object storage grew 35% for IoT sensor data, yielding 20% operational cost reductions through predictive maintenance, while HHS reports healthcare providers increased storage 28% for patient records, supporting AI insights that reduce readmissions by 15%.

Storage in Big Data Market Restraints:

-

Security, privacy, and compliance challenges hinder adoption of big data storage solutions

Big data storage platforms handle sensitive organizational and customer information, raising concerns regarding security, data privacy, and regulatory compliance. Enterprises storing financial, healthcare, or personal data must adhere to strict regulations, increasing the complexity of implementation. Threats like cyberattacks, data breaches, and unauthorized access pose significant risks. Implementing robust encryption, access controls, and compliance protocols increases costs and operational challenges. Organizations in highly regulated industries may delay adoption due to these concerns. Security and compliance risks therefore remain major restraints, limiting the market potential and slowing the deployment of storage solutions for big data applications globally.

For instance, NIST reports that 82% of data breaches in 2025 involved big data repositories, with average costs reaching USD 4.88 million per incident due to exposed structured and unstructured data.

The U.S. Department of Homeland Security notes ransomware attacks on storage systems rose 37% in 2025, particularly targeting IoT-fed datasets in manufacturing.

Storage in Big Data Market Opportunities:

-

Growing adoption of hybrid and multi-cloud storage solutions to address data scalability and flexibility needs

Hybrid and multi-cloud storage solutions offer organizations flexibility, scalability, and cost efficiency to manage expanding data volumes. Enterprises can store critical data on-premises while leveraging public clouds for scalability and remote access. This approach reduces infrastructure costs, improves disaster recovery, and enhances operational efficiency. Integration with big data analytics, AI, and machine learning platforms provides actionable insights in real time. Industries such as BFSI, healthcare, retail, and manufacturing increasingly adopt hybrid solutions to support digital transformation initiatives. The rising preference for cloud-enabled storage presents significant growth opportunities for vendors in the big data storage market.

For example, Hitachi Vantara reports that hybrid setups reduce infrastructure costs by 20–30% through tiered storage, supporting real-time analytics in retail via automated data placement across on-premises systems and Microsoft Azure.

Storage in Big Data Market Segment Analysis

-

By Deployment Mode, Cloud dominated with 61% share in 2025; Cloud fastest growing (CAGR).

-

By Component, Services dominated with 40% share in 2025; Services fastest growing (CAGR).

-

By Storage Type, Cloud Storage dominated with 24% share in 2025; Software-Defined Storage (SDS) fastest growing (CAGR).

-

By Industry, BFSI dominated with 26% share in 2025; Retail fastest growing (CAGR).

By Deployment Mode, Cloud segment dominates the Storage in Big Data Market, expected to grow fastest

Cloud segment dominated the Storage in Big Data Market in 2025 due to its flexibility, scalability, and cost-effectiveness, allowing enterprises to manage large volumes of structured and unstructured data efficiently. Cloud storage enables real-time access, seamless integration with analytics platforms, and supports hybrid and multi-cloud strategies. The segment is expected to grow at the fastest CAGR from 2026-2035 as organizations increasingly adopt cloud solutions for digital transformation, remote access, disaster recovery, and AI-driven data management, driving rapid market expansion.

By Component, Services segment dominates the Storage in Big Data Market, expected to grow fastest

Services segment dominated the Storage in Big Data Market in 2025 as enterprises increasingly rely on consulting, integration, deployment, and maintenance services to manage complex storage infrastructure. Services ensure optimal performance, seamless implementation, and reduced operational challenges for big data platforms. The segment is expected to grow at the fastest CAGR from 2026-2035 due to rising demand for outsourced expertise, cloud adoption, and hybrid storage solutions, enabling organizations to optimize costs, enhance efficiency, and accelerate big data storage adoption.

By Storage Type, Cloud Storage segment dominates the Storage in Big Data Market, Software-Defined Storage (SDS) expected to grow fastest

Cloud Storage segment dominated the Storage in Big Data Market in 2025 due to its scalability, flexibility, and cost-efficiency. Enterprises prefer cloud storage for managing massive volumes of structured and unstructured data, enabling real-time access, seamless integration with analytics platforms, and supporting digital transformation initiatives across industries.

Software-Defined Storage (SDS) segment is expected to grow at the fastest CAGR from 2026-2035 as organizations adopt SDS for flexibility, automation, and efficient management of heterogeneous storage environments. SDS allows dynamic provisioning, scalability, and integration with cloud and on-premises systems, driving faster adoption in enterprises seeking cost-effective, high-performance, and software-driven storage solutions.

By Industry, BFSI segment dominates the Storage in Big Data Market, Retail expected to grow fastest

BFSI segment dominated the Storage in Big Data Market in 2025 due to the high demand for secure, real-time storage solutions for transactions, risk analysis, and fraud detection. Banks and financial institutions adopt advanced storage platforms to ensure compliance, operational efficiency, and data-driven decision-making, leading to the largest market share.

Retail segment is expected to grow at the fastest CAGR from 2026-2035 as retailers increasingly use big data storage to analyze customer behavior, optimize inventory, and enhance personalized marketing. Real-time insights, scalability, and cloud integration drive adoption, enabling improved operational efficiency, customer experience, and data-driven strategic decision-making across the retail industry.

Storage in Big Data Market Regional Analysis

North America Storage in Big Data Market Insights

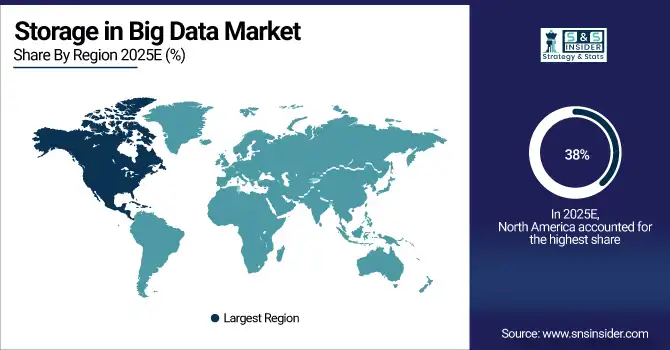

North America dominated the Storage in Big Data Market with the highest revenue share of about 38% in 2025 due to early adoption of big data technologies, strong presence of leading cloud and storage providers, and high investments in digital infrastructure. Enterprises across BFSI, IT, healthcare, and retail deploy advanced storage solutions to manage large-scale data, analytics, and regulatory compliance. Mature data center ecosystems and increasing demand for cloud-based storage further strengthened the region’s market dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Storage in Big Data Market Insights

Asia Pacific segment is expected to grow at the fastest CAGR of about 18.90% from 2026-2035 due to rapid digitalization, growing cloud adoption, and increasing enterprise data generation in emerging economies. Industries such as BFSI, retail, manufacturing, and telecom are increasingly leveraging big data analytics. Rising investments in smart technologies, data centers, government initiatives, and expanding SME adoption are accelerating the need for scalable, secure, and efficient storage solutions across the region.

Europe Storage in Big Data Market Insights

Europe holds a significant position in the Storage in Big Data Market due to strong regulatory frameworks, high enterprise adoption of data analytics, and increasing demand for secure and compliant storage solutions. Industries such as BFSI, healthcare, manufacturing, and government actively invest in scalable storage infrastructure to manage growing data volumes. Rising cloud adoption, data sovereignty requirements, and modernization of data centers continue to support steady market growth across the region.

Middle East & Africa and Latin America Storage in Big Data Market Insights

Middle East & Africa and Latin America are steadily advancing in the Storage in Big Data Market due to increasing digital transformation initiatives, cloud infrastructure investments, and expanding data-driven industries. Growing adoption of big data analytics across BFSI, telecom, retail, and government sectors supports demand for scalable storage solutions. Improving data center capacity, rising enterprise digitization, and supportive government programs further contribute to sustained regional market growth.

Storage in Big Data Market Competitive Landscape:

IBM Corporation

IBM provides enterprise-scale storage solutions designed for AI, analytics, and big data workloads. Its offerings, including FlashSystem and Storage Scale platforms, deliver high throughput, low latency, and hybrid cloud integration. IBM’s storage portfolio combines hardware, software, and AI-driven management tools to enable organizations to store, access, and analyze unstructured and structured data efficiently. It supports cloud-scale operations, accelerates data-driven insights, and enhances scalability and resiliency for global enterprises.

-

2023: IBM launched Storage Scale System 6000, offering 7M IOPS and high bandwidth throughput for demanding AI and big data workloads.

-

2024: IBM introduced Storage Assurance, boosting FlashSystem performance, resilience, and efficiency across enterprise big data storage environments.

-

2025: IBM collaborated with NVIDIA AI Data Platform to enhance storage for unstructured data, integrating with watsonx and hybrid cloud for scalable analytics.

NetApp, Inc.

NetApp delivers unified data storage solutions optimized for big data and AI workloads. Its AFF A-Series, StorageGRID, and Kubernetes-supported platforms provide high IOPS, scalable throughput, and secure storage for enterprises. NetApp integrates software-defined storage, hybrid cloud management, and advanced automation to enable rapid analytics, flexible data orchestration, and efficient lifecycle management. Its solutions help organizations accelerate AI insights, streamline operations, and ensure resilient storage infrastructure for modern data-intensive applications.

-

2024: NetApp unveiled AFF A-Series for modern workloads, delivering high IOPS, scalable throughput, and enterprise-grade security for big data and AI pipelines.

-

2025: NetApp expanded AFF platforms and StorageGRID, adding Kubernetes support to enhance scalability and flexibility for analytics and AI workloads.

Hewlett Packard Enterprise

HPE provides intelligent storage solutions for enterprise-scale big data and AI applications. Leveraging software-defined storage, NVMe scaling, and hybrid cloud architectures, HPE GreenLake and Alletra platforms optimize throughput, analytics, and automation. HPE’s AI-driven management enables efficient data operations, accelerates insight generation, and unifies storage across on-premises and cloud environments. Partnerships with NVIDIA and other AI platforms enhance HPE’s ability to support modern, high-volume, and mission-critical workloads.

-

2024: HPE introduced software-defined storage with AI automation in GreenLake, unifying data management and optimizing high-volume workloads.

-

2025: HPE revealed unified data layer with NVIDIA AI, boosting hybrid cloud storage access and accelerating data-to-insight lifecycles.

Amazon Web Services (AWS)

AWS provides scalable, high-performance cloud storage solutions for analytics, AI, and big data. Services like Amazon S3, FSx, and Storage Gateway deliver exabyte-scale capacity, high throughput, and robust security. AWS enables organizations to store, query, and analyze massive datasets efficiently, supporting data lakes, ML pipelines, and cloud-native applications. Continuous innovations, including metadata querying and intelligent tiering, optimize costs and accelerate insights for enterprise-scale AI and big data workloads.

-

2024: AWS re:Invent 2024 introduced S3 Tables and FSx Intelligent-Tiering, improving storage performance and analytical capabilities across data lakes.

-

2025: AWS emphasized exabyte-scale S3 growth and new S3 Tables supporting tabular analytics for AI and big data workloads.

Microsoft Azure

Microsoft Azure provides enterprise cloud storage solutions designed for big data, analytics, and AI workloads. Azure Storage offers high throughput, SSD scaling, and exabyte-level capacity, enabling fast access to massive datasets. Integration with Azure Data Box, Blob Storage, and hybrid architectures accelerates data migration and analytics. Azure’s scalable storage platform supports cloud-native AI, real-time insights, and high-performance analytics, empowering organizations to manage, process, and secure large volumes of structured and unstructured data efficiently.

-

2023: Azure Storage handled over 100 exabytes with high SSD scaling and transactions for analytics, database, and big data workloads.

-

2024: Azure Data Box 120 & 525 launched, accelerating large-scale data migrations for analytics and data lake use cases.

-

2025: Azure Blob Storage rearchitected for exabyte scale, supporting millions of I/O transactions per second and high-throughput AI workloads.

Key Players

-

Dell Technologies Inc.

-

Hewlett Packard Enterprise (HPE)

-

NetApp, Inc.

-

Microsoft Corporation (Azure)

-

Google LLC (Google Cloud)

-

Oracle Corporation

-

SAP SE

-

SAS Institute Inc.

-

Hitachi Vantara (Hitachi, Ltd.)

-

Western Digital Corporation

-

Seagate Technology PLC

-

Huawei Technologies Co., Ltd.

-

Samsung Electronics Co., Ltd.

-

Pure Storage, Inc.

-

Teradata Corporation

-

VMware Inc.

-

Scality

-

Cloudian

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 66.18 Billion |

| Market Size by 2035 | USD 330.99 Billion |

| CAGR | CAGR of 17.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment Mode(Cloud, On-Premises) • By Component(Hardware, Software, Services) • By Storage Type(Network Attached Storage (NAS), Direct Attached Storage (DAS), Storage Area Network (SAN), Software-Defined Storage (SDS), Cloud Storage) • By Industry(Banking, Financial Services, & Insurance (BFSI), Healthcare, Retail, IT & Telecommunications, Government, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Dell Technologies Inc., Hewlett Packard Enterprise (HPE), NetApp, Inc., Amazon Web Services (AWS), Microsoft Corporation (Azure), Google LLC (Google Cloud), Oracle Corporation, SAP SE, SAS Institute Inc., Hitachi Vantara (Hitachi, Ltd.), Western Digital Corporation, Seagate Technology PLC, Huawei Technologies Co., Ltd., Samsung Electronics Co., Ltd., Pure Storage, Inc., Teradata Corporation, VMware Inc., Scality, Cloudian |

Frequently Asked Questions

North America dominated the Storage in Big Data Market in 2025.

The Cloud Storage segment dominated the Storage in Big Data Market in 2025.

Increasing data generation across enterprises and growing requirement for advanced analytics and data-driven decision-making

The Storage in Big Data Market was valued at USD 66.18 billion in 2025.

The Storage in Big Data Market is expected to grow at a CAGR of 17.57% from 2026 to 2035.

Get in Touch