Synthetic Dyes Market Report Scope & Overview:

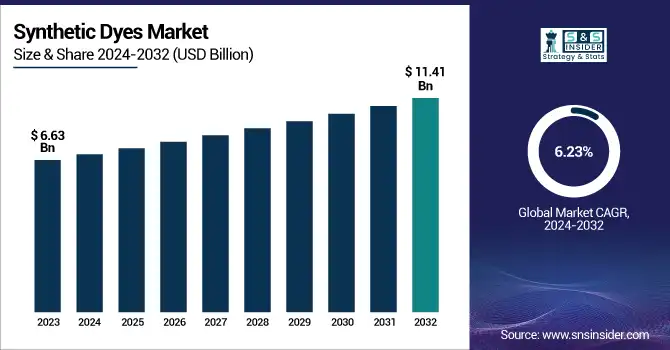

The Synthetic Dyes Market Size was valued at USD 6.63 Billion in 2023 and is expected to reach USD 11.41 Billion by 2032, growing at a CAGR of 6.23% over the forecast period of 2024-2032.

To Get more information on Synthetic Dyes Market - Request Free Sample Report

The synthetic dyes market is shaped by innovation, regulation, and shifting global dynamics. Our report draws a clear comparison between synthetic and natural dyes, emphasizing synthetic dyes’ dominance in durability and cost while noting the eco-driven rise of natural options. It explores evolving regional regulatory compliance trends impacting global trade and production. The innovation landscape is examined through patent filing trends, showcasing ongoing advancements. Government export incentives and tax subsidies are detailed, especially in nations prioritizing chemical exports. The report also assesses how geopolitical disruptions influence supply chains and material sourcing. Finally, it highlights the economic weight of the industry by analyzing the synthetic dye sub-sector’s contribution to GDP, particularly in leading manufacturing countries, offering a complete market perspective.

The US Synthetic Dyes Market Size was valued at USD 672.71 Million in 2023 with a market share of around 70% and growing at a significant CAGR over the forecast period of 2024-2032.

The US synthetic dyes market is experiencing steady growth, driven by rising demand from the textile, automotive, and packaging industries. The surge in eco-friendly dye solutions, supported by innovations from companies like Huntsman Corporation and Chemours Company, is reshaping product offerings. Organizations such as the American Association of Textile Chemists and Colorists (AATCC) are encouraging sustainable practices and innovation through industry standards and research initiatives. Additionally, the U.S. Environmental Protection Agency’s (EPA) focus on cleaner production has prompted manufacturers to invest in advanced dyeing technologies, boosting market competitiveness. These dynamics, coupled with steady domestic demand and technological innovation, continue to propel the market forward.

Synthetic Dyes Market Dynamics

Drivers

-

Adoption of Smart Textile Technologies is Elevating the Application of Performance-Driven Synthetic Dyes Across Sectors

The rapid integration of smart textiles across industries such as sportswear, healthcare, and military has driven the demand for high-performance synthetic dyes. These textiles often require dyes with specific properties—such as heat resistance, UV protection, and conductivity to function effectively in various environments. As synthetic dyes offer customization and stability under harsh conditions, they are preferred over natural alternatives for smart fabrics. Leading companies like DuPont and Clariant AG have been actively involved in formulating specialized dyes suitable for conductive or thermochromic applications in smart wearables. For instance, performance wear developed for athletes often incorporates moisture-wicking and color-stable properties, which depend heavily on high-quality synthetic dyes. Moreover, military uniforms embedded with sensors or camouflage effects require robust dye formulations to withstand extreme weather and operational conditions. As the global smart textile market grows, synthetic dyes that meet these new material standards are in increasing demand. This has led to higher R&D investments by both startups and established firms to expand their product portfolios with advanced dye technologies. Government agencies like the U.S. Department of Defense and National Science Foundation are funding research initiatives involving responsive textile materials, adding a policy-driven dimension to this market shift. This synergy between technological innovation and dye chemistry is opening new frontiers for synthetic dyes beyond traditional applications. The expanding use of functional fabrics will continue to fuel the adoption of specialized synthetic dyes, making this a critical driver of market growth.

Restraints

-

Fluctuating Prices of Petrochemical Feedstocks Used in Dye Manufacturing Negatively Affect Profit Margins for Dye Producers

Synthetic dyes are predominantly derived from petrochemical-based feedstocks, making them highly sensitive to fluctuations in global crude oil prices. The instability in raw material pricing, driven by geopolitical tensions, supply chain disruptions, and changes in global energy policies, directly impacts the cost structure of dye production. For example, the Russia-Ukraine conflict and sanctions on oil-producing nations have caused significant volatility in benzene and toluene prices two primary inputs for dye synthesis. As a result, manufacturers often face difficulty in maintaining competitive pricing while ensuring consistent product quality. This challenge is further exacerbated in export-oriented markets, where low-cost suppliers from emerging economies intensify price wars. Dye manufacturers operating in the United States also have to navigate environmental taxes and carbon emission penalties, adding another layer of cost variability. While some large firms can absorb or pass on these costs, small to mid-sized enterprises may struggle to maintain profitability, limiting their ability to invest in innovation or expansion. The uncertainty in raw material costs acts as a persistent barrier to growth and long-term planning, especially for players heavily dependent on imported feedstocks. Therefore, the synthetic dyes market remains vulnerable to oil market dynamics, which restrains its potential for sustainable and predictable growth.

Opportunities

-

Collaborative Research Initiatives with Academic Institutions Drive Innovation and Product Development in High-Performance Synthetic Dyes

Partnerships between dye manufacturers and academic institutions are unlocking opportunities for advanced research and innovation in synthetic dye chemistry. U.S. universities such as North Carolina State University and the Massachusetts Institute of Technology (MIT) are known for their materials science and textile engineering programs, often collaborating with industry leaders on research projects. These partnerships focus on developing high-performance, sustainable, and application-specific dyes particularly for smart textiles, medical devices, and high-end fashion. For example, research funded by the National Science Foundation (NSF) has resulted in the development of self-healing colorants and responsive dyes that change hue based on temperature or pH. Manufacturers benefit by gaining early access to cutting-edge technologies and intellectual property, while academic institutions gain real-world platforms to validate their research. These synergies are accelerating time-to-market for innovative products and expanding the capabilities of synthetic dyes across sectors. As such collaborations become more structured and outcome-focused, they represent a strong opportunity for long-term market expansion and technological leadership.

Challenge

-

Persistent Consumer Perception Issues Regarding Toxicity of Synthetic Dyes Limit Adoption in Health-Conscious Product Segments

Despite significant advancements in dye formulation and safety, synthetic dyes continue to face negative perceptions among consumers concerned about chemical exposure. This is particularly true in segments like children’s apparel, personal care, and food packaging, where even trace elements of harmful compounds can deter purchases. Public scrutiny is amplified by increasing awareness campaigns, NGO activism, and viral misinformation, which often portray synthetic dyes as universally harmful. This perception challenge places pressure on brands and manufacturers to switch to natural or certified organic alternatives, even when synthetic options are safe, efficient, and more cost-effective. In the absence of transparent labeling and educational outreach, these misconceptions persist, slowing down adoption in sensitive product categories. For synthetic dye producers, this poses a challenge that cannot be addressed purely through product innovation; it requires sustained efforts in consumer education, transparency, and certification to rebuild trust and validate safety claims. Until then, the market will continue facing hurdles in perception-driven sectors.

Synthetic Dyes Market Segmental Analysis

By Product

Reactive dyes dominated the synthetic dyes market in 2023, accounting for a market share of 37.8%. Reactive dyes held the dominant position in the synthetic dyes market owing to their superior wash fastness, vibrant color profiles, and strong compatibility with cellulose fibers such as cotton and rayon. Their chemically reactive nature forms covalent bonds with textile fibers, ensuring long-lasting color even after multiple washes—making them especially favorable in the textile sector, which remains the largest consumer of dyes. According to the American Association of Textile Chemists and Colorists (AATCC), reactive dyes are now preferred over direct dyes due to their eco-friendliness and reduced effluent load. In addition, government initiatives like India’s Integrated Processing Development Scheme (IPDS) and China’s 14th Five-Year Plan, which promotes sustainable textile manufacturing, have indirectly boosted the demand for reactive dyes in textile hubs. Leading players such as Huntsman International LLC and Archroma have increased their production of low-salt and biodegradable reactive dyes, aligning with global environmental norms. The increasing adoption of digital textile printing, which favors reactive dyes for high-resolution cotton prints, has further propelled their usage in both developing and developed markets.

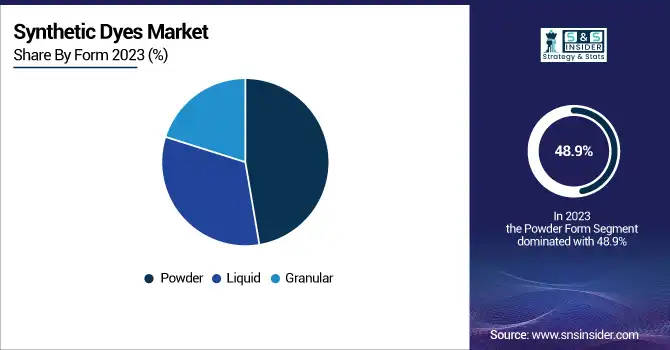

By Form

Powder form dominated the synthetic dyes market in 2023, holding an estimated market share of 48.9%. Powder dyes remained the most preferred form in the synthetic dyes market due to their cost-effectiveness, ease of transportation, and extended shelf life. Their low moisture content makes them highly stable, which is crucial in regions with varying humidity levels. Manufacturers prefer powdered dyes for bulk production runs in textiles, leather, and paper industries as they allow easy formulation adjustments. According to the U.S. Environmental Protection Agency (EPA), powdered dyes also reduce shipping-related emissions due to their lower weight-to-volume ratio compared to liquid counterparts. Key producers such as LANXESS and Dystar offer a wide range of powder-based synthetic dyes optimized for energy-efficient dyeing processes. In markets like India and China, where textile processing is carried out in large batches, powdered dyes have proven more practical than liquid forms. Additionally, ongoing developments in dust-free granulated powders and water-soluble sachets have improved user safety and handling, further reinforcing powder dyes' leadership in the global market.

By End-use

The textiles segment dominated the synthetic dyes market in 2023, commanding a market share of approximately 61.4%. The textiles industry remained the backbone of the synthetic dyes market in 2023, driven by the sector’s sheer scale and evolving demands for vibrant, durable, and functional dyes. According to the National Council of Textile Organizations (NCTO) in the United States, textiles continue to innovate rapidly, incorporating performance features such as moisture control, UV resistance, and antimicrobial coatings all of which rely on synthetic dyes. Asia, particularly China, India, and Bangladesh, emerged as the largest producers and exporters of dyed textiles, creating strong regional demand for synthetic dyes. Furthermore, with the rise of fast fashion and e-commerce platforms like Shein and H&M expanding their dyed apparel lines, the volume of synthetic dye consumption in this segment has grown substantially. Synthetic dyes also fulfill the technical needs of digital textile printing, now widely adopted in the fashion and home décor sectors. Governments in textile-heavy regions have implemented favorable schemes and pollution control subsidies that indirectly support dye production.

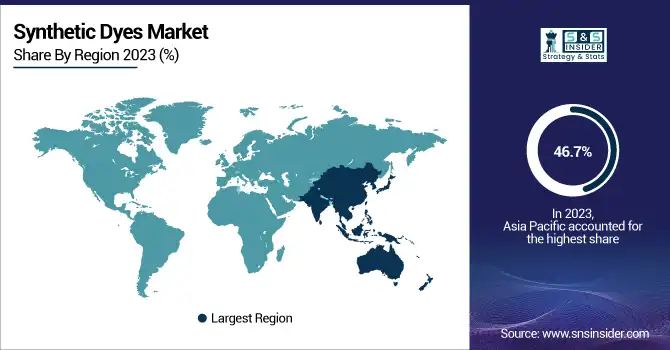

Synthetic Dyes Market Regional Outlook

Asia Pacific dominated the synthetic dyes market in 2023 with a market share of 46.7%. Asia Pacific’s leadership in the synthetic dyes market is largely attributable to its enormous textile manufacturing capacity, cost-effective production infrastructure, and favorable regulatory frameworks. Countries such as China, India, and Bangladesh serve as global textile powerhouses, accounting for over 60% of the world’s dyed textile output. According to the China National Textile and Apparel Council (CNTAC), China alone contributed to over 40% of global textile exports in 2023, supported by its robust supply chains and integrated dye manufacturing clusters in provinces like Jiangsu and Zhejiang. India’s Ministry of Chemicals and Fertilizers also reported a significant increase in synthetic dye exports through its “Make in India” initiative, particularly in Gujarat’s dye manufacturing belt. Bangladesh’s Ready-Made Garment (RMG) industry, supported by organizations like the Bangladesh Garment Manufacturers and Exporters Association (BGMEA), heavily relies on synthetic dyes for fast fashion exports. Additionally, relaxed labor laws, growing domestic demand, and rising foreign direct investments have positioned Asia Pacific as a self-reinforcing hub for synthetic dye consumption and production. With increasing urbanization and disposable incomes, consumers in the region continue to drive demand for dyed textiles, home furnishings, and automotive fabrics, making Asia Pacific a dominant force in shaping the global market landscape.

On the other hand, North America emerged as the fastest growing region in the synthetic dyes market, with a significant CAGR during the forecast period of 2024 to 2032. North America's rapid growth in the synthetic dyes market is being driven by technological innovation, demand for sustainable solutions, and expanding applications in smart textiles and high-performance materials. The United States, in particular, is witnessing increasing adoption of synthetic dyes in non-textile industries such as automotive interiors, medical textiles, and aerospace composites. According to the U.S. Department of Commerce, American textile and dye manufacturers are benefiting from reshoring initiatives and the Inflation Reduction Act, which promotes domestic production. Companies like Huntsman International LLC and DyStar LP are pioneering high-purity, low-impact synthetic dye products tailored for digital printing and technical applications. Meanwhile, Canada is experiencing growth in eco-labeled textile exports, supported by the Canadian Apparel Federation’s sustainability push. Mexico is evolving as a nearshoring destination for North American brands, boosting regional dye demand for localized production. Regulatory clarity and environmental compliance, led by agencies like the U.S. Environmental Protection Agency (EPA), are pushing the industry toward cleaner processes and water-efficient dyeing technologies. These combined trends driven by innovation, policy, and reshoring are making North America a high-growth region poised for transformative expansion in the synthetic dyes landscape.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Archroma (Reactive Blue 19, Acid Black 210, Disperse Red 73)

-

Atul Ltd. (Reactive Red 195, Sulphur Black BR, Vat Blue 4)

-

BASF SE (Cibacron Brilliant Red, Palanil Yellow, Irgalite Blue)

-

Bodal Chemicals Ltd. (Reactive Blue 21, H Acid, Vinyl Sulfone Ester)

-

Clariant AG (Remazol Brilliant Blue, Indanthren Yellow F4G, Sandoplast Red)

-

DIC Corporation (Oil Red O, Lithol Rubine, Nigrosine)

-

DyStar Group (Zhejiang Longsheng Group Co., Ltd.) (Reactive Blue 160, Disperse Orange 30, Acid Yellow 49)

-

Everlight Chemical Industrial Corporation (Disperse Blue 56, Acid Red 183, Reactive Yellow 145)

-

Hangzhou Tiankun Chem Co., Ltd. (Disperse Violet 93, Reactive Black 5, Acid Blue 113)

-

Huntsman International LLC (Reactive Navy Blue RX, Disperse Black ECT, Acid Blue 25)

-

Jay Chemical Industries Pvt. Ltd. (Reactive Orange 122, Reactive Blue 13, Vinyl Sulfone Orange)

-

Jiangsu Yabang Dyestuff Co., Ltd. (Reactive Black 39, Disperse Red 167, Acid Yellow 194)

-

Kiri Industries Ltd. (Reactive Yellow 160, Acid Red 337, Vinyl Sulphone Ester Orange)

-

KIWA Chemical Industry Co., Ltd. (Acid Red 97, Disperse Blue 3, Basic Violet 10)

-

LANXESS AG (Bayfast Yellow, Macrolex Red, Solvent Blue 35)

-

Nippon Kayaku Co., Ltd. (Kayacelon Blue HRL, Kayacelon Yellow HR, Kayarus Blue A-R)

-

Sudarshan Chemical Industries Ltd. (Sudarshan Disperse Blue 79, Disperse Violet 28, Sudarshan Acid Red 57)

-

Synthesia, a.s. (Acid Blue 25, Direct Red 81, Reactive Black 5)

-

Zhejiang Longsheng Group Co., Ltd. (Reactive Red 218, Disperse Blue 359, Acid Violet 49)

-

Zhejiang Runtu Co., Ltd. (Reactive Blue 222, Acid Black 210, Disperse Yellow 54)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 6.63 Billion |

| Market Size by 2032 | USD 11.41 Billion |

| CAGR | CAGR of 6.23% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Reactive Dyes, Vat Dyes, Acid Dyes, Direct Dyes, Disperse Dyes, Others) •By Form (Liquid, Powder, Granular) •By End-use (Textiles, Pulp & Paper, Leather, Building & Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Huntsman International LLC, LANXESS AG, DyStar Group (Zhejiang Longsheng Group Co., Ltd.), Archroma, Clariant AG, Kiri Industries Ltd., Atul Ltd., Bodal Chemicals Ltd., Everlight Chemical Industrial Corporation and other key players |

Frequently Asked Questions

Asia Pacific led the Synthetic Dyes Market in 2023 due to its massive textile output and supportive industrial policies.

Smart textiles are boosting demand in the Synthetic Dyes Market for performance-driven and functional dye applications.

The textiles sector remains the largest consumer in the Synthetic Dyes Market, accounting for over 61% share in 2023.

Reactive dyes dominate the Synthetic Dyes Market for their superior wash fastness and fiber compatibility, especially in textiles.

The Synthetic Dyes Market is expected to reach USD 11.41 billion by 2032, driven by robust demand and innovation.

Get in Touch