Testing, Inspection, and Certification (TIC) Market Size Analysis:

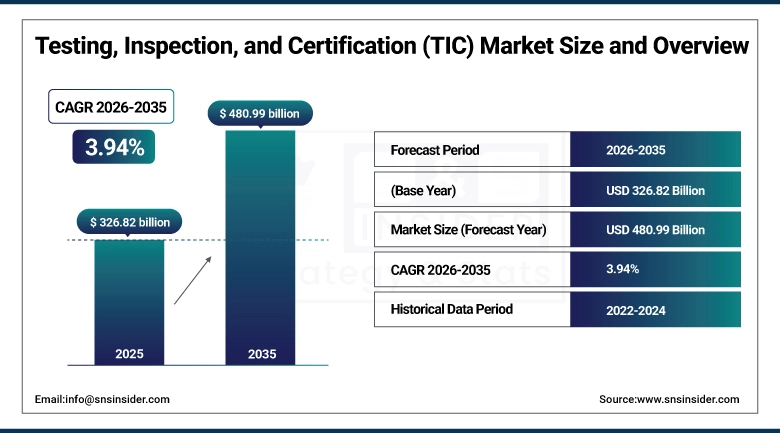

The Testing, Inspection, and Certification (TIC) Market Size was valued at USD 326.82 billion in 2025 and is expected to reach USD 480.99 billion by 2035 and grow at a CAGR of 3.94% over the forecast period 2026-2035.

The Testing, Inspection, and Certification (TIC) industry is driven by the need for quality assurance, safety, and regulatory compliance in various industries. With the rise in globalization and complexity in supply chains, the demand for testing and inspection services has increased. With the development in technology, testing and inspection have become efficient with the help of automation and data analytics. Increasing consumer awareness and environmental/safety regulations also boost the demand for testing and inspection services. Outsourcing also supports the growth of testing and inspection services.

Testing, Inspection and Certification (TIC) Market Size and Growth:

-

Market Size in 2025: USD 326.82 Billion

-

Market Size by 2035: USD 480.99 Billion

-

CAGR: 3.94% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

Get more information on Testing, Inspection, and Certification Market - Request Free Sample Report

Key Testing, Inspection, and Certification (TIC) Market Trends:

-

Growth in international trade is driving demand for TIC services to ensure compliance with diverse country-specific regulations and standards.

-

Complex global supply chains require extensive testing and inspection at every stage to maintain quality and regulatory adherence.

-

Increasing consumer expectations for safe, reliable, and high-quality products are boosting investments in TIC services.

-

Online reviews and social media influence brand reputation, emphasizing the importance of product quality and safety certification.

-

Rising focus on food safety and contamination prevention is driving stricter testing and certification in the food and beverage sector.

U.S. Testing, Inspection and Certification (TIC) market Size Outlook:

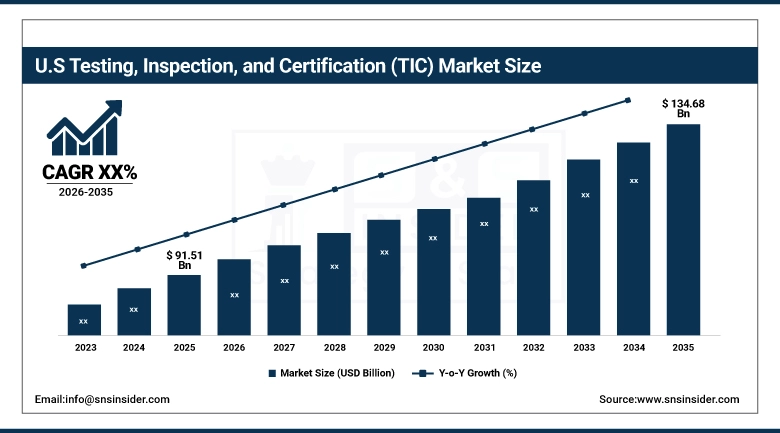

The U.S. Testing, Inspection and Certification (TIC) market is projected to grow from USD 91.51 Billion in 2025E to USD 134.68 Billion by 2035. Growth is driven by stringent regulatory compliance mandates across healthcare, food safety, and industrial sectors, alongside increasing emphasis on supply chain quality assurance and product safety standards. Rising investments in renewable energy infrastructure, electric vehicle certification, and the expansion of e-commerce requiring rigorous testing further accelerate market demand, ensuring safety, quality, and operational integrity across diverse American industries.

Testing, Inspection, and Certification Market Growth Drivers:

-

Navigating intricate regulations and ensuring compliance in the TIC market influenced by global trade.

The growth of international trade is a major factor affecting the TIC market. As nations participate in global trade, products must meet various regulations and standards unique to each market. Extensive testing, inspection, and certification are required to ensure compliance with varying country-specific requirements. For instance, a product made in China and meant to be sold in the European Union must adhere to the strict regulations of the EU, which can vary from those in the United States or other areas. Globalization has created an intricate supply chain system, with parts of a solitary product possibly coming from various nations.

-

Increasing consumer safety demand is leading to higher investments in TIC services to ensure quality standards are met.

Consumers are now demanding quality, safe, and reliable products because of the large amount of information on the internet. The changing nature of consumers has forced companies to invest more in TIC services to ensure that their products meet the highest quality and safety standards. The emergence of social media and internet review sites has also heightened the importance of quality in the image of the company’s brand name. Consumers are becoming increasingly concerned about food safety in the food and beverage industry. This has forced companies to invest more in quality testing and certification of their products to ensure that they are safe and free of contaminants.

Testing, Inspection, and Certification (TIC) Market Restraints:

-

Small and medium-sized testing, inspection, and certification firms embrace sophisticated technologies at a slower pace.

Smaller and medium-sized testing, inspection, and certification (TIC) companies frequently encounter difficulties in implementing advanced technologies because of various factors that affect their speed of integration. A major limitation that these companies face is the restricted financial resources at their disposal. Smaller companies may struggle to allocate the significant capital needed to invest in advanced technologies like automation tools, artificial intelligence, or state-of-the-art testing equipment. Smaller firms may find it difficult to invest financially in these high-risk opportunities that have uncertain returns.

Moreover, the challenge of incorporating new technologies into current systems is significantly difficult. Small and medium-sized TIC companies may not have the required technical knowledge or staff to effectively set up and upkeep complex systems. Providing training for employees on using new technologies and modifying current processes to incorporate these advancements can require a lot of resources and time, leading to increased reluctance.

Testing, Inspection, and Certification (TIC) Market Opportunities:

-

Integration of Advanced Technologies in TIC Services

The incorporation of AI, IoT, and automation is changing the face of the TIC market by improving efficiency, accuracy, and speed of testing and inspection. The incorporation of AI ensures analytics, which enables predictive maintenance and instant decision-making. The incorporation of IoT ensures remote monitoring and collection of data. The incorporation of automation ensures accuracy and minimizes errors and cost of operation. These technologies also ensure digital inspection and smart compliance. They allow faster certification. The need for digital inspection and smart compliance is increasing as industries adopt digital transformation.

TIC - Testing, Inspection, and Certification Market Segment Analysis:

By Application

The infrastructure segment led the market with a revenue share of more than 15% in 2025. Increased infrastructural activities in various countries, such as China, India, and some European countries, especially in the development of transportation systems, are expected to enhance the rate of adoption of TIC services and products in these regions, providing a boost to the market. The consumer goods and retail, as well as the agriculture and Medical & Life Science, chemicals, energy & power, education, and government, manufacturing, healthcare, and Chemicals, oil & gas, and petroleum, public sector, automotive, aerospace & defense, supply chain & logistics, and other applications segments also influence the market.

The consumer goods and retail segment are expected to grow at a faster rate during 2026-2035, due to the inspection activities that the companies in this sector carry out. To provide flawless products to its customers, consumer goods companies must comply with various quality regulations and standards. This is the deployment of highly efficient and comprehensive inspection systems and, consequently, the growth in the TIC market. Additionally, companies in the retail sector must provide customers with optimum products and the best possible customer shopping experience, which enhances the penetration of TIC services and technologies and, consequently, drives market growth.

By Service Type

Testing led the market in 2025 with a market share of more than 42%. It involves a wide range of activities such as product development and manufacturing that are demanded across different industries. Therefore, products and systems are under testing to ensure they meet safety, quality, and legal requirements. To comply with the demand and assure their customers of quality services, companies currently prefer using services of licensed test centers for the safety of their products. Their focus on material durability and strength, as well as functional and operational reliability, has resulted in their dominance in the market.

Inspection is considered to be the fastest-growing segment during 2026-2035 in the TIC market. It is defined by the growth of this segment because of the increased number of government regulations in such industries as construction, energy, and manufacturing. The demand is stated to grow as the risk associated with the in-house inspection of equipment with no standards and regulations for such inspections has also grown. The tendency is maintained because of the growing global trade, stricter government regulations surrounding the development and adoption of unified standards for world trade, and smart inspection technologies that also sustain demand for inspections.

By Sourcing

The In-House segment held a market share of around 56% in 2025 and dominated the market. This approach enables companies to retain control over the quality, speed, and confidentiality of services, which is particularly important in precision and highly regulated industries. Companies utilize In-House TIC services in the pharmaceutical, aerospace, and automotive sectors, among others, because of the high standards and the need for protection of proprietary processes. Given that companies conduct the services in-house, they can appreciate risks effectively, comply with the requirements of complex regulations, and adapt the services to their specific conditions. At the same time, third-party access is limited, meaning that the majority of the risk is mitigated by the organization itself.

The outsourced is the most rapidly growing segment with a faster CAGR between 2026-2035. The situation is conditioned by the expansion of global supply chains and increasing demands, which make it difficult for companies to sustain versatile and specialized TIC services. Companies seek the services of third parties to benefit from providers’ advanced technology, knowledge, and worldwide coverage. The outsourced segment represents an appealing option for smaller entities because they have a varying degree of burden but may not require institutionalization of In-House TIC services.

Testing, Inspection, and Certification (TIC) Market Regional Analysis:

Asia Pacific Testing, Inspection, and Certification (TIC) Market Insights

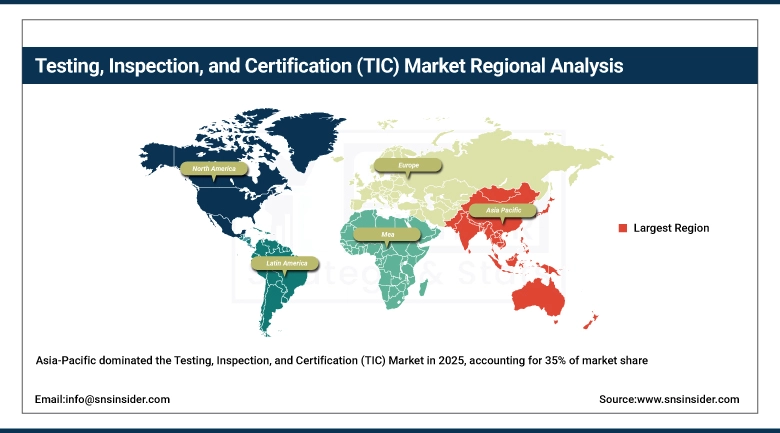

Asia Pacific dominated the market in 2025 with a market share of over 35%. The prime driving factors that contribute to this growth include the expanding industrial base, growing manufacturing activities, and the increasing demand for improved quality and safety by consumers in the region. Additionally, the industrial growth experienced in China, India, and Southeast Asian countries requires these industries to increase their TIC services to ensure their products comply with international standards. The booming construction, electronics, and automotive industries in the region further stimulate the need and the demand for full-service TIC solutions.

Need any customization research on Testing, Inspection, And Certification Market - Enquiry Now

Europe Testing, Inspection, and Certification (TIC) Market Insights

Europe is projected to witness a massive growth rate during the forecast period. The presence of established and eminent automotive industries in countries such as Germany and France also makes the seamless deployment of the testing and inspection ecosystem enhance the operations of Europe-based automotive production companies. Similarly, with the presence of exceptional fashion brands and retail and consumer goods corporations based in countries like Italy, Portugal, and the U.K., they nurture and catalyze the growth, nurturing the growth of the local testing and certification market.

North America Testing, Inspection, and Certification (TIC) Market Insights

The North America Testing, Inspection, and Certification (TIC) market is driven by stringent regulatory standards, growing consumer demand for quality and safety, and expanding industrial and manufacturing activities. Key sectors include automotive, food & beverage, and electronics, with TIC services ensuring compliance, reliability, and competitive advantage across supply chains.

Latin America and Middle East & Africa TIC Market Insights

The LATAM and MEA Testing, Inspection, and Certification (TIC) markets are growing due to increasing industrialization, regulatory enforcement, and rising consumer awareness of product quality and safety. Key sectors include energy, construction, and food & beverage, with TIC services ensuring compliance, risk mitigation, and enhanced market credibility.

Testing, Inspection & Certification (TIC) Companies are:

-

SGS Group

-

Eurofins Scientific

-

Apave International

-

TIC Sera

-

Element Materials Technology

-

UL LLC

-

QR Testing

-

Hohenstein

-

Dekra Certification

-

ALS Limited

-

Intertek Group plc

-

SAI Global Limited

-

MISTRAS Group, Inc

-

TUV SUD

-

TUV Rheinland

-

DNV

-

Kiwa

-

CTC Group

Competitive Landscape for Testing, Inspection, and Certification (TIC) Market:

SGS Group, a global leader in testing, inspection, and certification (TIC) services, ensures product quality, safety, and regulatory compliance across industries. The company provides comprehensive solutions, including laboratory testing, audits, and certification, supporting global trade and consumer confidence.

- In January 2025, SGS introduced an AI-powered predictive compliance platform that enables companies to identify potential regulatory risks in advance. This solution enhances proactive quality management and reduces the likelihood of non-compliance across supply chains.

TÜV SÜD is a global testing, inspection, and certification (TIC) company providing safety, quality, and sustainability solutions across industries. The company offers product testing, system certification, inspection, and training services, helping businesses comply with regulations and enhance operational efficiency.

- In March 2025, TÜV SÜD launched a digital twin-based inspection service designed to simulate industrial environments and detect potential defects before physical testing. This innovation improves inspection accuracy and reduces operational downtime.

Bureau Veritas is a global leader in testing, inspection, and certification (TIC) services, offering expertise in quality, health, safety, and environmental compliance. The company supports industries with auditing, certification, laboratory testing, and consulting to ensure regulatory adherence and operational excellence.

- In February 2025, Bureau Veritas introduced an integrated ESG verification platform that combines real-time data analytics with certification services, enabling companies to monitor sustainability performance and ensure compliance with evolving global standards.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 326.82 Billion |

| Market Size by 2035 | USD 480.99 Billion |

| CAGR | CAGR of 3.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Testing, Inspection, Certification) • By Sourcing (In-House Sourcing, Outsourced) • By Application (Consumer Goods & Retail, Agriculture & Food, Chemicals, Infrastructure, Energy & Power, Education, Government, Manufacturing, Healthcare, Mining, Oil & Gas and Petroleum, Public Sector, Automotive, Aerospace & Defense, Supply Chain & Logistics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | SGS Group, Bureau Veritas, Eurofins Scientific, Apave International, IRClass, TIC Sera, Element Materials Technology, UL LLC, QR Testing, Hohenstein, Dekra Certification, ALS Limited, Intertek Group plc, SAI Global Limited, MISTRAS Group, TUV SUD, TUV Rheinland, DNV, Kiwa, and CTC Group. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Testing, Inspection, and Certification (TIC) Market in 2025.

Ans: The Testing segment dominated the Testing, Inspection, and Certification (TIC) Market.

Ans: Increasing consumer safety demand is leading to higher investments in TIC services to ensure quality standards are met.

Ans: Testing, Inspection, and Certification (TIC) Market size was USD 326.82 billion in 2025 and is expected to Reach USD 480.99 billion by 2035.

Ans: The Testing, Inspection, and Certification (TIC) Market is expected to grow at a CAGR of 3.94% during 2026-2035.

Get in Touch