Through Glass Vias (TGV) Substrate Market Size Analysis:

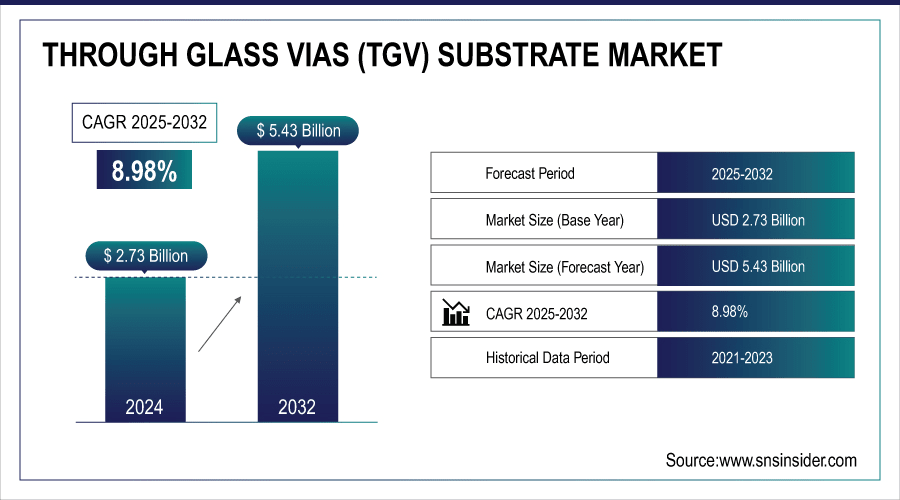

The Through Glass Vias (TGV) Substrate Market size was valued at USD 2.73 Billion in 2024 and is projected to reach USD 5.43 Billion by 2032, growing at a CAGR of 8.98% during 2025-2032.

The Through Glass Vias (TGV) Substrate Market is experiencing significant growth due to rising demand for miniaturized, high-performance electronic components across various sectors. The TGV technology achieves vertical electrical glass feedthroughs with good electrical insulating properties, low signal loss and high thermal stability. Its attributes make it suited for applications where high frequency operation and compactness are required. Meanwhile, the TGV substrates are also increasingly being used as they are providing higher I/O density for next generation devices and lower EMI concerns. Rapid market growth is being spurred by on-going yield, scalability, and cost-journey improvements.

To Get More Information On Through Glass Vias (TGV) Substrate Market - Request Free Sample Report

The E-Core Alliance (Taiwan’s E&R Engineering is the prime mover), which includes more than 15 members, is working on TGV-compatible glass substrates for AI chiplets, reportedly with via drilling speeds of 8,000 vias/sec. Among the other key partners are Manz AG, Scientech and ShyaWei Optronics, with the U.S. funding this work through the CHIPS Act.

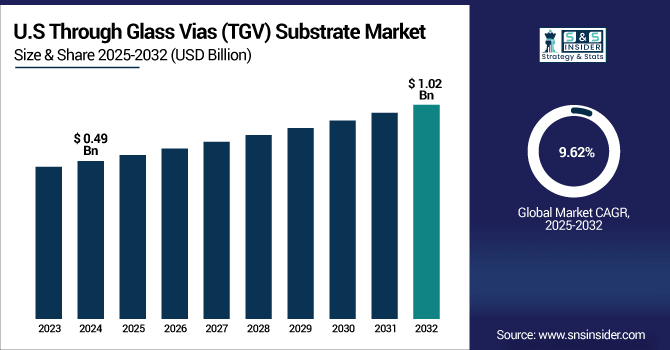

The U.S. Through Glass Vias (TGV) Substrate Market size was valued at USD 0.49 Billion in 2024 and is projected to reach USD 1.02 Billion by 2032, growing at a CAGR of 9.62% during 2025-2032. The country’s growth fueled by robust demand in automotive electronics, 5G network deployment, advanced semiconductor manufacturing and high-level data communication, driving Through Glass Vias (TGV) Substrate market growth.

Through Glass Vias Substrate Market Dynamics:

Drivers:

-

Rising AI Chip Complexity Fuels Industry Shift to Glass Substrates for Enhanced Signal Performance

The key driver for the Through Glass Vias (TGV) Substrate Market is the growing trend of the glass substrates in advanced semiconductor packages owing to the requirement for high performance and miniaturization in today's electronics. Glass provides excellent electrical insulating, flatness and low signal loss, which is suitable for AI chips and high-speed communication devices. With increasing complexity and power density on chips the need for increased connection and heat handling will add even further to this demand. The market is also propelled by strategic investments, such as government support programs, and collaborations, such as the E-Core Alliance, which has assembled global partners to fast track R&D, simplify supply chains and strengthen production capabilities to spur global expansion of glass base materials’ application in lieu of traditional materials.

Taiwan's E&R Engineering launched the E-Core System and formed the E-Core Alliance to promote glass substrates in advanced chipmaking. The coalition includes global firms like Manz AG and Scientech to deliver end-to-end glass substrate solutions.

Restraints:

-

Manufacturing Complexity and Cost Constraints Hinder Widespread Adoption of Glass TGV Substrates

A major restraint in the Through Glass Vias (TGV) Substrate market is the high manufacturing complexity and associated costs of processing glass substrates. Advanced processes, such as laser drilling, metallization, and via filling, require special apparatus and fine adjustment, resulting in high production costs. Early TGV suffered from slow via processing speed preventing high-volume production, and though faster processes are available they are still capex intensive. There is also a need for high accuracy and severe quality requirement to be met, which can also push up cost. These also hinder large-scale adoption, particularly for smaller manufacturers. As a result, although glass substrates are beneficial in terms of excellent performance, it is difficult to achieve mass production by meeting both performance and cost requirements of a product and rapid commercialization of the product is hindered.

Opportunities:

-

Thermal and Power Limitations in Current Packaging Propel Growth and Investment in Glass Substrate Technologies

The Through Glass Vias (TGV) Substrate Market presents significant opportunities driven by growth opportunity to fix the thermal, power, and cost challenges of current packaging technology solutions including HBM and CoWoS, addressing the challenge of high speed connectivity with dies packaged upon conventional interposer substrates, growing cooperatively with HBM and CoWoS, and overcoming the burning issue of Moore’s wall where lager chips need to access memory quicker and/or cheaper than the current methods. Next-generation AI chips and high-speed communication devices available Glass substrates have superior thermal resistance, lower warpage, and better signal transmission. Increasing investment from major industry players including Intel and AMD, and widespread supply chain networks in South Korea, simplify the process of rapid commercialization and scale-up. Moreover, increasing demand for miniaturization and high computing power in the consumer electronics, automotive, and telecom industries would contribute to market growth. manufacturers of TGV and inspection technologies are discovering new opportunities in this emerging landscape as well.

Challenges:

-

Technical Integration and Material Compatibility Challenges Delay Mass Production and Widespread Adoption of TGV Substrates.

The Through Glass Vias (TGV) substrate market is constrained by several critical challenges. The high cost and fact that TGV integration is a semiconductor manufacturing is unfortunately a factor of not producing standard products off a standard machine is an unfortunate reality. Thermal expansion mismatch control between glass and other materials also continues to be difficult, and there is increasing risk of damaging the substrate in handling and processing. One of the problems is that the glass substrate material and process is not well standardized, which makes the compatibility a problem through the supply chain. Additionally, the TGV laser drilling second through-put is slow as compared to traditional via formation processes, which further delays mass production schedules of the industry. Finally, strong ecosystem cooperation from equipment suppliers, material suppliers, and chipmakers delays the commercialization of TGV substrates and its wide utilization.

TGV Substrate Market Segmentation Analysis:

By Type

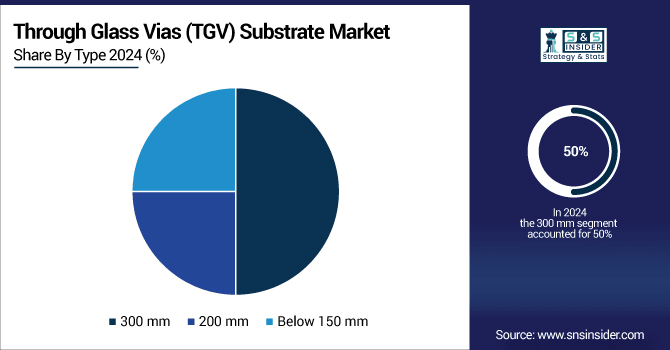

The 300 mm segment held a dominant Through Glass Vias (TGV) Substrate Market share of around 50% in 2024, and are witnessing widespread adoption owing to compatibility with the advanced semiconductor manufacturing process, which allows high throughput and meets the increasing demand for high-performance and miniaturized chips across AI and communication devices.

The 200 mm segment is expected to experience the fastest growth in the Through Glass Vias (TGV) Substrate Market over 2025-2032 with a CAGR of 10.02%. The increasing popularity of cost-effective, flexible substrates is driving growth for mid-tier semiconductor devices, which are driving innovations in industries, such as consumer electronics, automotive and communications across the globe.

By Application

The Consumer Electronics segment held a dominant Through Glass Vias (TGV) Substrate Market share of around 40% in 2024, propelled by rising popularity of efficient, miniature devices such as wearables, smartphones, and tablets. Miniaturization trends, combined with requirements for increased data rates, are driving the switch to TGV, resulting in more than doubling of the TGV growth.

The Automotive segment is expected to experience the fastest growth in the Through Glass Vias (TGV) Substrate Market over 2025-2032 with CAGR 13.09%. with the increasing deployment of ADAS, electric vehicles, and connected cars. The rapid expansion is driven by the growing need for dependable, miniaturized and high-performance electronic components.

By End-Use

The OEMs segment held a dominant Through Glass Vias (TGV) Substrate Market share of around 60% in 2024, owing to its innovators backed by advanced glass substrate technologies. By focusing on high-performance miniaturized chips for consumer electronics and automotive applications and by making significant investments in R&D and strategic partnerships, they increase the pace of market growth and expand the versatility of glass substrate applications globally.

The Automotive segment is expected to experience the fastest growth in the Through Glass Vias (TGV) Substrate Market over 2025-2032 with CAGR 10.55%. is driven by the increasing demand for advanced driver-assistance systems (ADAS), electric vehicles, and autonomous driving technologies. These applications require high-performance, reliable, and compact semiconductor components, which glass substrates with TGV technology can efficiently support due to their superior electrical performance, thermal stability, and miniaturization capabilities, fueling market expansion.

Through Glass Vias (TGV) Substrate Market Regional Outlook:

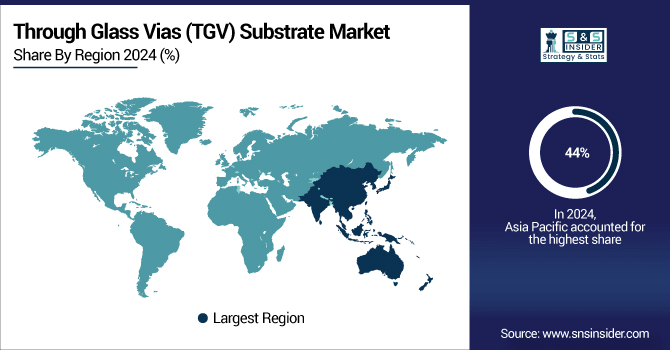

In 2024, the Asia Pacific dominated the Through Glass Vias (TGV) Substrate market and accounted for 44% of revenue share, due to a well-established infrastructure for semiconductor production, heavy investments by major chipmakers, and the growth in the adoption of advanced packaging technologies. Shift in the APAC region towards innovation, along with rising adoption of AI, 5G, and high-speed communication devices accelerate the market growth.

Get Customized Report as Per Your Business Requirement - Enquiry Now

China leads the Asia Pacific Through Glass Vias (TGV) Substrate market, driven by rapid semiconductor manufacturing growth, government support, and increasing demand for advanced electronics in consumer, automotive, and telecom sectors.

North America is projected to register the fastest CAGR of 10.68% during 2025-2032, due to high investments in semiconductor manufacturing, rising demand for high-performance electronics, technological improvements in 5G and AI, and surge in uptake of electric vehicles, and IoT devices, which result in demand for advanced substrate solutions across the region.

The U.S. leads the TGV substrate market due to strong semiconductor infrastructure, rising demand for compact electronics, and growing applications in 5G, photonics, and medical device technologies.

In 2024, Europe emerged as a promising region in the Through Glass Vias (TGV) Substrate market, led by the growing semiconductor self-sufficiency concerns among nations, government incentives for advanced manufacturing, and the escalating demand from the automotive and the consumer electronics industry along with the growing investments on the 5G infrastructure and renewable energy technologies, which had been driving the adoption of substrates across industries.

LATAM and MEA is experiencing steady growth in the Through Glass Vias (TGV) Substrate market, due to the growth in electronics manufacturing, increased in the uptake of smart devices, growing spending in infrastructure and demand for more substrates from the automotive industry and telecommunications which is catering to an increase in the substrate in the emerging regions.

Key Players:

The Through Glass Vias (TGV) Substrate market companies are Corning Incorporated, Samsung Electro-Mechanics, Amkor Technology, Inc., ASE Group, Taiwan Semiconductor Manufacturing Company (TSMC), Shinko Electric Industries Co., Ltd., Unimicron Technology Corporation, Ibiden Co., Ltd., Kinsus Interconnect Technology Corp., Onto Innovation, LPKF Laser & Electronics SE. and Others.

Recent Developments:

-

In May 2025, Nippon Electric Glass has developed two types of large TGV glass core substrates for next-gen semiconductor packages, featuring laser modification/etching and CO₂ laser processing, now available as samples.

-

In April , 2025, Onto Innovation and LPKF joined forces to enhance high-volume manufacturing of advanced glass substrates by integrating Onto’s Firefly inspection system at LPKF’s Hannover facility, boosting quality control for semiconductor panel-level packaging.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.73 Billion |

| Market Size by 2032 | USD 5.43 Billion |

| CAGR | CAGR of 8.98% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (300 mm, 200 mm and Below 150 mm) • By Application (Consumer Electronics, Automotive, Healthcare, Aerospace and Defense, Telecommunications and Others) • By End User (OEMs, ODMs and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | The Through Glass Vias (TGV) Substrate market companies are Corning Incorporated, Samsung Electro-Mechanics, Amkor Technology, Inc., ASE Group, Taiwan Semiconductor Manufacturing Company (TSMC), Shinko Electric Industries Co., Ltd., Unimicron Technology Corporation, Ibiden Co., Ltd., Kinsus Interconnect Technology Corp., Onto Innovation, LPKF Laser & Electronics SE.AND Others. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Through Glass Vias (TGV) Substrate Market in 2024.

Ans: The “300 mm” segment dominated the Through Glass Vias (TGV) Substrate Market .

Ans: Key drivers of the Through Glass Vias (TGV) Substrate Market include increasing demand for miniaturized and high-performance electronic devices and advancements in 3D packaging technology.

Ans: The Through Glass Vias (TGV) Substrate was USD 2.73 Billion in 2024 and is expected to Reach USD 5.43 Billion by 2032.

Ans: The Through Glass Vias (TGV) Substrate Market is expected to grow at a CAGR of 8.98% during 2025-2032.

Get in Touch