Trulicity Market Report Scope & Overview:

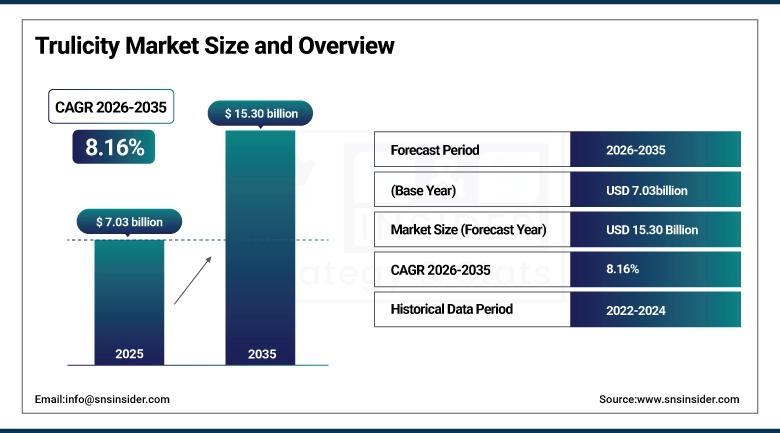

The Trulicity Market size is valued at USD 7.03 Billion in 2025 and is projected to reach USD 15.30 Billion by 2035, growing at a CAGR of 8.16% during the forecast period 2026–2035.

The Trulicity Market analysis report evaluates the market dynamics, new drug developments, and therapeutic applications of the product. The growth in type 2 diabetes and obesity incidences, increasing use of GLP-1 receptor agonists, growing indications in the cardiovascular space, and strengthening healthcare infrastructure are some key factors influencing strong market growth from 2026 to 2035.

Trulicity was used more than 2 billion times as a prescription drug in 2025, owing to the rising number of diabetes patients, growing obesity rates, and increased use of GLP-1 by physicians for metabolic and cardiovascular diseases.

Trulicity Market Size and Forecast:

-

Market Size in 2025: USD 7.03 Billion

-

Market Size by 2035: USD 15.30 Billion

-

CAGR: 8.16% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Trulicity Market - Request Free Sample Report

Trulicity Market Trends:

-

The increasing number of individuals with type 2 diabetes and obesity will continue to drive the uptake of GLP 1 treatments.

-

Entry into obesity and cardiovascular conditions will widen the indications for Trulicity to include beyond diabetes alone.

-

The move toward high dose regimens (3.0 mg and 4.5 mg) to boost efficacy for weight management and advanced disease states.

-

Increase in at-home self-administration through pens and telehealth support is anticipated.

-

The Asia Pacific becomes the fastest-growing region due to the growing number of diabetics in India and China.

-

E-commerce/pharmacies online become more prevalent, owing to increased digital health acceptance and convenience.

-

Reimbursement pressures and pricing concerns become an issue in Europe and developing markets.

-

Expiration of patents and biosimilars will be a reality after 2030.

-

Semaglutide (Ozempic/Wegovy, Mounjaro) is emerging competition in obesity and diabetes segments.

-

High risk overlapping populations with aging populations increase steadily the demand for Trulicity.

U.S. Trulicity Market Insights:

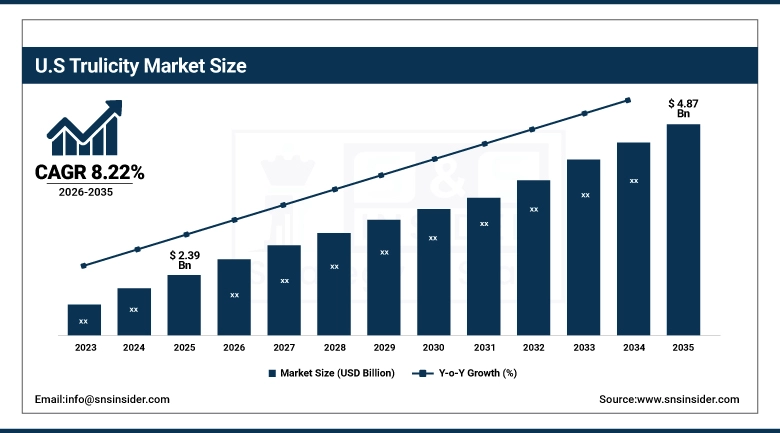

The U.S. Trulicity Market is projected to grow from USD 2.39 Billion in 2025 to USD 4.87 Billion by 2035, at a CAGR of 8.22%. The growth will be fueled by the increasing incidence of type 2 diabetes and obesity, higher usage of GLP 1 receptor agonists for metabolic and cardiovascular management, high acceptance of novel biologics, and innovative investment in novel injectable pen delivery systems.

Trulicity Market Growth Drivers:

-

Rising prevalence of type 2 diabetes and obesity is driving demand for advanced GLP‑1 receptor agonist therapies.

Cardiovascular risk reduction and metabolic disorders are major factors driving the adoption of Trulicity by the market. Biologic drugs such as Trulicity injectables with greater dosages and new technologies for better efficiency have gained popularity in hospitals, retail pharmacies, specialty clinics, and home care settings due to their benefits in managing glycaemia, obesity, and cardiovascular risk. Improved efficacy and safety, along with easy application and increased patient compliance, are contributing to increased demand, better clinical effectiveness, and continued expansion of the market.

Over 58% of hospitals, retail pharmacies, and specialty clinics were using Trulicity formulations to treat diabetes, obesity, and cardiovascular risk in 2025.

Trulicity Market Restraints:

-

Pricing pressures, reimbursement challenges, and competition from alternative GLP‑1 therapies are key restraints on Trulicity market growth.

Cost containment regulations will apply to hospitals, retail pharmacies, and specialized clinics, especially in Europe and developing countries. The expiration of patents after 2030 could allow biosimilars to come into the market and disrupt the leadership position of Eli Lilly. Another major threat is increased competition from new-generation GLP 1 medication from Novo Nordisk (Ozempic / Wegovy). Furthermore, limitations on patient access to healthcare services in poor areas, regulatory issues with broader indications, and safety concerns associated with prolonged treatment periods could also act as barriers to entry.

In 2025, over 42% of health professionals noted difficulties with costs and reimbursements when considering Trulicity as their primary medication choice.

Trulicity Market Opportunities:

-

Growing expansion of GLP‑1 receptor agonists into obesity management and cardiovascular risk reduction presents significant opportunities for the Trulicity market.

The healthcare providers in clinical settings and distribution network providers have embraced advanced biological treatments to deal with the two conditions, that is, obesity and diabetes. This development can be exploited by the pharmaceutical manufacturers as they introduce higher-dose and patient-friendly Trulicity formulation and also explore other uses of their products. The constant improvement in the injectable drug delivery systems, increased safety and efficacy, and patient adherence are factors promoting the usage.

As of 2025, more than 47% of the healthcare providers embraced Trulicity in managing both obesity and diabetes and even cardio risks.

Trulicity Market Segmentation Analysis:

-

By Therapeutic Application, Type 2 Diabetes (primary indication) held the largest market share of 59.38% in 2025, while Obesity/weight management (emerging use) are expected to grow at the fastest CAGR of 9.68% during 2026–2035.

-

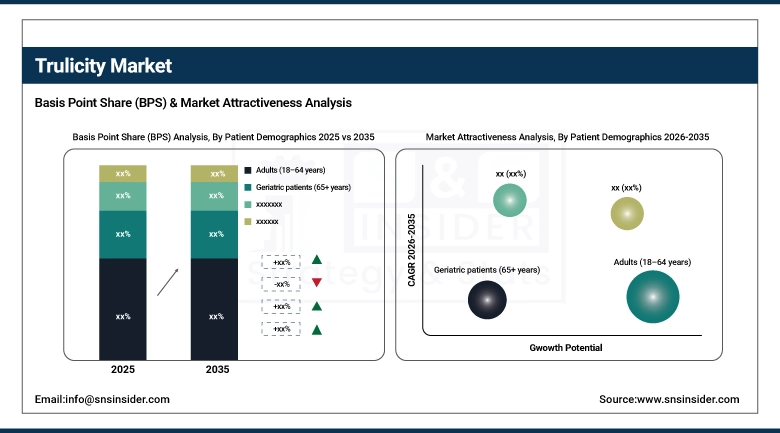

By Patient Demographics, Adults (18–64 years) dominated with 54.69% market share in 2025, whereas High-risk populations (obese + diabetic overlap) are projected to record the fastest CAGR of 10.93% through 2026–2035.

-

By Distribution Channel, Hospital pharmacies accounted for the highest market share of 29.87% in 2025, while online/e-commerce pharmacies are expected to grow at the fastest CAGR of 9.60% during the forecast period.

-

By Dosage & Formulation, 1.5 mg once weekly pen dominated with a 24.56% share in 2025, while 4.5 mg once weekly pen are anticipated to expand at the fastest CAGR of 9.70% through 2026–2035.

By Therapeutic Application, Type 2 Diabetes (primary indication) Dominate While Obesity/Weight Management (emerging use) Grow Rapidly:

Type 2 Diabetes (the primary indication) constitutes the dominant part of the market due to the drug's effectiveness in treating diabetes and wide application among healthcare professionals. The preference for Trulicity can be attributed to the proven effectiveness of the medication, the ease of taking it only once per week, and good safety. The treatment area constitutes the mainstay of Trulicity's market position, being widely prescribed in healthcare facilities.

Obesity/Weight Management (emerging use) has become the most fastest growing indication due to the increase in the number of obese people, increased knowledge about the use of GLP 1 drugs to treat obesity, and the willingness of physicians to prescribe high-dose formulations of Trulicity.

By Patient Demographics, Adults (18–64 years) Dominate While High‑risk populations (obese + diabetic overlap) Grow Rapidly:

The Adults (18-64 years old) form the dominant share of the market, owing to the extensive occurrence of type 2 diabetes and obesity among this population. Clinical acceptance and physician endorsement of GLP 1 drugs in treating metabolic diseases are the driving factors behind the prominence of Trulicity as a leading medication. This segment enjoys the advantages of administering the drug on a weekly basis.

High-risk individuals (obese + diabetic overlap) are one of the fastest-growing segments in the market due to their need for dual-action drugs and the effectiveness of large-dose drugs in controlling their medical issues. The increasing knowledge about dual-action medications and the effectiveness of Trulicity in addressing health issues such as weight loss and reducing cardiovascular risks are the main drivers of growth among this segment.

By Distribution Channel, Hospital pharmacies Dominate While Hospital Pharmacies Grow Rapidly:

The Hospital Pharmacy sector continues to be the dominant segment due to high prescription rates by physicians and well-defined treatment methods for managing chronic diseases. The hospitals will still be playing a vital role in starting patients on medication and making sure they have access to new biologic drugs.

The Online and e-commerce Pharmacies have experienced fastest growth as a result of health technology uptake, consumer demand for convenience, and increased use of GLP 1-based treatments through the web platform. This sector has disrupted the access paradigm and is expected to be a key driver for future growth within the market.

By Dosage & Formulation, 1.5 mg once‑weekly pen Dominates While 4.5 mg once‑weekly pen Grow Rapidly:

The 1.5 mg once weekly pen segment is the most dominant one due to its optimal combination of efficiency, tolerance, and reliability for treating diabetes in the long run. This dosage continues to be the recommended option for the treatment of the condition in question. Its widespread physician preference and patient adherence make it the standard starting dose, reinforcing its role as the backbone of Trulicity’s therapeutic portfolio.

The 4.5 mg once weekly pen segment that should be taken once a week is among the formulations that show the fastest rates of adoption due to the best results achieved regarding weight loss and more effective glycemic control. The importance of this type of pen will continue to increase in light of obesity treatment.

Trulicity Market Regional Analysis:

North America Trulicity Market Insights:

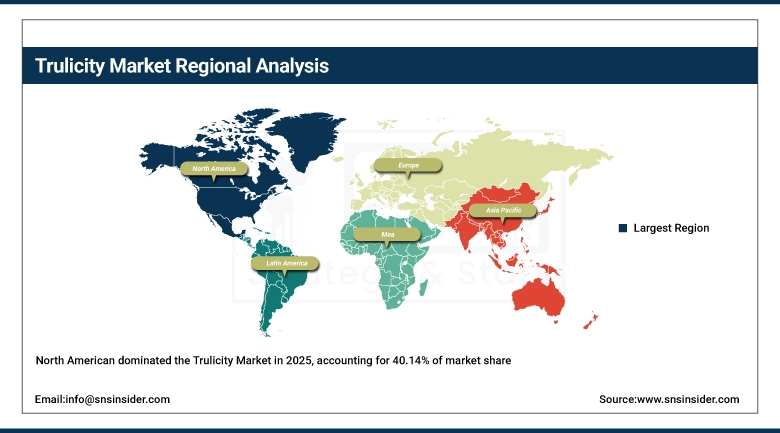

North America dominates the world Trulicity market with 40.14% share, due to the presence of advanced healthcare facilities, presence of high levels of diabetes and obesity cases, and good reimbursements schemes. The use of GLP 1 therapies by doctors, alongside advancements in high doses of this therapy, contribute to North America's dominance in this field. Telemedicine and online pharmacies contribute toward greater access for patients. Consistent research and investments in the metabolic sector assure that North America will remain the dominant force in Trulicity markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Trulicity Market Insights:

The U.S. is the largest market for Trulicity due to the widespread use of healthcare services, advanced medical practices, and physician confidence in GLP 1 treatments. Increased cases of obesity and the adoption of risk management plans to manage cardiovascular disease are fueling uptake. The willingness to use once-weekly injection pens and favorable insurance structures makes it easy to adopt the drug. Improvements made through dosage innovations and obesity treatments make it the leading consumer of Trulicity.

Asia Pacific Trulicity Market Insights:

Asia-Pacific region has emerged as one of the fastest-growing regions with CAGR of 9.23%, driven by an increase in the number of cases of diabetes in India and China, improved healthcare facilities, and increased knowledge about obesity. Governments are spending a lot of money on their chronic disease initiatives, while digital technology is helping patients access better treatment. Drug companies are positioning themselves in this region through low-cost drugs and extensive distribution networks.

China Trulicity Market Insights:

China's Trulicity market is growing extremely fast due to the fact that China is home to some of the largest populations of diabetics, and increasing cases of obesity. The government's plans to boost chronic care management and increase the penetration rate of biologicals are contributing immensely toward the growth of the market. Through partnerships with local firms and distribution of products in various parts of the country, China is becoming an increasingly important part of Asia Pacific's growth story.

Europe Trulicity Market Insights:

Europe boasts a robust Trulicity presence driven by the sophistication of its healthcare infrastructure, the level of awareness about metabolic diseases, and well-established reimbursement systems. The use of the drug is fairly universal among both hospitals and specialists’ offices, even as prices become a concern along with stringent regulations. Increased programs related to weight loss and cardiovascular prevention contribute to market expansion. Consistent development in biologics and delivery technologies ensures sustained relevance of Trulicity.

Germany Trulicity Market Insights:

Germany is one of the key markets of Europe for Trulicity due to a good health care system and coverage and high physician acceptance. The increase in obesity rates and development of cardiovascular disease prevention programs drives the need for Trulicity. Hospitals and specialized centers play a leading role in prescribing Trulicity and other GLP-1 drugs, while the retail pharmacy market and the internet pharmacies also contribute significantly.

Latin America Trulicity Market Insights:

The Latin American Trulicity market is expanding at a steady pace due to higher incidences of diabetes and obesity, increased access to healthcare services, and better understanding of GLP 1 treatments among doctors. Brazil and Mexico are the top markets, helped by national programs focused on chronic disease management. Although there are issues related to reimbursement and costs, the expansion of retail pharmacies and online pharmacy platforms has enhanced patient access.

Middle East & Africa Trulicity Market Insights:

The Middle East & Africa segment is still evolving, with increased instances of diabetes and obesity fuelling the need for novel treatments. The GCC countries, owing to their well-established healthcare system and favourable reimbursement environment, have been at the forefront of adoption. Although there are still constraints regarding access and cost in Africa, with increasing healthcare spending and collaborations, the landscape is expected to become favourable for Trulicity in the long run.

Trulicity Market Competitive Landscape:

Eli Lilly and Company is one of the top U.S.-based pharmaceutical companies that produce Trulicity, putting it at the vanguard of the GLP 1 receptor agonist industry. Eli Lilly’s commitment to metabolic disorders and the advancements in weekly injections using a pen have further strengthened its position as a market leader. The efforts made by Eli Lilly in developing high doses, widening cardiovascular indications, and partnering in R&D activities are expected to sustain its market leadership position.

-

In June 2025, Eli Lilly advanced its pipeline with tirzepatide (Mounjaro), expanding obesity and diabetes indications alongside Trulicity, strengthening its GLP‑1 portfolio.

Novo Nordisk is one of the largest pharmaceutical companies in Denmark and specializes in the development of diabetes and obesity medications. With popular GLP-1 products including Ozempic and Wegovy, Novo Nordisk rivals Trulicity for metabolic disorders. The focus of the company is on developing cutting-edge solutions for weight management, lowering risk factors associated with heart diseases, and improving drug delivery methods.

-

In August 2025, Novo Nordisk expanded Wegovy’s approval for cardiovascular risk reduction, enhancing its role beyond obesity management and intensifying competition with Trulicity.

Pfizer Inc. is a renowned American pharmaceuticals company whose drug portfolio includes biologics and medicines for metabolism and cardiac issues. Although not the creator of Trulicity, Pfizer has a substantial stake in the market for treating diabetes and obesity by virtue of collaborations, biosimilar products, and biologics. This position is made possible by Pfizer’s commitment to developing innovative treatments and robust logistics.

-

In December 2025, Pfizer advanced its metabolic pipeline with early‑stage GLP‑1 and dual agonist candidates, aiming to expand its footprint in obesity and diabetes care.

Trulicity Market Key Players:

-

Eli Lilly

-

Novo Nordisk

-

Pfizer

-

Sanofi

-

AstraZeneca

-

Merck & Co.

-

Johnson & Johnson

-

GlaxoSmithKline (GSK)

-

Boehringer Ingelheim

-

Amgen

-

Roche

-

Novartis

-

Takeda Pharmaceutical

-

Bayer AG

-

Bristol Myers Squibb

-

Teva Pharmaceuticals

-

Cipla

-

Sun Pharma

-

Dr. Reddy’s Laboratories

-

Lupin

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.03 Billion |

| Market Size by 2035 | USD 15.30 Billion |

| CAGR | CAGR of 8.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Therapeutic Application (Type 2 Diabetes (primary indication), Obesity/Weight Management (emerging use), Cardiovascular Risk Reduction, Metabolic Disorders (potential pipeline expansion), Others), • By Patient Demographics (Adults (18–64 Years), Geriatric Patients (65+ Years), Pediatric/Adolescent (off-label/clinical trials), High-Risk Populations (obese + diabetic overlap), Others), • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online/E-commerce Pharmacies, Specialty Clinics, Others), • By Dosage & Formulation (1.5 mg Once Weekly Pen, 0.75 mg Once Weekly Pen, 3.0 mg Once Weekly Pen, 4.5 mg Once Weekly Pen, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Eli Lilly, Novo Nordisk, Pfizer, Sanofi, AstraZeneca, Merck & Co., Johnson & Johnson, GlaxoSmithKline (GSK), Boehringer Ingelheim, Amgen, Roche, Novartis, Takeda Pharmaceutical, Bayer AG, Bristol Myers Squibb, Teva Pharmaceuticals, Cipla, Sun Pharma, Dr. Reddy’s Laboratories, Lupin. |

Frequently Asked Questions

North America dominated with a 40.14% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 9.23% during 2026–2035.

Type 2 Diabetes (primary indication) dominated with a 59.38% share in 2025, while Obesity/weight management (emerging use) are projected to grow at the fastest CAGR of 9.68% during 2026–2035.

Increasing adoption of GLP‑1 receptor agonists for both metabolic and cardiovascular indications, expanding healthcare access and reimbursement programs, and ongoing innovation in higher‑dose formulations and convenient delivery devices

The market is valued at USD 7.03 Billion in 2025 and is projected to reach USD 15.30 Billion by 2035.

The Trulicity Market is projected to grow at a CAGR of 8.16% during 2026–2035.

Get in Touch