Upstream Petrotechnical Training Services Market Report Scope & Overview:

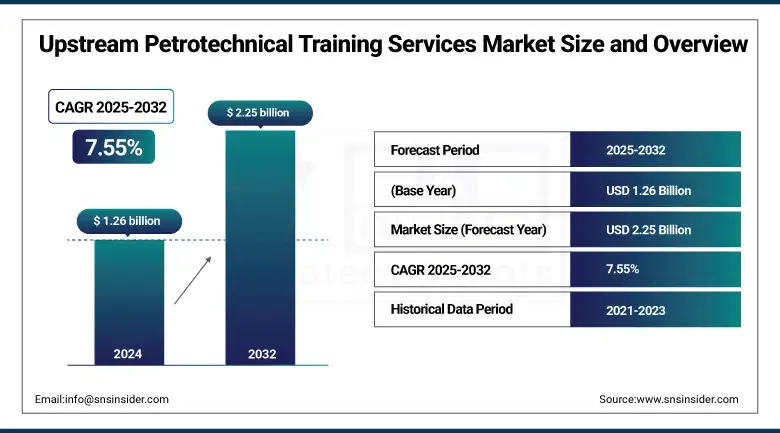

The Upstream Petrotechnical Training Services Market Size was valued at USD 1.26 billion in 2024 and is expected to reach USD 2.25 billion by 2032 and grow at a CAGR of 7.55% over the forecast period 2025-2032.

The market addresses the growing need for skilled professionals in oil and gas exploration and production. It offers technical instruction in disciplines such as geoscience, drilling, reservoir management, and production operations. As the industry embraces digital transformation and faces an aging workforce, demand for innovative training methods, like virtual simulations, cloud-based platforms, and blended learning, continues to grow. Energy companies are investing in workforce upskilling to maintain operational efficiency and meet safety and environmental standards. This market plays a critical role in sustaining the technical capabilities required to navigate increasingly complex and data-driven upstream environments.

To Get more information On Upstream Petrotechnical Training Services Market - Request Free Sample Report

According to the study, the rising complexity of upstream oil and gas operations has led to increased demand for specialized petrotechnical training services. As experienced professionals retire, companies face a growing skills gap, driving the adoption of digital learning tools and simulation-based training. This shift has resulted in higher enrollment across online platforms and customized corporate programs. With over 60% of E&P firms prioritizing workforce upskilling, training providers are expanding offerings to support evolving operational and technological needs.

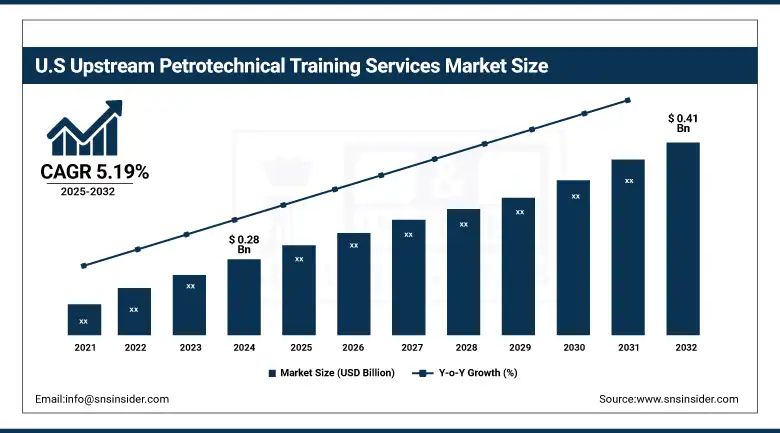

The U.S. Upstream Petrotechnical Training Services Market size was USD 0.28 billion in 2024 and is expected to reach USD 0.41 billion by 2032, growing at a CAGR of 5.19% over the forecast period of 2025–2032.

The U.S. market is primarily driven by rising demand for skilled technical professionals and rapid digital transformation across oil and gas operations. The U.S. dominates the North American market due to its high concentration of active upstream projects and major E&P firms. This leads to increased investment in advanced training platforms and simulation-based learning, reinforcing the country’s leadership in upstream petrotechnical workforce development.

Market Dynamics

Key Drivers:

-

Increased Adoption of Digital Oilfield Technologies in Exploration and Production Drives Upstream Petrotechnical Training Services Market Growth

The growing reliance on digital oilfield technologies such as advanced seismic imaging, AI-driven reservoir modeling, and real-time data monitoring is significantly boosting the demand for upstream petrotechnical training services. As exploration and production (E&P) operations become increasingly digitized, there is a pressing need for a highly skilled workforce proficient in these emerging tools. Companies are prioritizing workforce training to enhance operational efficiency, reduce downtime, and improve safety across upstream projects.

The result is a surge in enrollments for technical training, particularly in regions like the Middle East and North America, where upstream activity is high. These advancements are not only improving job readiness among professionals but are also ensuring compliance with evolving regulatory and safety standards. Thus, the proliferation of digital oilfield technologies is a core driver fueling the growth of the upstream petrotechnical training services market.

Restraints:

-

High Cost of Customized Technical Training Solutions Limits Upstream Petrotechnical Training Services Market Expansion

The high cost associated with developing and delivering customized petrotechnical training programs is restraining the expansion of the upstream training services market. Companies operating in the upstream oil and gas sector often require tailored training solutions that match their specific operational processes, equipment, and regional compliance requirements. Designing these bespoke programs involves significant investment in subject matter expertise, software development, and simulation tools, which can be cost-prohibitive for smaller firms or those operating in price-sensitive markets.

Moreover, the need for continual updates in training content to keep pace with rapidly evolving technologies adds to the financial burden. Many companies hesitate to allocate sufficient training budgets, especially during periods of oil price volatility or reduced capital expenditures. This reluctance creates a gap between technological adoption and workforce readiness, ultimately impacting productivity and safety. Additionally, the lack of scalable, cost-effective training models discourages widespread adoption in emerging markets. As a result, while the need for specialized training is growing, the associated costs are a significant barrier that limits the overall market potential for upstream petrotechnical training services.

Opportunities:

-

Expansion of Offshore Drilling Projects in Latin America Creates Lucrative Opportunities for Upstream Petrotechnical Training Services Market Providers

The increasing investments in offshore drilling activities, especially across Latin America, are opening up lucrative opportunities for upstream petrotechnical training service providers. Countries like Brazil and Guyana are ramping up offshore exploration, fueled by recent deepwater discoveries and supportive government policies. This rapid expansion requires a new generation of technically skilled professionals trained in offshore-specific operations, including subsea engineering, drilling safety, and environmental compliance. Training providers are responding by developing region-specific programs and partnering with local institutions to enhance accessibility.

For instance, in May 2025, PetroSkills announced a new partnership with a Brazilian technical institute to launch bilingual offshore training programs aligned with national oil company (NOC) requirements. These developments are vital to meeting the operational demands of new offshore projects, which often involve high-risk environments and advanced technologies.

Challenges:

-

Shortage of Experienced Trainers and Instructors Hampers Quality and Accessibility in Upstream Petrotechnical Training Services Market

The limited availability of qualified instructors with hands-on upstream oil and gas experience is a major challenge hindering the growth of the petrotechnical training services market. As the industry evolves with new technologies and operational complexities, the demand for instructors who can provide real-world insights and contextually relevant training has surged.

However, many experienced professionals are nearing retirement, and the pipeline of new talent entering the instructional field is insufficient to fill the gap. This shortage affects both the quality and scalability of training programs, particularly in specialized domains such as enhanced oil recovery, deepwater drilling, and geomechanics. As a result, training institutions often struggle to maintain program standards and are forced to rely on less experienced personnel or outdated teaching methods.

Additionally, the lack of qualified trainers can delay training schedules, particularly in remote or offshore locations where accessibility is already a constraint. This challenge is further exacerbated in developing regions, where industry-academic linkages are weak. Consequently, the shortage of skilled instructors poses a serious hurdle to building a technically proficient workforce and sustaining the long-term growth of the upstream petrotechnical training services market.

Segmentation Analysis:

By Training Type

The Training Courses segment held the largest revenue share of 35% in 2024, driven by its standardized approach and accessibility across global upstream operations. As E&P companies prioritize consistent competency frameworks, training courses, especially those accredited by institutions like IWCF and IADC, have become essential. Product development includes modular e-learning, adaptive testing, and multilingual platforms. The growing focus on regulatory compliance and cross-functional skillsets is boosting the adoption of formal courses, thereby strengthening this segment’s impact on the upstream petrotechnical training services market.

The Simulator (Immersive Training) segment is projected to grow at a CAGR of 16.52%, fueled by increased demand for realistic, hands-on learning experiences. As offshore drilling and deepwater projects become more complex, companies seek VR/AR-based simulators for safe, scenario-based training. In 2024, Schlumberger introduced a 4D simulator for live well-control practices. These advancements enhance situational awareness and decision-making, directly correlating with safer and more efficient operations in the upstream petrotechnical training services market.

By Training Mode

Operational Training dominated the market with a 25% share in 2024, primarily because of its direct role in improving on-site safety, procedural efficiency, and equipment handling. With increasing automation in drilling and completion operations, field staff require practical instruction on real-time operations. These targeted programs reduce human error and improve asset performance, making operational training a cornerstone of upstream petrotechnical training services.

Information Management training is expanding rapidly at a 19.23% CAGR, as E&P firms contend with vast volumes of subsurface and production data. With AI, cloud computing, and digital twins becoming mainstream, training in data curation, cybersecurity, and digital workflows is crucial. This digital transformation fuels the demand for specialized training in information systems, directly impacting growth within the upstream petrotechnical training services market.

By Upstream Sector

The Exploration segment commanded a 44% revenue share in 2024, attributed to the critical need for specialized knowledge in geophysics, seismic interpretation, and basin modeling. As upstream firms target untapped reserves, they rely on high-skill training for accurate risk assessment and data interpretation. The complexity and capital intensity of exploration necessitate continuous upskilling, reinforcing this segment’s dominance in the upstream petrotechnical training services market.

The Development segment is growing at a CAGR of 10.38%, driven by the adoption of advanced recovery methods such as waterflooding, CO₂ injection, and horizontal drilling. Training needs have expanded to include reservoir simulation, completions design, and production optimization. As companies seek to maximize output from existing fields, the development phase drives continuous learning, significantly shaping the upstream petrotechnical training services market.

By End-User

National Oil Companies (NOCs) led the market with a 59% revenue share in 2024, reflecting their scale, government backing, and workforce nationalization mandates. These firms often invest heavily in in-house academies and partnerships with global providers. The NOCs’ strategic role in regional energy security ensures robust demand for skill development, making them the largest end-user group in the upstream training services market.

Independent Oil Companies (IOCs) are expanding at a CAGR of 9.06%, driven by their agile approach and growing investment in unconventional plays. Unlike large NOCs or majors, IOCs prefer modular, cloud-based, and virtual training tools to stay cost-efficient. In 2024, an independent U.S. E&P firm adopted AI-based training analytics for performance monitoring. Their focus on maximizing ROI and minimizing downtime fuels demand for modern, scalable training solutions, reinforcing this segment’s growing influence in the upstream petrotechnical training services market.

Regional Analysis:

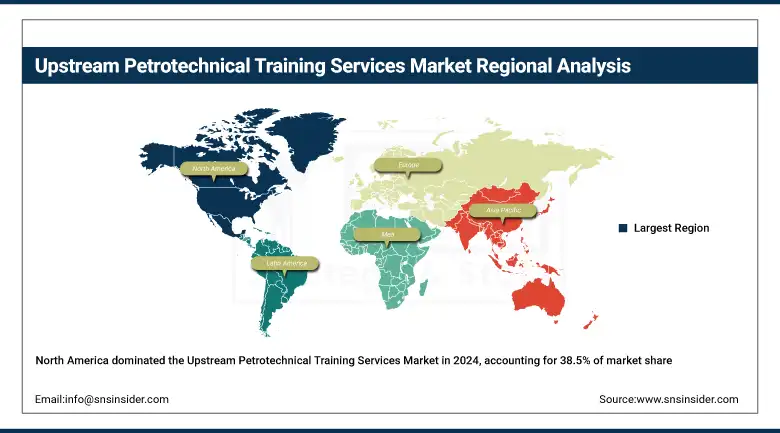

North America is the dominant region in the Upstream Petrotechnical Training Services Market in 2024, with an estimated market share of 38.5%. High shale production, digital oilfield integration, and a mature upstream workforce drive North America’s leadership in the petrotechnical training market. The United States leads the region, backed by intensive exploration in the Permian Basin, widespread adoption of simulation-based learning, and strong regulatory compliance. In 2024, U.S.-based training firms introduced AI-powered learning analytics and real-time well-control simulators. These innovations reinforce the U.S. as the central hub for advanced, safety-focused, and digitally enabled upstream training solutions in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region in the Upstream Petrotechnical Training Services Market in 2024 with an estimated CAGR of 15.6%. Accelerating offshore exploration, growing domestic energy demand, and government-backed skill development programs fuel Asia Pacific’s training market growth. China dominates this fast-growing region due to rising investment in deepwater projects and national mandates for technical workforce upskilling. In 2024, Chinese firms deployed immersive VR-based training platforms and expanded petroleum institutes in coastal cities. Supported by upstream digitalization and localized curriculum development, China is positioning itself as the training and technology engine of Asia Pacific’s evolving energy landscape.

Europe’s Regulatory Focus and Aging Offshore Infrastructure Drive the Upstream Petrotechnical Training Services Market in 2024. Strict compliance standards, safety mandates, and the need to modernize operations in mature fields sustain Europe’s demand for petrotechnical training. Norway leads the region, driven by extensive North Sea operations, cutting-edge offshore innovation, and sustained investment in digital training platforms. In 2024, Norwegian providers launched cloud-integrated simulators for subsea systems and decommissioning workflows. With advanced oilfield technologies and a future-ready workforce, Norway anchors Europe’s specialized and compliance-driven upstream training environment.

In 2024, the Upstream Petrotechnical Training Services Market in the Middle East & Africa (MEA) and Latin America gains momentum through nationalization policies and offshore project expansion. In MEA, Saudi Arabia leads, backed by state-owned initiatives like Saudi Aramco’s training academies and a focus on upstream localization. Riyadh’s investment in immersive, multilingual training tools strengthens regional capabilities. In Latin America, Brazil dominates due to extensive deepwater activity and Petrobras-led training partnerships. In 2024, both regions saw upgrades in digital content delivery and offshore simulator labs, helping build scalable, high-impact training systems in geographies focused on maximizing upstream productivity and talent development.

Key Players:

The upstream petrotechnical training services market companies are The Society of Petroleum Engineers, International Association of Drilling Contractors, The European Association of Geoscientists and Engineers, The Society of Exploration Geophysicists, American Petroleum Institute, Total S.A., Royal Dutch Shell, Baker Hughes, Halliburton, Intertek Group plc., RPS Group PLC, PetroKnowledge, Novomet Group, Aucerna, International Human Resources Development Corporation, Asia Edge Pte Ltd., Petroskills, IFP Training, PetroEdge, and HOT Engineering GmbH, and Others.

Recent Developments:

-

December 2024: IADC expanded its network of accredited training providers by accrediting eight new organizations. This expansion enhances global access to industry-standard well control, managed‑pressure‑drilling, and drilling safety training, key aspects of upstream petrotechnical education for drilling operations globally.

-

May 2025: EAGE launched a new series of 11 short courses as part of its first semester 2025 catalogue. Offered in classroom, online, and in-house formats, these include upstream-focused modules such as Full Waveform Inversion, VSP Technology & DAS, and Structural Geology, all relevant to petrotechnical training in exploration and reservoir characterization.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.26 Billion |

| Market Size by 2032 | USD 2.25 Billion |

| CAGR | CAGR of 7.55% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Training Type (Training Courses, Face-To-Face, In-House, Online, E-Learning, Simulator [Immersive Training]) • By Training Mode (Operational Training, Information Management, Health, Safety & Environment [HSE], Domain Training, Geology & Geophysics, Petrophysics, Surface Facilities Design & Engineering, Geomechanics, Field Operations & Management, Reservoir Engagement, Drilling Engineering, Other [Production Engineering, Economics & Finance]) • By Upstream Sector (Exploration, Development, Production) • By End-User (National Oil Companies, Independent Oil Companies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Society of Petroleum Engineers, International Association of Drilling Contractors, The European Association of Geoscientists and Engineers, The Society of Exploration Geophysicists, American Petroleum Institute, Total S.A., Royal Dutch Shell, Baker Hughes, Halliburton, Intertek Group plc., RPS Group PLC, PetroKnowledge, Novomet Group, Aucerna, International Human Resources Development Corporation, Asia Edge Pte Ltd., Petroskills, IFP Training, PetroEdge, and HOT Engineering GmbH. |

Frequently Asked Questions

Ans: North America dominated the Upstream Petrotechnical Training Services Market in 2024.

Ans: The Training Courses segment dominated the Upstream Petrotechnical Training Services Market.

Ans: The major growth factor of the Upstream Petrotechnical Training Services Market is the increasing adoption of advanced digital oilfield technologies requiring specialized technical workforce training.

Ans: The Upstream Petrotechnical Training Services Market size was USD 1.26 billion in 2024 and is expected to reach USD 2.25 billion by 2032.

Ans: The Upstream Petrotechnical Training Services Market is expected to grow at a CAGR of 7.55% during 2025-2032.

Get in Touch