Procurement As a Service Market Report Scope & Overview:

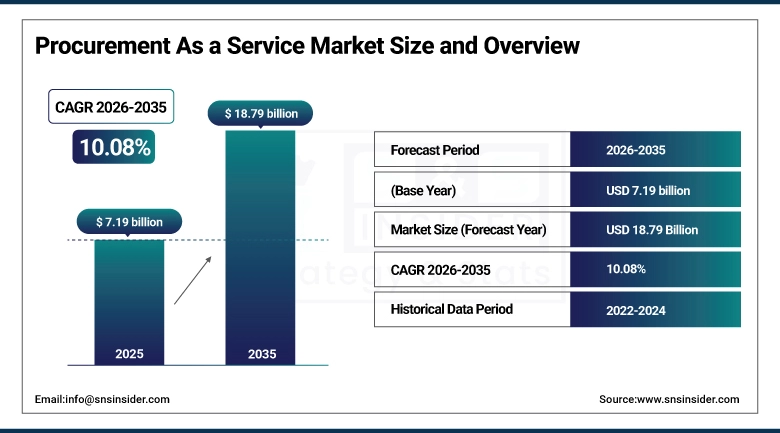

The Procurement As a Service Market Size was valued at USD 7.19 Billion in 2025 and is expected to reach USD 18.79 Billion by 2035 and grow at a CAGR of 10.08% over the forecast period 2026-2035.

The Procurement as a Service Market growth is primarily fueled by the increasing adoption of digital procurement platforms, automation and advanced analytics in businesses, which is a key driver for the growth of Procurement as a Service Market. In order to improve all round procurement performance, organizations are focusing on strategic sourcing, supplier risk management and contract optimization. In addition to this move from on-premise procurement solutions to cloud-based solutions that provide scalability and flexibility; there is further acceleration of market trends. With the growing focus on sustainability and ESG compliance, there too is an upcoming driver of the trend, PaaS models help organizations embed green procurement and ethical supplier management practices at the core of operations. According to study, over 65% of enterprises adopting Procurement as a Service (PaaS) cite automation and analytics as the primary drivers of cost reduction and efficiency gains.

Market Size and Forecast:

-

Market Size in 2025: USD 7.19 Billion

-

Market Size by 2033: USD 18.79 Billion

-

CAGR: 10.08% from 2026 to 2033

-

Base Year: 2025

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Procurement As a Service Market - Request Free Sample Report

Procurement As a Service Market Trends

-

Rising adoption of cloud-based PaaS platforms for real-time spend visibility globally.

-

Increased use of automation and AI to optimize procurement cycles efficiently.

-

Integration of procurement platforms with ERP, supplier, and contract management systems.

-

Growing focus on ESG compliance and sustainable sourcing in procurement decisions.

-

Ethical supplier evaluation and green procurement tracking becoming standard enterprise practices.

-

Regulatory pressure and digital transformation driving adoption of advanced procurement solutions.

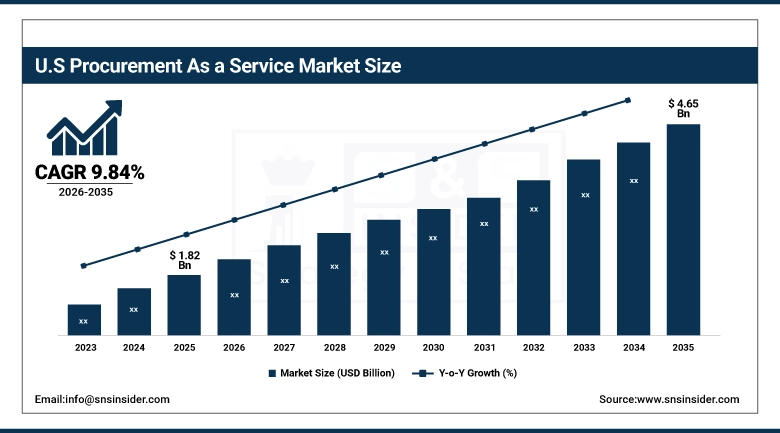

The U.S. Procurement As a Service Market size was USD 1.82 Billion in 2025E and is expected to reach USD 4.65 Billion by 2033, growing at a CAGR of 9.84% over the forecast period of 2026-2033, due to widespread cloud adoption, advanced digital infrastructure, and strong enterprise demand for automated, AI-driven procurement solutions, enhancing strategic sourcing, spend visibility, supplier management, and operational efficiency across industries.

Procurement As a Service Market Growth Drivers:

-

Cloud-Based Procurement Platforms Driving Efficiency and Real-Time Business Insights Globally

The primary driver fueling the Procurement as a Service Market growth is the increasing adoption of cloud-based procurement solutions. Enterprises have transitioned away from traditional on-premises traditional procurement systems to cloud platforms that offer greater scalability and flexibility that provide real-time access to procurement data. PaaS platforms leveraging cloud infrastructure facilitate companies to make supplier management easier with automated procurement workflows and embedded analytics for spend transparency. It enables organizations to speed up the procurement cycle, aggregate the most favorable sourcing decisions and streamline operational effectiveness, which is even more important for large enterprises with complex supply chains. Similarly, the cloud model also enables integrated connection with ERP, finance and supplier management systems, which leads to seamless connectivity and thus easing the pathway for organizations to realize end-to-end procurement optimization.

PaaS users achieve 20–30% improvement in supplier onboarding and contract compliance.

Procurement As a Service Market Restraints:

-

High Deployment And Maintenance Costs Challenge Widespread Procurement As A Service

The high costs associated with deployment and maintenance is one of the major factors hindering the growth of the PaaS market. Integrating a fully-fledged procurement service platform incurs very large subscription fees, onboarding expenses and IT integration costs while cloud-based ones lower some bare infrastructure overheads. Moreover, it’s the total ownership cost, because ongoing updates, cyber security, and the training the staff needs to undergo to handle such a system can also add to the total cost of ownership. These financial roadblocks, whilst the long-term ROI is a positive, can slow down adoption for firms and organisations based in regions particularly sensitive to cost. A barrier to wider market penetration is the high up front and operational costs.

Procurement As a Service Market Opportunities:

-

Sustainable And ESG-Focused Procurement Creating New Growth Opportunities Worldwide

A major opportunity in the PaaS market lies in sustainability and ESG-driven procurement. With companies increasingly working towards ethical sourcing, reducing carbon footprint, and green supply chain management, PaaS platforms provide the ability to monitor and manage these processes. With ESG compliance tracking, enterprises can evaluate sustainability KPIs for their suppliers and help ensure regulatory compliance along with other procurement decisions that adhere to environmental best practices. This will enable companies to meet corporate sustainability objectives and build shareholder and customer trust. With increasing regulatory pressure and consumer pressure for sustainable practices, PaaS providers have a golden opportunity to provide ESG (Environmental, Social and Governance) focused modules that facilitate adoption and differentiation in the market.

ESG-enabled PaaS platforms help enterprises achieve an average 15% reduction in supply chain carbon emissions.

Procurement As a Service Market Segment Highlight:

-

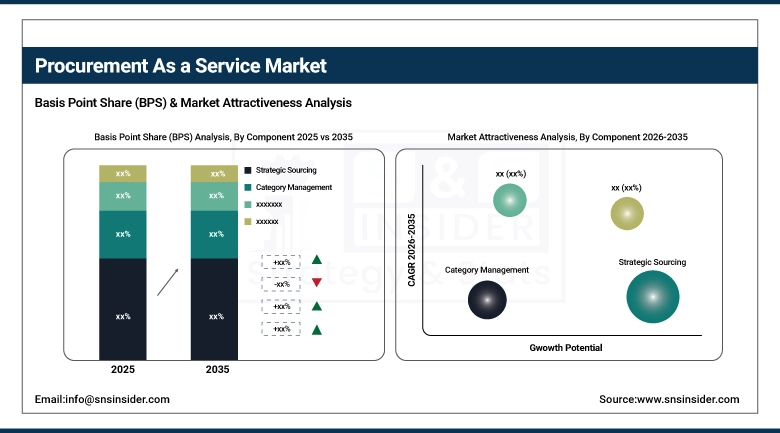

By Component: In 2025, Strategic Sourcing led the market with share 31.09%, while Transactions Management are the fastest-growing segment with a CAGR 10.54%.

-

By Deployment Mode: In 2025, Cloud-Based led the market with share 73.40%, with is the fastest-growing segment with a CAGR 12.50%.

-

By Organization size: In 2025 Large enterprise led the market with share 60.40%, while SME the fastest-growing segment with a CAGR 10.04%.

-

By End Use: In 2025, Manufacturing led the market with share 24.30%, while Healthcare is the fastest-growing segment with a CAGR 11.80%.

Procurement As a Service Market Segmentation Analysis:

By Component, Strategic Sourcing Leads Market and Transactions Management Fastest Growth

In the Procurement as a Service Market, the Strategic Sourcing segment leads the market due to its plays an important part in managing supplier selection, cost management, and overall procurement efficiency. More and more enterprises are using PaaS platforms to enhance their strategic sourcing capabilities by providing advanced analytics, supplier collaboration, and risk mitigation tools that enable better decision-making and operational performance.

Transactions Management segment is expected to grow at fastest CAGR, with increased adoption as organizations focus on automating their procure-to-pay processes, including invoice processing and purchase order management, to lower cycle times and eliminate errors. This growth is being driven by the accelerating uptake of digital and cloud-based procurement solutions that enable enterprises to simplify transactional processes with transparency and visibility throughout the supply chain.

By Deployment Mode, Cloud-Based Lead Market with Fastest Growth

Cloud-Based segment dominated the Procurement as a Service Market as it provides for scalability, flexibility, and access to procurement data in real-time. Additionally, enterprises are opting for a distinct set of solutions to replace the on-premises supplier management and procure-to-pay platforms with a cloud-based PaaS platform to optimize supplier management, automate workflows, and operate analytics capabilities for spending visibility.

cloud deployment is witnessing the fastest growth as enterprises of all sizes embrace digital procurement solutions to improve efficiency, contain operational costs, and leverage integration with ERP and finance systems. The increasing propensity towards subscription-based models and the relatively less upfront capital required for infrastructure deepens the cloud adoption and makes it the fastest expanding and most sought item in the industry.

By Organization size, Large Enterprise Leads Market and SME Fastest Growth

In the Procurement as a Service Market, Large Enterprises lead the market owing to their need for intricate procurement functionalities, large supplier networks, and high adoption for advanced digital procurement solutions. PaaS solutions help large enterprises to maximize their sourcing trajectory, effectively manage contracts along their procurement cycle, and end to end visibility of their procurement operations that help increase efficiency and gain cost optimum levels.

The fastest growing segment is SMEs where these companies are progressively deploying PaaS solutions for cost pressure relief, process automation, and on-demand, scalable, cloud-based procurement functionalities. Encouragingly, increasing awareness of digital procurement benefits, along with comparatively lower costs of deployment and seamless integration with existing systems, is pushing SMEs towards the rapid adoption of PaaS.

By End Use, Manufacturing Lead Market and Healthcare Fastest Growth

Manufacturing segment leads the market owing to complexities in supply chains, large volume of products to procure or services to outsource, as well as need for stratgic sourcing, spend management, and supplier risk mitigation activities. Furthermore, manufacturers are leveraging PaaS platforms to drive operational efficiencies, automate procurement workflows, and gain visibility into supplier performance and spend analytics in real-time.

Procurement As a Service Market Regional Analysis:

North America Procurement As a Service Market Insights:

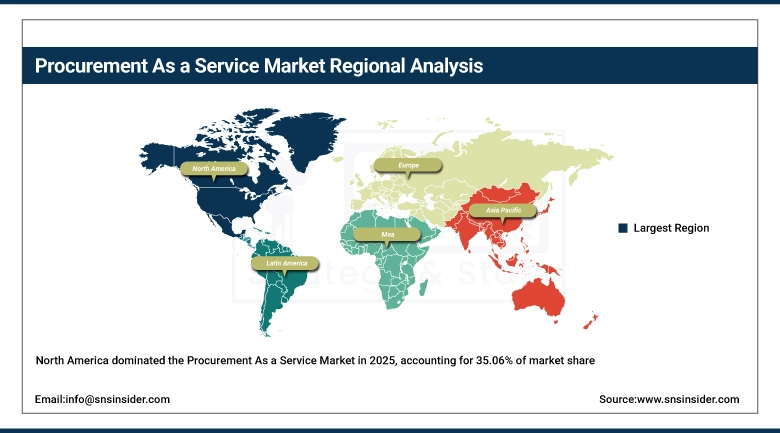

The Procurement As a Service Market in North America held the largest share 35.06% in 2025, North America dominates the Procurement as a Service Market, accounting for the largest market share due of the presence of advanced digital infrastructure, higher adoption of cloud-based procurement solutions in North America region and due to presence of key PaaS providers such as Accenture, IBM and Infosys and many other leading players. PaaS is gaining traction among organizations in the region, which are seeking to improve operational efficiencies by using PaaS platforms to facilitate strategic sourcing, contract management and spend optimization.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Procurement As a Service Market Insights

In 2025, Asia-Pacific is the fastest-growing region in the Procurement As a Service Market, projected to expand at a CAGR of 11.50%, wing to high digital transformation, high cloud adoption, and increasingly large SME and enterprise ecosystems. Strong digital procurement investments will support strategic sourcing, automate transactions and improve supplier management in countries such as China, India, Japan and Australia. The increasing emphasis on operational efficiency, cost-efficiency, and ESG-compliant procurement is driving adoption across manufacturing, healthcare and BFSI sectors.

Europe Procurement As a Service Market Insights

Europe holds a significant position in the Procurement As a Service Market, driven by presence of strong digital infrastructure, regulatory compliance and increase in the adoption of cloud-based procurement solutions. Companies in the region are using the PaaS platforms for improved strategic sourcing, automation of procurement lifecycle processes, and spend visibility control. Sustainable & ESG-compliant procurement remain in the limelight, driving adoption of tools for ethical sourcing & supplier assessment.

Latin America (LATAM) and Middle East & Africa (MEA) Procurement As a Service Market Insights

The Procurement As a Service Market in Latin America (LATAM) and Middle East & Africa (MEA) is witnessing steady growth, driven by increasing digital transformation initiatives and rising adoption of cloud-based procurement solutions. Enterprises across both regions are focusing on strategic sourcing, spend management, and supplier risk mitigation to enhance operational efficiency and reduce costs. Growing awareness of ESG-compliant and sustainable procurement practices is further accelerating market adoption. Additionally, the need for automation, advanced analytics, and end-to-end visibility is encouraging organizations to deploy PaaS platforms, positioning LATAM and MEA as emerging regions with significant potential for Procurement as a Service providers.

Procurement As a Service Market Competitive Landscape

Accenture is one of the key players in the market and offers end-to-end procurement service solutions based on cloud that leverages automation & analytical capabilities. It is a strategic sourcing, supplier management, and contact optimization company that helps enterprises achieve cost savings, better operational efficiencies, and ESG-compliant procurement practices on a global basis.

-

In February 2024, Accenture acquired Insight Sourcing to strengthen strategic sourcing and procurement services across private equity and consumer goods sectors.

GEP is a prominent player in the Procurement As a Service Market, providing cloud-based procurement platforms and strategic sourcing solutions. The company focuses on automating procurement processes, enhancing supplier performance, and enabling spend visibility. GEP helps organizations achieve operational efficiency, cost savings, and sustainable procurement practices through innovative digital tools.

-

In April 2024, GEP released its Procurement & Supply Chain Tech Trends Report, highlighting generative AI and technology innovations enhancing procurement agility.

Procurement As a Service Market Key Players:

Some of the Procurement As a Service Market Companies are:

-

Accenture

-

Infosys Limited

-

Genpact

-

GEP

-

IBM Corporation

-

WNS (Holdings) Ltd

-

Capgemini

-

Wipro Limited

-

HCL Technologies Limited

-

Tata Consultancy Services (TCS)

-

Xchanging (DXC Technology)

-

Aegis Limited

-

Corbus LLC

-

Proxima Group

-

SAP SE

-

Oracle Corporation

-

Zycus Inc

-

Jaggaer

-

Simfoni Limited

-

Kissflow Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.19 Billion |

| Market Size by 2035 | USD 15.49 Billion |

| CAGR | CAGR of 18.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Strategic Sourcing, Category Management, Transactions Management, Process Management, Spend Management, Contract Management) •By Deployment Mode (On-Premises, Cloud-Based) •By Organization Size (Large Enterprise, SME) •By End-use (BFSI, IT & Telecom, Healthcare, Retail, Manufacturing, Energy & Utilities, Travel & Hospitality, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Accenture, Infosys Limited, Genpact, GEP, IBM Corporation, WNS (Holdings) Ltd, Capgemini, Wipro Limited, HCL Technologies Limited, Tata Consultancy Services (TCS), Xchanging (DXC Technology), Aegis Limited, Corbus LLC, Proxima Group, SAP SE, Oracle Corporation, Zycus Inc, Jaggaer, Simfoni Limited, Kissflow Inc., and Others. |

Frequently Asked Questions

North America dominated the Procurement As a Service Market in 2025.

The Strategic Sourcing segment dominated the Procurement As a Service Market.

The major growth factor of the Procurement As a Service (PaaS) Market is the increasing adoption of digital and cloud-based procurement solutions by enterprises.

The Procurement As a Service Market size was USD 7.19 billion in 2025 and is expected to reach USD 18.79 billion by 2035.

The Procurement As a Service Market is expected to grow at a CAGR of 10.08% during 2026-2035.

Get in Touch