Urinary Drainage Bags Market Size & Trends:

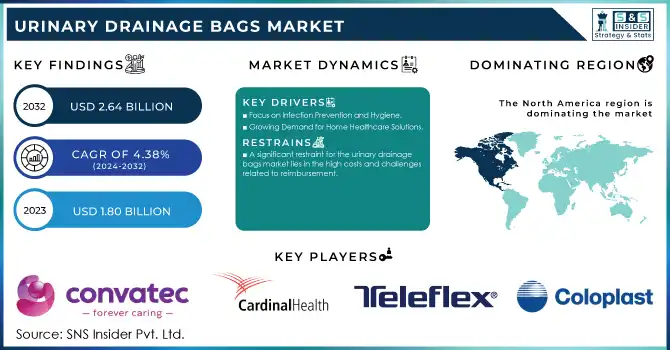

The Urinary Drainage Bags Market size was valued at USD 1.80 Billion in 2023 and is expected to reach USD 2.64 Billion by 2032 with a growing CAGR of 4.38% over the forecast period of 2024-2032.

To Get More Information on Urinary Drainage Bags Market - Request Sample Report

The Urinary Drainage Bags Market is experiencing steady growth, driven by various factors including the increasing prevalence of urological conditions, advancements in healthcare, and growing demand for home healthcare solutions. In the U.S. alone, urinary incontinence affects approximately 25 million adults, with the incidence rising significantly among the aging population, where more than 50% of people over the age of 65 are affected by some form of urinary incontinence. This statistic highlights the growing need for reliable urinary drainage solutions to address this widespread condition.

Technological advancements in urinary drainage bags have enhanced patient comfort and reduced complications. For instance, infection-resistant materials and anti-reflux valves are now commonly integrated into these products. The CDC’s recommendations for preventing catheter-associated urinary tract infections (CAUTI) emphasize the importance of such innovations, as CAUTI is one of the most common healthcare-associated infections, accounting for approximately 32% of all hospital-acquired infections in the U.S. By using products with infection-prevention features, healthcare providers can help reduce the risk of these infections.

Hospitals and healthcare institutions are also adopting stricter guidelines to manage the use of urinary drainage bags. According to a study published in the American Journal of Infection Control (AJIC), hospitals implementing evidence-based strategies to manage indwelling catheters saw a 25% reduction in CAUTI rates. These results reflect the positive impact of well-managed urinary drainage systems in preventing infections and improving patient outcomes.

In addition to hospital settings, home healthcare is an emerging trend reshaping the market. A report by Home Care Pulse revealed that 65% of people prefer to receive care at home for conditions like urinary incontinence, prompting a rise in demand for portable and easy-to-use urinary drainage bags designed for home care. This shift is supported by the availability of insurance coverage, including Medicare, which reimburses patients for medically necessary urinary drainage devices, making them more accessible to a broader range of individuals.

Market Dynamics

Drivers

-

Focus on Infection Prevention and Hygiene

The increasing emphasis on infection prevention in healthcare settings is a key driver for the urinary drainage bags market. With urinary tract infections (UTIs) being one of the most common hospital-acquired infections, there has been a shift toward improving the safety and hygiene of urinary drainage systems. Innovations such as antimicrobial coatings, closed drainage systems, and advanced valve technologies are integral in reducing infection risks associated with indwelling catheters and urinary drainage bags. These advancements improve patient outcomes and ensure compliance with stringent infection control protocols in hospitals and long-term care facilities. The integration of infection-resistant materials into drainage bags helps reduce the likelihood of catheter-associated urinary tract infections (CAUTI), making these products crucial for hospitals striving to enhance patient safety and reduce healthcare costs associated with infections.

-

Growing Demand for Home Healthcare Solutions

The increasing preference for home healthcare is significantly driving the urinary drainage bags market. Many patients, especially the elderly or those with chronic conditions such as incontinence, are opting to manage their health at home rather than in a clinical setting. This shift is largely motivated by the convenience, comfort, and cost-effectiveness that home care provides. As a result, there is a rising demand for portable, discreet, and user-friendly urinary drainage bags. These bags are designed for at-home use, ensuring ease of management for patients and caregivers. The availability of insurance coverage, including reimbursement by Medicare for medically necessary products, has also made home care solutions more accessible, further boosting market growth. This trend reflects a broader healthcare shift towards personalized care and the increasing role of patient autonomy in healthcare management.

-

Rising Prevalence of Urological Disorders and Expanding Healthcare Infrastructure

The growing incidence of urological disorders, including bladder dysfunction, prostate conditions, and neurological disorders that affect bladder control, is significantly fueling the demand for urinary drainage bags. As the global population ages, these conditions are becoming more prevalent, particularly among individuals over the age of 65, leading to an increased need for products that help manage these health challenges. Additionally, the expansion of healthcare infrastructure, especially in emerging economies, has made these medical devices more accessible to a broader population. Hospitals, ambulatory care centers, and home healthcare providers are investing in advanced urinary drainage solutions to ensure better patient care and treatment outcomes. This increased healthcare access, coupled with the growing awareness of effective management of urological conditions, is contributing to the expansion of the urinary drainage bags market globally.

Restraints

-

A significant restraint for the urinary drainage bags market lies in the high costs and challenges related to reimbursement.

Although urinary drainage bags are crucial for patients with conditions such as incontinence or post-surgery recovery, they can be costly, particularly for long-term use in home care settings. In many areas, insurance coverage for these products is limited, and patients may face substantial out-of-pocket expenses. While Medicare and other health programs provide reimbursement for necessary urinary drainage devices, the process can be complex, and not all product types or advanced features may be covered. This financial burden is particularly challenging for low-income patients or those in countries with less comprehensive healthcare systems. Furthermore, healthcare facilities in emerging markets may have budget limitations, restricting their ability to invest in advanced drainage solutions or infection-resistant technologies, which can slow the market's expansion in these regions.

Urinary Drainage Bags Market Segmentation Analysis

By Product

In 2023, leg bags dominated the urinary drainage bags market, making up a significant portion of the market share. They accounted for 60% of the market due to their widespread use in clinical and home care environments. Leg bags are preferred for their portability, as they can be discreetly worn under clothing, allowing patients with mobility needs to go about their daily activities with ease. Their convenience and ability to support an active lifestyle have made them the product of choice, especially for individuals with indwelling catheters who need long-term urinary management. Their design ensures comfort and ease of use, leading to continued dominance in the market.

The large bags segment is anticipated to be the fastest growing over the forecast period, driven by their increased adoption in healthcare facilities. Large bags are commonly used for patients who require continuous drainage or have higher urinary output, such as those recovering from surgery or managing specific urological conditions. The demand for large bags is growing due to advancements in design and features like infection-resistant materials, making them an attractive option for hospital use. Their larger capacity makes them suitable for extended use, leading to their rising popularity in medical settings.

By Capacity Segment

The 500-1000 ml capacity segment was the dominant segment in 2023, accounting for approximately 45% of the market. This capacity range is ideal for a variety of patients who experience moderate urinary output, making it the most commonly used size in both hospital and home care environments. These bags provide a balance between portability and sufficient storage, offering comfort for ambulatory patients. Their versatility and ability to manage the needs of a broad range of patients contributed to their dominance in the market.

The 1000-2000 ml capacity segment is the fastest growing throughout the forecast period, mainly due to the increasing demand for larger bags in clinical settings. Larger bags are increasingly used for patients with high urinary output or those who need long-term management post-surgery. The shift toward more comprehensive care solutions, combined with innovations in bag design, has led to the expansion of this segment. These bags provide extended functionality, making them suitable for patients requiring continuous drainage, and their use is rising in both hospital and home care environments.

Regional Outlook

In 2023, North America dominated the urinary drainage bags market with a 40% share, driven by its advanced healthcare infrastructure, heightened awareness of urological conditions, and the growing prevalence of issues like incontinence, bladder dysfunction, and prostate disorders. The United States, in particular, played a significant role in this growth, showing strong demand for hospital-grade and home-care drainage solutions. The region’s adoption of cutting-edge healthcare technologies, with favorable reimbursement policies, continues to fuel market expansion.

Europe followed closely behind, supported by factors such as a rapidly aging population and increasing healthcare investments. Countries like Germany, the UK, and France are witnessing rising demand for urinary drainage bags due to an increase in chronic conditions and a growing emphasis on enhancing patient quality of life. Additionally, Europe’s emphasis on infection control and hygiene drives the adoption of advanced drainage systems, including antimicrobial and closed systems.

The Asia Pacific region is expected to experience the fastest growth, thanks to rapid advancements in healthcare infrastructure, particularly in nations like China and India. With greater access to healthcare and rising awareness, the demand for urinary drainage products is increasing. Furthermore, the aging population and the growing incidence of urological diseases are significantly contributing to the market expansion in this region.

Do You Need any Customization Research on Urinary Drainage Bags Market - Enquire Now

Key Players

-

-

Leg Bags

-

Large Bags

-

Overnight Drainage Bags

-

Urological Catheters

-

-

-

Urinary Drainage Bags (Leg Bags & Large Bags)

-

Closed System Drainage Bags

-

Foley Catheters

-

-

-

Urinary Drainage Bags (Standard & Leg Bags)

-

Catheters

-

Closed Systems for Infection Control

-

-

-

Leg Bags

-

Overnight Drainage Bags

-

Urinary Catheters and Accessories

-

-

BD (C. R. Bard, Inc.)

-

Urinary Drainage Bags

-

Foley Catheters

-

Leg Bags with Integrated Features

-

-

McKesson Medical Surgical, Inc.

-

Urinary Drainage Bags (Leg Bags & Large Bags)

-

Catheters and Other Urological Products

-

-

Amsino International, Inc.

-

Urinary Drainage Bags (Leg Bags, Night Bags)

-

Catheters

-

Infection Prevention Systems

-

-

Flexicare Medical Ltd.

-

Urinary Drainage Bags

-

Leg Bags

-

Closed Catheter Systems

-

-

Medline Industries, Inc.

-

Urinary Drainage Bags (Leg Bags & Overnight Bags)

-

Urological Catheters

-

Closed Drainage Systems

-

-

Manfred Sauer GmbH

-

Urinary Drainage Bags

-

Leg Bags

-

Indwelling Catheters

-

-

B.Braun Melsung AG

-

Urinary Drainage Bags (Leg & Large Bags)

-

Catheters

-

Closed System Drainage Solutions

-

-

Becton, Dickinson and Company

-

Urinary Drainage Bags

-

Urological Catheters

-

Infection Prevention Products

-

Recent Developments

In April 2024, Ingenion Medical Ltd. received the CE mark for its Cymactive 2.0R urinary catheter, designed to treat men with chronic, non-neurogenic urinary retention. This innovative technology aims to replicate natural urination, offering significant improvements for men currently using Foley-type catheters, as noted by CEO Edward Cappabianca.

In March 2024, Phyllis W. from Akron, OH, developed the Catheter Bag Hanger, a vertical support system to prevent urine and bodily fluid backup in catheter bags. The device features an L-shaped body that can be placed under a patient’s body on various surfaces, such as a hospital bed or stretcher, keeping the bag upright to avoid fluid backup.

| Report Attributes | Details |

| Market Size in 2023 | USD 1.80 Billion |

| Market Size by 2032 | USD 2.64 Billion |

| CAGR | CAGR of 4.38% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Large Bags, Leg Bags) • By Capacity (0-500 ml, 500-1000 ml, 1000-2000 ml) • By Usage (Reusable, Disposable) • By End-use (Hospitals, Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ConvaTec, Inc., Cardinal Health, Teleflex, Inc., Coloplast, BD (C. R. Bard, Inc.), McKesson Medical Surgical, Inc., Amsino International, Inc., Flexicare Medical Ltd., Medline Industries, Inc., Manfred Sauer GmbH, B.Braun Melsung AG, Becton, Dickinson and Company |

| Key Drivers | • Focus on Infection Prevention and Hygiene • Growing Demand for Home Healthcare Solutions • Rising Prevalence of Urological Disorders and Expanding Healthcare Infrastructure |

| Restraints | • A significant restraint for the urinary drainage bags market lies in the high costs and challenges related to reimbursement. |

Frequently Asked Questions

Ans: With a share of 40% in 2023, North America dominated the global market for urinary drainage bags. This can be attributed to the increasing prevalence of specific disorders such as bladder cancer, benign prostatic

Ans: The rising prevalence of urologic disorders such as bladder cancer and urine incontinence, as well as the rising need for home care services, are some of the main drivers propelling the expansion of the urinary drainage bag market.

Ans: The major Key Players are ConvaTec, Inc., Cardinal Health, Teleflex, Inc., Coloplast BD, McKesson Medical Surgical, Inc., Amsino International, Inc., Flexicare Medical Ltd., Medline Industries, Inc., Manfred Sauer GmbH and others.

Ans: The Urinary Drainage Bags Market is Supposed to Achieve USD 2.64 billion by 2032.

Ans: The CAGR Growth rate of Urinary Drainage Bags is approx. CAGR 4.38% for the forecast period of 2024-2032.

Get in Touch