Veterinary Diagnostics Market Report Scope & Overview:

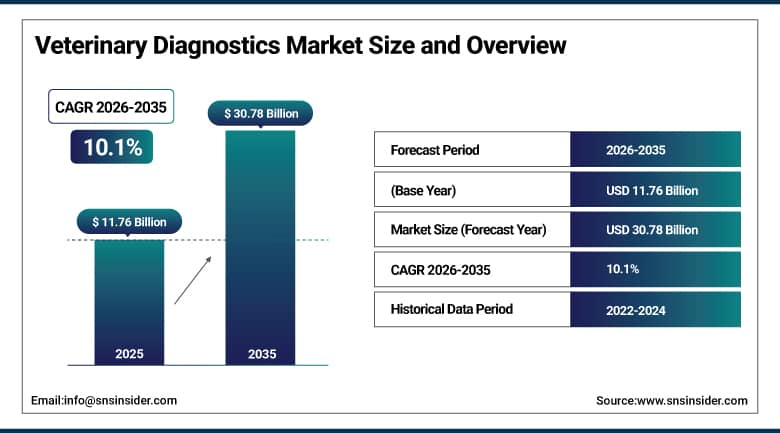

The Veterinary Diagnostics Market size was USD 11.76 Billion in 2025 and is expected to reach USD 30.78 Billion by 2035, growing at a CAGR of 10.1% from 2026–2035.

The Veterinary Diagnostics Market is growing due to the higher prevalence of diseases among animals, increased numbers of pets, and increased knowledge about preventive healthcare for animals. The rising spending on healthcare for companion animals, increased production of livestock, and the need for early diagnosis of diseases are some of the factors driving the market. Technology-driven advancements in molecular diagnostics, point-of-care diagnostics, and artificial intelligence-driven diagnostics are improving accuracy and efficiency of testing methods. Also, government programs for zoonosis surveillance, increasing visits to the veterinarian, and growing veterinary laboratories network is aiding market growth.

According to the World Organisation for Animal Health (WOAH), over 75% of emerging infectious diseases in humans originate from animals (zoonotic diseases), significantly increasing global investment in veterinary diagnostics and surveillance systems. Furthermore, the Food and Agriculture Organization (FAO) estimates that global livestock production includes more than 1.3 billion cattle, 1.2 billion sheep, and 1 billion pigs worldwide, creating substantial demand for routine disease monitoring and diagnostic services.

Veterinary Diagnostics Market Size and Forecast

-

Market Size in 2026E: USD 12.95 Billion

-

Market Size by 2035: USD 30.78 Billion

-

CAGR: 10.1% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Veterinary Diagnostics Market - Request Free Sample Report

Veterinary Diagnostics Market Trends

-

Point-of-care diagnostic platforms are expanding accessibility to advanced testing in veterinary clinic settings.

-

Molecular diagnostics including PCR and next-generation sequencing are gaining adoption for pathogen detection in livestock.

-

Wearable diagnostic sensors for companion animals are enabling continuous health monitoring and early disease detection.

-

Zoonotic disease surveillance keeps driving government investment in veterinary diagnostic infrastructure globally.

-

AI-powered diagnostic image analysis is improving accuracy in veterinary radiology and pathology workflows.

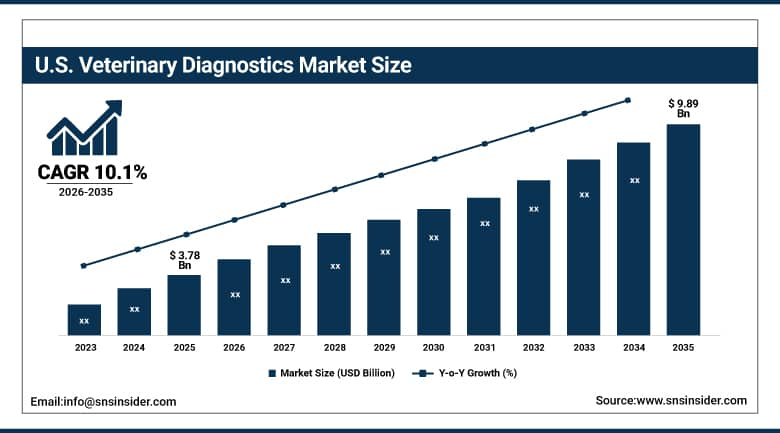

The U.S. Veterinary Diagnostics Market Outlook

The U.S. Veterinary Diagnostics Market is estimated at approximately USD 3.78 Billion in 2025, it is expected to reach approximately USD 9.89 Billion by 2035, applying the global CAGR of 10.1%.

Innovative diagnostic devices and increased utilization of point-of-care testing remain dominant trends in the U.S., contributing to efficiency in providing veterinary care services. As a result of the presence of an advanced system of veterinary care, along with a large number of pets kept in homes, the market share in the U.S. comprised a significant part of the global veterinary diagnostics market in 2023. The American Veterinary Medical Association reports that almost 70% of households in the country had pets in 2023. The USDA conducts studies aimed at increasing the accuracy of diagnostic tests for livestock diseases.

According to the American Pet Products Association (APPA), U.S. pet industry spending reached approximately USD 147 billion in 2023, reflecting strong companion animal healthcare expenditure, including veterinary diagnostics and preventive care services.

Veterinary Diagnostics Market Segment Analysis

-

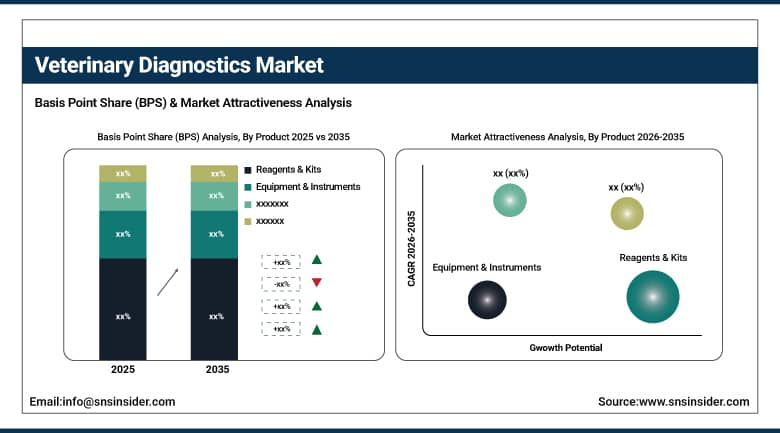

By Product, Reagents & Kits segment dominated the Veterinary Diagnostics Market in 2025 with 47% share; Equipment & Instruments segment is the fastest growing segment.

-

By Animal Type, Companion Animals segment dominated the market in 2025 with 61% share; Production Animals segment is the fastest growing segment.

-

By Testing Category, Immunology & Serology segment dominated the market in 2025 with 24% share; Molecular Diagnostics segment is the fastest growing segment.

-

By End-use, Reference Laboratories segment dominated the Veterinary Diagnostics Market in 2025 with 49% share; Veterinarians segment is the fastest growing segment.

By Product, Reagents & Kits segment dominates the Veterinary Diagnostics Market, Equipment & Instruments segment expected to grow fastest

The Reagents & Kits segment dominated the Veterinary Diagnostics Market because of the continuous need for the use of diagnostic kits to diagnose various diseases. Veterinary laboratories and veterinary clinics use these reagents and kits to conduct accurate and faster diagnoses of different animal diseases. The growing number of testings, the rising incidence of various infectious and chronic diseases among animals, along with innovations in products are contributing to increased demands. Moreover, their continuous need for replacement is helping in generating revenues and creating market dominance.

The Equipment & Instruments segment is the fastest growing owing to the rising adoption of advanced diagnostic machines in the field of veterinary healthcare. Veterinary hospitals and veterinary laboratories are using modern equipment in order to carry out accurate tests and make the process fast and efficient. The increasing demand for point-of-care diagnostics, the growing veterinary healthcare infrastructure, and technological innovations in medical equipment are driving their adoption.

By Animal Type, Companion Animals segment dominates the Veterinary Diagnostics Market, Production Animals segment expected to grow fastest

The Companion Animals segment dominated the Veterinary Diagnostics Market owing to the rise in pet ownership, expenditure on veterinary healthcare, and greater emphasis on preventive veterinary diagnostics. People owning pets are increasingly relying on health tests, early disease diagnosis, and advanced diagnostics. Increased use of pet insurance plans, increased visits to veterinarians, and strong emotional bonds between the pet owner and pets have resulted in a surge in diagnostics. This further cemented its leadership position in the global market.

The Production Animals segment is the fastest growing due to the increasing emphasis on livestock health and infection control to enhance productivity in commercial farms. Advanced diagnostic techniques are being used by farmers to detect infections earlier, prevent disease outbreaks, and manage herds better. The increasing global demand for meat products, milk, and poultry, along with strict regulatory norms related to food safety, has led to increased adoption of veterinary diagnostics.

By Testing Category, Immunology & Serology segment dominates the Veterinary Diagnostics Market, Molecular Diagnostics segment expected to grow fastest

The Immunology & Serology segment dominated the market owing to its extensive usage in detecting infectious diseases, tracking immune reactions, and performing routine health assessment of animals. The tests are quick, accurate, and cost-effective, and can thus be performed in veterinary clinics, hospitals, and reference labs. Rising incidence rates of zoonotic and infectious diseases, increased vaccinations, and high demand for disease detection are some of the factors that have helped maintain the dominance of the segment.

The Molecular Diagnostics segment is the fastest growing owing to its ability to detect infectious agents and genetic anomalies in animals very sensitively, specifically, and quickly. Adoption of PCR and other molecular techniques has made it possible to diagnose diseases in their early stages. Rising investments in advanced veterinary laboratories, increased demand for precise diagnosis, and continuous innovations in technology are some of the reasons behind the rising adoption rate.

By End-use, Reference Laboratories segment dominates the Veterinary Diagnostics Market, Veterinarians segment expected to grow fastest

The Reference Laboratories segment dominated the Veterinary Diagnostics Market because of their capability to conduct large scale and sophisticated testing using high-quality technology available at the lab. Reference labs help veterinary clinics and hospitals diagnose diseases, run confirmation tests, and do special analyses. Growing need for accurate diagnoses, development of laboratory network, and investment in better diagnostic testing capabilities have been boosting the segment's importance in helping them occupy the top spot in the veterinary diagnostics market.

The Veterinarians segment is the fastest growing because of increasing usage of diagnostic technologies that help veterinarians detect diseases quickly and decide on the type of treatment. Veterinarians have been buying diagnostic devices which will make their work more efficient. Growing number of pets, preventive care, and availability of portable diagnostic equipment have been making veterinarians opt for advanced diagnostic solutions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Veterinary Diagnostics Market Insights

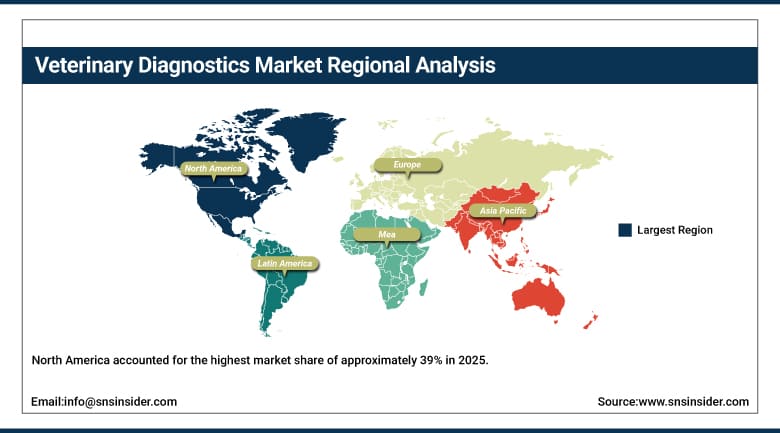

North America accounted for the highest market share of approximately 39% in 2025. This is due to the presence of an advanced veterinary system and high investment in pet healthcare in the region. The region benefits from good support by governmental agencies in animal health research, together with the advanced diagnostic techniques such as molecular diagnostics and imaging techniques. The USA has a well-established veterinary clinic, hospital, and reference laboratory network.

The USA is responsible for 82.5% of North American revenue. Growth in diagnostic tests as well as investments in healthcare expenditure makes it clear that the domestic market fundamentals in North America are good.

Furthermore, the U.S. Department of Agriculture (USDA) reports that the U.S. livestock sector includes approximately 87 million cattle and calves, 74 million swine, and 5.2 million sheep and lambs, all requiring continuous disease monitoring and veterinary testing to ensure animal health and food safety.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Veterinary Diagnostics Market Insights

The European region is an important market for veterinary diagnostic products, due to strict pharmaceutical regulations and good veterinary healthcare facilities. Germany dominates the market due to good manufacturing capabilities of pharmaceuticals and animal health products. France and the UK also represent substantial demand from their respective growing market of companion animals and agriculture veterinary segments.

Germany contributes to around 24.6% of European revenues. Food safety regulations and antibiotic resistance monitoring demands have been increasingly boosting the demand for veterinary diagnostic products.

The European Medicines Agency (EMA) supports veterinary pharmacovigilance and disease monitoring frameworks across the EU, strengthening diagnostic adoption for animal health safety and regulatory compliance.

In addition, Eurostat reports that the EU maintains a substantial livestock population, including approximately 142 million pigs, 76 million cattle, and 60 million sheep and goats combined, creating sustained demand for veterinary diagnostics to ensure disease prevention and food safety compliance.

Asia Pacific Veterinary Diagnostics Market Insights

The Asia Pacific Veterinary Diagnostics Market is seen as the fastest growing regional market due to the increasing rate of pet ownership, increased diseases among livestock, and increased veterinary infrastructure. The growing awareness of early detection of diseases and the need for preventive animal health care is making things better. The technological advances in imaging, molecular diagnostics, and test kits are improving the effectiveness of the process. Furthermore, there are government efforts and higher veterinary expenses supporting the growth of the market.

The Food and Agriculture Organization (FAO) notes that Asia accounts for the largest share of global livestock production, including more than 60% of the global swine population and rapidly expanding poultry production involving billions of birds annually. In addition, India’s Ministry of Fisheries, Animal Husbandry and Dairying reports that the country’s livestock population exceeds 537 million animals, highlighting its large-scale veterinary healthcare and diagnostic requirements.

China accounts for approximately 40.6% of Asia Pacific revenue. Growing pet ownership culture and rising food safety standards are simultaneously expanding both companion animal and production animal diagnostics demand. As regional disposable incomes and regulatory standards keep rising, this growth trajectory should continue strengthening.

Moreover, China operates one of the world’s largest animal production systems, with hundreds of millions of pigs and poultry, further driving demand for advanced disease surveillance and molecular diagnostic technologies.

MEA & Latin America Veterinary Diagnostics Market Insights

The UAE leads MEA revenue at approximately 22.8%. Growing companion animal ownership and expanding veterinary infrastructure both support regional demand. Saudi Arabia is also expanding its veterinary healthcare capacity.

Brazil leads Latin American revenue at approximately 43.8%. Large agricultural sector and growing companion animal care investment both drive regional veterinary diagnostics demand. Mexico and Argentina contribute secondary demand through their own expanding livestock and companion animal sectors.

Market Dynamics

Growth Drivers: Rising prevalence of zoonotic diseases necessitating advanced veterinary diagnostics

The rising occurrence of zoonotic diseases capable of being passed from animals to people is an increasingly pressing problem, which creates an immediate need for the implementation of advanced veterinary diagnostic systems. At present, zoonoses cause 60 percent of all human infectious diseases that are currently known. Emerging zoonoses comprise 75 percent of all new infectious diseases. Infections with tularemia have increased by 56 percent between 2011 and 2022 in the US. The H5N1 type of avian influenza virus is capable of causing infections in over 48 mammalian hosts.

Leptospirosis leads to almost one million severe cases of illness and almost 59,000 deaths annually. All of the statistics above stress the importance of having efficient veterinary diagnostic services that would allow detecting zoonotic diseases early on and dealing with them. Since the pressure of zoonotic diseases is continuously growing, the need for investing in veterinary diagnostic services remains relevant.

Restraints: High cost of advanced diagnostic technologies limiting accessibility

An increase in the number of zoonotic diseases that are transmissible from animals to humans is an issue that has become increasingly important, and it requires the application of modern systems of veterinary diagnostics to solve. Currently, zoonoses account for 60 percent of the total number of infectious human diseases that are known. Emerging zoonoses make up 75 percent of all emerging infectious diseases. There has been a 56 percent rise in the rate of infections with tularemia from 2011 to 2022 in the US. H5N1 type of avian influenza virus can infect more than 48 mammalian species.

Leptospirosis results in about a million cases of severe disease and 59 thousand deaths per year. All of the above numbers indicate the significance of having efficient veterinary diagnostics in order to be able to detect zoonotic diseases and address them. As the threat of zoonotic diseases continues to grow, the necessity to invest in veterinary diagnostics becomes increasingly significant.

Opportunities: Emerging markets in Asia Pacific presenting growth potential

The Asia Pacific region will see several lucrative growth opportunities owing to increasing investments in veterinary healthcare and increasing demand for animal products. The increasing middle-class population, increased disposable income, higher acceptability of pets, and strong demand for animal protein all contribute to such growth. Among these countries, India and China will show the highest CAGR during this period because of investments in veterinary healthcare and higher consumption of animal products.

The increasing global standards of food safety have led to investments in diagnostic capabilities for livestock in emerging markets. The government funding for One Health campaigns in several developing countries is contributing towards the growth of veterinary laboratory capabilities in such countries. With continued growth in pet ownership and awareness of food safety in emerging markets, the potential will continue to grow over the forecast period.

Recent Developments:

-

2023: IDEXX Laboratories launched the SNAP Leish 4Dx Test in November 2023, expanding its point-of-care rapid diagnostic portfolio for vector-borne disease detection in companion animals.

-

2023: Boule Diagnostics introduced H50V in June 2023, an affordable veterinary hematology solution with advanced features designed to make laboratory-quality diagnostics accessible to veterinary clinics.

-

2023: BioCheck unveiled VetAssure in April 2023, a biosecurity diagnostic tool leveraging bioluminescence technology for pigs and poultry, addressing growing biosecurity needs in commercial livestock operations.

Veterinary Diagnostics Market Key Players are:

-

IDEXX Laboratories, Inc.

-

Zoetis Inc.

-

Heska Corporation

-

Thermo Fisher Scientific Inc.

-

Virbac S.A.

-

Neogen Corporation

-

Bio-Rad Laboratories, Inc.

-

FUJIFILM Holdings Corporation

-

Randox Laboratories Ltd.

-

INDICAL BIOSCIENCE GmbH

-

bioMérieux SA

-

Agrolabo S.p.A.

-

QIAGEN N.V.

-

Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

-

Eurofins Scientific SE

-

MEGACOR Diagnostik GmbH

-

BioChek B.V.

-

Biogal Galed Laboratories

-

AniPOC Ltd.

-

Gold Standard Diagnostics Corp

Veterinary Diagnostics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.76 Billion |

| Market Size by 2035 | USD 30.78 Billion |

| CAGR | CAGR of 10.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Consumables, Reagents & Kits, Equipment & Instruments) • By Animal Type (Production Animals, Companion Animals) • By Testing Category (Clinical Chemistry, Microbiology, Parasitology, Histopathology, Cytopathology, Hematology, Immunology & Serology, Imaging, Molecular Diagnostics, Other Categories) • By End-use (Reference Laboratories, Veterinarians, Animal Owners/ Producers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IDEXX Laboratories, Inc., Zoetis Inc., Heska Corporation, Thermo Fisher Scientific Inc., Virbac S.A., Neogen Corporation, Bio-Rad Laboratories, Inc., FUJIFILM Holdings Corporation, Randox Laboratories Ltd., INDICAL BIOSCIENCE GmbH, bioMérieux SA, Agrolabo S.p.A., QIAGEN N.V., Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Eurofins Scientific SE, MEGACOR Diagnostik GmbH, BioChek B.V., Biogal Galed Laboratories, AniPOC Ltd., Gold Standard Diagnostics Corp. |

Frequently Asked Questions

The Veterinary Diagnostics Market is expected to grow at a CAGR of 10.1% from 2026 to 2035.

The Veterinary Diagnostics Market was valued at USD 11.76 Billion in 2025.

Rising prevalence of zoonotic diseases, growing pet ownership worldwide, and expanding livestock food safety requirements are the primary growth factors.

The Immunology & Serology segment dominated the Veterinary Diagnostics Market in 2025.

North America dominated the Veterinary Diagnostics Market with approximately 39% revenue share in 2025.

Get in Touch