Molecular Diagnostics Market Report Scope & Overview:

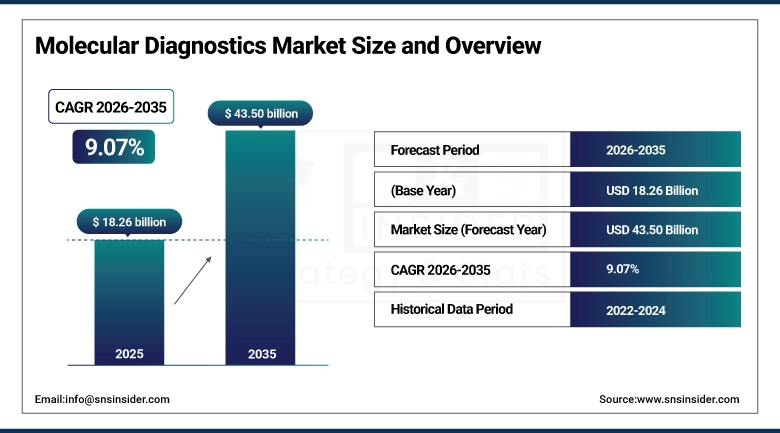

The Molecular Diagnostics Market size was valued at USD 18.26 Billion in 2025 and is projected to reach USD 43.50 Billion by 2035, growing at a CAGR of 9.07% during 2026–2035.

The Molecular Diagnostics Market is experiencing significant growth driven by increasing demand for accurate, rapid, and early disease detection. These diagnostics use advanced techniques to analyze genetic material, enabling precise identification of infectious diseases, cancer, and genetic disorders. Technological advancements such as PCR and next-generation sequencing have enhanced testing efficiency and reliability. The growing focus on personalized medicine, rising healthcare awareness, and the need for effective disease management are further accelerating market expansion, making molecular diagnostics an essential component of modern healthcare systems worldwide.

Molecular Diagnostics Market Size and Forecast:

-

Market Size in 2025: USD 18.26 Billion

-

Market Size by 2035: USD 43.50 Billion

-

CAGR: 9.07% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Molecular Diagnostics Market - Request Free Sample Report

Molecular Diagnostics Market Key Trends:

-

Rising adoption of Polymerase Chain Reaction and next-generation sequencing technologies enabling faster and more accurate disease detection.

-

Growing demand for point-of-care molecular testing solutions for rapid diagnostics in decentralized healthcare settings.

-

Increasing focus on personalized medicine and companion diagnostics driving the use of molecular testing in targeted therapies.

-

Expansion of applications in oncology, infectious diseases, and genetic disorder screening boosting overall market adoption.

-

Technological advancements in automation and integration of AI in molecular diagnostics improving efficiency and reducing turnaround time.

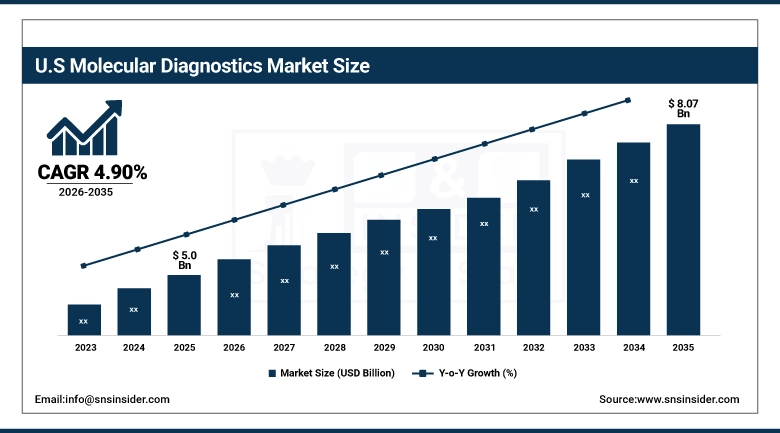

The U.S. Molecular Diagnostics Market size was valued at USD 5.0 Billion in 2025 and is projected to reach USD 8.07 Billion by 2035, growing at a CAGR of 4.90% during 2026–2035. Growth in the U.S. molecular diagnostics market is driven by rising chronic diseases, advanced healthcare infrastructure, increasing adoption of personalized medicine, strong R&D investments, and expanding use of rapid, accurate diagnostic technologies.

Molecular Diagnostics Market Drivers

-

Rising Demand for Early and Accurate Disease Diagnosis

The rise in the incidence of infectious diseases, cancer, and genetic disorders are one of the key trends fueling the molecular diagnostics market. Additionally, the increasing demand for point-of-care diagnostic technologies for timely diagnosis and treatment of diseases to improve patient outcome further supports the widespread adoption of advanced diagnostic technologies. Precision of PCR, Next Generation Sequencing and Real Time Testing Methods are being broadened by the increasing capacity of detection and the range of diagnostic diseases. Moreover, The increasing emphasis on personalized medicine and the development of targeted therapies is also propelling the demand.

Molecular Diagnostics Market Restraints:

-

High Costs and Technical Complexity Limiting Widespread Adoption

Bone muscle diseases like increasing infectious diseases, cancer, and genetic disorders which is major factor to drive the growth of molecular diagnostics market. The increasing demand for early and accurate diagnosis to enhance patient outcomes has highly stimulated the acceptance of innovative diagnostic technologies. PCR advancements, next generation sequencing along with real time testing methods are improving accuracy and speed. Moreover, the increasing emphasis on personalized medicine and targeted therapies is contributing to higher demand. Widespread adoption is also supported due to government initiatives, rising healthcare expenditure and increasing number of diagnostic laboratories, especially in developed and emerging markets.

Molecular Diagnostics Market Opportunities

-

Expansion of Point-of-Care Testing and Personalized Medicine

The molecular diagnostic market is expected to thrive due to the increasing need for rapid, decentralized diagnostic solutions. Point of care testing has the potential to help make decisions faster, with expedited patient management, as it can be conducted at remote and resource-poor settings. Portable and automated diagnostic devices are being developed to make testing faster, easier and more accessible. Additionally, growing awareness and implementation of personalized medicine and associated companion diagnostic techniques are creating newer opportunities for targeted therapies. The growth of the market in the years to come can be attributed to growing emerging markets, propelling investments on healthcare infrastructure as well constant technology developments.

Molecular Diagnostics Market Segment Analysis:

-

By Technology: In 2025, Polymerase Chain Reaction (PCR) dominated with 48% share; Next-Generation Sequencing (NGS) fastest growing segment during 2026–2035

-

By Product: In 2025, Reagents & Kits dominated with 52% share; Software & Services fastest growing segment during 2026–2035

-

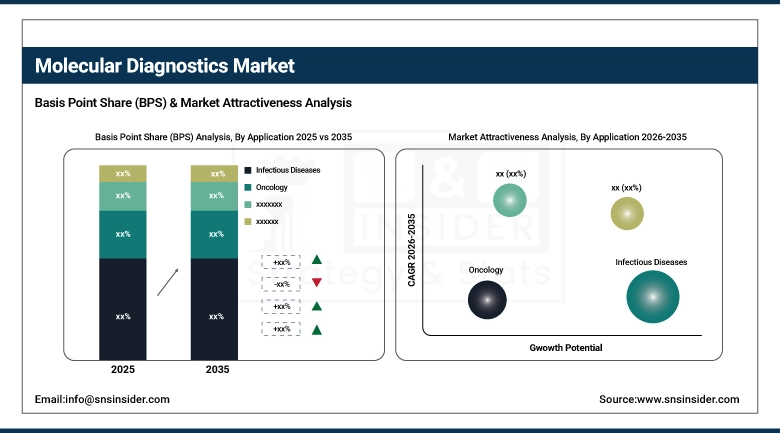

By Application: In 2025, Infectious Diseases dominated with 45% share; Oncology fastest growing segment during 2026–2035

-

By End User: In 2025, Diagnostic Laboratories dominated with 50% share; Hospitals & Clinics fastest growing segment during 2026–2035

By Application: Infectious Diseases Dominate, Oncology Fastest-Growing

Infectious Diseases hold the largest market share in the application segment, primarily due to the high global burden of infectious conditions such as COVID-19, HIV, tuberculosis, and influenza. Molecular diagnostics play a critical role in the rapid and accurate detection of pathogens, supporting timely treatment and disease control measures. The increased focus on pandemic preparedness has further strengthened this segment.

Oncology is the fastest-growing application segment, driven by the rising prevalence of cancer and the growing adoption of precision medicine. Molecular diagnostics enable early cancer detection, tumor profiling, and monitoring of treatment response, improving patient outcomes. Advancements in biomarker discovery and companion diagnostics are further fueling growth in oncology applications.

By Technology: PCR Dominates, NGS Fastest-Growing

Polymerase Chain Reaction (PCR) leads the technology segment in the market, owing to its high sensitivity, accuracy, and rapid turnaround time in detecting infectious diseases and genetic conditions. PCR-based tests have been widely adopted across clinical laboratories and hospitals, especially during the COVID-19 pandemic, which significantly boosted their demand globally. The reliability and cost-effectiveness of PCR technologies continue to support their dominant position in routine diagnostic applications.

Next-Generation Sequencing (NGS) is the fastest-growing segment, driven by increasing demand for advanced genomic analysis and precision medicine. NGS enables comprehensive genetic profiling, making it highly valuable in oncology, rare disease diagnosis, and personalized treatment planning. Continuous technological advancements and declining sequencing costs are further accelerating the adoption of NGS across developed and emerging healthcare markets.

By Product: Reagents & Kits Dominate, Software & Services Fastest-Growing

Reagents & Kits dominate the product segment, as they are essential consumables required for every molecular diagnostic test. The recurring need for reagents in routine testing, coupled with the growing volume of diagnostic procedures, has significantly contributed to their large market share. The expansion of testing for infectious diseases and genetic disorders further supports sustained demand for these products.

Software & Services represent the fastest-growing segment, supported by increasing integration of data analytics, bioinformatics, and automation in molecular diagnostics. Advanced software solutions are essential for managing large genomic datasets, particularly in NGS applications, enabling efficient interpretation and clinical decision-making. The shift toward digital healthcare and laboratory automation is further driving growth in this segment.

By End User: Diagnostic Laboratories Dominate, Hospitals & Clinics Fastest-Growing

Diagnostic Laboratories lead the end user segment with a market share, as they are the primary centers for conducting high-volume molecular testing. These laboratories are equipped with advanced diagnostic instruments and skilled professionals, enabling efficient and accurate testing services. The outsourcing of diagnostic services by hospitals and clinics further contributes to their dominance.

Hospitals & Clinics are the fastest-growing segment, driven by the increasing adoption of point-of-care molecular testing and the need for rapid, on-site diagnostics. The integration of molecular diagnostic platforms within hospital settings enhances patient management by enabling quicker clinical decisions. Growing healthcare infrastructure and investment in decentralized testing solutions are supporting this segment’s expansion.

Molecular Diagnostics Market Regional Analysis:

North America Molecular Diagnostics Market Insights:

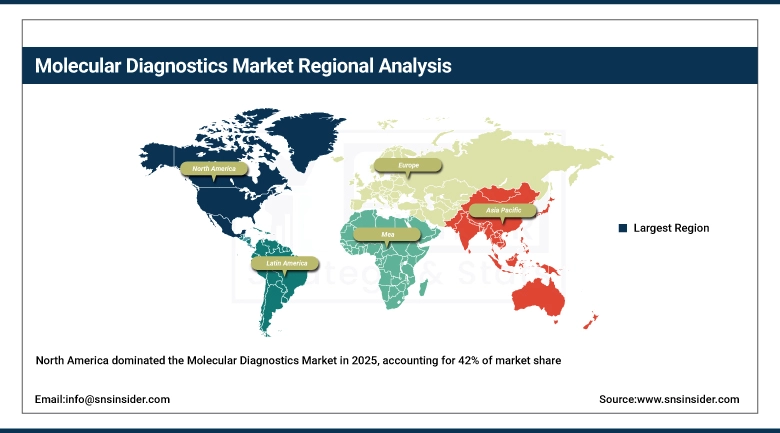

North America dominates the Molecular Diagnostics Market, accounting for approximately 42% of the global market share in 2025. This leadership is driven by advanced healthcare infrastructure, high adoption of cutting-edge diagnostic technologies, and strong presence of key market players. Significant investments in research and development, along with increasing demand for early and accurate disease detection, further support market growth. Additionally, favorable reimbursement policies and widespread use of molecular testing in clinical practices contribute to the region’s continued dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Molecular Diagnostics Market Insights:

Asia-Pacific is the fastest-growing region in the Molecular Diagnostics Market, driven by expanding healthcare infrastructure, rising population, and increasing prevalence of infectious and chronic diseases. Growing awareness about early disease detection and rapid adoption of advanced diagnostic technologies are accelerating market growth. Government initiatives to improve healthcare access and investments in biotechnology and diagnostics sectors further support expansion. Additionally, increasing demand for affordable and accurate testing solutions is contributing to the strong growth trajectory of the market in the region.

Europe Molecular Diagnostics Market Insights:

Europe holds a significant position in the Molecular Diagnostics Market, supported by well-established healthcare systems and strong emphasis on early disease detection and prevention. The region benefits from advanced laboratory infrastructure and increasing adoption of innovative diagnostic technologies. Growing prevalence of chronic and infectious diseases, along with rising demand for personalized medicine, is driving market growth. Additionally, supportive regulatory frameworks and continuous investments in research and development contribute to the steady expansion of the molecular diagnostics market across Europe.

Latin America Molecular Diagnostics Market Insights:

Latin America is an emerging market in the Molecular Diagnostics sector, driven by improving healthcare infrastructure and increasing awareness of early disease detection. Rising prevalence of infectious diseases and growing demand for accurate diagnostic solutions are supporting market growth. Government initiatives to expand access to healthcare services and diagnostic testing are further contributing to development. Additionally, increasing investments in healthcare facilities and gradual adoption of advanced molecular technologies are expected to boost market expansion in the region.

Middle East & Africa (MEA) Molecular Diagnostics Market Insights:

The Middle East & Africa (MEA) Molecular Diagnostics Market is witnessing steady growth, supported by improving healthcare infrastructure and rising demand for advanced diagnostic solutions. Increasing prevalence of infectious diseases and growing focus on early disease detection are key factors driving adoption. Government initiatives to strengthen healthcare systems and expand diagnostic capabilities are further contributing to market development. Additionally, rising investments in healthcare and gradual adoption of molecular diagnostic technologies are expected to support continued growth in the region.

Molecular Diagnostics Market Competitive Landscape:

Roche Diagnostics is a division of F. Hoffmann-La Roche Ltd., a global healthcare company founded in 1896 and headquartered in Switzerland. Roche Diagnostics specializes in innovative diagnostic solutions, offering a wide range of products including molecular diagnostics, clinical chemistry, immunoassays, and tissue diagnostics used in laboratories, hospitals, and research institutions worldwide. The company is a leader in molecular testing technologies, particularly in PCR and sequencing-based diagnostics, enabling early and accurate disease detection across oncology, infectious diseases, and genetic disorders. Roche operates in over 100 countries and employs more than 100,000 people globally.

-

In March 2024, Roche Diagnostics expanded its molecular diagnostics portfolio by launching advanced PCR-based assays designed to improve rapid detection of infectious diseases and support decentralized testing in clinical settings.

Thermo Fisher Scientific Inc. was founded in 2006 and is a global leader in scientific services and products, headquartered in the United States. The company provides a broad range of solutions including analytical instruments, reagents, consumables, software, and molecular diagnostic tools for healthcare, research, and industrial applications. Thermo Fisher plays a significant role in molecular diagnostics through its advanced PCR systems, next-generation sequencing platforms, and applied biosystems technologies, supporting disease detection, genetic analysis, and precision medicine initiatives worldwide. The company operates in over 50 countries and has more than 130,000 employees globally.

-

In February 2024, Thermo Fisher Scientific introduced new next-generation sequencing (NGS) solutions aimed at enhancing clinical diagnostics and enabling faster, more accurate genomic analysis for personalized medicine applications.

Molecular Diagnostics Market Key Players:

-

Roche Diagnostics

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

Qiagen N.V.

-

Danaher Corporation (Cepheid)

-

bioMérieux SA

-

Siemens Healthineers AG

-

Hologic Inc.

-

Becton, Dickinson and Company (BD)

-

Agilent Technologies Inc.

-

Illumina, Inc.

-

PerkinElmer, Inc.

-

Bio-Rad Laboratories, Inc.

-

Sysmex Corporation

-

Grifols, S.A.

-

Myriad Genetics, Inc.

-

Exact Sciences Corporation

-

Hoffmann-La Roche Ltd.

-

GenMark Diagnostics (Roche)

-

Tecan Group Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.26 Billion |

| Market Size by 2035 | USD 43.50 Billion |

| CAGR | CAGR of 9.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology: (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Microarrays, In Situ Hybridization (ISH), Others) • By Product: (Reagents & Kits, Instruments, Software & Services) • By Application: (Infectious Diseases, Oncology, Genetic Testing, Blood Screening, Others) • By End User: (Hospitals & Clinics, Diagnostic Laboratories, Research & Academic Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Roche Diagnostics, Thermo Fisher Scientific Inc., Abbott Laboratories, Qiagen N.V., Danaher Corporation (Cepheid), bioMérieux SA, Siemens Healthineers AG, Hologic Inc., Becton, Dickinson and Company (BD), Agilent Technologies Inc., Illumina, Inc., PerkinElmer, Inc., Bio-Rad Laboratories, Inc., Sysmex Corporation, Grifols, S.A., Myriad Genetics, Inc., Exact Sciences Corporation, F. Hoffmann-La Roche Ltd., GenMark Diagnostics (Roche), Tecan Group Ltd. |

Frequently Asked Questions

Ans: The Molecular Diagnostics Market is expected to grow at a CAGR of 9.07% during 2026–2035.

Ans: The market was valued at USD 18.26 Billion in 2025 and is projected to reach USD 43.50 Billion by 2035.

Ans: The key drivers of the Molecular Diagnostics Market include rising infectious diseases, increasing cancer prevalence, demand for early diagnosis, technological advancements, personalized medicine adoption, and growing healthcare infrastructure globally.

Ans: The Polymerase Chain Reaction (PCR) segment dominated during the projected period.

Ans: North America dominated the Molecular Diagnostics Market in 2025.

Get in Touch