Companion Animal Health Market Report Scope & Overview:

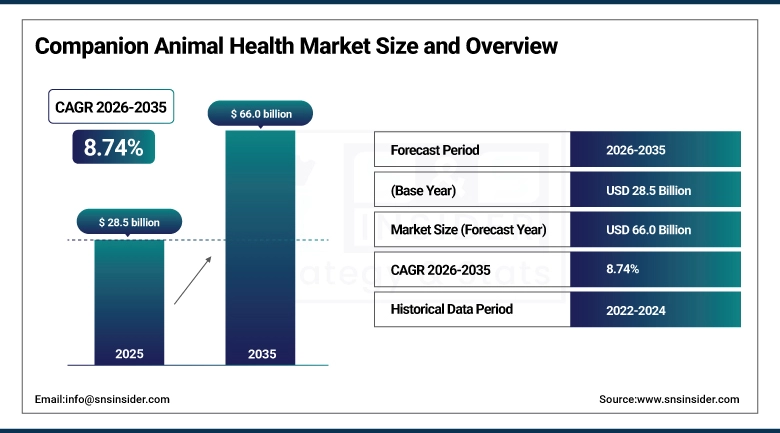

The Companion Animal Health Market was valued at USD 28.5 billion in 2025 and is expected to reach USD 66.0 billion by 2035, growing at a CAGR of 8.74% from 2026–2035.

The market of Companion Animal Health is enjoying a period of healthy growth and development, attributed to the worldwide phenomenon of pet humanization, increased uptake of pets in developing and developed countries alike, and the incorporation of sophisticated veterinary diagnostic technologies, medication, and preventive measures. Pet owners are spending more and more of their budget on animal health care, looking for high-quality treatment, diagnostics, and nutrition that match the standards applied in human medicine. The growing adoption of pet insurance, telemedicine for veterinarians, and artificial intelligence in diagnostics is also opening up more opportunities for revenue generation in the field of companion animal health care.

Industry reports have always proven that humanizing pets is the sole strongest structural driver of demand within the market for companion animal health, averaging more than USD 2,085 annually per pet on healthcare costs in 2024. This figure includes veterinary care, pharmaceuticals, preventative treatment, and high-end nutrition as pet owners strive to prolong the lives of their companion animals.

Companion Animal Health Market Size and Forecast

-

Market Size in 2025: USD 28.5 Billion

-

Market Size by 2035: USD 66.0 Billion

-

CAGR: 8.74% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Companion Animal Health Market - Request Free Sample Report

Companion Animal Health Market Trends

-

Emerging trends towards pet humanization leading to investments in high-end veterinary services, specialty therapies, preventive health strategies, and functional nutrition products.

-

Use of AI-based veterinary diagnostics tools helping in rapid identification of diseases and creation of personalized treatment plans.

-

Concentration on telehealth and telemedicine in veterinary industry facilitating access to veterinary consultations in remote geographical locations.

-

Increase in importance given to longevity of pets leading to development of ant-aging products, genetic testing products, and disease management services.

-

Pet insurance becoming common lowering the cost of veterinary services and encouraging consumption of high-end services.

-

Growth in biologics used by companion animals, which include use of monoclonal antibodies for pain relief and immunology.

-

Increased distribution of veterinary products through e-commerce channels making veterinary products easily available and competitively priced.

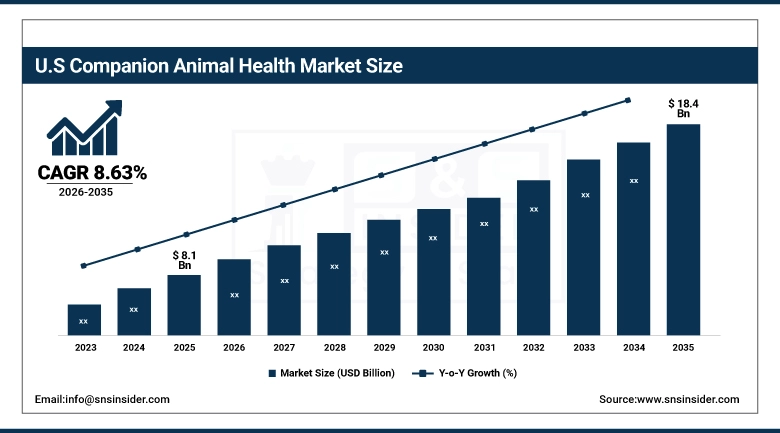

U.S. Companion Animal Health Market was valued at USD 8.1 billion in 2025 and is expected to reach USD 18.4 billion by 2035, registering a CAGR of 8.63% during 2026–2035.

The U.S. Companion Animal Health Market leads globally in terms of size due to 86.9 million pet-owning households, which account for around 66% of all U.S. households, an advanced veterinary system, and per capita expenditures on pet healthcare that rank highest in the world. The U.S. boasts cutting-edge pharmaceutical and biotechnology industries that help develop new treatment options in companion animal healthcare, from monoclonal antibodies to gene therapy and artificial intelligence-based diagnostics. Growth in pet insurance adoption is making premium costs less of a barrier.

The U.S. FDA's Accelerated Conditional Approval pathway for animal drugs, demonstrated through the regulatory process for longevity-focused companion animal therapeutics such as Loyal's LOY-001 for large dog breeds, signals an expanding frontier of biotech innovation in companion animal medicine that is expected to generate significant new revenue streams within the U.S. market through 2035.

Companion Animal Health Market Segment Insights

-

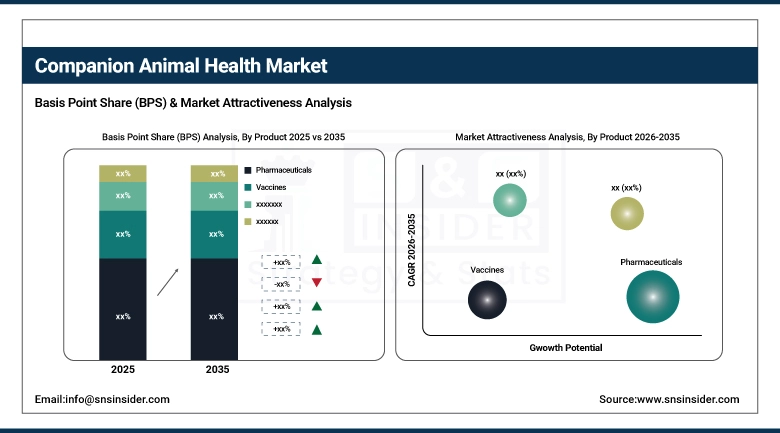

Based on Product, Pharmaceuticals accounted for the largest market share (~43%) in 2025; Diagnostics expected to be the fastest-growing segment (CAGR).

-

Based on Animal Type, Dogs accounted for the largest market share (~39%) in 2025; Cats expected to be the fastest-growing segment (CAGR).

-

Based on Distribution Channel, Veterinary Hospitals & Clinics accounted for the largest market share in 2025; E-Commerce expected to be the fastest-growing segment (CAGR).

-

Based on End-Use, Veterinary Hospitals & Clinics accounted for the largest market share in 2025; Home Care expected to be the fastest-growing segment (CAGR).

Companion Animal Health Market Segment Analysis

By Product, Pharmaceuticals dominate, Diagnostics expected to grow fastest

Pharmaceuticals emerged as the most dominant market segment, contributing a market share of about 43% in 2025 due to the consistent increase in the demand for antibiotics, antiparasiticide, anti-inflammatory drugs, and other innovative biologics such as monoclonal antibodies. The development of Librela by Zoetis for canine osteoarthritis and Cytopoint for treating atopic dermatitis in dogs can be considered breakthrough companion animal biologics that have gained blockbuster status, proving the immense market potential for innovative companion animal drug discovery. The research and development of companion animal pharmaceutical products are constantly increasing, with many more new molecular entities and biologics being discovered in the areas of oncology, cardiovascular diseases, and age-related disorders.

Diagnosics was expected to record the highest CAGR during the period of forecast from 2025 to 2035. Increasing demand for rapid, reliable point-of-care diagnostics tests, alongside the increased use of artificial intelligence-based diagnostic imaging systems and molecular diagnostic technologies, has resulted in the rapid growth of the market. IDEXX Laboratories has consistently pioneered in the development of in-clinic veterinary diagnostics and reference laboratories for companion animal testing, driving market growth.

By Animal Type, Dogs dominate, Cats expected to grow fastest

Dogs was the biggest segment holding about 39% market share in 2025 due to the fact that the world population of pets is mostly made up of dogs, which is why there has been a more significant investment in canine pharmaceutical drugs and vaccines than there had been for feline products. This segment is making more money than the others due to the fact that dogs are costing owners more each year in terms of veterinary fees.

Cats would be the fastest-growing segment with the highest CAGR from 2025-2035. Rising adoption rates of cats in particular around the world, especially among younger individuals and those living in cities in small apartments, coupled with increased development of cat-specific pharmaceuticals and increased attention to cat healthcare are driving this rapid market growth. In 2022, the FDA approved a feline monoclonal antibody therapy from Zoetis, marking a new era in the development of feline-targeted medicines.

By Distribution Channel, Veterinary Clinics dominate, E-Commerce expected to grow fastest

Hospital Pharmacies and Clinics accounted for the largest market distribution channel share in 2025. This was due to the medical necessity of prescribed products, vaccines, and diagnostics that required professional intervention by veterinarians. The hospital pharmacy model provided the assurance of product quality, proper medication counseling, and integration of the medication into the treatment plan, hence remaining the largest channel in terms of prescription pharmaceuticals and diagnostic products.

E-Commerce will account for the highest CAGR between 2026 and 2035. Pet pharmacy online platforms have been able to attract an increasing number of customers for OTC products such as flea and tick preventative products, dietary supplements, and nutritional products recommended by veterinarians. Increasing customer preferences towards online purchasing of veterinary products such as preventative products due to convenience and competitive pricing through online e-commerce sites is driving growth in this channel.

Companion Animal Health Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

United Kingdom |

30% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

52% |

North America Companion Animal Health Market Insights

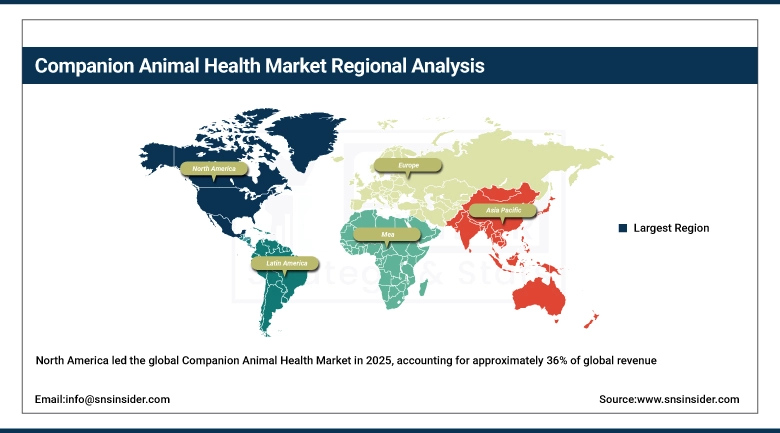

North America led the global Companion Animal Health Market in 2025, accounting for approximately 36% of global revenue. The United States represents the overwhelming majority of North American market revenue, supported by the world's highest absolute pet ownership numbers, the most advanced veterinary pharmaceutical R&D ecosystem, high pet insurance penetration, and the presence of leading global animal health companies including Zoetis, Merck Animal Health, and Elanco. Canada contributes meaningfully with 7.9 million pet dogs and 8.5 million cats and a well-developed veterinary services infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Companion Animal Health Market Insights

Asia Pacific is expected to register the fastest CAGR during the forecast period of 2026–2035. Rising disposable incomes, rapid urbanization, evolving cultural attitudes toward companion animals, and growing awareness of preventive pet healthcare are driving explosive companion animal market growth across China, India, Japan, South Korea, and Southeast Asia. China's rapidly expanding pet population, India's rising urban pet ownership, and Japan's premium pet care culture are key demand drivers. Regional government welfare campaigns and growing private veterinary clinic networks are improving animal healthcare access.

Europe Companion Animal Health Market Insights

Europe retained a substantial presence in the international Companion Animal Health Market in 2025, with the UK, Germany, France, and Italy being the key countries. European pet owners exhibit a high level of awareness regarding preventative animal care, making them willing to invest in good-quality tests and treatment options. The strict vet drug regulatory framework in the EU helps maintain high product quality standards while encouraging continuous development of pharmaceutical products. The increasing trend of pet insurance and preventative healthcare programs in Europe drives market growth.

Middle East & Africa and Latin America Companion Animal Health Market Insights

The Middle East and Africa and Latin America Companion Animal Health Markets constitute emerging markets, driven by increased pet ownership in urban centers, increased middle-income levels, and higher awareness regarding companion animal health. Brazil is the leading market in Latin America due to its large population of pets, efficient pharmaceutical sales networks, and robust demand for pet products. The GCC countries are experiencing increasing use of premium pet care, which has contributed to high demand for companion animal health products and services.

Companion Animal Health Market Growth Drivers:

-

Pet humanization and rising consumer willingness to invest in advanced companion animal healthcare

The primary growth driver for the Companion Animal Health Market is the deepening emotional bond between humans and companion animals globally, which is translating directly into increased healthcare investment. Pet owners are increasingly viewing their animals as family members deserving of medical care equivalent to that available for human family members, driving demand for premium diagnostics, specialized therapeutics, preventive vaccines, and functional nutrition products. This behavioral shift is structural and generationally reinforced, with millennials and Gen Z pet owners demonstrating particularly high pet healthcare spending relative to older demographics.

The growing convergence of human and veterinary medicine is creating a virtuous innovation cycle, where breakthroughs in human oncology, immunology, and genomics are being rapidly adapted for companion animal applications – including monoclonal antibody therapies, immunotherapy, and precision medicine diagnostics – that command premium pricing and generate substantial new revenue streams for animal health pharmaceutical companies and veterinary specialty practices.

Companion Animal Health Market Restraints

-

High cost of advanced veterinary treatments and limited insurance penetration constraining market access

One of the key barriers to the Companion Animal Health Market is the prohibitively high cost of sophisticated diagnostics, specialty drugs, and operations that are not accessible to many pet owners without insurance cover. Even though there is an increase in awareness regarding pet insurance, the rate of penetration is still relatively low in almost all countries except the UK and Sweden, with most expenses incurred being from personal payment. The state of economic conditions could lead to low levels of pet health expenses.

Companion Animal Health Market Opportunities

-

AI-driven veterinary diagnostics and companion animal longevity therapeutics

The integration of artificial intelligence into veterinary diagnostic imaging, point-of-care testing platforms, and clinical decision support systems represents a significant growth opportunity, enabling faster and more accurate disease detection while reducing the expertise burden on veterinary practitioners in underserved areas. Simultaneously, the emerging field of companion animal longevity medicine – targeting the biological mechanisms of aging in dogs and cats through novel therapeutics, genetic screening, and personalized wellness programs – is creating an entirely new premium market segment with strong consumer willingness to pay. Telehealth platforms connecting pet owners with veterinary specialists remotely are further expanding the addressable market by reducing geographic barriers to specialist consultation.

Recent Developments:

-

2026: Zoetis launched AI-powered precision medicine diagnostic tools enabling personalized companion animal treatment protocols based on genetic and biomarker profiles. Multiple companion animal longevity-focused biotech companies advanced clinical programs for age-extension therapeutics targeting large dog breeds, attracting substantial venture capital investment and regulatory engagement with the FDA's Accelerated Conditional Approval pathway.

-

2025 (March): Zoetis introduced AI-powered precision medicine diagnostics aimed at enhancing treatment efficacy and personalizing care for companion animals globally, marking a major milestone in the integration of artificial intelligence into veterinary clinical decision-making and individualized treatment planning.

-

2024 (November): Merck Animal Health launched BRAVECTO TriUNO, a novel combination parasiticide providing comprehensive protection against internal and external parasites for dogs, receiving European Commission regulatory approval. The product represents significant advancement in companion animal preventive care, offering simplified once-quarterly treatment regimens for parasite prevention.

Companion Animal Health Market Key Players

Some of the Companion Animal Health Market Companies are:

-

Zoetis Inc.

-

Merck Animal Health

-

Elanco Animal Health

-

Boehringer Ingelheim Animal Health

-

Virbac S.A.

-

Ceva Santé Animale

-

IDEXX Laboratories Inc.

-

Vetoquinol S.A.

-

Royal Canin (Mars Inc.)

-

Hill’s Pet Nutrition (Colgate-Palmolive)

-

Nestlé Purina PetCare

-

Mars Petcare

-

Nutreco N.V.

-

Neogen Corporation

-

Animalcare Group

Companion Animal Health Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.5 Billion |

| Market Size by 2035 | USD 66.0 Billion |

| CAGR | CAGR of 8.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Pharmaceuticals, Vaccines, Diagnostics, Nutrition, Others) • By Animal Type (Dogs, Cats, Others) • By Distribution Channel (Veterinary Hospitals & Clinics, Retail Pharmacies, E-Commerce, Others) • By End-Use (Veterinary Hospitals & Clinics, Home Care, Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Zoetis Inc, Merck Animal Health, Elanco Animal Health, Boehringer Ingelheim Animal Health, Virbac S.A., Ceva Santé Animale, IDEXX Laboratories Inc, Vetoquinol S.A., Royal Canin (Mars Inc.), Hill’s Pet Nutrition (Colgate-Palmolive), Nestlé Purina PetCare, Mars Petcare, Nutreco N.V., Neogen Corporation, Animalcare Group |

Frequently Asked Questions

North America dominated the Companion Animal Health Market in 2025, accounting for approximately 36% of global market revenue.

The Pharmaceuticals segment dominated the Companion Animal Health Market in 2025, accounting for approximately 43% of global product revenue.

Pet humanization and rising consumer willingness to invest in advanced companion animal healthcare, combined with continuous pharmaceutical and diagnostic innovation enabling higher-quality veterinary treatments.

The Companion Animal Health Market was valued at USD 28.5 billion in 2025.

The Companion Animal Health Market is expected to grow at a CAGR of 8.74% from 2026 to 2035.

Get in Touch