Water-based Resin Market Report Scope & Overview:

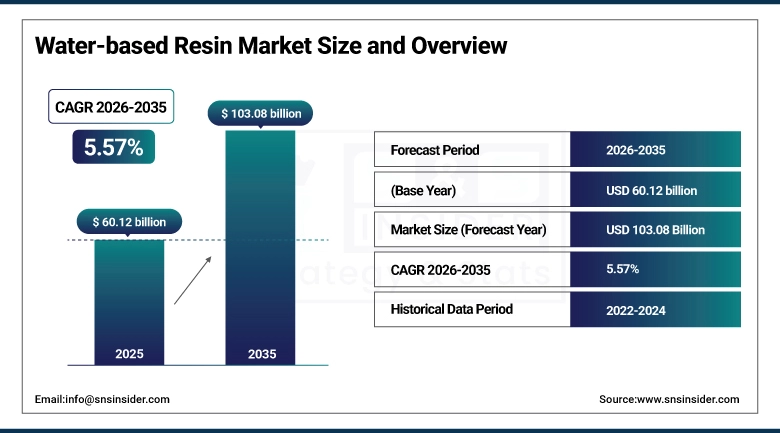

The Water-based Resin Market size was valued at USD 60.12 Billion in 2025 and is projected to reach USD 103.08 Billion by 2035, growing at a CAGR of 5.57% during 2026-2035. Factors such as increase in environmental stringent laws against VOC, growing demand for eco-friendly coatings, rapid growth of the construction and automotive from both region and sector, and the increasing preference of water-based products as sustainable, low toxicity and highly functional alternatives in various industrial and consumer applications across the globe have been observed as key drivers for this market.

Market Size and Forecast:

-

Market Size in 2025: USD 60.12 Billion

-

Market Size by 2035: USD 103.08 Billion

-

CAGR: 5.57% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Water-based Resin Market - Request Free Sample Report

Key Water-based Resin Market Trends

-

Shift toward low-VOC and eco-friendly formulations driven by strict environmental regulations worldwide.

-

Rising demand from construction and automotive sectors for sustainable, high-performance coating solutions.

-

Increasing adoption of water-based acrylic resins due to versatility and cost-effectiveness in coatings.

-

Growth in packaging industry usage for safer, non-toxic, and food-compliant adhesive applications.

-

Technological advancements improving durability, water resistance, and curing efficiency of resin systems.

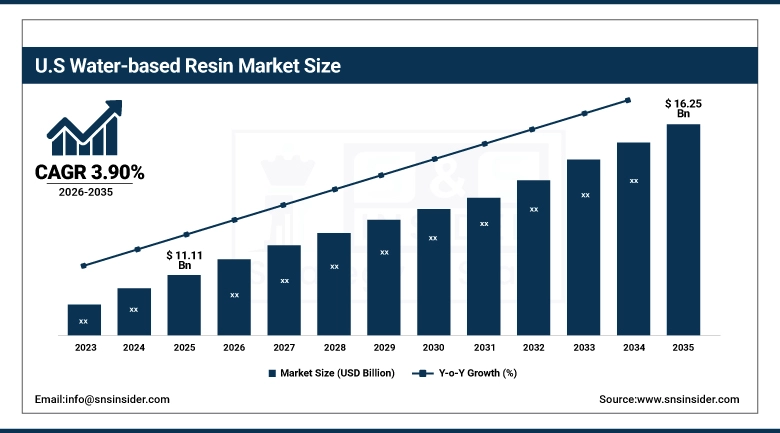

The U.S. Water-based Resin Market size was valued at USD 11.11 Billion in 2025 and is projected to reach USD 16.25 Billion by 2035, growing at a CAGR of 3.90% during 2026-2035. The U.S. market is the dominant national market within North America, characterized by a mature adoption profile in architectural and industrial coatings where water-based resin systems have been the regulatory standard for many years, a large packaging industry transitioning adhesive and coating specifications toward water-based systems in response to recyclability and food safety requirements, and a sophisticated industrial manufacturing base that consumes water-based adhesive and sealant resins across automotive assembly, electronics, and construction applications.

Water-based Resin Market Growth Drivers:

-

Water-based Resin Market Growth Drivers Rising Sustainability Demand and Regulatory Push for Low VOC Solutions Globally

Water based resin market is highly influenced by the increasing global awareness about sustainability and stringent regulations limiting VOC emissions. The rising demand for resins in the construction, automobile, and packaging sectors is also driving their use. Urbanization, industrialization, and infrastructure development, particularly in emerging economies, are fueling their usage. Innovations in technologies that offer improved performance and durability along with high water resistance capabilities are also contributing to the growth in the market. Moreover, the increased preference among consumers for non-toxic and safer products is driving demand.

Water-based Resin Market Restraints:

-

Water-based Resin Market Restraints High Production Costs and Performance Limitations Restricting Faster Adoption Across Industries Globally

Although there is significant growth in the market, there are limitations that include high costs of production compared to solvent-based products which restrict their use in cost-sensitive areas. Poor performance such as low resistance and high drying time makes the product less preferred in high performance industrial settings. Poor awareness and knowledge of production in underdeveloped countries make the market penetration difficult. Price volatility of raw materials and complicated process of formulation also pose major difficulties in production. There are compatibility problems with some substrates, and the product reacts unfavorably with some environments during its application.

Water-based Resin Market Opportunities:

-

Water-based Resin Market Opportunities Expansion in Green Materials and Advanced Industrial Applications Driving Future Growth Potential

Water-based resin industry represents lucrative avenues owing to increasing world movement towards environment friendly materials and recycling practices. Investment trends towards sustainable infrastructure construction and ecofriendly buildings are generating high demands for environmentally safe coating products. New uses in electric car packages and advanced adhesive formulations can contribute towards additional sales channels. Breakthroughs in biological and hybrid resin formulations will provide advanced performance abilities. Market expansion in Asia-Pacific, Latin American and Middle Eastern geographical locations represent new markets to tap into. Research and development efforts to improve durability, efficiency and economy of resins will drive future market expansion worldwide.

Water-based Resin Market Segment Analysis

-

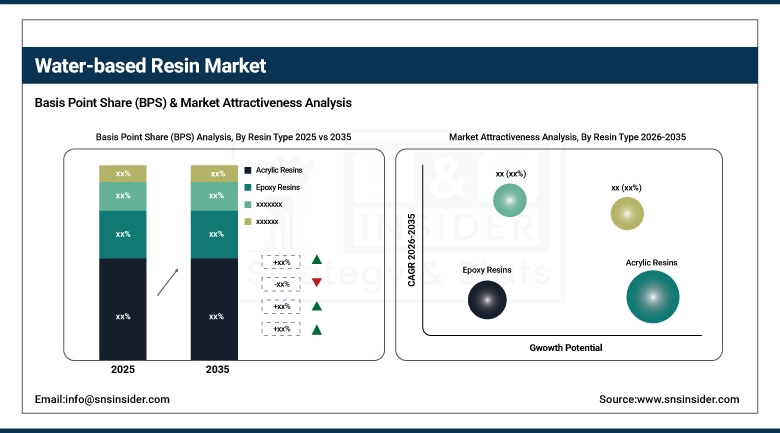

By Resin Type, Acrylic Resins dominated with 41.83% in 2025, and Polyurethane Resins are expected to grow at the fastest CAGR of 7.04% from 2026 to 2035.

-

By Application, Paints & Coatings dominated with 48.36% in 2025, and Printing Inks are expected to grow at the fastest CAGR of 6.75% from 2026 to 2035.

-

By End-Use Industry, Building & Construction dominated with 34.27% in 2025, and Packaging is expected to grow at the fastest CAGR of 6.68% from 2026 to 2035.

-

By Formulation Type, Water-Dispersible Resins dominated with 36.91% in 2025, and Water-Dispersible Resins are also expected to grow at the fastest CAGR of 5.91% from 2026 to 2035.

By Resin Type, Acrylic Resins Lead Water-based Resin Market While Polyurethane Resins Set for Fastest Growth 2026 to 2035

Acrylic resins hold significant market share in the water-based resin market because of their durability, adhesion, weather-resistance, and flexibility in coating and adhesive applications. The extensive application of acrylic resins in paints and coatings makes them dominant players in the market. On the other hand, the polyurethane resin segment is experiencing exponential growth owing to rising demands for durable, flexible, and abrasion-resistant products. In addition, the favorable properties of polyurethane resins in terms of mechanical strength and chemical resistance make them an ideal choice for various industrial applications.

By Application, Paints & Coatings Lead Water-based Resin Market While Printing Inks Show Fastest Growth 2026 to 2035

The paints and coatings sector dominates the market share for water-based resins, primarily due to high demand from the construction, automotive, and infrastructure development sectors. The environment-friendly and regulatory compliance attributes have made these products extremely popular. Printing inks emerge as the fastest-growing category, backed by growth in the packaging sector, e-commerce, and a surge in the demand for sustainable printing ink options. Growth in the use of water-based inks for printing on food packaging labels and flexible packaging materials has contributed immensely to the growth rate.

By End-Use Industry, Building & Construction Leads Water-based Resin Market While Packaging Shows Fastest Growth 2026 to 2035

The construction and building industry accounts for the majority share in the water-based resin market owing to its wide application in architectural coatings and adhesives. The packaging industry is witnessing high growth due to increased online transactions and stringent food safety standards. There is an increased demand for eco-friendly packaging solutions. Adhesives, coatings, and inks are gaining popularity in the packaging industry owing to their water-based nature. Increased environmental concerns coupled with stringent regulations are expected to boost adoption in both developed and developing countries.

By Formulation Type, Water-Dispersible Resins Lead and Maintain Fastest Growth in Water-based Resin Market 2026 to 2035

Water-dispersible resins have been taking over the market owing to their good stability, easy applicability, and better performance in coatings, adhesives, and inks. The suitability of such resins for a wide range of uses in the industrial sector makes them much sought after. These are the fastest-growing segments owing to the rising need for high-performance, low-VOC, and eco-friendly formulations. Improved formulating technology is improving durability, water-resistance, and effectiveness. The growing usage in the construction, automotive, and packaging sectors is adding fuel to the fire.

Water-based Resin Market Regional Analysis

Europe Water-based Resin Market Insights

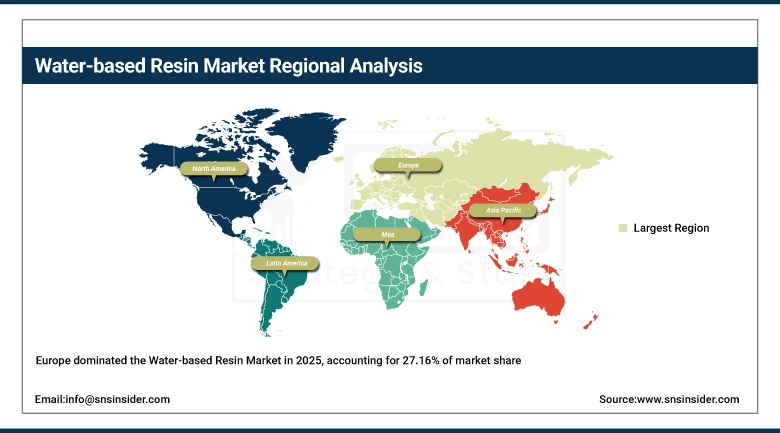

Europe held 27.16% at USD 16.33 Billion in 2025, growing at a CAGR of 4.71% through 2035. Europe is the global leader in regulatory-driven water-based resin adoption, with the EU's Decopaint Directive, Industrial Emissions Directive, and REACH regulation collectively establishing the world's most comprehensive framework of VOC emission and chemical safety standards that have driven water-based resin adoption across architectural, automotive, industrial, and specialty coating applications over the past two decades. Germany, France, the UK, the Netherlands, and Italy are the five largest national markets within the region by water-based resin consumption volume, reflecting the concentration of automotive manufacturing, coatings production, and industrial activity in Western Europe. BASF SE, Covestro AG, Allnex GmbH, and Arkema S.A. are the most significant European producers of water-based resin systems, with manufacturing operations across multiple countries that supply both the European domestic market and global export customers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Germany Water-based Resin Market Insights

Germany was the leading national market for water-based resins in Europe in 2025, driven by the country's large automotive manufacturing and coatings supply chain that represents one of the world's most advanced adopters of water-based coating resin systems, the presence of BASF SE's global dispersions and resins business and Covestro AG's polyurethane dispersions operations, and a construction industry that operates under rigorous indoor emission standards that have established water-based resin formulations as the default specification in commercial and residential interior coating and adhesive applications.

North America Water-based Resin Market Insights

North America held a 21.84% share of the global Water-based Resin Market in 2025 at USD 13.13 Billion, growing at the slowest regional CAGR of 4.17% through 2035. The region's relatively moderate growth rate reflects the maturity of water-based resin adoption in its largest application markets, where architectural paints, construction adhesives, and industrial coatings transitioned to water-based systems under regulatory pressure many years ago, limiting the incremental conversion opportunity that drives faster growth in less-mature markets. The region's market stability is anchored by a large replacement demand in existing applications and growing demand from flexible packaging and printing ink segments where transition from solvent-based to water-based systems is still actively underway. Dow Inc., Celanese Corporation, and Eastman Chemical Company are significant North American producers of water-based resin systems across acrylic, polyurethane, and vinyl acetate emulsion categories.

U.S. Water-based Resin Market Insights

The United States dominated North America's water-based resin market at 84.62%, USD 11.11 Billion in 2025. The U.S. is the world's most developed single national market for water-based resin applications, with the architectural coatings, industrial maintenance, and flexible packaging segments having undergone extensive water-based transitions that have established water-based systems as the formulation standard in most major application categories.

Asia Pacific Water-based Resin Market Insights

Asia Pacific is the largest and fastest-growing region at a CAGR of 6.68% through 2035, valued at USD 26.62 Billion in 2025 and projected to reach USD 50.70 Billion by 2035. China is by far the dominant national market within the region and the single largest consumer of water-based resins globally, driven by the enormous scale of its architectural paint, automotive coating, packaging, and printing ink industries and the aggressive national regulatory program targeting VOC emission reduction from industrial and building coating applications that has been one of the most powerful drivers of water-based resin demand globally over the past five years. India is the region's second-fastest-growing national market as urbanization, manufacturing growth, and rising environmental regulatory standards across coatings and adhesives drive water-based adoption in a market where solvent-borne systems still account for a significant share of industrial applications. Japan and South Korea represent technically advanced water-based resin markets where high-performance polyurethane and acrylic dispersion systems for automotive, electronics, and specialty coating applications drive per-unit-value demand significantly above regional commodity averages.

China Water-based Resin Market Insights

China leads the Asia Pacific Water-based resins market owing to its vast industrial base, active construction industry, and high demand for coatings India comes next, boosted by development in infrastructure, manufacture of automobiles, and regulations favoring adoption of eco-friendly low VOC resins.

Latin America (LATAM) and Middle East & Africa (MEA) Water-based Resin Market Insights

Latin America was valued at USD 2.38 Billion in 2025 and is growing at a CAGR of 4.59% through 2035, with Brazil and Mexico representing the two largest national markets within the region across architectural paints, automotive coatings, and packaging adhesive applications. Brazil's large domestic architectural paint market, dominated by Sherwin-Williams' Tintas Coral and Suvinil brands that have progressively transitioned their product ranges to water-based acrylic systems, is the primary driver of regional water-based resin demand, supplemented by the country's growing flexible packaging and industrial coating sectors. Middle East and Africa was valued at USD 1.67 Billion in 2025 and is growing at the fastest regional CAGR of 6.62% through 2035, with construction activity in Gulf states, South Africa, and growing North African economies generating demand for water-based architectural and industrial coating resins, supplemented by manufacturing sector growth in countries including Morocco, Egypt, and the UAE that is expanding the industrial coatings and adhesives consumption base within the region.

Competitive Landscape for Water-based Resin Market:

BASF SE is located in Ludwigshafen, Germany, and is the biggest maker of waterborne resin dispersions, with its production and sales value ranking first worldwide. Its products are mainly acrylic, polyurethane, and vinyl acetate emulsion polymers and include Acronal, Joncryl, Dispersol, and Lupranat.

-

In 2024, BASF SE launched an expanded range of bio-attributed acrylic dispersion products under its Acronal ECO line, produced using bio-based acrylic acid derived from renewable feedstocks that reduce the fossil carbon content of the resin by up to 50% compared to conventional petroleum-derived acrylic dispersions, targeting coatings and adhesives customers with product carbon footprint reduction commitments that require documented Scope 3 emission improvements in their raw material supply chains.

Covestro AG, whose corporate headquarters are based in Leverkusen, Germany, is one of the market leaders in the water dispersible polyurethane resin systems category under the Bayhydrol range of products, manufacturing and distributing premium performance PUD coating and adhesive resins for applications in the automotive industry, wood, leather, and textiles markets in Europe, Asia Pacific, and North America. The superior knowledge in the chemistry of polyurethane compounds coupled with an efficient isocyanate sourcing process allows Covestro to occupy an advantageous market position in the premium water-based resins category.

- In 2024, Covestro AG expanded its Bayhydrol water-dispersible polyurethane resin production capacity at its Map Ta Phut facility in Thailand to address growing demand from Southeast Asian automotive Tier 1 coating suppliers and wood coating manufacturers who are transitioning from solvent-borne polyurethane coating systems to water-based PUD alternatives in response to Thailand and Vietnam's progressively tightening VOC emission regulations for industrial coating operations and increasingly common sustainability-based procurement requirements from export market customers in Europe and Japan.

Water-based Resin Market Key Players:

-

BASF SE

-

Dow Inc.

-

Arkema S.A.

-

Covestro AG

-

Celanese Corporation

-

DIC Corporation

-

Eastman Chemical Company

-

Evonik Industries AG

-

H.B. Fuller Company

-

Lubrizol Corporation

-

Momentive Performance Materials Inc.

-

Nan Ya Plastics Corporation

-

Solvay S.A.

-

Synthomer plc

-

Wanhua Chemical Group

-

Hexion Inc.

-

ADEKA Corporation

-

Olin Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 60.12 Billion |

| Market Size by 2035 | USD 103.08 Billion |

| CAGR | CAGR of 5.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Acrylic Resins, Epoxy Resins, Polyurethane Resins, Alkyd Resins, and Polyester & Others) • By Application (Paints & Coatings, Adhesives & Sealants, Printing Inks, and Others (Textiles, Paper, Construction, etc.)) • By End-Use Industry (Building & Construction, Automotive, Packaging, Textile & Paper, and Industrial) • By Formulation Type (Water-Soluble Resins, Water-Dispersible Resins, and Emulsion-Based Resins) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Inc., Arkema S.A., Allnex GmbH, Covestro AG, Celanese Corporation, DIC Corporation, Eastman Chemical Company, Evonik Industries AG, H.B. Fuller Company, Huntsman Corporation, Lubrizol Corporation, Momentive Performance Materials Inc., Nan Ya Plastics Corporation, Solvay S.A., Synthomer plc, Wanhua Chemical Group, Hexion Inc., ADEKA Corporation, Olin Corporation |

Frequently Asked Questions

Asia Pacific led the Water-based Resin Market in 2025.

Acrylic Resins dominated the Water-based Resin Market with a 41.83% share in 2025.

Key drivers include tightening global VOC emission regulations for coatings, adhesives, and printing inks, growing packaging sustainability commitments from brand owners requiring water-based lamination and coating systems, and rapid industrialization and regulatory enforcement in Asia Pacific accelerating the shift from solvent-borne to water-based resin systems across all major application sectors.

The Water-based Resin Market size was USD 60.12 Billion in 2025 and is projected to reach USD 103.08 Billion by 2035.

The Water-based Resin Market is expected to grow at a CAGR of 5.57% from 2026-2035.

Get in Touch