Water Treatment Chemicals Market Report Scope & Overview:

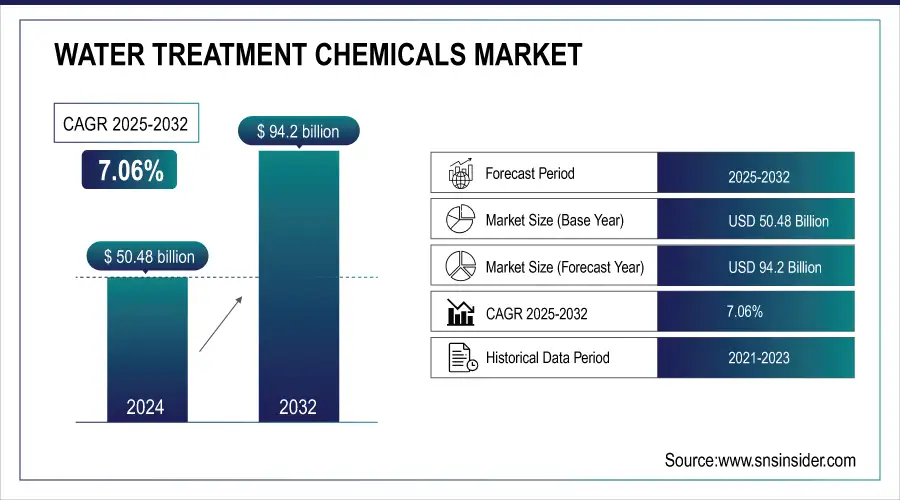

The Water Treatment Chemicals Market Size was valued at USD 50.48 billion in 2024, and is expected to reach USD 94.2 billion by 2032, and grow at a CAGR of 7.06% over the forecast period 2024-2032.

The water treatment chemicals market is presently undergoing significant transformation, impelled by a set of dynamic factors and recent technological changes. Various growing concerns regarding water contamination and toxic pollutants have increased interest in the implementation of new water treatments to eliminate such harmful contaminants as "forever chemicals" (PFAS). These chemical compounds are notorious for being persistent in the environment; hence, they become of prime concern to regulatory bodies and also to industry players. The recent water filtration technologies being developed are indicative of the market's proactive ways of handling persistent contaminants. This involves the unveiling of a breakthrough filtration material in September 2024 that is said to have the potential to effectively remove long-lasting chemicals from water. This new material employs an advanced filtration technique that can target and remove such stubborn pollutants and thus could be a potential solution for the problem of the persistence of water contamination. This further illustrates an increasing focus on the development of specialty materials with the capability to resolve complex water quality issues.

Get More Information on Water Treatment Chemicals Market - Request Sample Report

Additionally, in January 2024, such zwitterionic hydrogels were developed by scientists that showed rapid removal of micropollutants from water. These hydrogels take advantage of their peculiar chemical nature to attract and neutralize the pollutants, thus joining the ranks of water purification chemicals. Their capability for fast and effective withdrawal of contaminants underlines the commitment of this industry to the ongoing improvement of methods for water purification and the fulfillment of more and more strict regulatory limits.

Furthermore, the advanced treatment technology commitment, in May 2023, it was reported that a new PFAS removal method in water was developed. Such treatment combines various chemicals to degrade the tough-to-break pollutant and thus manifests effort into one of the most challenging environmental concerns. The continuous development and refinement of such methods are representative of the market commitment to improvement in assurance about water safety and emerging contamination concerns. Similarly, in April 2024, the EPA set new limits on the levels of PFAS in drinking water, reflecting heightened regulatory pressure on the water treatment industry. These regulations will lead to more intense processes of water treatment, further spurring innovation in water treatment chemicals. Companies are subsequently upgrading their products to current standards and appropriate solutions for safe water.

Moreover, the chemical storage facilities in Raleigh, North Carolina, were enhanced in July 2024 to improve the security of its water supply. This would indeed reflect the practical measures taken to ensure sufficient and safe storage of water treatment chemicals to be highly instrumental in maintaining effectiveness in treatment processes and public health. The water treatment chemicals market is experiencing swift growth based on the development of technologies, variations in regulatory environments, and increases in demands for effective solutions against water pollution. Alongside new material and technique development, growing regulatory pressures will also help shape the future of water treatment with emerging challenges faced by the industry.

Water Treatment Chemicals Market Size and Forecast:

-

Market Size in 2024: USD 50.48 Billion

-

Market Size by 2032: USD 94.20 Billion

-

CAGR: 7.06% (2024–2032)

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

Key Water Treatment Chemicals Market Trends

-

Growing adoption of green and biodegradable chemicals driven by sustainability and stricter discharge regulations.

-

Rising demand for advanced coagulants and flocculants in municipal and industrial wastewater treatment.

-

Increasing integration of digital monitoring and smart dosing systems to optimize chemical usage and reduce operational costs.

-

Expansion of desalination projects, especially in water-scarce regions like the Middle East and Asia-Pacific.

-

Strong growth in industrial wastewater recycling and reuse initiatives to support circular economy models.

-

Consolidation through M&A and strategic partnerships among key players to strengthen portfolios and global reach.

-

Accelerated adoption in emerging economies due to rapid urbanization, industrialization, and infrastructure development.

Water Treatment Chemicals Market Growth Drivers

-

Increasing regulatory pressures to remove contaminants like PFAS are driving innovation and demand for advanced water treatment chemicals.

Increasing regulatory pressures to eliminate contaminants such as PFAS are one of the major driving forces for innovation and demand in the Water Treatment Chemicals Market. As governments and environmental agencies around the world set stricter regulations on the permissible levels of hazardous substances in drinking water, companies are driven to innovate better and more efficient means of treatment. For example, the US EPA has imposed strict limits on PFAS concentrations; thus, water utilities and treatment plants have to seek emerging technologies capable of meeting such standards and installing them. Companies have been investing in developing special adsorbents and ion exchange resins for efficient capture and removal of PFAS from water supplies. The European Union in Europe has imposed regulations classifying PFAS as substances of concern, inspiring the development of novel chemical formulations targeting these contaminants. Companies like 3M and DuPont have active research and commercialization efforts regarding novel chemical treatments and filtration media that are targeted and specifically engineered to address PFAS and other emerging pollutants. These economies achieve not only regulatory compliance but also the improvement of water safety and quality-clear indications of how the market responds to continuously changing environmental standards. Therefore, regulatory pressures will keep on increasing, imposing the necessity for advanced and effective chemicals in water treatment.

• Investments in advanced filtration technologies are increasingly being driven by the environmental and health impacts of polluted water sources.

Increasing awareness of environmental effects, along with increasing health-related effects due to contaminated water, has been one of the prime reasons for investment in improved filtration technologies within the water treatment chemicals market. As more and more people are becoming aware of the health and ecological costs arising from polluted water, demand is increasing. Incidents like water contamination recently brought to the fore in the lead crisis of Flint, Michigan- have driven massive investments into new filtration technologies. Greater awareness has made sure that substantial funds flow toward advanced filtration systems, which can remove a wider range of contaminants present in water supplies, from heavy metals to pharmaceuticals and microplastics. In response to this demand, new advanced filtration technologies have emerged and commercialized from companies including Danaher and Pentair, such as ultrafiltration membranes and advanced oxidation processes, improving water purity and safety. The ecological impacts of water pollution, ranging from aquatic life to biodiversity, increasingly raise awareness that fuels investments into environmentally friendly water treatment technologies. These advanced solutions are further being accelerated through government incentives and public-private partnerships, reflecting a proactive approach toward better water treatment and sustainability. On account of increasing awareness, there is likely to be more stringent enforcement for innovative and efficient filtration technologies, hence ongoing developments and increased market activity in the sector of water treatment chemicals.

Water Treatment Chemicals Market Restraints

-

High costs associated with developing and implementing advanced water treatment technologies can limit adoption, especially in developing regions.

High costs developed and involved in the implementation of advanced water treatment technologies can greatly impede this technology's adoption, especially in developing regions. Advanced filtration systems, chemical treatments involving nanotechnology or advanced oxidation processes, and related filtration systems are extremely capital-intensive in terms of research, infrastructure, and maintenance costs. In developing countries, where the budgets for water infrastructures are very limited, such high costs become unaffordable. For instance, state-of-the-art advanced reverse osmosis systems or electrochemical treatments require high investments not only in their purchase but also in their operational use fact that most countries with limited resources might hardly be able to bear continuously. As a result, a large number of developing regions may hardly adopt these technologies, continuing to rely on more traditional methods that already appear less effective and do not fully address emerging water quality issues. Presently, sophisticated solutions are financially prohibitive for widespread application, which means there is a requirement to deal with complicated contaminants for better water safety.

Water Treatment Chemicals Market Opportunities

-

Emerging markets present significant growth potential for water treatment chemicals as infrastructure development and environmental regulations expand.

Infrastructure development and expanding environmental regulations in emerging markets have created large growth opportunities for water treatment chemicals. As investment in the upgrading and expansion of infrastructure within the water market in emerging regions continues to rise to meet the increasing population and urbanization, so does the need for appropriate and effective water treatment. Specifically, the increased enforcement of higher environmental standards in countries of Southeast Asia and Africa has increasingly realized water pollution and improvements in public health using new systems for water purification. It is on these bases that companies specializing in water treatment chemicals find a fertile environment to introduce their products and technologies. While investments in state-of-the-art water treatment plants and improvements in regulatory frameworks have created the need for advanced sophisticated chemicals to treat a wide range of contaminants, these markets, though at constant development processes, do nevertheless represent some major opportunities for growth and innovation in the water treatment area. Companies could be brought into a strategic position by leveraging the growing demand for effective and efficient treatments.

Water Treatment Chemicals Market Challenge:

• Rapid technological advancements require continuous investment in research and development, posing a challenge for companies to keep pace and remain competitive.

The high pace at which water treatment chemicals technology is unfolding calls for almost incessant reinvestment in research and development. Hence, the main challenge to any competitive company is the pressure to continuously innovate along with every new technology such as advanced filtration materials or novel chemical treatments so as not to fall behind. For instance, enterprises that work on the development of the latest nanomaterials or smart water monitoring systems usually require substantial R&D investments regarding the creation and commercialization of such value-enhanced solutions. These continuous investment needs may outweigh financial burdens and thus become a real entry barrier for small companies or low-budget enterprises since they hardly can compete with the leading group to whom such investments could be easier to bear. Consequently, companies have to balance their R&D expenditures against other needs for operations to offer state-of-the-art products that can meet new and emerging water quality problems.

Water Treatment Chemicals Market Segment Analysis:

By End-use Industry

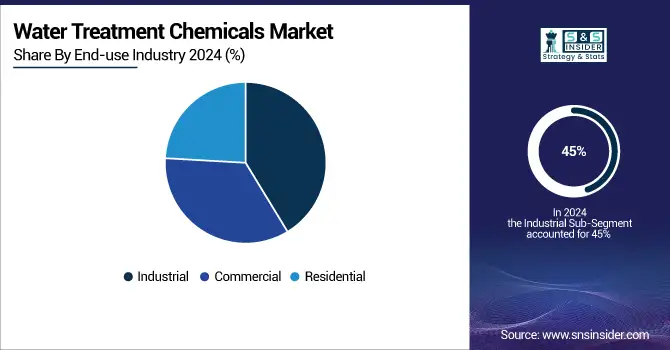

The Industrial segment dominated the Water Treatment Chemicals Market and accounted for approximately 45% of the estimated share in 2023. Major driving factors such as extensive application in power generation, oil and gas extraction industries, chemicals, and mining drive the dominance of this segment. Most of the processes in industries require massive usage of water, which has to be treated for various reasons: to assure efficiency in operations, to prevent any damage to machinery or equipment involved in the process, and to follow environmental laws. For instance, the chemical treatment in power generation involves boiler water treatment and cooling systems, while in the oil and gas segment, the applications are found in enhanced oil recovery and the treatment of produced water. Since all these industries are in great demand, the extensive use of water treatment chemicals in these industries significantly contributes to the leading market share of the Industrial segment.

By Type

The coagulants and flocculants segment dominated the Water Treatment Chemicals Market in 2023, commanding a market share of approximately 35%, as per estimation. This can be because coagulants and flocculants have the largest applicative areas in water treatment, be it for municipalities, industrial processes, or other wastewater treatments. Such chemicals are mainly used for the removal of suspended solids and impurities from water through the aggregation of particles into large clumps that could be later easily separated by filtration or sedimentation. For example, the most commonly applied coagulants and flocculants in water treatment involve alum and polyacrylamide; these are essential agents that should be involved in the treatment of drinking water so that it meet safety standards and is appropriate for consumption. Their effectiveness in improving process effectiveness for water purification and applicability to a wide range of industries keeps them way ahead of other competitors.

By Application

Cooling Water Treatment dominated and accounted for about 40% of the total Water Treatment Chemicals Market in 2023. This is primarily because cooling water treatment has become an indispensable aspect of the functioning of all industries and the generation of power. Cooling systems form an integral part of industrial processes and generation of power to dissipate the built-up heat. Water treatment programs are meant to address the issues of scaling, corrosion, and biological fouling, each of which may reduce system efficiency. Most of the chemical treatment applied to the cooling towers in the power plants for efficient performance and a longer life span includes scale inhibitors and biocides. This underlines a high segment of the market, involving the high volume of cooling water used and the critical need to ensure operational efficiency with reduced downtime.

Water Treatment Chemicals Market Regional Outlook

North America Water Treatment Chemicals Market Insights

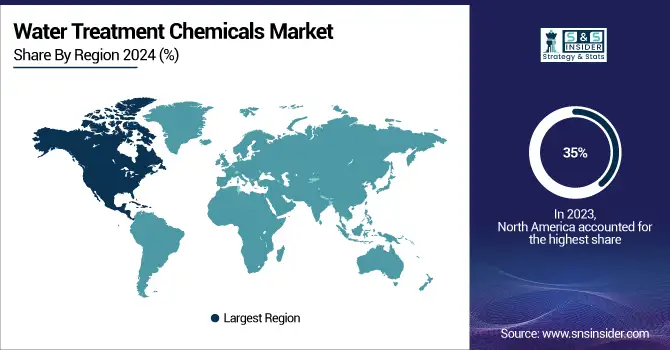

In 2023, North America dominated the Water Treatment Chemicals Market, contributing around 35% to the total estimate, considering the region has highly developed infrastructure for industries, stringent environmental regulations, and soaring demands across multiple sectors. For instance, the U.S. and Canada have very strong industrial activities in areas such as power generation, chemical manufacturing, etc., for which large-scale water treatment is required to regulate processes and meet regulatory standards. Further, substantial investments in upgrading water treatment plants and controlling emerging contaminants have also strengthened the market growth in this region. Thus, the strong orientation of North America toward both water quality and technology within treatment methods cements its leading position in the global market.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Asia Pacific Water Treatment Chemicals Market Insights

The APAC is estimated to lead the Water Treatment Chemicals Market in 2024 owing to rapid increasing urbanization, industrialization and growing water scarcity concerns in China, India and Southeast Asia. Increased government spending toward municipal water treatment plants with more stringent environmental regulations is expected to drive demand for coagulants, flocculants, and disinfectants. "Moreover, strong growth is underpinned by high consumption for water in power generation, textiles and the food and beverage industry in the area."

Europe Water Treatment Chemicals Market Insights

Europe is a developed but slowly growing market, driven by stringent water quality regulations and policies on sustainability in the EU. Countries such as Germany, France and the UK are increasingly inclined towards greener and bio-based chemical formulations, with a view to reduce environmental footprint. The industrial water reuse and zero-liquid-discharge technologies, and the presence of relatively large number of chemical and pharmaceutical industries are again driving the demand for treatment chemical market.

Latin America (LATAM) Water Treatment Chemicals Market Insights

In Latin America, the market demand is increasing due to water pollution concerns and the upgrade of treatment plants. Brazil, Mexico and Chile are driving usage with help from government efforts to improve access to clean drinking water. End-users include mining, oil & gas, and food processing industries that require specialty chemicals to enhance purification performance and comply with regulations.

Middle East & Africa Water Treatment Chemicals Market Insights

Middle East & Africa market is growing fast on account of acute water shortage in this region and extensive use of desalination technologies in Gulf countries such as Saudi Arabia, Saudi Arabia, and Qatar. Demand from projects for large-scale water treatment and for advanced chemicals used in scaling, corrosion prevention, and microbial control will support gains. In Africa urbanization and the development of industry, especially in South Africa and Egypt, are also fuelling the growth of the market.

Competitive Landscape for Water Treatment Chemicals Market:

Kemira OYJ

Kemira is a leading global provider of sustainable chemical solutions for water-intensive industries, specializing in coagulants, flocculants, and biocides for municipal and industrial water treatment.

-

In February 2024, Kemira launched a new range of biodegradable flocculants in Europe to help municipalities meet stringent EU wastewater treatment regulations.

Lanxess AG

Lanxess develops specialty chemicals, including water treatment solutions such as ion exchange resins and disinfectants, serving industrial and municipal clients worldwide.

-

In May 2024, Lanxess expanded its ion exchange resin production facility in Leverkusen, Germany, to meet growing demand for ultrapure water in power generation and semiconductor industries.

Water Treatment Chemicals Market Companies are

-

Lanxess

-

DuPont

-

Akzo Nobel NV

-

Solenis LLC

-

Ecolab Inc

-

Baker Hughes

-

Suez SA

-

Lonza Group

-

LG Chem Ltd.

-

BASF SE

-

Eastman Chemical Company

-

Evonik Industries AG

-

Mitsubishi Chemical Group Corporation

-

Huntsman Corporation

-

Dow Inc.

-

Clariant AG

-

Perstorp Holding AB

-

Arkema S.A.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 50.48 Billion |

| Market Size by 2032 | USD 94.20 Billion |

| CAGR | CAGR of 7.06% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Coagulants & Flocculants, pH Adjusters & Softeners, Biocides & Disinfectants, Scale Inhibitors & Dispersants, Corrosion Inhibitors, Chelating agents, Anti-foaming agents, Others) •By Application (Boiler water treatment, Cooling water treatment, Raw water treatment, Water Desalination, Chemical processing, Power generation, Others) •By End-use Industry (Residential, Commercial, Industrial, Power, Oil and Gas, Chemical Manufacturing, Mining and Mineral Processing, Food and Beverage, Pulp and Paper, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Kemira OYJ, Lanxess, DuPont, Akzo Nobel NV, Solenis LLC, Ecolab Inc, Baker Hughes, Suez SA, Lonza Group, LG Chem Ltd., BASF SE, Eastman Chemical Company, Merck KGaA, Evonik Industries AG, Mitsubishi Chemical Group Corporation, Huntsman Corporation, Dow Inc., Clariant AG, Perstorp Holding AB, Arkema S.A. |

Frequently Asked Questions

Yes.

Kemira OYJ (Finland), Lanxess (Germany), DuPont (US), Akzo Nobel NV (Netherlands), Solenis LLC (US), Ecolab Inc (US),Baker Hughes (US), Suez SA (France) and, Lonza Group (Switzerland) are some of the major players of the Global Water Treatment Chemicals Market.

Emerging markets present significant opportunities for water treatment chemicals as infrastructure development and environmental regulations expand.

The Water Treatment Chemicals Market is expected to grow at a CAGR of 7.06%.

The Water Treatment Chemicals Market Size was valued at USD 50.48 billion in 2024 and is expected to reach USD 94.20 billion by 2032.

Get in Touch