Wellness Supplements Market Report Scope & Overview:

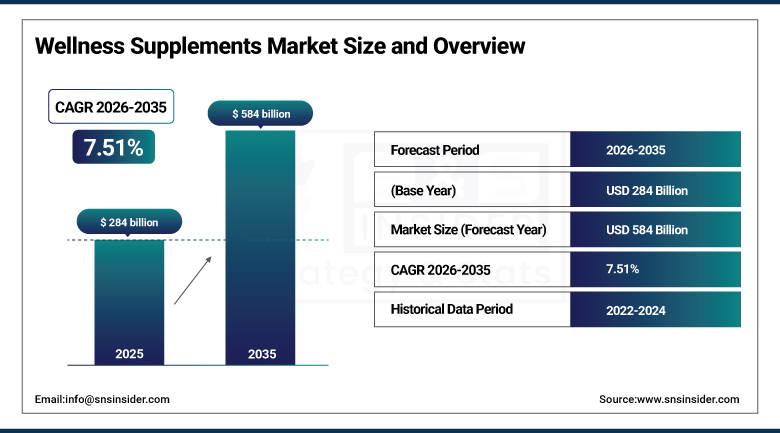

The Wellness Supplements Market was valued at USD 284 billion in 2025 and is expected to reach USD 584 billion by 2035, growing at a CAGR of 7.51% from 2026-2035.

Wellness Supplements Market growth has been propelled by the increased consciousness for health across the globe and the growing importance of preventive healthcare and strengthening the body's immunity. Consumers are relying more and more on vitamin, protein, and herbal supplements to tackle lifestyle diseases as well as stay healthy. Fitness culture, aging population, and busy schedules in the cities are contributing to this growth. Growth in e-commerce websites and subscription-based services is helping consumers get easy access to the products. Personalization and innovation have played crucial roles in boosting market growth globally.

The Council for Responsible Nutrition's 2023 Consumer Survey on Dietary Supplements documents that 77% of U.S. adults take dietary supplements, the highest reported rate in survey history, with multivitamins, vitamin D, and omega-3 fatty acids as the three most commonly consumed supplement categories.

The Global Wellness Institute's 2023 wellness economy report values the global dietary supplement market as the second-largest wellness economy segment after personal care, reflecting the category's commercial scale relative to fitness, healthy eating, and traditional medicine wellness sectors.

Wellness Supplements Market Size and Forecast

-

Market Size in 2025: USD 284 Billion

-

Market Size by 2035: USD 584 Billion

-

CAGR: 7.51% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Wellness Supplements Market - Request Free Sample Report

Wellness Supplements Market Trends

-

Rising focus on preventive healthcare and healthy lifestyles is driving the wellness supplements market.

-

Growing adoption of vitamins, minerals, probiotics, and herbal supplements is boosting market growth.

-

Expansion of fitness culture and personalized nutrition trends is fueling product demand.

-

Increasing awareness of immunity, gut health, and mental well-being is shaping adoption trends.

-

Advancements in nutraceutical formulations, clean-label products, and bioavailable ingredients are enhancing effectiveness.

-

Rising e-commerce penetration and direct-to-consumer brands are supporting market expansion.

-

Collaborations between supplement manufacturers, healthcare professionals, and wellness brands are accelerating innovation and global adoption.

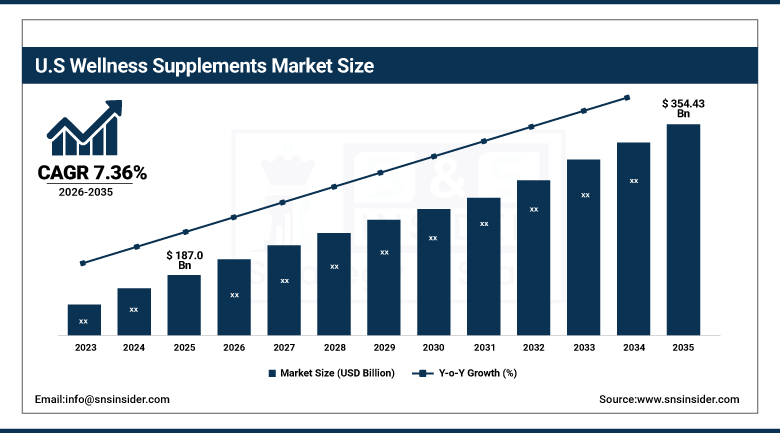

U.S. Wellness Supplements Market was valued at USD 187.0 billion in 2023 and is expected to reach USD 354.43 billion by 2032, growing at a CAGR of 7.36% from 2026-2035.

The United States’ Wellness Supplements Market is witnessing steady growth owing to increased health awareness, focus on preventive healthcare, and increased consumer interest in vitamin-based, protein-based, and immunity-boosting supplements. An increasing trend towards fitness along with hectic lifestyles and the aging population base are also contributing to supplement usage in a significant manner.

The Natural Marketing Institute's 2024 Health and Wellness Report documents that the average U.S. supplement consumer spends USD 712 annually on dietary supplements a per-capita spend that is 3.2x the global average reflecting the depth of supplement integration into U.S. health and wellness routines.

Amazon's supplement category which generated estimated USD 12 billion in U.S. supplement sales in 2023 is the world's largest single supplement distribution platform, demonstrating the e-commerce transformation of supplement retail that has enabled thousands of DTC supplement brands to compete nationally without retail shelf space.

Wellness Supplements Market Segment Analysis

-

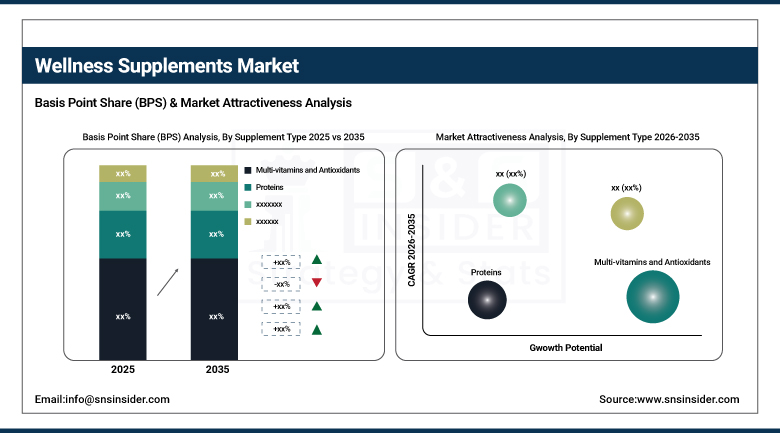

By Supplement Type, Multi-vitamins and Antioxidants segment dominated the Wellness Supplements Market in 2025 with ~34% share; Proteins segment is fastest growing (CAGR).

-

By Application, Immune Health segment dominated the Wellness Supplements Market in 2025 with ~29% share; Weight Management segment is fastest growing (CAGR).

-

By Form, Capsules & Tablets segment dominated the Wellness Supplements Market in 2025 with ~36% share; Gummies & Softgels segment is fastest growing (CAGR).

-

By Distribution Channel, Offline segment dominated the Wellness Supplements Market in 2025 with ~55% share; Online segment is fastest growing (CAGR).

By Supplement Type, Multi-vitamins & Antioxidants segment dominates the Wellness Supplements Market, Protein Supplements segment expected to grow fastest.

Multi-vitamins and antioxidants dominate the Wellness Supplements Market because of their multi-purpose nature and preventive healthcare. These supplements have numerous benefits such as supporting overall nutrition, boosting immunity, and helping protect cells, thus catering to all consumers irrespective of their ages. The fact that they are easy to consume and recommended by healthcare experts is also contributing to their popularity.

The fastest-growing supplements category is represented by protein supplements, which can be explained by the increased awareness regarding fitness and active lifestyles. In addition, many people are participating in sports and training sessions at the gyms and other similar venues. Therefore, a high demand for protein supplements for building muscles and managing body weight is currently observed. Increasing interest in functional nutrition and plant-based proteins is also driving growth.

By Application, Immune Health segment dominates the Wellness Supplements Market, Weight Management segment expected to grow fastest.

Immune health dominates the Wellness Supplements Market owing to their growing preference for preventive measures and wellness. There is a rising trend of consumers choosing products which boost immunity levels, owing to heightened awareness about health along with certain weaknesses associated with lifestyles. Products which can be made up of vitamins, minerals, and herbs, among other elements, are commonly used for boosting immunity levels.

Weight management segment are forecasted to have the highest CAGR, owing to the increase in obesity and sedentary habits, and rising trends toward fitness and proper dieting. Increasingly, consumers will be looking for weight loss supplements that can promote weight management through fat burning, metabolism boosters, and appetite suppressants. Fitness regimes and body transformations will also play a major role in its growing demand.

By Form, Capsules & Tablets segment dominates the Wellness Supplements Market, Gummies & Softgels segment expected to grow fastest.

Capsules and tablets account for a large share of the Wellness Supplements Market because they are easy to consume, provide accurate dosages, have a longer shelf life, and are well known by consumers. The production and distribution of these types of supplements are simple, making them the most popular choice by far among pharmaceutical and nutraceutical companies. The high degree of acceptance by health care providers and consumers also plays a role in making them the most popular choice.

Gummies and softgels are the fastest growing segment, because they are more palatable and convenient to consume than tablets and capsules, and they appeal more to consumers, particularly the young generation. These types of supplements make taking vitamins more enjoyable than regular pills, thus improving adherence to their daily intake. The growing demand for more innovative and convenient health products is contributing to their popularity in different markets.

By Distribution Channel, Offline segment dominates the Wellness Supplements Market, Online segment expected to grow fastest.

Offline channels will continue to dominate the market because of high trust among customers in pharmacies, drug stores, and specialist health stores. A lot of customers feel more comfortable having consultations with the pharmacist or healthcare professional before buying their supplements. Well-developed distribution channels and easy availability of the product also contribute to this. The ease of evaluating a product and getting authentic products still makes offline channels highly attractive for sales.

Online distribution will be the fastest-growing distribution channel due to the growth of online business penetration, convenient buying experience, and high availability of products. People tend to buy their supplements online because of the convenience of doorstep delivery and better prices compared to offline channels. The development of specialized online stores that sell healthy products will increase the adoption rate of online distribution even further.

Wellness Supplements Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

86% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

North America Wellness Supplements Market Insights

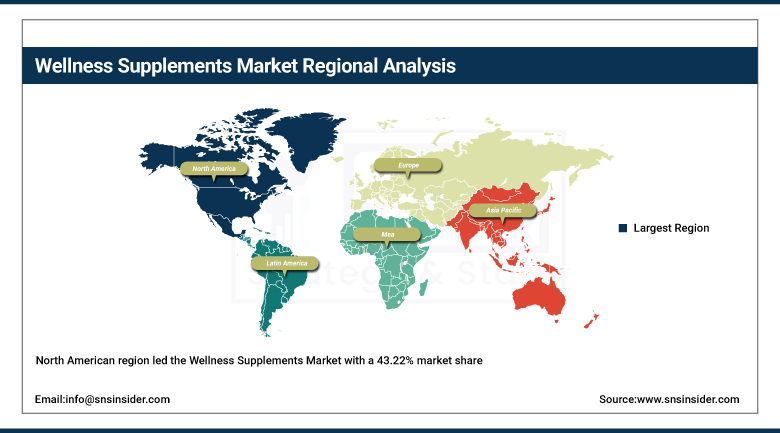

The North American region led the Wellness Supplements Market with a 43.22% market share owing to its high health awareness levels, high expenditure by consumers on preventive health care, and prevalence of vitamin, protein, and immune booster supplements. This region enjoys the advantage of having a matured nutraceuticals industry, efficient retail and online distribution networks, and presence of top global health supplement companies. In addition, the region’s growing emphasis on fitness and wellness practices amongst the population is contributing to the rise in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Wellness Supplements Market Insights

Asia-Pacific is currently the region with the fastest growth rate in the Wellness Supplements Market. This trend can be attributed to increased awareness about health, higher disposable incomes, and urbanization. The middle-class group in the Asia-Pacific region continues to grow; hence, an increased demand for vitamin, protein, and immune-strengthening supplements. There is also an increase in the number of lifestyle diseases in the region, which boosts the market growth rate. There has been considerable development of e-commerce sites, thereby making products easily available. Increased fitness trends, personal nutrition, and social media campaigns are fueling the market growth.

Europe Wellness Supplements Market Insights

The Europe Wellness Supplements Market is witnessing steady growth fueled by heightened health consciousness, an aging demographic, and preventive healthcare. The growing preference for immune support, vitamins, and herbal supplements is helping the market grow. Clean label and organic supplements are gaining popularity due to stringent food safety laws and quality awareness among consumers. Increasing online shopping and pharmacy sales are making supplements more accessible. Moreover, the growing trend of fitness and customized nutritional solutions is further promoting consumption of wellness supplements.

Middle East & Africa and Latin America Wellness Supplements Market Insights

The Middle East & Africa and Latin America Wellness Supplements Market is expanding at a constant pace because of growing health consciousness, increasing per capita income levels, and adoption of preventive care strategies. Increased urbanization and changed lifestyle patterns are fueling the consumption of supplements such as vitamins and proteins, along with immunity enhancers. The growing popularity of online shopping is making products available in both markets. Lack of awareness in rural areas and cost sensitiveness are two important challenges faced by the market.

Wellness Supplements Market Growth Drivers:

-

Rising Health Consciousness and Preventive Healthcare Adoption Driving Strong Demand for Wellness Supplements Across Global Consumer Markets

The growing recognition of the importance of preventive care and overall well-being is a major reason why there is an increased demand for wellness supplements among people globally. People are becoming more inclined towards gaining immunity, improving their energy levels, and maintaining their good health instead of opting for reactionary treatments. The growing trend of lifestyle illnesses such as obesity, diabetes, and heart disease is prompting people to opt for nutritional supplements as a routine practice. Apart from that, the growing role of social media and fitness influencers is also contributing to the growth of the market.

Wellness Supplements Market Restraints:

-

Presence of Strict Regulatory Frameworks and Product Quality Concerns Limiting Market Expansion in Certain Regions and Consumer Segments

The strict regulations and standards imposed on dietary supplements are posing difficulties for manufacturers and restraining market growth in many areas. The differences in licensing procedures, packaging laws, and ingredient usage regulations between countries make it difficult for multinational organizations to operate effectively. Also, issues concerning the legitimacy of products, the quality standards of these products, and any fraudulent health claims about their benefits have become a threat to consumer confidence. The absence of consistent testing measures in some underdeveloped nations makes this market risky.

Wellness Supplements Market Opportunities:

-

Growing Demand for Personalized Nutrition and AI Driven Supplement Recommendations Creating High Value Growth Opportunities in Wellness Market

Growing use of personalized nutritional products is opening up new growth avenues within the wellness supplements industry. The use of artificial intelligence and genetics tests is allowing organizations to provide customized supplement advice depending on personal health status, nutrition requirements, and living style. The rising tendency among consumers to opt for specialized health solutions such as immune boosters, fitness, and brain function are contributing to product development innovations. Personalized supplement services are increasingly becoming popular through subscription models because of their efficacy. Increasing digital healthcare ecosystems and wearable health gadgets will create future growth prospects in this domain.

Recent Developments:

-

Herbalife launched LifeGenetics platform in 2026, combining genetic risk scoring with AI-based supplement personalization through its distributor network, enabling scalable DNA-based nutrition recommendations without requiring traditional lab-based testing kits for consumers globally.

-

Nestlé Health Science acquired Persona Nutrition in 2025, strengthening its personalized supplement subscription capabilities and expanding its reach in the growing digital wellness segment, enhancing competition against DTC-focused nutrition and AI-driven personalized supplement platforms.

-

Pfizer Consumer Healthcare launched Centrum Silver 75+ reformulation in 2025, enhancing vitamin D3, magnesium glycinate, and CoQ10 levels to address the nutritional needs of aging populations, supporting rising demand among adults over 75 years globally.

Wellness Supplements Market Key Players

Some of the Wellness Supplements Market Companies

-

GNC

-

doTERRA International LLC

-

Herbalife Nutrition

-

Amway

-

Garden of Life

-

New Chapter, Inc.

-

Swisse

-

By-Health

-

Nature's Bounty

-

NOW Foods

-

Optimum Nutrition

-

USANA Health Sciences

-

Nature Made

-

Vitacost.com

-

Bodybuilding.com

-

International Vitamin Corporation

-

Abbott Laboratories

-

Arko Corp

-

Plexus Worldwide

-

New U Life

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 284 Billion |

| Market Size by 2035 | USD 584 Billion |

| CAGR | CAGR of 7.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Supplement Type (Proteins, Carbohydrates, Multi-vitamins and Antioxidants, Fibers, Minerals, Others) • By Application (Inflammatory Bowel Diseases, Metabolic Diseases, Weight Management, Women's Health, Allergic Disorders, Immune Health, Others) • By Form (Gummies & Softgels, Capsules & Tablets, Powder Form, Liquid Form, Others) • By Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GNC, doTERRA International LLC, Herbalife Nutrition, Amway, Garden of Life, New Chapter, Inc., Swisse, By-Health, Nature's Bounty, NOW Foods, Optimum Nutrition, USANA Health Sciences, Nature Made, Vitacost.com, Bodybuilding.com, International Vitamin Corporation, Abbott Laboratories, Arko Corp, Plexus Worldwide, New U Life. |

Frequently Asked Questions

North America dominated with approximately 43.22% share; Asia Pacific is the fastest growing at 8.49% CAGR.

Online distribution channel is the fastest growing segment (CAGR).

Immune Health segment dominated the Wellness Supplements Market with ~29% share; Weight Management segment is the fastest growing (CAGR).

The Wellness Supplements Market was valued at USD 284 billion in 2025.

The Wellness Supplements Market is expected to grow at a CAGR of 7.51% from 2026 to 2035.

Get in Touch