Zirconium Market Report Scope & Overview:

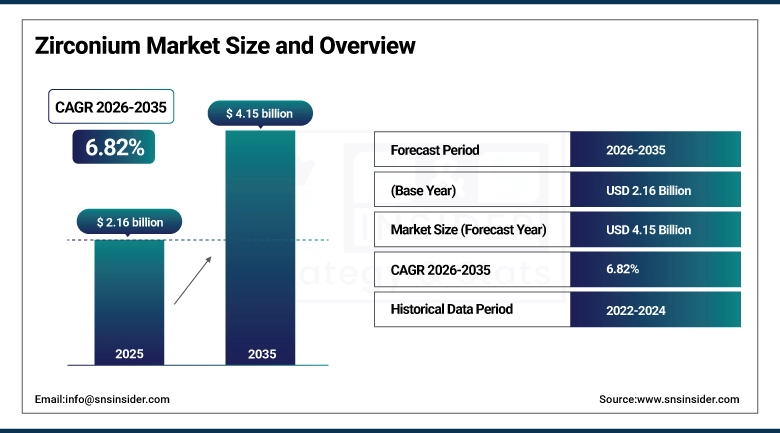

The Zirconium Market size was valued at USD 2.16 Billion in 2025 and is projected to reach USD 4.15 Billion by 2035, growing at a CAGR of 6.82% during 2026–2035.

Zirconium is a lustrous, grey-white transition metal derived primarily from the mineral zircon (ZrSiO₄) and baddeleyite (ZrO₂), extracted through mineral sand mining operations concentrated in Australia, South Africa, and a small number of other coastal deposit locations globally. The metal and its derivative compounds possess a combination of properties high melting point, corrosion resistance, low neutron absorption cross-section, and chemical stability across extreme temperature ranges that make it commercially indispensable across ceramics, refractories, nuclear energy, chemical processing, and advanced materials manufacturing.

Zirconium Market Size and Forecast:

-

Market Size in 2025: USD 2.16 Billion

-

Market Size by 2035: USD 4.15 Billion

-

CAGR: 6.82% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Zirconium Market - Request Free Sample Report

Key Zirconium Market Trends:

-

Nuclear energy capacity additions in China, India, and Eastern Europe are expanding demand for zirconium alloy cladding tubes at a rate that is creating supply security concerns among reactor operators outside existing supply chains.

-

Advanced zirconia ceramics are gaining share in dental restoration, joint replacement, and medical implant applications as manufacturing precision and biocompatibility documentation improve.

-

Zirconium-based catalysts are attracting research investment for application in hydrogen production, CO₂ conversion, and biomass processing as the chemical industry evaluates low-carbon process routes.

-

Supply concentration risk is increasing attention to zircon mineral sand reserve development outside Australia and South Africa, with projects in Mozambique, Madagascar, and Senegal advancing toward production.

-

Yttria-stabilized zirconia is expanding in solid oxide fuel cell electrolyte applications as fuel cell deployment for stationary power and transportation grows beyond demonstration scale.

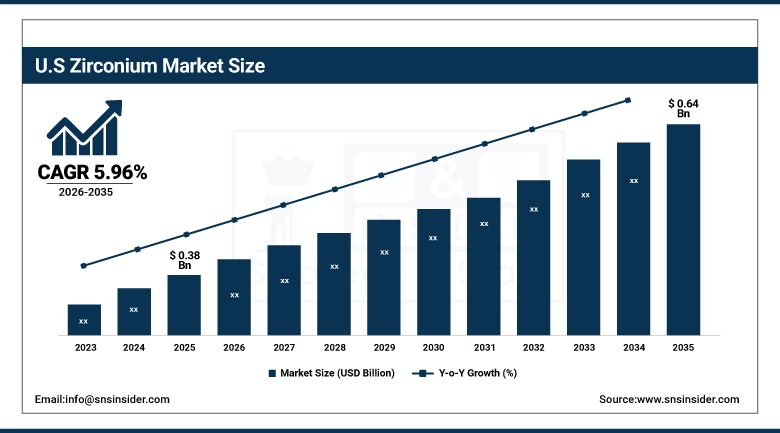

The U.S. Zirconium Market was valued at USD 0.38 Billion in 2025 and is projected to reach USD 0.64 Billion by 2035, growing at a CAGR of 5.96% during 2026–2035. The United States does not host major zircon mining operations but is a substantial consumer of zirconium derivatives across nuclear, chemical processing, and advanced ceramics applications. The US nuclear energy sector’s demand for zirconium alloy cladding tubes consumed at every reactor fuel reload cycle provides a stable, long-cycle demand base.

'

'

Zirconium Market Growth Drivers:

-

Ceramic Tile and Sanitaryware Production Growth Across Asia Pacific and the Middle East Sustains the Largest Volume Demand Category for Zircon-Derived Opacifiers and Zirconium Silicate

Ceramics account for 52.38% of zirconium application demand in 2025. Construction activity across Asia Pacific, particularly in China, India, Vietnam, and Indonesia, sustains zircon flour and opacifier consumption that underpins the majority of global zircon demand by volume. Zirconium silicate is the primary opacifier in ceramic glaze formulation for wall tiles, sanitaryware, and tableware. Urbanization and rising housing standards create a demand floor that grows with population and income levels across the region.

Zirconium Market Restraints:

-

Zircon Mineral Sand Supply Is Geographically Concentrated in Australia and South Africa, Creating Single-Point Procurement Risk for Downstream Processors and End-Users Who Have Limited Alternative Source Access Within Short Contracting Timelines

Australia and South Africa account for the dominant share of global zircon mineral sand production. Iluka Resources and Tronox are the largest producers, and their combined output decisions directly influence global pricing. Downstream processors producing zircon flour, zirconia, and chemical derivatives have limited ability to substitute alternative mineral sources at short notice because feed quality specifications are calibrated to specific ore characteristics. Geographic concentration creates procurement risk that becomes commercially significant during mining disruptions or extended shipping constraint periods.

Zirconium Market Opportunities:

-

Advanced Zirconia Applications in Medical Devices, Solid Oxide Fuel Cells, and Thermal Barrier Coatings for Aerospace Turbines Represent High-Value Growth Segments Where Zirconia Demand Growth Outpaces Bulk Ceramics Volume Growth in Revenue Terms

Yttria-stabilized zirconia and ceria-stabilized zirconia serve advanced materials applications where mechanical strength, ionic conductivity, and thermal insulation combine in ways no alternative material replicates. In dental restoration, zirconia full-contour crowns and bridges have replaced metal-ceramic systems in many clinical applications due to superior aesthetics and reduced chipping risk. In solid oxide fuel cells, zirconia electrolyte membranes enable high-efficiency electrochemical conversion at temperatures where proton exchange membrane alternatives cannot function. In aerospace, thermal barrier coatings on turbine blades permit higher inlet temperatures, improving fuel efficiency in commercial aviation and power generation turbines.

Zirconium Market Segment Analysis:

By Product Type: Zircon Sand Leads While Zirconia (ZrO₂) Drives the Fastest Growth Through 2035

Zircon Sand dominated with a 31.42% share in 2025, valued at approximately USD 0.68 Billion, while Zirconia (ZrO₂) is expected to grow at the fastest CAGR of approximately 8.44% through 2035.

Zircon sand holds the leading share as the primary commercial form in which zirconium enters the processing supply chain, with its price setting the floor for all downstream product categories. Zirconia is growing fastest as advanced ceramic, fuel cell, dental, and thermal coating applications create demand for high-purity grades at values well above commodity zircon, shifting revenue toward converted product categories. Zirconium metal and alloys carry the highest unit values and grow steadily on nuclear demand.

By Application: Ceramics Lead While Nuclear Applications Drive the Fastest Growth Through 2035

Ceramics dominated with a 52.38% share in 2025, valued at approximately USD 1.13 Billion, while Nuclear Applications are expected to grow at the fastest CAGR of approximately 10.26% through 2035.

Ceramics hold the dominant application share because tile and sanitaryware sectors consume zirconium silicate opacifiers at volumes no other application category approaches. Nuclear applications are growing fastest because new reactor construction in China, India, and other markets creates step-change demand for zirconium alloy cladding, and the technically restricted, geopolitically sensitive nature of nuclear-grade supply creates procurement urgency among reactor operators.

By End-Use Industry: Construction & Building Materials Lead While Energy & Nuclear Power Registers Among the Fastest CAGRs Through 2035

Construction & Building Materials dominated with a 46.27% share in 2025, valued at approximately USD 1.00 Billion, while Energy & Nuclear Power is expected to grow at a CAGR of approximately 8.32% through 2035.

Construction and building materials hold the leading end-use share because ceramic tile and sanitaryware, both tied to construction output, are the primary commercial volume pathways for zircon. Asia Pacific’s urbanization and residential building programs drive the majority of this segment’s demand. Energy and nuclear power is growing rapidly as reactor construction programs in multiple countries create decade-scale cladding procurement commitments, and policy interest in nuclear as low-carbon baseload power extends the demand outlook.

By Form / Processing Stage: Natural Zircon (Mineral Sand) Leads While Chemical Derivatives Register Fastest CAGR Through 2035

Natural Zircon (Mineral Sand) dominated with a 34.16% share in 2025, valued at approximately USD 0.74 Billion, while Chemical Derivatives are expected to grow at the fastest CAGR of approximately 8.15% through 2035.

Natural zircon mineral sand holds the leading form share as the input stage for all downstream product forms, though its share is declining as processed forms grow faster. Chemical derivatives are growing fastest because zirconium surface treatment chemicals, catalysts, and specialty coatings serve industrial and advanced materials markets where demand is driven by processing requirements rather than construction cycles, providing exposure to higher-growth end segments.

Zirconium Market Regional Analysis:

Asia Pacific Zirconium Market Insights

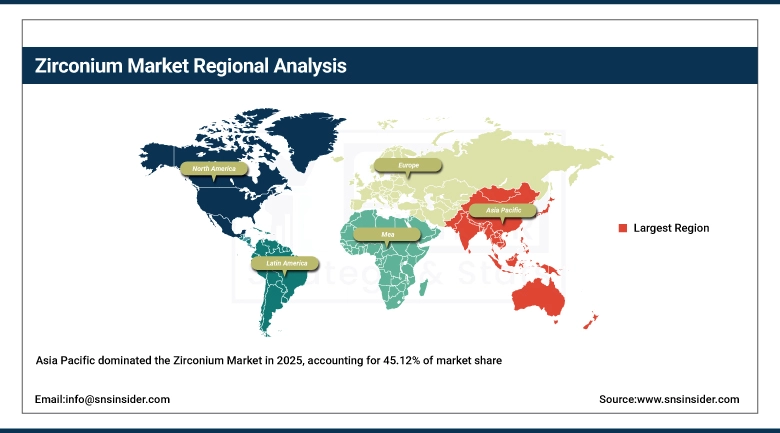

Asia Pacific dominated the Zirconium Market in 2025, accounting for 45.12% of market share, valued at USD 0.97 Billion, and reaching USD 2.02 Billion by 2035. China is the dominant national market and the world’s largest consumer of zircon across all product forms, driven by its ceramic tile manufacturing industry the largest globally by output volume its expanding nuclear reactor construction program, and its growing advanced ceramics manufacturing sector serving domestic and export markets. India and Southeast Asian markets are secondary growth contributors as their tile production capacity and construction-linked ceramic consumption expand with urbanization.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Zirconium Market Insights

North America accounted for 22.36% of the Zirconium Market in 2025, valued at USD 0.48 Billion, and is projected to reach USD 0.84 Billion by 2035 at a CAGR of 5.72% during the forecast period.

North America’s zirconium demand is concentrated in nuclear, chemical processing, and advanced ceramics rather than bulk tile ceramics. The US nuclear fleet requires regular zirconium alloy cladding procurement on 18-to-24-month reload cycles. Chemical industry consumption of zirconium catalysts and surface treatment agents provides a steady industrial demand base, while aerospace and defense consume zirconium thermal barrier coatings at unit values substantially above commercial ceramic grades.

U.S. Zirconium Market Insights

The United States accounts for 78.64% of North American demand in 2025. The U.S. Zirconium Market was valued at USD 0.38 Billion in 2025 and is projected to reach USD 0.64 Billion by 2035, growing at a CAGR of 5.39% during 2026–2035. The US is a net importer of zircon mineral sand, sourcing primarily from Australia and South Africa, and a net producer of higher-value zirconium derivatives including nuclear-grade zirconium metal processed at domestic facilities serving the domestic reactor operator market.

Europe Zirconium Market Insights

Europe held a 27.84% share of the Zirconium Market in 2025, valued at USD 0.60 Billion, and is expected to reach USD 1.06 Billion by 2035 at a CAGR of 5.93% during the forecast period. European demand is supported by an established ceramic tile manufacturing sector in Spain, Italy, and Poland, a significant refractories industry serving steelmakers, and nuclear power generation across France, the Czech Republic, Finland, and the United Kingdom that creates consistent zirconium alloy procurement demand. Spain and Italy are the two largest ceramic producing nations in Europe and together represent the primary route through which European zircon consumption flows into the global demand balance.

Germany Zirconium Market Insights

Germany leads the European zirconium market in advanced applications through specialty ceramics manufacturing, refractories demand from steelmaking, and chemical industry consumption of zirconium-based catalysts. German producers supply advanced zirconia components to automotive and medical sectors, while BASF and Evonik use zirconium compounds in catalyst formulations, differentiating German demand from the construction-driven ceramics volumes that characterize Southern European markets.

China Zirconium Market Insights

China is the dominant national market within Asia Pacific, consuming the largest share of globally traded zircon through ceramic tile and sanitaryware production serving both domestic construction and export markets. China’s nuclear reactor construction pipeline is the second major demand driver, with cladding procurement volumes placing upward pressure on nuclear-grade zirconium supply and driving domestic zirconium metal processing investment.

Latin America and Middle East & Africa Zirconium Market Insights

Latin America held approximately 2.41% of the global Zirconium Market in 2025, valued at USD 0.05 Billion, and is expected to reach USD 0.12 Billion by 2035 at a CAGR of 8.53% during the forecast period. Brazil is the primary market, supported by ceramic tile manufacturing in São Paulo and Santa Catarina states that positions Brazil as one of the world’s largest tile producers, and by refractories demand from steelmaking operations. Middle East & Africa held approximately 2.27% of market share in 2025, valued at USD 0.05 Billion, and is expected to reach USD 0.11 Billion by 2035 at a CAGR of 8.31% during the forecast period. South Africa’s position as a major zircon mineral sand producer gives its domestic industry access to raw material at advantageous economics, while Gulf state construction programs drive ceramic tile consumption in countries that are net importers of finished ceramic products and the zircon opacifiers used in their production.

Competitive Landscape for Zirconium Market:

Iluka Resources Limited

Iluka Resources is among the world’s largest producers of zircon mineral sand, with operations in Western Australia and South Australia underpinning long-term supply agreements with ceramic, chemical, and refractory customers across Europe and Asia. The company has developed a rare earth refinery processing elements recovered as by-products of mineral sand operations, representing diversification into the broader critical minerals supply chain.

In March 2025, Iluka Resources updated its mineral sand production guidance for the Eneabba and Jacinth-Ambrosia operations, confirming sustained zircon output targets through 2027 and signaling commitment to long-term supply agreements with European ceramic producers requiring supply security documentation for regulatory compliance purposes.

Tronox Holdings plc

Tronox operates an integrated mineral sands business spanning zircon and titanium mining in Australia, South Africa, and the United States, alongside titanium dioxide pigment production. Its zircon output positions it among the largest global suppliers, with access to multiple deposit types across geographies that provide procurement diversification for major ceramic and chemical customers.

In January 2025, Tronox announced operational efficiency improvements at its KwaZulu-Natal mineral sands operations in South Africa, including upgraded mineral separation plant equipment that increased zircon concentrate recovery rates and reduced processing costs, supporting the company’s cost position in a market where zircon pricing is influenced by spot and contract benchmark negotiations with major ceramic producers.

Zirconium Market Key Players:

-

Iluka Resources Limited

-

Tronox Holdings plc

-

Kenmare Resources plc

-

Eramet

-

Base Resources Limited

-

Alkane Resources Ltd

-

Doral Mineral Sands Pty Ltd

-

Lanka Mineral Sands Ltd

-

V.V. Mineral

-

Southern Ionics Minerals LLC

-

Saint-Gobain ZirPro

-

ATI Inc.

-

Western Zirconium (Westinghouse)

-

BaoTi Group

-

Luxfer MEL Technologies

-

Zirconium Chemicals Ltd

-

American Elements

-

Imerys

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.16 Billion |

| Market Size by 2035 | USD 4.15 Billion |

| CAGR | CAGR of 6.82% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Zircon Sand, Zircon Flour / Powder, Zirconia (ZrO₂), Zirconium Metal & Alloys, and Zirconium Chemicals) • By Application (Ceramics (Tiles, Sanitaryware, Advanced Ceramics), Foundry & Casting, Refractories, Zirconium Chemicals & Catalysts, and Nuclear Applications), • By End-Use Industry (Construction & Building Materials, Automotive & Aerospace, Chemical & Petrochemical, Energy & Nuclear Power, and Electronics & Healthcare), • By Form / Processing Stage (Natural Zircon (Mineral Sand), Processed Zircon (Flour, Opacifiers), Fused Zirconia, and Chemical Derivatives |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Iluka Resources Limited, Tronox Holdings plc, Rio Tinto Group, Kenmare Resources plc, Eramet, Base Resources Limited, Alkane Resources Ltd, Doral Mineral Sands Pty Ltd, Lanka Mineral Sands Ltd, V.V. Mineral, Southern Ionics Minerals LLC, Saint-Gobain ZirPro, Tosoh Corporation, ATI Inc., Western Zirconium (Westinghouse), BaoTi Group, Luxfer MEL Technologies, Zirconium Chemicals Ltd, American Elements, Imerys |

Frequently Asked Questions

Zircon Sand dominated the Zirconium Market with a 31.42% share in 2025.

Asia Pacific dominated the Zirconium Market in 2025.

Ceramic tile production growth across Asia Pacific driving zircon opacifier demand, nuclear power capacity additions expanding zirconium alloy cladding requirements, and advanced zirconia adoption in medical and energy applications are the primary drivers of market growth.

The Zirconium Market size was USD 2.16 Billion in 2025 and is expected to reach USD 4.15 Billion by 2035.

The Zirconium Market is expected to grow at a CAGR of 6.82% from 2026–2035.

Get in Touch