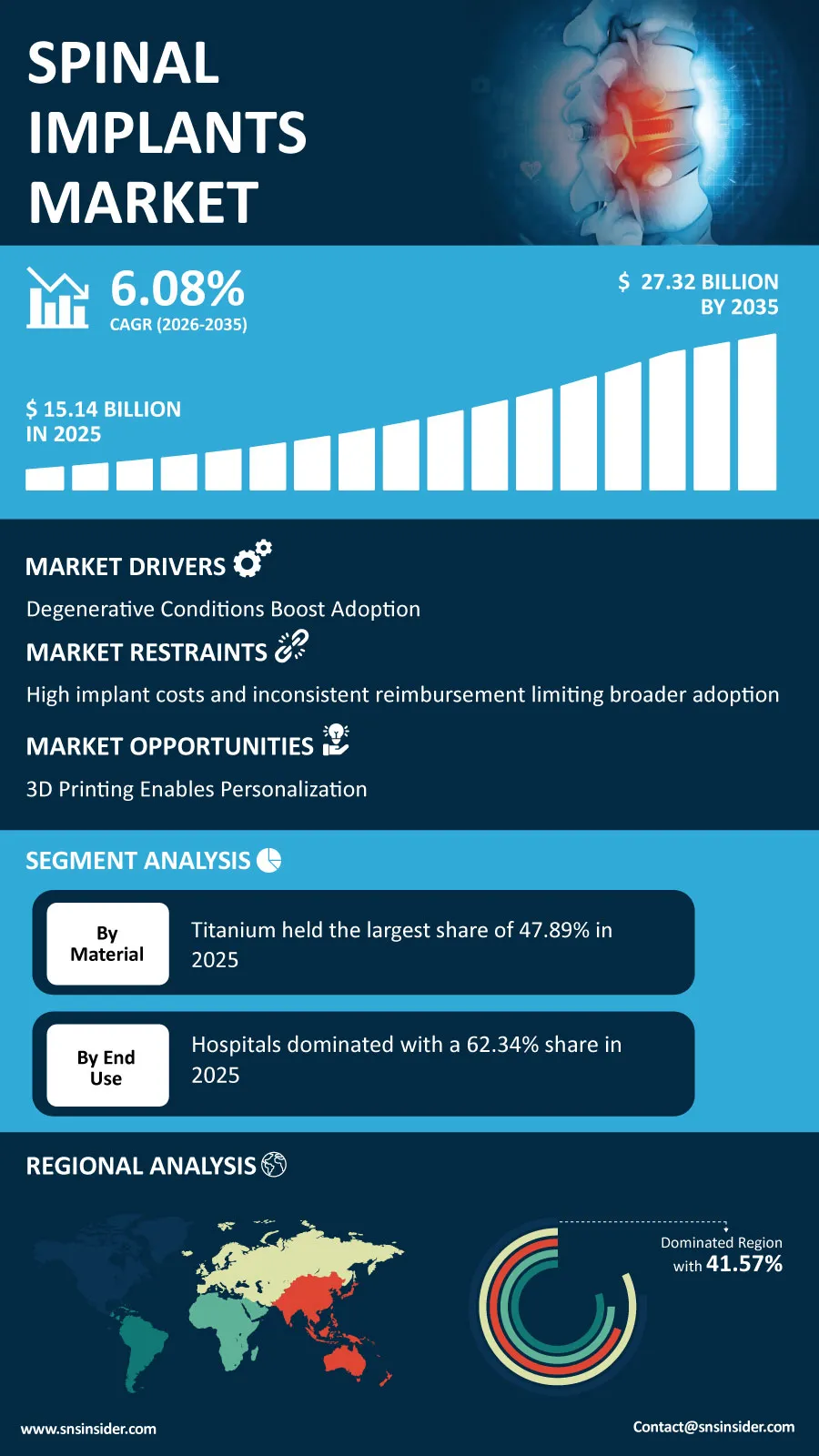

The global Spinal Implants Market is witnessing sustained expansion as healthcare providers increase their focus on advanced spine care solutions to address the growing burden of musculoskeletal disorders. "According to a recent study by SNS Insider, the global Spinal Implants Market size valued at USD 15.14 billion in 2025, is anticipated to grow to USD 27.32 billion by 2035, registering a CAGR of 6.08% over the 2026–2035 forecast period."

The increasing demand for surgery among patients with spinal disorders is driving healthcare organizations and the medical devices industry to incorporate technologies that enhance clinical results and reduce recovery time. With more investment being made into the construction of advanced orthopedic facilities by healthcare providers, it is essential that innovations in spinal implants continue to play an increasingly critical role in treating spinal disorders.

To Get Detailed Insights on the Spinal Implants Market – Request a Sample Report

Advanced Surgical Technologies Reshape Spine Care

There have been some remarkable changes in the field of spinal surgeries that can benefit the entire healthcare industry. More often, the doctors rely on navigation technology and robotics to perform precise operations with minimal risks. As a result, there have been increased applications of implants in the field of routine and complicated spinal surgeries.

In addition to that, there have been the development of implants with advanced biomechanical features that help doctors to provide their patients with customized solutions. Innovations in biomaterials and implant design continue supporting faster healing, enhanced stability, and improved long-term patient outcomes.

Key Market Findings Highlight Strong Growth Opportunities

Fusion devices remained the leading product category, accounting for 38.46% of market revenue in 2025 due to their widespread use in treating degenerative spinal disorders. Artificial discs are projected to register the fastest expansion through 2035 with a 7.24% CAGR, reflecting increasing preference for motion-preserving procedures.

Among device types, lumbar implants represented the largest revenue share at 41.18% in 2025, supported by the high prevalence of lower back disorders. Cervical implants are expected to deliver the fastest growth, advancing at a 7.12% CAGR during the forecast period.

Open surgery continued to account for the largest procedural share with 55.23% of market revenue in 2025. However, minimally invasive spine surgery is gaining momentum and is forecast to expand at a 7.03% CAGR as healthcare providers prioritize shorter hospital stays and quicker patient recovery.

Titanium remained the preferred implant material with a 47.89% market share owing to its strength, durability, and biocompatibility. Meanwhile, PEEK-based implants are expected to witness the fastest growth at a 7.18% CAGR as demand increases for lightweight materials that support improved post-operative imaging.

Hospitals generated 62.34% of total market revenue in 2025, reflecting their leadership in performing complex spinal procedures. Ambulatory Surgical Centers are projected to experience the fastest growth, driven by the expanding adoption of outpatient minimally invasive spine surgeries.

Innovation and Personalized Treatment Continue Driving Market Evolution

Customization of treatments is becoming popular among health care professionals, as they aim at increasing patient satisfaction and efficiency in surgery. With the advancement in printing 3D implants, surgeons can use implants that are custom made for each individual’s anatomy.

The use of artificial intelligence technology is also becoming an essential element in spine surgeries, improving preoperative planning and intraoperative navigation. Through the integration of artificial intelligence with robots and imaging devices, surgeons can now perform more complicated surgeries with increased precision.

Growing research into next-generation biomaterials further supports the industry's transition toward implants that offer improved durability, reduced complications, and enhanced patient comfort throughout recovery.

Regional Markets Maintain Positive Growth Momentum

North America continued to be the largest regional market in 2025, accounting for 41.57% of revenues globally. The presence of strong healthcare infrastructure, high adoption rates of latest technologies in surgery and continuous investments in innovation are sustaining the regional dominance. North America has been the dominant market due to the presence of various spine treatment centers across the region in the U.S.

The fastest growth rate is projected for Asia Pacific driven by health reforms in emerging nations, such as China, India, Japan, and others due to increase in spending on healthcare, rising penetration of specialized orthopedics services and aging populations.

Europe has maintained stable demand for spine implants due to the presence of highly developed healthcare infrastructures and growing awareness about minimal spinal surgery procedures, whereas the regions of Latin America and the Middle East are slowly gaining expertise in treating spinal disorders.

Leading Companies Strengthen Competitive Landscape

The spinal implants industry continues to experience strong competition as manufacturers invest in product innovation, digital surgical technologies, and strategic collaborations to strengthen their global presence.

Some of the leading companies operating in the global spinal implants market include Medtronic, Johnson & Johnson (DePuy Synthes), Stryker, NuVasive, Globus Medical, Zimmer Biomet, Alphatec Spine, Orthofix International, B. Braun Melsungen AG, RTI Surgical, SeaSpine Holdings Corporation, Ulrich GmbH & Co. KG, Spineart, Aesculap Implant Systems, VB Spine LLC, Centinel Spine LLC, K2M Group Holdings, Amedica (CTL Amedica), Xtant Medical Holdings, and SpineGuard.

An SNS Insider analyst Parry Kardani commented, "Growing demand for precision spine care, combined with rapid innovation in implant materials, minimally invasive procedures, and digital surgical technologies, is transforming the spinal implants market. Companies investing in patient-specific solutions and next-generation surgical platforms are expected to strengthen their competitive position as global demand for advanced spinal treatment continues to expand."

About the Author

Get in touch