Spinal Implants Market Report Scope & Overview:

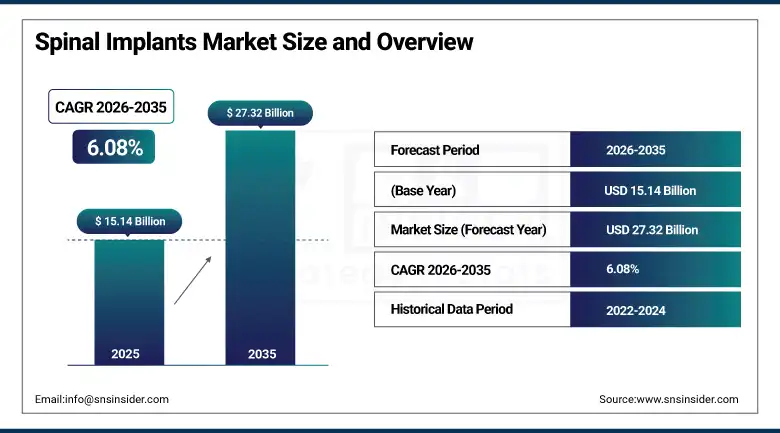

The Spinal Implants Market size was USD 15.14 Billion in 2025 and is expected to reach USD 27.32 Billion by 2035, growing at a CAGR of 6.08% from 2026–2035.

The Spinal Implants Market is growing steadily owing to the rising incidence of spinal problems, degenerative disc disorders, scoliosis, and spinal injuries. An aging population that is at high risk of suffering from spinal issues is expected to fuel the uptake of spinal fusion and motion preservation devices. Advanced technologies being introduced in the field of spine surgery, including 3D-printed implants, minimally invasive spine surgery, and biologics, contribute toward improved surgical success and recovery. Furthermore, growing healthcare spending, increased usage of advanced surgical methods, and expanding spine care services will positively impact market growth.

According to the World Health Organization (WHO), low back pain affects approximately 619 million people globally and is the leading cause of disability worldwide. The organization projects that the number of affected individuals will increase to around 843 million by 2050, highlighting the growing need for spinal treatment and intervention solutions. Furthermore, the United Nations Department of Economic and Social Affairs (UN DESA) estimates that the global population aged 65 years and older will rise from 857 million in 2021 to nearly 1.6 billion by 2050, significantly increasing the prevalence of age-related degenerative spinal disorders.

Spinal Implants Market Size and Forecast

-

Market Size in 2026E: USD 16.06 Billion

-

Market Size by 2035: USD 27.32 Billion

-

CAGR: 6.08% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Spinal Implants Market - Request Free Sample Report

Spinal Implants Market Trends

-

Minimally invasive and robotic spine surgeries are driving demand for next-generation implant systems.

-

Titanium and PEEK biomaterials are improving implant strength, fusion rates, and patient recovery times.

-

3D-printed, anatomically customized implants are gaining wider clinical acceptance among spine surgeons.

-

AI-based surgical planning and navigation tools are improving procedural precision and patient outcomes.

-

Motion-preservation devices like artificial discs are gaining ground over traditional fusion procedures.

The U.S. Spinal Implants Market Outlook

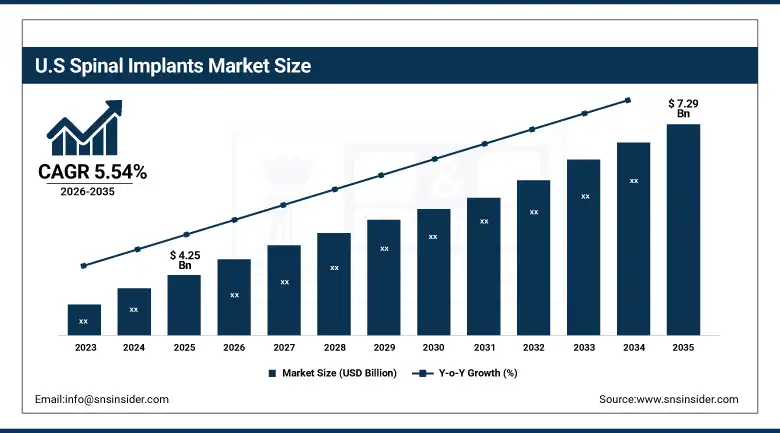

The U.S. Spinal Implants Market was valued at approximately USD 4.25 Billion in 2025. It is expected to reach approximately USD 7.29 Billion by 2035. The market is growing at a CAGR of approximately 5.54%.

Rising degenerative spine disorder cases keep driving steady U.S. market growth nationwide. Growing use of minimally invasive and motion-preserving implants is accelerating this trend further. Strong focus on 3D-printed, patient-specific implants keeps the U.S. at the innovation forefront. Robust R&D investment from major device makers reinforces this leadership position consistently. Motion-preserving devices and minimally invasive technologies continue gaining ground among American spine surgeons.

According to the Centers for Disease Control and Prevention (CDC), approximately 39% of U.S. adults experience back pain, making it one of the most common health conditions in the country and a significant contributor to demand for spinal treatments and implantable devices.

Spinal Implants Market Segment Analysis

-

By Product Type, Fusion Devices held the largest market share of 38.46% in 2025, while Artificial Discs are expected to grow at the fastest CAGR of 7.24% during 2026–2035.

-

By Device Type, Lumbar dominated with a 41.18% share in 2025, while Cervical is anticipated to record the fastest CAGR of 7.12% through 2026–2035.

-

By Surgery Type, Open Surgery accounted for the largest share of 55.23% in 2025, while Minimally Invasive Surgery is forecasted to register the fastest CAGR of 7.03% during 2026–2035.

-

By Material, Titanium held the largest share of 47.89% in 2025, while PEEK is expected to grow at the fastest CAGR of 7.18% during 2026–2035.

-

By End User, Hospitals dominated with a 62.34% share in 2025, while Ambulatory Surgical Centers are anticipated to record the fastest CAGR of 7.05% through 2026–2035.

By Product Type, fusion devices segment dominates the market, while artificial discs segment is the fastest-growing segment

The Fusion Devices segment dominated the market in 2025 owing to its widespread adoption for the treatment of degenerative disc disease, spinal instability, spine deformities, and traumatic conditions. These products provide long-lasting stability of the spine and have a long clinical track record that makes them popular among surgeons. With growing numbers of spinal fusion procedures driven by factors such as aging of the population and increased incidence of spinal diseases, demand has surged even more.

The Artificial Discs segment is the fastest growing due to the high demand for motion-preserving solutions as compared to conventional spinal fusions. The artificial discs allow maintenance of motion and decrease stress on other vertebrae. Improvements in implants themselves as well as surgical techniques have helped achieve positive results. Increasing patient and physician awareness of the advantages of motion-preserving surgery is driving the segment ahead.

By Device Type, lumbar segment dominates the market, while cervical segment is the fastest-growing segment

The Lumbar segment dominated the market in 2025 due to the higher prevalence rate of various conditions such as degenerative disc diseases, spinal stenosis, and herniated discs. The lumbar spine suffers from high mechanical stress; hence, it is more prone to age-related problems. The higher demand for surgeries related to lumbar spine fusion and stability, coupled with increased expenditure by healthcare facilities in spinal care, has boosted the demand. Additionally, technological advances in lumbar implants help sustain the dominance of the segment.

The Cervical segment is the fastest growing due to the rising diagnoses and treatment of cervical spine disorders resulting from aging, sedentary lifestyle, and improper posture among other reasons. Improvements in treatment techniques through the development of advanced cervical implants have helped increase the success rate of treatment. Increased awareness about the importance of treating cervical spine ailments and increased inclination toward minimally invasive surgeries have propelled the growth of the segment.

By Surgery Type, open surgery segment dominates the market, while minimally invasive surgery segment is the fastest-growing segment

The Open Surgery segment dominated the market in 2025, owing to its use in treating complex spine-related conditions that require substantial visualization and surgical access. These procedures include those conducted on cases with complicated spinal deformities, multi-level spinal diseases, and challenging revision surgeries. Due to the high demand for open surgery procedures owing to the number of complex spinal surgeries done around the world, the segment retained its dominance.

The Minimally Invasive Surgery segment is the fastest growing due to the rising need for less invasive surgical methods that minimize tissue trauma, blood loss, post-surgery pain, and the duration of hospital stays. With advancements in imaging devices, navigation technologies, and surgical instruments, these procedures have become even more accurate and effective. Faster recovery and rehabilitation times have contributed to the preference for such surgical approaches.

By Material, titanium segment dominates the market, while PEEK segment is the fastest-growing segment

The Titanium segment dominated the market in 2025 because of its outstanding mechanical properties. First of all, titanium is strong, durable, and resistant to corrosion; additionally, titanium is characterized by good biocompatibility. The usage of titanium makes the implants structurally sound and effectively interacting with the neighboring bone tissue. Besides, titanium is widely used successfully in spinal surgery for decades, which means that this product is highly trusted by surgeons because of its excellent performance.

The PEEK segment is the fastest growing due to mechanical attributes and compatibility with new-generation spinal implants. The PEEK material possesses similar elastic qualities to those of the bone, which reduces stress shielding and helps distribute load better. The radiolucent property of the material allows better imaging after surgery and assessing the process of fusion. The rising demand for improved surgical materials is driving the market forward.

By End User, hospitals segment dominates the market, while ambulatory surgical centers segment is the fastest-growing segment

The Hospitals segment dominated the market in 2025 owing to their capability of undertaking intricate spinal surgeries through a surgical infrastructure that can undertake the same. Hospitals conduct numerous spinal surgeries especially complicated and risky ones with the help of a medical team and postoperative care. Availability of diagnostic equipment and reimbursement further contribute to the segment’s dominance. Spinal surgeries in patients are increasing, which reinforces the segment's dominance in the market.

The Ambulatory Surgical Centers segment is the fastest growing due to the increasing number of individuals opting for cost-efficient and effective surgical treatment. This segment provides quick surgical processes, reduced expenses associated with hospital stays, and improved recovery periods when compared to traditional surgical procedures. Improvements in minimally invasive spinal surgery methods facilitate these surgeries to be carried out in ambulatory centers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Spinal Implants Market Insights

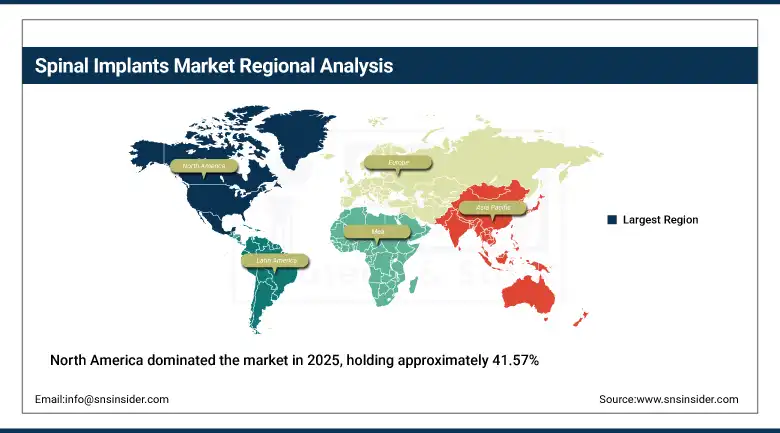

North America dominated the market in 2025, holding approximately 41.57% of revenue. Strong healthcare infrastructure and rising degenerative spine disorder cases both support this lead. High adoption of new surgical procedures keeps reinforcing the region’s leadership position further. Well-defined reimbursement policies and strong R&D capabilities both add to this advantage.

The United States accounts for approximately 82.5% of North American revenue. Surgeons here show high awareness of minimally invasive and motion-preserving technologies. Strong innovation, product adoption, and commercialization capability keep this region firmly in the lead.

The U.S. Census Bureau estimates that the population aged 65 years and older will exceed 80 million by 2040, increasing the incidence of degenerative spinal conditions that often require spinal fusion and stabilization procedures. Furthermore, the National Institutes of Health (NIH) reports that more than 1.6 million spinal procedures are performed annually in the United States, including spinal fusion, decompression, and motion-preservation surgeries.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Spinal Implants Market Insights

Europe has seen steady growth from rising degenerative spine condition cases nationwide. Increasing attention toward minimally invasive and motion-preserving procedures keeps driving regional growth. Germany, the UK, France, and Italy all contribute strong healthcare infrastructure regionally.

Germany accounts for approximately 24.6% of European revenue. Advanced healthcare systems and high surgical performance both support this leading regional position. Strict regulatory standards keep pushing adoption toward patient-specific, evidence-based implant solutions.

According to Eurostat, approximately 21% of the European Union population is aged 65 years or older, representing one of the highest proportions globally. This demographic trend is contributing to a rising incidence of degenerative spinal conditions, osteoporosis-related vertebral fractures, and other age-associated spine disorders that require surgical intervention.

Additionally, the European Commission Health Directorate reports increasing healthcare investments focused on musculoskeletal disorders, rehabilitation programs, and healthy aging initiatives, supporting broader access to advanced spinal care and implant technologies.

Asia Pacific Spinal Implants Market Insights

Asia Pacific is the fastest-growing market for spinal implants, expanding at a CAGR of 7.16%. Rising degenerative spine disease cases and an aging population both drive this growth. China, India, Japan, and South Korea are all expanding minimally invasive procedure adoption.

According to the World Health Organization (WHO) Western Pacific Region, Asia accounts for a substantial share of the global elderly population, contributing to an increasing incidence of degenerative spinal diseases and age-related orthopedic conditions.

Furthermore, the India Ministry of Health and Family Welfare highlights the growing burden of musculoskeletal and orthopedic disorders driven by population aging, sedentary lifestyles, and changing demographics.

Japan, one of the world’s oldest societies, has approximately 29% of its population aged 65 years and older, according to the Statistics Bureau of Japan, further supporting demand for spinal fusion devices, motion-preservation implants, and minimally invasive spine surgeries.

China accounts for approximately 40.6% of Asia Pacific revenue. Significant investment in next-generation biomaterials and hospital infrastructure keeps fueling regional expansion. This regional growth should keep outpacing the global average through the forecast period.

Additionally, China’s National Health Commission reports that the population aged 60 years and above exceeds 310 million people, creating strong demand for spinal treatments, surgical procedures, and implantable devices.

MEA & Latin America Spinal Implants Market Insights

The UAE leads MEA revenue at approximately 22.8%. Expanding healthcare infrastructure and rising awareness of advanced surgical treatments both support this position. Saudi Arabia and South Africa are also investing in modern hospital capacity.

Brazil leads Latin American revenue at approximately 43.8%. Growing healthcare spending and rising adoption of modern spine care both drive this lead. Argentina and Mexico contribute secondary demand through their own expanding healthcare systems.

Market Dynamics

Growth Drivers: Rising burden of degenerative spine disorders accelerating demand for advanced implant solutions

An increase in degenerative spine disorders is a key growth factor in this market. Spondylosis, disc degeneration, and stenosis have been on the rise due to aging of the global population. Lifestyle habits that affect health adversely are another factor behind an increase in cases of spinal diseases. These trends are creating demand for more complicated surgeries and sophisticated implants. The role of spinal implants involves structural support and helping in achieving successful recoveries after surgery. Spinal implant procedures increased by 6.8% in 2025 alone.

These new demands are shaping the practices of surgeons in dealing with the spine as well. Surgeons are increasingly adopting advanced implants and surgical techniques that offer less invasive treatment options. Motion preservation systems are becoming popular in addition to conventional fusions. With the increasing aging populations in many regions of the world, there will be sustained demand in this regard. There is great potential in manufacturing spinal implants based on new technology. Hospital purchasing departments are favoring implants with good clinical records.

Restraints: High implant costs and inconsistent reimbursement limiting broader adoption

The high price of implants serves as a significant hindrance to wider market penetration in many other areas. Besides, complicated approval processes contribute to increased time and cost of implementation. High standards for classifications and safety testing significantly delay the introduction to the market. Compliance leads to an increase in costs which ultimately translates into higher expenses for the patient or the payer.

Coverage programs are usually inconsistent in most areas, thereby hindering market penetration. Patients find it difficult to obtain reimbursement because coverage is either inconsistent or does not exist at all. Especially, when it comes to newer technologies, which preserve motion and minimally invasive procedures. This makes it even more challenging for new players in addition to established companies to penetrate markets. Small manufacturers have a hard time obtaining reimbursement due to lack of bargaining power.

Opportunities: Advances in 3D printing, biomaterials, and AI-guided surgery creating new personalized treatment options

Improvements in 3D printing technologies and materials offer promising new growth avenues. Custom-made implants result in better fitting, surgical procedure success, and implant longevity. The next generation of biomaterials is also increasingly biocompatible and effective over time. Both AI-driven planning surgery and robotic navigation procedures offer increased precision and fewer complications.

The combination of these advancements is encouraging surgeons to use personalized spine treatment more widely. Patient-customized and 3D-printed implants made up 22% of all new devices in 2025. Early investment into these technologies could offer a distinct competitive edge for companies involved. With continued growth of personalized medicine in healthcare, these prospects seem likely to keep growing.

Recent Developments:

-

2025: Medtronic launched the CD Horizon ModuLeX Spinal System, adding modular screws and improved 3D visualization for complex spinal deformity procedures.

-

2025: DePuy Synthes expanded its spine portfolio at AAOS 2025, introducing advanced implants and data-driven surgical technologies to support its digital-orthopaedics strategy.

-

2025: Stryker showcased its next-generation Mako SmartRobotics spine platform and completed the sale of its U.S. spinal implants business to VB Spine.

Spinal Implants Market Key Players are:

-

Medtronic

-

Johnson & Johnson (DePuy Synthes)

-

Stryker

-

NuVasive

-

Globus Medical

-

Zimmer Biomet

-

Alphatec Spine

-

Orthofix International

-

B. Braun Melsungen AG

-

RTI Surgical

-

SeaSpine Holdings Corporation

-

Ulrich GmbH & Co. KG

-

Spineart

-

Aesculap Implant Systems

-

VB Spine, LLC

-

Centinel Spine, LLC

-

K2M Group Holdings

-

Amedica (CTL Amedica)

-

Xtant Medical Holdings

-

SpineGuard

Spinal Implants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.14 Billion |

| Market Size by 2035 | USD 27.32 Billion |

| CAGR | CAGR of 6.08% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Fusion Devices, Non-Fusion Devices, Artificial Discs, Bone Graft Substitutes, Spinal Bone Stimulators, Others) • By Device Type (Thoracic, Cervical, Lumbar) • By Surgery Type (Open Surgery, Minimally Invasive Surgery) • By Material (Titanium, Stainless Steel, PEEK, Others) • By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic, Johnson & Johnson (DePuy Synthes), Stryker, NuVasive, Globus Medical, Zimmer Biomet, Alphatec Spine, Orthofix International, B. Braun Melsungen AG, RTI Surgical, SeaSpine Holdings Corporation, Ulrich GmbH & Co. KG, Spineart, Aesculap Implant Systems, VB Spine, LLC, Centinel Spine, LLC, K2M Group Holdings, Amedica (CTL Amedica), Xtant Medical Holdings, SpineGuard |

Frequently Asked Questions

The Spinal Implants Market is expected to grow at a CAGR of 6.08% from 2026 to 2035.

The Spinal Implants Market was valued at USD 15.14 Billion in 2025.

Rising degenerative spine disorder cases, growing minimally invasive surgery adoption, and advances in 3D-printed implants are the primary growth factors.

The Fusion Devices segment dominated the Spinal Implants in 2025. The Artificial Discs segment is growing fastest.

North America dominated the Spinal Implants Market with approximately 41.57% revenue share in 2025. Asia Pacific is the fastest-growing region.

Get in Touch