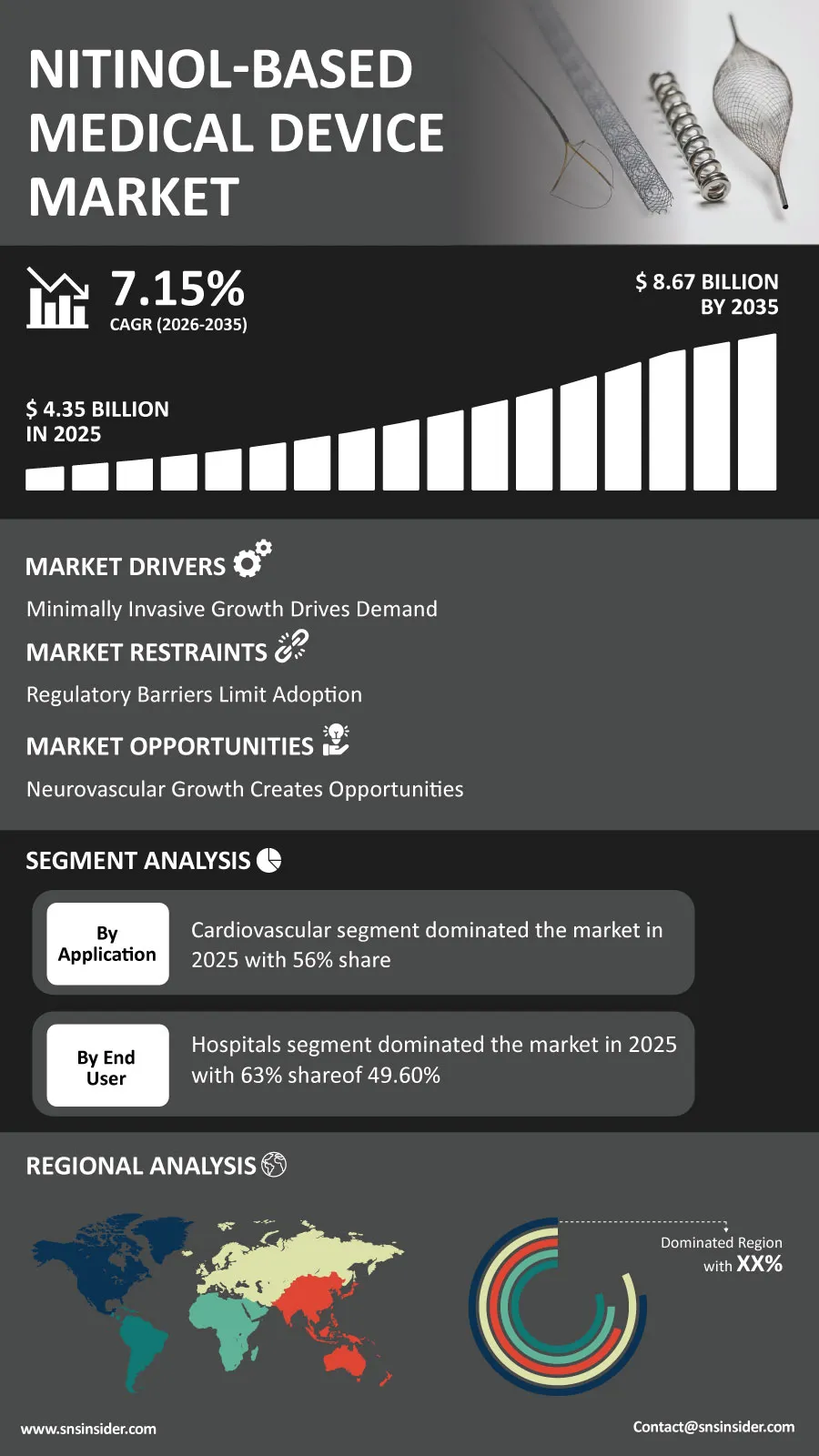

The global Nitinol-Based Medical Device Market is witnessing sustained growth as healthcare providers increasingly adopt advanced interventional technologies that improve procedural precision and patient recovery. “According to a recent study by SNS Insider, the global Nitinol-Based Medical Device Market size valued at USD 4.35 billion in 2025, is anticipated to grow to USD 8.67 billion by 2035, registering a CAGR of 7.15% over the 2026–2035 forecast period.”

Minimally invasive treatment solutions have continued to dominate healthcare systems in both developed and developing countries as a means of reducing hospitalization periods, cutting down on complications, and improving patient results. The remarkable flexibility, strength, and shape-memory properties of nitinol have been the key factors in making this alloy vital in a broad spectrum of medical instruments in procedures related to cardiology, neurology, orthopedics, and urology.

To Get Detailed Insights on the Nitinol-Based Medical Device Market –

Innovation in Interventional Medicine Accelerates Market Growth

The emphasis among medical device manufacturers today is in coming up with devices that will help navigate complicated anatomical structures, while at the same time retaining their structure in challenging clinical procedures. This trend is being driven by the increase in the application of catheter-based interventions, alongside the increasing confidence of physicians in implantable technologies.

The improvements in the products are in keeping with the industry's desire to enhance its clinical performance. For instance, Boston Scientific in 2025 rolled out a more durable nitinol peripheral stent platform, while Medtronic came up with advanced delivery systems that improve procedural accuracy in peripheral interventions.

Key Market Findings Highlight Strong Segment Performance

The stents segment accounted for 41% of market revenue in 2025, supported by rising demand for vascular interventions. Retrieval devices are projected to record the fastest growth throughout the forecast period as stroke treatment and foreign-body retrieval procedures become more common.

By application, cardiovascular devices represented 56% of the global market in 2025 due to the increasing burden of heart and vascular diseases worldwide. Meanwhile, the urology segment is expected to expand at the fastest pace as minimally invasive treatment options gain broader acceptance.

Among end users, hospitals captured 63% of total market revenue in 2025 owing to high procedural volumes and specialized clinical infrastructure. Ambulatory Surgical Centers (ASCs) are anticipated to witness the strongest future growth as outpatient procedures continue to increase globally.

Expanding Clinical Applications Support Future Demand

Further advancements will come with the increased usage of the technology in the fields of cardiovascular treatment, neurovascular interventions, orthopedic surgery, and urology. Increasing number of elderly patients and the growing prevalence of chronic diseases will lead to an increase in the number of procedures, which will prompt the use of more sophisticated tools that provide better results.

Manufacturers are focusing on innovations in terms of materials used in order to increase the level of flexibility, durability, and biocompatibility of their products. These developments are enabling physicians to perform increasingly complex procedures with greater confidence while supporting shorter recovery periods for patients.

Regional Markets Demonstrate Strong Growth Potential

In 2025, North America emerged as the dominant market segment, with around 87.4% contribution from the US towards total regional revenue. Efficient reimbursement policies, good hospital infrastructure, and prevalence of heart-related ailments are among some of the key factors contributing to regional dominance. In 2025, the US market alone was worth USD 1.58 billion and is projected to grow up to around USD 2.70 billion by 2033 at a CAGR of 6.97%.

Asia Pacific is estimated to witness the fastest regional growth at a CAGR of 7.84% till 2035. Japan made up 32.6% of total regional revenue in 2025, whereas increasing health care spending in China, India, South Korea, and other parts of Southeast Asia provides good growth opportunities in advanced interventional devices.

Germany represented 22.3% of Europe's regional revenue in 2025, while Saudi Arabia accounted for 31.2% of Middle East & Africa revenue and Brazil contributed 44.2% of Latin America's market, reflecting continued investment in specialized cardiovascular care across emerging healthcare systems.

Leading Companies Strengthen Competitive Landscape

Competition remains robust as leading manufacturers continue investing in research, product development, and clinical partnerships to expand their portfolios. Major participants operating in the global nitinol-based medical device market include Medtronic, Boston Scientific, Abbott Laboratories, Stryker Corporation, Cardinal Health, Cook Medical, BD (Becton, Dickinson and Company), Terumo Corporation, MicroPort Scientific, Teleflex Incorporated, Merit Medical Systems, Endologix, B. Braun Melsungen AG, W. L. Gore & Associates, Olympus Corporation, Cochlear Limited, Conformis, and Olympus Terumo Biomaterials (OTB).

An SNS Insider analyst Parry Kardani commented, "Growing preference for minimally invasive therapies, combined with continuous advances in device engineering and expanding cardiovascular treatment capacity worldwide, will continue to create significant opportunities for manufacturers developing next-generation nitinol-based medical technologies."

About the Author

Get in touch