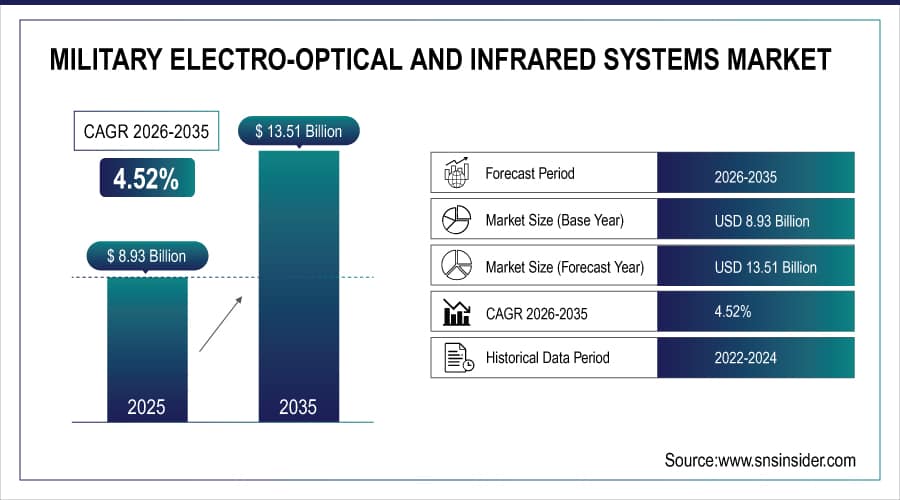

As per the SNS Insider Report titled, Military Electro-Optical and Infrared Systems Market by Platform, by Component, by Technology, by Application, by End User, and Region, Global Forecast 2026–2035, “The global Military Electro-Optical and Infrared Systems Market size was valued at USD 8.93 billion in 2025, is anticipated to grow to USD 13.51 billion by 2035, registering a CAGR of 4.52% during the forecast period 2026–2035.”

Key Takeaways:

-

Airborne platforms accounted for approximately 58% of the market share in 2025, driven by increasing deployment of advanced surveillance, targeting, and reconnaissance systems in military aircraft.

-

Land platforms are projected to witness the fastest growth during 2026–2035 owing to rising investments in border security, armored vehicle modernization, and battlefield awareness capabilities.

-

Sensors & Detectors dominated the component segment with a 34% revenue share in 2025 due to their critical role in threat detection, target acquisition, and intelligence gathering operations.

-

Laser Designators & Illuminators are expected to register the fastest CAGR through 2035 as precision-guided weapon systems continue to gain prominence across modern defense forces.

-

Infrared Systems held the largest technology share of 35% in 2025, supported by widespread adoption for night vision, thermal imaging, and target tracking applications.

-

Hyperspectral Systems are anticipated to emerge as the fastest-growing technology segment during the forecast period due to their enhanced capability to identify concealed objects and improve situational awareness.

-

Surveillance & Reconnaissance represented approximately 33% of total market revenue in 2025, reflecting the growing importance of real-time intelligence and battlefield monitoring.

-

Navigation & Guidance is forecast to expand at the fastest CAGR during 2026–2035 as military forces increasingly adopt advanced precision navigation and targeting solutions.

-

Air Force accounted for nearly 39% of market revenue in 2025 owing to extensive integration of electro-optical and infrared technologies across fighter aircraft, UAVs, and airborne surveillance platforms.

-

Navy is expected to record the fastest growth rate through 2035, driven by increasing deployment of EO/IR systems for maritime surveillance, coastal security, and naval combat operations.

-

North America captured 36.80% of global market revenue in 2025, while Asia Pacific is projected to register the fastest CAGR of approximately 5.87% during the forecast period.

Why Military Electro-Optical and Infrared Systems Market is Growing?

There is steady growth in the Military Electro-Optical & Infrared Systems Market owing to increasing emphasis among various defense entities across the globe on improved situational awareness, enhanced intelligence, and precision targeting.

Modern military applications are dependent on advanced sensor technologies that enable reliable performance in day, night, and adverse climatic conditions. Rising geopolitical tensions, issues with border security, and defense modernization initiatives are boosting investments in state-of-the-art surveillance and reconnaissance systems.

EO/IR systems provide crucial battlefield intelligence and allow the military forces to identify, detect, and track any potential threat accurately. Increasing deployments of UAVs, autonomous military systems, and network centric warfare technologies are adding impetus to the growth of the market.

Further, innovations in the field of sensors technology, thermal imaging techniques, and hyper-spectral imaging systems have been aiding operational effectiveness and widespread use in air, ground, and naval defense applications.

Military Electro-Optical and Infrared Systems Market Statistics

-

Defense budgets across the globe are rising as countries enhance their military readiness and develop sophisticated surveillance and reconnaissance tools.

-

There is an increase in the use of unmanned vehicles carrying EO/IR sensors for surveillance purposes by military forces.

-

Thermal imaging and infrared equipment are becoming indispensable for modern warfare applications, especially during night time missions.

-

Long-range surveillance equipment is being developed by border security agencies around the world for improving surveillance operations.

-

Modernization plans by navies are creating a growing need for advanced marine surveillance and target acquisition systems.

-

There is an increase in the use of precision weapons, which is driving the demand for laser designators and advanced targeting systems.

-

Artificial intelligence and machine learning are becoming integrated into EO/IR technology to enable automated decision-making processes.

Emerging Trends:

In terms of developments within the Military Electro-Optical and Infrared Systems Market, innovations that revolve around better sensor functionality, high-resolution imagery and advanced target recognition features are prevalent. Multi-sensor fusion technologies have been developed by defense companies to incorporate IR, electro-optic, radar, and hyperspectral capabilities to offer comprehensive battlefield awareness.

Image-processing technologies that leverage the power of artificial intelligence are becoming more common and contribute to quick identification of possible threats. This development is important especially when operating in challenging environments, where timely decisions are crucial.

Hyperspectral technologies are experiencing an increase in popularity as they enable the identification of concealed targets, camouflage as well as chemicals. Furthermore, the development of smaller-sized sensors allows their implementation in unmanned vehicles, portable systems, and even next-gen combat vehicles.

There is a rising demand for connected EO/IR systems that facilitate the exchange of real-time intelligence between multiple military units and support a more advanced data-centric approach to military operations.

Top 10 Companies

-

RTX Corporation

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

L3Harris Technologies, Inc.

-

BAE Systems plc

-

Leonardo S.p.A.

-

Thales Group

-

Elbit Systems Ltd.

-

Teledyne FLIR LLC

-

Saab AB

About the Author

Get in touch