Military Electro-Optical and Infrared Systems Market Report Scope & Overview:

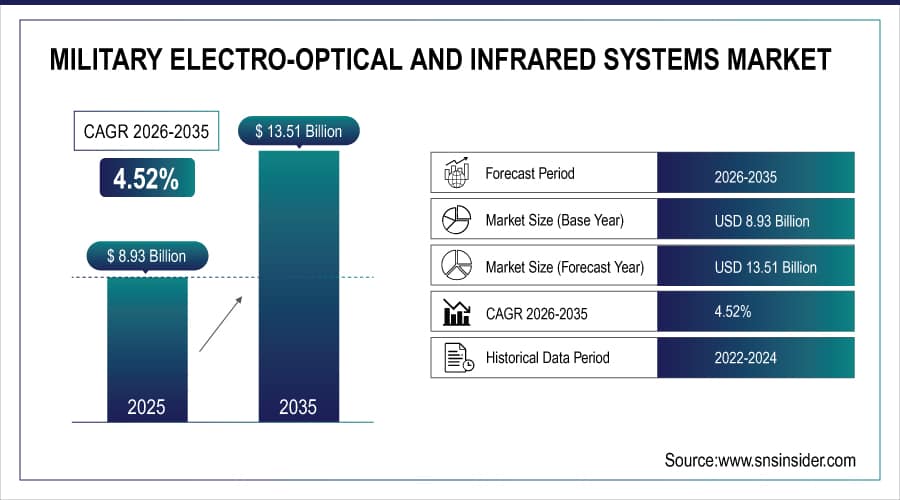

The Military Electro-Optical and Infrared Systems Market is valued at USD 8.93 billion in 2025 and is expected to reach USD 13.51 billion by 2035, growing at a CAGR of 4.52 % from 2026-2035.

Military Electro-Optical and Infrared (EO/IR) Systems Market is growing due to increasing defense modernization programs and rising demand for advanced surveillance, reconnaissance, and targeting capabilities. Armed forces are investing in EO/IR systems to enhance situational awareness, night-vision operations, and precision strike effectiveness across air, land, and naval platforms. Technological advancements in sensors, imaging resolution, and multispectral systems are improving performance and reliability. Additionally, growing geopolitical tensions, increased defense budgets, and the integration of EO/IR systems with unmanned platforms and AI-enabled analytics are further driving market expansion.

Military Electro-Optical and Infrared (EO/IR) Systems Market Size and Forecast

-

Market Size in 2025: USD 8.93 Billion

-

Market Size by 2035: USD 13.51 Billion

-

CAGR: 4.52 % from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Military Electro-Optical and Infrared Systems Market - Request Free Sample Report

Military Electro-Optical and Infrared Systems Market Trends

-

Rising demand for advanced surveillance and targeting systems to enhance situational awareness across modern military operations

-

Increasing investments in EO/IR modernization programs to support intelligence reconnaissance and persistent border security missions

-

Growing integration of AI and sensor fusion technologies to improve target detection identification and tracking accuracy

-

Expansion of unmanned platforms driving demand for lightweight compact EO/IR payloads with enhanced performance

-

Advancements in thermal imaging and multispectral sensors enabling superior performance in low visibility and nighttime conditions

U.S. Military Electro-Optical and Infrared (EO/IR) Systems Market Size Outlook:

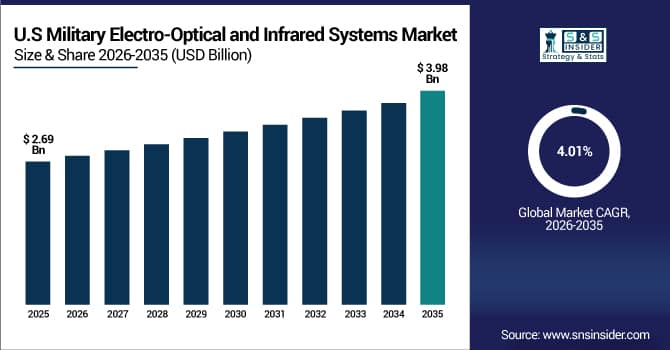

The U.S. Military Electro-Optical and Infrared (EO/IR) Systems Market is valued at USD 2.69 billion in 2025 and is expected to reach USD 3.98 billion by 2035, growing at a CAGR of 4.01 % from 2026-2035. The U.S. EO/IR Systems Market is growing due to rising defense modernization efforts and increasing demand for advanced surveillance, reconnaissance, and targeting capabilities. Investments in high-resolution sensors, night-vision technologies, and AI-enabled systems, along with integration into unmanned platforms, are enhancing operational efficiency and driving steady market growth.

EO/IR Systems Market Growth Drivers:

-

Rising global defense budgets and increasing focus on intelligence, surveillance, and reconnaissance missions are driving strong demand for advanced military EO/IR systems worldwide

Growing geopolitical tensions, border disputes, and asymmetric warfare threats are compelling governments to increase defense spending. A major portion of these budgets is being allocated to intelligence, surveillance, and reconnaissance (ISR) capabilities to enhance battlefield awareness and threat detection. Military EO/IR systems play a critical role in day-and-night surveillance, target identification, and situational awareness across land, naval, and airborne platforms. As armed forces modernize equipment and enhance ISR readiness, demand for high-resolution, long-range EO/IR sensors continues to grow steadily worldwide.

87% of global defense programs prioritized investment in advanced military EO/IR systems fueled by rising defense budgets and the critical need for enhanced ISR capabilities in modern warfare.

-

Growing adoption of unmanned platforms and network-centric warfare is accelerating integration of EO/IR sensors for enhanced situational awareness and target acquisition

The increasing deployment of unmanned aerial vehicles, unmanned ground vehicles, and unmanned maritime systems has significantly boosted demand for EO/IR payloads. These sensors enable real-time intelligence gathering, persistent surveillance, and precision targeting without risking human lives. Additionally, network-centric warfare concepts emphasize data sharing across platforms, where EO/IR systems serve as critical sensing nodes. Integration with command-and-control systems improves situational awareness and mission effectiveness. As militaries invest in autonomous and connected defense systems, EO/IR sensor integration remains a key technological requirement.

85% of defense programs integrated EO/IR sensors into unmanned platforms and network-centric architectures driving real-time situational awareness, precision targeting, and battlefield dominance.

EO/IR Systems Market Restraints:

-

High development, procurement, and maintenance costs of advanced EO/IR systems limit adoption among cost-constrained defense forces and smaller military organizations

Advanced military EO/IR systems require sophisticated sensors, cooling mechanisms, optics, and image-processing technologies, making them expensive to develop and procure. Ongoing maintenance, calibration, and upgrades further increase lifecycle costs. Smaller defense forces and developing nations often face budget constraints, limiting their ability to deploy advanced EO/IR solutions at scale. Cost pressures may lead to delayed procurement cycles or reliance on legacy systems. These financial barriers restrict broader market penetration and slow adoption in regions with limited defense spending.

In 2025, 76% of cost-constrained defense forces and smaller militaries deferred adoption of advanced EO/IR systems due to high development, procurement, and lifecycle costs prioritizing affordability over cutting-edge capabilities.

-

Stringent export controls, technology transfer restrictions, and regulatory approvals hinder international sales and delay deployment of military EO/IR systems

Military EO/IR technologies are considered sensitive defense equipment and are subject to strict export control regulations in many countries. Governments impose limitations on technology transfer, licensing, and international sales to protect national security interests. These regulatory requirements can delay contract approvals, restrict market access, and complicate cross-border partnerships. Defense manufacturers often face lengthy approval timelines and compliance costs. Such restrictions reduce global market expansion opportunities and limit the ability of suppliers to serve allied or emerging defense markets efficiently.

78% of defense firms faced delays in global EO/IR system deployment due to stringent export controls, technology transfer restrictions, and complex regulatory approvals limiting international market access and revenue growth.

EO/IR Systems Market Opportunities:

-

Technological advancements in sensor fusion, artificial intelligence, and image processing create opportunities for next-generation EO/IR systems with improved detection capabilities

Rapid advancements in artificial intelligence, machine learning, and sensor fusion technologies are transforming military EO/IR systems. AI-enabled image processing improves target recognition, reduces false alarms, and enhances decision-making speed. Sensor fusion integrates EO, IR, radar, and other data sources to provide comprehensive situational awareness. These innovations enable longer detection ranges, higher accuracy, and improved performance in complex environments. Defense forces increasingly seek next-generation EO/IR solutions with intelligent capabilities, creating strong opportunities for innovation-driven vendors.

In 2025, 83% of defense developers integrated AI-driven sensor fusion and advanced image processing into next-generation EO/IR systems significantly enhancing target detection, situational awareness, and mission effectiveness.

-

Rising demand for EO/IR upgrades, retrofitting, and lifecycle support programs offers long-term revenue opportunities for defense contractors and system integrators

Many military platforms currently operate legacy EO/IR systems that require upgrades to meet modern operational requirements. Defense forces are investing in retrofitting programs to enhance sensor performance, extend platform life, and reduce replacement costs. Additionally, long-term maintenance, repair, overhaul, and lifecycle support services generate recurring revenue for suppliers. As modernization initiatives continue, demand for system upgrades and support contracts is expected to rise. This creates sustained business opportunities for defense contractors and system integrators across global markets.

81% of defense contractors and system integrators secured long-term revenue streams by delivering EO/IR upgrades, retrofits, and lifecycle support driven by modernization mandates and extended platform service lives.

Military Electro-Optical and Infrared (EO/IR) Systems Market Segment Highlights

-

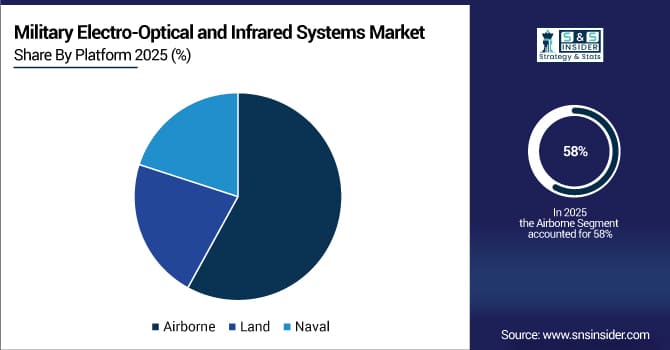

By Platform: Airborne led with 58% share, while Land is the fastest-growing segment.

-

By Component: Sensors & Detectors led with 34% share, while Laser Designators & Illuminators is the fastest-growing segment.

-

By Technology: Infrared Systems led with 35% share, while Hyperspectral Systems is the fastest-growing segment.

-

By Application: Surveillance & Reconnaissance led with 33% share, while Navigation & Guidance is the fastest-growing segment.

-

By End User: Air Force led with 39% share, while Navy is the fastest-growing segment.

By Platform: Airborne led, while Land is the fastest-growing segment.

Airborne platforms dominate the Military EO/IR market due to their extensive use in fighter jets, transport aircraft, reconnaissance aircraft, and unmanned aerial vehicles (UAVs). EO/IR systems on airborne platforms provide critical surveillance, target acquisition, and situational awareness capabilities. High mobility, extensive coverage, and advanced integration with navigation and fire-control systems make airborne EO/IR systems the largest revenue contributor. Their deployment in both combat and intelligence missions ensures continuous demand, while upgrades in sensor technologies and miniaturization further reinforce the dominance of airborne platforms in the global market.

Land platforms are the fastest-growing segment as armies increasingly equip vehicles and ground troops with advanced EO/IR systems for surveillance, targeting, and navigation. Soldier-borne sights, vehicle-mounted systems, and tactical observation sensors are rapidly adopted to improve battlefield awareness and precision engagement. Rising defense modernization programs, border security initiatives, and unmanned ground vehicle deployments are accelerating growth. The segment’s expansion is further supported by lightweight, modular, and portable EO/IR solutions, enabling smaller units to benefit from high-performance imaging capabilities, making land platforms a high-growth focus for military technology investments.

By Component: Sensors & Detectors led, while Laser Designators & Illuminators is the fastest-growing segment.

Sensors & Detectors dominate the market as the core component of EO/IR systems, including focal plane arrays, photodetectors, and imaging sensors. These components capture high-resolution imagery and thermal data, forming the backbone of surveillance, reconnaissance, and targeting systems. Their critical role in enhancing operational accuracy, reliability, and mission success drives large-scale procurement across air, land, and naval platforms. Continuous advancements in sensitivity, low-light performance, and integration with AI analytics further reinforce the dominance of sensors and detectors in the EO/IR ecosystem.

Laser Designators & Illuminators are the fastest-growing component segment, supporting precision targeting, range-finding, and guided munitions. Modern militaries increasingly rely on laser-based systems to enhance accuracy, reduce collateral damage, and support multi-platform interoperability. Growth is fueled by demand for advanced targeting in both airborne and land combat systems, coupled with expanding use in unmanned systems and integrated fire-control networks. Technological improvements, such as compact, eye-safe lasers and high-power illumination systems, drive adoption, positioning laser designators as a rapidly growing revenue contributor in the EO/IR market.

By Technology: Infrared Systems led, while Hyperspectral Systems is the fastest-growing segment.

Infrared (IR) systems dominate the EO/IR market due to their essential role in night operations, low-visibility environments, and thermal detection. IR imaging provides real-time situational awareness, target acquisition, and reconnaissance capabilities across air, land, and naval platforms. High demand in defense for surveillance, tactical engagement, and autonomous platform integration ensures sustained dominance. Continuous enhancements in thermal sensor resolution, range, and detection speed, along with integration with AI and targeting systems, reinforce infrared systems as the largest technology segment in military EO/IR applications.

Hyperspectral systems are the fastest-growing technology segment, offering advanced detection, material identification, and target discrimination capabilities. These systems provide multi-band imaging beyond standard visible and infrared, supporting precision intelligence, surveillance, and reconnaissance (ISR). Rapid growth is driven by the increasing need for advanced battlefield awareness, detection of camouflaged targets, and integration with unmanned platforms. Investments in hyperspectral payloads for aircraft, UAVs, and satellites, combined with technological miniaturization, are accelerating adoption, positioning hyperspectral systems as a high-growth area within the EO/IR technology market.

By Application: Surveillance & Reconnaissance led, while Navigation & Guidance is the fastest-growing segment.

Surveillance & Reconnaissance dominate the EO/IR market as the primary function across all platforms. EO/IR systems are extensively used for monitoring enemy movements, intelligence gathering, and battlefield awareness. This application is critical for national defense, border security, and mission planning. High adoption is driven by the increasing need for real-time data collection, target tracking, and interoperability across platforms. Continuous upgrades in sensor resolution, AI analytics, and long-range imaging further strengthen the dominance of surveillance and reconnaissance as the largest application segment.

Navigation & Guidance is the fastest-growing application segment, as EO/IR systems are increasingly integrated with UAVs, missiles, and precision-guided munitions. These systems enhance accuracy, reduce operational risks, and support autonomous navigation in low-visibility or GPS-denied environments. Growth is fueled by demand for advanced military vehicles, drones, and smart munitions capable of precise engagement. Improvements in miniaturization, AI-assisted image processing, and sensor fusion are accelerating adoption, making navigation and guidance a rapidly expanding use case within the EO/IR market.

By End User: Air Force led, while Navy is the fastest-growing segment.

The Air Force dominates EO/IR adoption due to extensive procurement for fighter aircraft, transport planes, and UAVs. EO/IR systems enable airborne ISR, targeting, and situational awareness missions, which are critical to modern air operations. High operational volumes, advanced platform integration, and continuous modernization programs reinforce Air Force dominance. The Air Force’s focus on upgrading legacy platforms with high-resolution EO/IR payloads ensures sustained revenue contribution, making it the largest end-user segment in the military EO/IR market.

The Navy is the fastest-growing end-user segment as maritime security and littoral operations drive the need for EO/IR integration on ships, patrol vessels, and unmanned systems. EO/IR systems provide enhanced situational awareness, target tracking, and missile defense capabilities at sea. Growth is accelerated by increasing investments in naval modernization, unmanned surface and underwater vehicles, and integrated defense networks. The adoption of advanced EO/IR payloads for surveillance, targeting, and navigation positions the Navy as a rapidly expanding customer segment in the global market.

Military Electro-Optical and Infrared Systems Market Regional Analysis

North America Military Electro-Optical and Infrared Systems Market Insights:

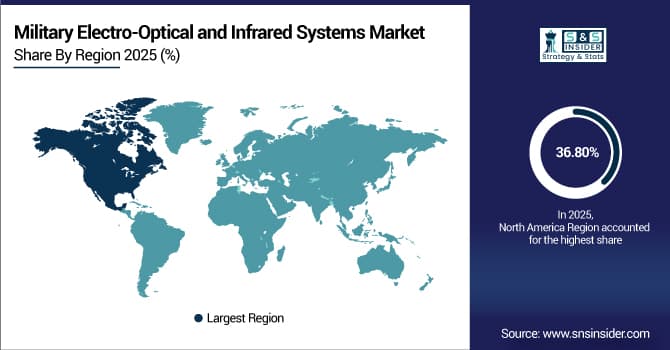

North America dominated the Military Electro-Optical and Infrared Systems Market with a 36.80% share in 2025 due to the region’s advanced defense infrastructure, high defense spending, and strong presence of leading defense contractors. Continuous investments in cutting-edge EO/IR technologies, surveillance systems, and precision targeting solutions further reinforced North America’s market leadership.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Military Electro-Optical and Infrared Systems Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 5.87% from 2026–2035, driven by increasing defense budgets, modernization of military forces, and rising demand for advanced surveillance, targeting, and reconnaissance systems. Growing geopolitical tensions, expansion of domestic defense manufacturing, and adoption of high-tech EO/IR solutions accelerate the market growth in the region.

Europe Military Electro-Optical and Infrared Systems Market Insights

Europe held a significant share in the Military Electro-Optical and Infrared Systems Market in 2025, supported by established defense programs, high R&D investments, and strong aerospace and defense manufacturing capabilities. Adoption of advanced surveillance, targeting, and reconnaissance systems, along with strategic modernization initiatives, further reinforced Europe’s stable market presence.

Middle East & Africa and Latin America Military Electro-Optical and Infrared Systems Market Insights

The Middle East & Africa and Latin America together exhibited moderate growth in the Military Electro-Optical and Infrared Systems Market in 2025, driven by increasing defense spending, modernization of armed forces, and rising demand for advanced EO/IR systems. Geopolitical concerns, expanding domestic defense industries, and procurement of high-technology surveillance and targeting solutions contributed to the regions’ growing market participation.

Military Electro-Optical and Infrared Systems Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin Corporation is a leading global defense and aerospace company, recognized for its advanced military technologies, including electro-optical and infrared (EO/IR) systems. The company develops high-precision sensors, targeting systems, and surveillance solutions for air, land, and maritime applications. Its EO/IR technologies are integrated into aircraft, unmanned systems, and missile platforms, enhancing situational awareness and operational effectiveness. With a strong R&D focus, Lockheed Martin delivers innovative, reliable, and mission-critical systems that support military modernization programs worldwide.

-

October 2024: Lockheed unveiled its next-generation Legion Pod IRST21 (Infrared Search and Track) enhancements at AUSA 2024, featuring improved long-range passive detection capabilities against stealth aircraft using advanced IR sensors and AI-enabled tracking algorithms. The pod is being integrated onto F-15EX and F-16 fleets.

Northrop Grumman Corporation

Northrop Grumman Corporation is a major U.S.-based defense and aerospace company specializing in advanced technologies, including EO/IR systems for military applications. The company designs and manufactures sensor systems, targeting pods, and integrated surveillance solutions for aircraft, naval vessels, and ground platforms. Northrop Grumman emphasizes precision, durability, and cutting-edge technology to improve battlefield awareness and targeting capabilities. Its products are widely adopted by armed forces globally, supporting intelligence, reconnaissance, and security missions with high reliability and performance.

-

March 2024: Northrop Grumman received a USD215 million U.S. Air Force contract to deliver LITENING Advanced Targeting Pods, which include cutting-edge mid-wave infrared (MWIR) and short-wave infrared (SWIR) sensors. The pods support precision strike missions for F-16s and A-10s.

Raytheon Technologies Corporation

Raytheon Technologies Corporation is a prominent global defense and aerospace company, known for its expertise in missile systems, radar, and EO/IR technologies. The company develops advanced electro-optical and infrared sensors, targeting systems, and surveillance solutions for military aircraft, naval platforms, and ground vehicles. Raytheon focuses on high-precision, reliable, and mission-critical systems that enhance situational awareness, target acquisition, and operational effectiveness. Its innovations support global defense forces in intelligence gathering, threat detection, and combat readiness.

-

May 2024: RTX’s Raytheon segment secured a USD498 million contract from the U.S. Department of Defense to supply AN/AAQ-28(V) LITENING G4+ targeting pods, featuring enhanced thermal imaging, laser range finding, and AI-assisted target recognition. Deliveries began in late 2024.

Military Electro-Optical and Infrared Systems Companies are:

-

Lockheed Martin Corporation

-

Raytheon Technologies Corporation

-

Thales Group

-

BAE Systems plc

-

Elbit Systems Ltd.

-

L3Harris Technologies, Inc.

-

Leonardo S.p.A.

-

Teledyne FLIR LLC

-

Rheinmetall AG

-

Saab AB

-

Safran SA

-

Israel Aerospace Industries Ltd.

-

Textron Inc.

-

CONTROP Precision Technologies

-

Hensoldt AG

-

Airbus SE

-

Aselsan A.Ş.

-

OIP Sensor Systems

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 8.93 Billion |

| Market Size by 2035 | USD 13.51 Billion |

| CAGR | CAGR of 4.25% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Airborne, Land, Naval) • By Component (Sensors & Detectors, Optics & Lenses, Processing Electronics, Displays, Laser Designators & Illuminators) • By Technology (Electro-Optical Systems, Infrared Systems, Multispectral Systems, Hyperspectral Systems) • By Application (Surveillance and Reconnaissance, Target Acquisition and Designation, Weapon Sighting and Fire Control, Navigation and Guidance) • By End User (Army, Navy, Air Force) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Thales Group, BAE Systems plc, Elbit Systems Ltd., L3Harris Technologies, Inc., General Dynamics Corporation, Leonardo S.p.A., Teledyne FLIR LLC, Rheinmetall AG, Saab AB, Safran SA, Israel Aerospace Industries Ltd., Textron Inc., CONTROP Precision Technologies, Hensoldt AG, Airbus SE, Aselsan A.Ş., OIP Sensor Systems. |

Frequently Asked Questions

North America dominated the Military Electro-Optical and Infrared Systems Market in 2025 with a 36.80% share.

Rising defense modernization programs and increasing demand for advanced surveillance, reconnaissance, and targeting capabilities are driving market growth.

Surveillance & Reconnaissance dominated the Military Electro-Optical and Infrared Systems Market by application.

The Military Electro-Optical and Infrared Systems Market was valued at USD 8.93 billion in 2025.

The Military Electro-Optical and Infrared Systems Market is expected to grow at a CAGR of 4.52% from 2026 to 2035.

Get in Touch