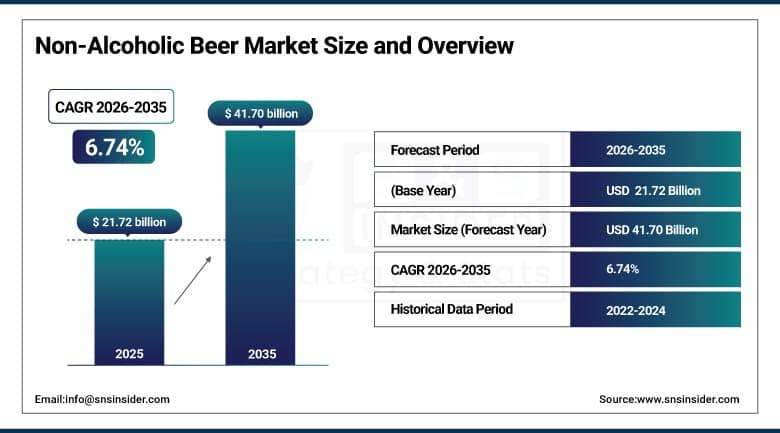

As per the SNS Insider Report titled, Non-Alcoholic Beer Market by Category, by Packaging, by Type, by Distribution Channel, and by Region, “The global Non-Alcoholic Beer Market size was estimated at USD 21.72 billion in 2025, is anticipated to grow to USD 41.70 billion by 2035, registering a CAGR of 6.74% during the forecast period 2026–2035.”

Key Takeaways

-

Bottles dominated the packaging segment with a 52.39% market share in 2025, supported by strong consumer preference, brand familiarity, and extensive retail availability.

-

Cans are projected to witness the fastest growth at a CAGR of 7.24% during 2026–2035 owing to their convenience, portability, recyclability, and growing appeal among younger consumers.

-

Regular Non-Alcoholic Beer accounted for 48.25% of the market revenue in 2025 due to its widespread availability and established consumer base.

-

Flavored Non-Alcoholic Beer is expected to register the fastest CAGR of 6.11% through 2035 as consumers increasingly seek innovative taste profiles and premium beverage experiences.

-

Alcohol-Free Beer held the largest share of 56.21% in 2025, driven by growing health consciousness and demand for beverages containing zero alcohol.

-

Low-Alcohol Beer is forecast to expand at the fastest CAGR of 7.64% during the forecast period as consumers look for balanced alternatives that offer traditional beer characteristics with reduced alcohol content.

-

Supermarkets and Hypermarkets dominated the distribution channel segment with a 62.58% market share in 2025 due to their broad product assortment and strong consumer accessibility.

-

Online Retail is anticipated to experience the fastest growth at a CAGR of 6.51% during 2026–2035, supported by expanding e-commerce platforms and changing purchasing behavior.

-

Europe dominated the Non-Alcoholic Beer Market and accounted for 40.35% of total revenue in 2025 due to strong consumer acceptance and the presence of established brewing companies.

-

Asia-Pacific is expected to witness the fastest growth during the forecast period, registering a CAGR of 7.28% from 2026 to 2035.

Why Non-Alcoholic Beer Market is Growing?

The Non-Alcoholic Beer Market is witnessing significant growth due to the rising preference for healthy living habits and responsible drinking. Increasing consciousness about the dangers linked to overconsumption of alcohol has fueled the need for other beverages which provide the flavor and sociability benefits of beer but lack the intoxicating effects.

Adoption of healthy living behaviors by millennials and Gen-Z individuals is resulting in high demand for non-alcoholic and lower alcohol beverages. The rising trend of mindful consumption in developed and developing countries is aiding market development.

Companies operating in the industry are focusing extensively on innovating new flavors and products to cater to diverse consumer needs. Technological advancements in the brewing process have led to improved taste and quality of beverages, thereby closing the gap in preferences.

Furthermore, high availability from supermarkets, specialty stores, restaurants, and online retail platforms is contributing to the sustained growth of the market.

Non-Alcoholic Beer Market Statistics

-

Consumers concerned about their health are becoming less dependent on alcohol consumption and looking for beverages which can help them in maintaining fitness and wellness.

-

The demand for functional and low-calorie beverages is increasing throughout the world, making it an ideal time for non-alcoholic beer production companies.

-

Millennials are becoming increasingly interested in alcohol-free beverages, specifically those of high value.

-

Advancements in technology are resulting in the enhanced flavor preservation of non-alcoholic beers.

-

E-commerce websites are now offering more options for non-alcoholic beverages, leading to increased sales for such products.

-

Non-alcoholic beverages are finding their way into menus at restaurants, bars, and other hospitality establishments.

-

The premiumization of the beverages market is motivating brands to offer craft-style and specialty non-alcoholic beers.

Emerging Trends

There are many innovations taking place in the Non-Alcoholic Beer Market with respect to the development of high-quality products, inclusion of functional ingredients, and flavors. There is an increased preference among young consumers for non-alcoholic beer that is flavored with fruits and botanicals.

The growth of craft non-alcoholic beer is considered one of the key trends in the market since beverage producers are adopting craft brewing practices to offer high-end drinking experiences. The demand for authentic beer without alcohol is on the rise among consumers.

There is an increasing emphasis among beverage companies to use sustainable packing solutions including the use of recyclable cans for their products. This is one of the most notable trends that has emerged in the market.

Finally, digital marketing activities, direct selling, and the subscription-based model have also started revolutionizing the dynamics of the market. Additionally, increased market access and investments in innovation will provide growth opportunities to players across the forecast period.

Top 10 Companies

-

Heineken N.V.

-

Anheuser-Busch InBev

-

Carlsberg Group

-

Asahi Group Holdings

-

Molson Coors Beverage Company

-

Guinness

-

Erdinger Weissbräu

-

Clausthaler

-

Suntory Holdings Limited

-

Kirin Holdings Company Limited

About the Author

Get in touch