1-Decene Market Report Scope & Overview:

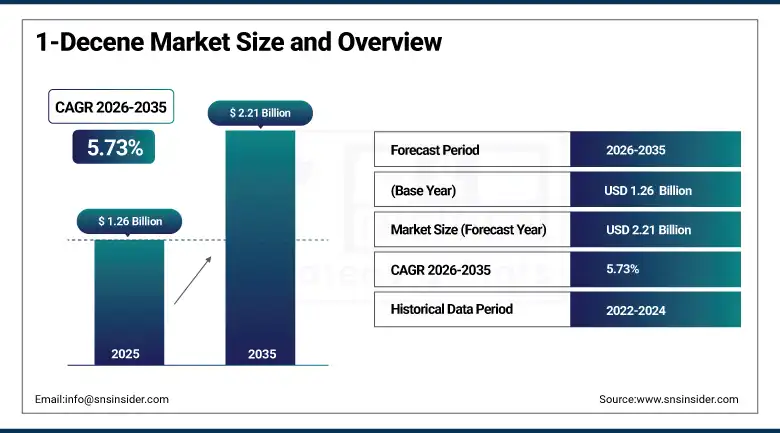

The 1-Decene Market size was USD 1.26 Billion in 2025 and is expected to reach USD 2.21 Billion by 2035, growing at a CAGR of 5.73% from 2026–2035.

The 1-Decene is an important alpha olefin utilized for the production of synthetic lubricants, polyethylene, and surfactants. The demand continues to increase in the automotive, packaging, and industrial industries. Market coverage entails production capacity and utilization in producing countries. The price and availability of raw materials greatly determine the cost composition. The trade flow determines the leading importers and exporters in the world. Environmental legislation encourages manufacturers to embrace more eco-friendly production processes. Technological innovation in catalysts continues, thereby improving yield and purity. Research and development expenditure in process optimization is increasing too across the industry. Capacity utilization in plants is improving as producers optimize efficiency levels. All this information is helpful in formulating long-term strategies. In 2023, Europe had the largest revenue share in the market.

In October 2024, INEOS took control of the production plant from Royal Dutch Shell. INEOS' alpha-olefins business got a boost after this acquisition. Additionally, there was expansion of its global production capacity base. This represents a general trend of mergers among key players in the chemicals industry. Major firms are working hard to lock up supply and expand capacity. Such a move assists manufacturers in meeting growing demand for superior quality PAO lubricants.

1-Decene Market Size and Forecast

-

Market Size in 2026E: USD 1.34 Billion

-

Market Size by 2035: USD 2.21 Billion

-

CAGR: 5.73% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get more information On 1-Decene Market - Request Free Sample Report

1-Decene Market Trends

-

Synthetic lubricant demand is rising fast as automakers shift toward electric vehicle transmission fluids.

-

Bio-based alpha olefin production is expanding as companies target lower carbon footprints.

-

Catalyst innovation is improving 1-Decene purity and reducing unwanted by-products during oligomerization.

-

Polyethylene producers are increasing 1-Decene use in flexible packaging and e-commerce applications.

-

Vertical integration is growing as producers secure ethylene feedstock to manage cost swings.

-

Trade flow shifts are reshaping import-export patterns as new regional production capacity comes online.

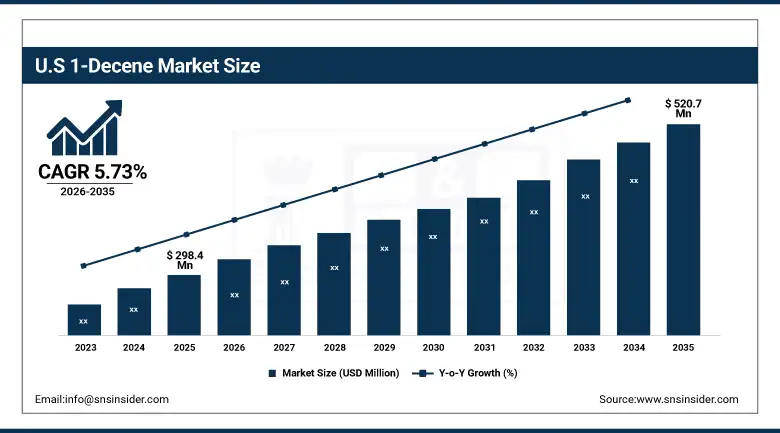

The U.S. 1-Decene Market Outlook

The U.S. 1-Decene Market was valued at approximately USD 298.4 Million in 2025. It is expected to reach approximately USD 520.7 Million by 2035. The market is growing at a CAGR of approximately 5.73%.

The U.S. has the largest single country's market share globally, due to its mature petrochemical industry, large ethylene volumes produced, as well as the increased demand for synthetic oils, polyethylene, and surfactants. Key production is conducted by companies such as ExxonMobil, Chevron Phillips Chemicals, and Shell. Due to favorable policies and adequate infrastructure, production continues to be efficient in the country. Stringent regulations have prompted firms to adopt cleaner manufacturing methods. Shale gas production in the United States is sufficient to ensure competitive pricing relative to other markets. This continues to make the U.S. a leader in global ethylene production.

In August 2024, Chevron Phillips Chemical and TotalEnergies created a joint venture company that aims to increase the production of poly-1-decene within North America. The initiative is geared towards meeting the increasing demand for polymers. The partnership utilizes the capabilities of each firm, where Chevron Phillips specializes in olefins while TotalEnergies focuses on the global business. Joint ventures enable producers to achieve economies of scale quicker and more easily than creating new plants.

1-Decene Market Segment Analysis

-

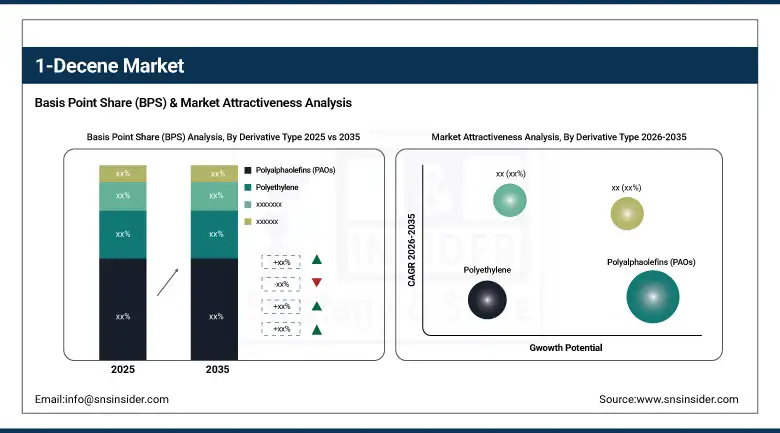

By Derivative Type, the polyalphaolefins segment dominated the 1-Decene market with approximately 48% share in 2025. The detergent alcohols segment is growing fastest, driven by rising surfactant demand in emerging markets.

-

By Application, the polyethylene segment dominated the 1-Decene market with approximately 52% share in 2025. The synthetic lubricants segment is growing fastest, driven by electric vehicle and industrial lubricant demand.

By Derivative Type, PAOs dominate, detergent alcohols grow fastest

Polyalphaolefins held the highest share of 1-Decene's global market share in 2025. Polyalphaolefins (PAOs) are synthetic hydrocarbons derived from 1-Decene. They provide high thermal stability and excellent viscosity characteristics, making them appropriate for applications like engine oils, gear oils, and other industrial lubricants. Production capacities of PAOs have increased recently through initiatives by ExxonMobil and Chevron Phillips Chemical. INEOS Oligomers released new grades of polyalphaolefin products in 2023, which provide superior oxidative stability. Moreover, Shell has started production of next-generation PAO-based lubricants designed for electric vehicle applications. Such lubricants minimize energy losses and fluid consumption, as part of increasing needs in this area from the automotive and aerospace industries.

Among derivatives, Detergent Alcohol is projected to show the highest growth rate. Increasing requirements for surfactants in developing countries are driving this demand. The household cleaners, personal care products, and industrial cleaning agents contain these alcohols. Increasing populations and per capita income levels in Asia-Pacific and Latin America drive their usage. Companies manufacture these products in-country in response to demand, and do not resort to importing. Consequently, this trend will continue, as developing nations continue to industrialize. Demand will continue growing faster than average demand for 1-Decene in general.

By Application, polyethylene dominates, synthetic lubricants grow fastest

In 2025, Polyethylene will account for around 52% of the 1-Decene application share. This is attributed to the increased need for high-performance plastics. It finds applications in the packaging, automobile, and construction industries. Linear low-density and high-density polyethylene utilize 1-Decene as a raw material. The two grades enhance the physical properties of toughness, resilience, and impact resistance. SABIC and Dow Inc. have invested in building capacities for polyethylene production. Dow Inc. released an advanced polyethylene type in 2023 to improve mechanical strength. LyondellBasell created an eco-friendly range of polyethylene through 1-Decene derivatives. E-commerce and food packaging continue to drive this market. Sustainability efforts also affect the selection and processing of feedstock.

Synthetic Lubricants is the fastest-growing segment within the market. It is due to the transition towards electric automobiles. Transmission fluids and thermal management require synthetic lubricants. There is an increase in environmental regulations against the use of mineral-based oils. Companies such as ExxonMobil and INEOS are increasing capacities to cater to this trend. Synthetic lubricants also find use in machinery in the industrial sector. With increased electrification of global vehicles, this application segment is expected to grow at a rapid pace ahead of the overall 1-Decene market.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Qatar |

32.6% |

|

Latin America |

Brazil |

38.4% |

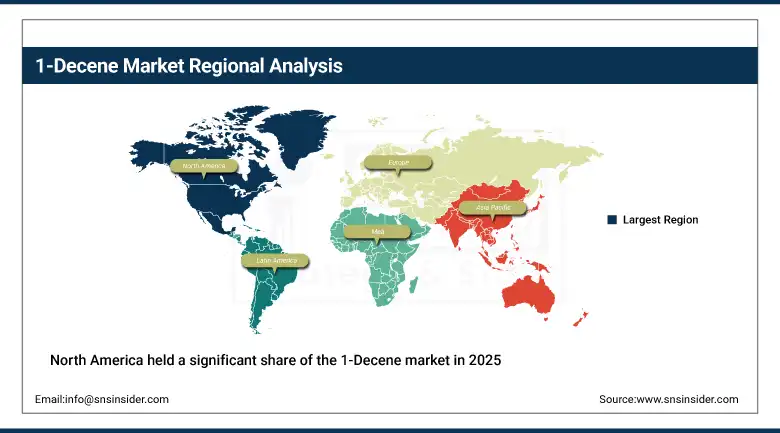

North America 1-Decene Market Insights

North America held a significant share of the 1-Decene market in 2025. Strong synthetic lubricant demand and advanced polymer production both support this position. The region benefits from a mature, fully developed petrochemical sector. ExxonMobil, Chevron Phillips Chemical, and Shell Chemicals all run major facilities here. Continued investment in enhanced oil recovery keeps feedstock costs competitive for regional producers.

The United States accounts for approximately 82.5% of North American revenue. ExxonMobil launched a new PAO-based lubricant series for electric vehicles in 2023. Rising packaging, automotive, and construction demand keeps pulling more 1-Decene into polyethylene production. Canada and Mexico contribute smaller, supplementary volumes to overall regional output. This trend should continue through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe 1-Decene Market Insights

Europe held the largest share of the 1-Decene market in 2025, at around 44%. Strong demand for synthetic lubricants and healthy polymer production both drive this lead. The region’s automotive and aerospace industries rely heavily on PAO-based lubricants. EU environmental rules are pushing producers toward bio-based and high-purity alpha olefins. Germany, France, and the Netherlands together host much of the region’s production capacity.

Germany accounts for approximately 28.4% of European revenue. INEOS Oligomers opened a new alpha olefin facility in 2023 to support steady regional supply. Shell Chemicals has also expanded its production capacity across the continent. Europe’s circular economy push keeps reinforcing its leadership position globally. Continued R&D funding for catalyst innovation should help sustain this advantage.

Asia Pacific 1-Decene Market Insights

Asia Pacific is the fastest-growing 1-Decene market today. Rapid industrialization and rising packaging demand are the key drivers. China leads regional consumption, supported by a large domestic polyethylene industry. Growing investment in petrochemical infrastructure keeps adding new capacity. South Korea and Japan also contribute steady demand through their established chemical sectors.

In China rising e-commerce and food packaging demand are pulling more polyethylene production into the region. India and Southeast Asia are also expanding their chemical manufacturing base. This regional growth should keep outpacing the global average for years.

MEA & Latin America 1-Decene Market Insights

Qatar leads MEA revenue through the country’s strong petrochemical base and abundant natural gas feedstock support this position. Qatar Chemical Company and Qatar Petroleum both run significant 1-Decene production operations. Saudi Arabia and the UAE contribute smaller but growing volumes to the region. Regional refining expansion projects should add further capacity over the coming years.

Brazil leads Latin American revenue through growing packaging and automotive demand support this position. Mexico and Argentina contribute secondary demand through their own expanding petrochemical sectors. Regional investment in downstream polyethylene capacity should continue lifting demand over time.

Market Dynamics

Growth Drivers: Rising synthetic lubricant demand and growing polyalphaolefin adoption across automotive and industrial sectors

Increasing demand for synthetic lubricants is one of the key drivers for growth. Synthetic oils, like PAOs, exhibit better thermal stability and lower volatility than mineral oils. Rapid growth is observed in the automobile, aviation, and industrial industries. This drives increased demand for high-grade lubricants that help enhance the performance of engines. Emission regulations have driven demand for synthetics even further. Companies such as ExxonMobil, INEOS, and Chevron Phillips Chemical continue to ramp up production capacity due to rising demand. The trend toward electric vehicles creates another area of growth for the industry. Synthetic lubricants are used in EV transmission systems as well as thermal management systems.

Bio-based PAO development is also picking up pace. Lubricant formulation technology keeps improving year after year. Asia Pacific and North America are both seeing strong demand growth. Rising industrial activity and growing investment in high-performance automotive lubricants support this trend. New additive packages are extending oil change intervals across both commercial and passenger vehicles. These factors together keep strengthening 1-Decene’s position as a key raw material across the lubricant value chain.

Restraints: Feedstock price volatility and supply chain disruptions limiting steady production

Price volatility in feedstocks is a key constraint on this market. The source of 1-Decene is mainly ethylene, which is produced using crude oil and natural gas. Volatility in crude oil prices is common due to various factors including geopolitical instabilities and OPEC's decision-making. It makes the cost of manufacturing increase and results in volatile margins. Disruptions within the supply chain also pose risks to companies. Port congestion, logistical challenges, and trade barriers are some of the issues that emerged recently in this regard. Small producers feel the impacts of price increases significantly.

The rising cost of shipping materials poses an even greater challenge for the companies in this industry. Regional variations in the acquisition of raw materials cause imbalance between supply and demand. In response to the challenge, producers are engaging in diversification strategies to minimize reliance on one source of materials. Other companies are resorting to vertical integration while long-term supply agreements are also increasing. However, the problem of uncertainty in oil prices persists, limiting sustainable growth in the global 1-Decene market.

Opportunities: Bio-based 1-Decene adoption creating new growth pathways across sustainable chemical production

The development of Bio-based 1-Decene represents an enormous future opportunity. Industries globally are moving towards chemical substitutes that are environmentally friendly. Manufacturers are focusing on the production of renewable and biobased alpha olefins. The need for biodegradable lubricants and green surfactants is increasing continuously. Authorities such as the EU and U.S. EPA are encouraging the use of bio-based chemicals. Even Shell and Sasol are researching the conversion of biomass into olefins. It may lead to innovative ways of producing low carbon emission 1-Decene.

Sustainability drives businesses into making environmental-friendly decisions. It ensures that industries have a sustainable source of raw material in the long run. If the production of bio-based alpha olefins becomes successful in the future, it can become a significant source of income. This can result in the reduction of carbon emissions by the industry. It may also lead to increased customer loyalty for manufacturers of bio-based products.

Recent Developments:

-

2024: INEOS acquired 1-Decene production assets from Royal Dutch Shell, strengthening its position in the alpha-olefins sector and expanding its global production reach.

-

2024: Chevron Phillips Chemical formed a joint venture with TotalEnergies to expand poly-1-decene production facilities across North America, addressing growing polymer demand.

-

2024: Evonik Industries finalized its merger with LANXESS, sharpening its focus on alpha-olefins including 1-Decene to improve production efficiency.

1-Decene Market Key Players are:

-

Royal Dutch Shell

-

INEOS

-

Chevron Phillips Chemical Company LLC

-

SABIC

-

Exxon Mobil Corporation

-

Qatar Chemical Company II Ltd.

-

Idemitsu Kosan Co. Ltd.

-

PJSC Nizhnekamskneftekhim

-

Agene Chemicals

-

Gelest Inc.

-

LG Chem

-

Qatar Petroleum

-

Sasol Limited

-

Mitsui Chemicals Inc.

-

Evonik Industries AG

-

TotalEnergies SE

-

LANXESS AG

-

BASF SE

-

Qatar Petrochemical Company (QAPCO)

-

Reliance Industries Limited

1-Decene Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.26 Billion |

| Market Size by 2035 | USD 2.21 Billion |

| CAGR | CAGR of 5.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Derivative Type (Polyalphaolefins (PAOs), Polyethylene, Detergent Alcohols, Oxo Alcohols, Others) • By Application (Surfactants, Plasticizers, Synthetic Lubricants, Polyethylene, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Royal Dutch Shell, INEOS, Chevron Phillips Chemical Company LLC, SABIC, Exxon Mobil Corporation, Qatar Chemical Company II Ltd., Idemitsu Kosan Co. Ltd., PJSC Nizhnekamskneftekhim, Agene Chemicals, Gelest Inc., LG Chem, Qatar Petroleum, Sasol Limited, Mitsui Chemicals Inc., Evonik Industries AG, TotalEnergies SE, LANXESS AG, BASF SE, Qatar Petrochemical Company (QAPCO), and Reliance Industries Limited. |

Frequently Asked Questions

The 1-Decene Market is expected to grow at a CAGR of 5.73% from 2026 to 2035.

The 1-Decene Market was valued at USD 1.26 Billion in 2025.

Rising synthetic lubricant demand, growing polyalphaolefin adoption in electric vehicles, and increasing bio-based alpha olefin investment are the primary growth factors.

The Polyalphaolefins segment dominated the 1-Decene Market with approximately 48% share in 2025.

Europe dominated the 1-Decene Market with approximately 44% revenue share in 2025.

Get in Touch