AD Network Software Market Report Scope & Overview:

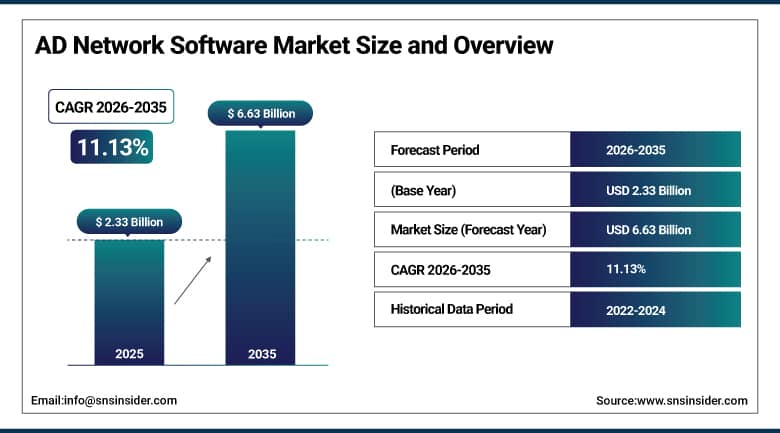

The AD Network Software Market was valued at USD 2.33 Billion in 2025 and is expected to reach USD 6.63 Billion by 2035, growing at a CAGR of 11.13% from 2026–2035.

The global AD network software market stands at the centre of the digital advertising industry’s structural transformation toward programmatic automation, AI-powered audience targeting, and real-time bidding infrastructure that is redefining how advertisers reach consumers and how publishers monetise digital inventory. Ad network software platforms serve as the technological intermediary connecting advertisers with publishers, orchestrating millisecond-duration real-time bidding auctions, audience data matching, campaign optimisation, fraud detection, and reporting workflows that collectively determine campaign efficiency across display, mobile, video, and connected TV formats.

Equativ launched its AI-powered programmatic platform Maestro by Equativ in January 2025, developed following feedback from over 500 clients, representing the most commercially significant independent ad network software innovation of the year. This development demonstrates the accelerating integration of artificial intelligence into programmatic advertising workflows, transforming campaign bidding strategy, audience segmentation, and inventory optimisation from manually configured rule sets into continuously learning automated systems that improve performance outcomes with each campaign cycle executed on the platform.

Market Size and Forecast

-

Market Size in 2026E: USD 2.59 Billion

-

Market Size by 2035: USD 6.63 Billion

-

CAGR: 11.13% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On AD Network Software Market - Request Free Sample Report

AD Network Software Market Trends

-

Rising adoption of AI and machine learning in ad network platforms is improving audience segmentation precision, predictive bidding, and real-time campaign optimisation across display, mobile, and video advertising formats globally.

-

Growing shift to first-party data strategies as third-party cookie deprecation accelerates is driving demand for ad network software with privacy-compliant audience targeting and contextual intelligence capabilities.

-

Expanding programmatic advertising adoption across mobile and connected TV platforms is broadening the inventory categories served by ad network software beyond traditional web display into high-growth OTT environments.

-

Increasing focus on brand safety and ad fraud prevention is compelling providers to integrate real-time traffic quality verification, invalid traffic filtering, and viewability measurement as standard platform capabilities.

-

Growing demand from SMEs for self-serve programmatic advertising access is driving adoption of lower-friction ad network software interfaces that democratise campaign management beyond large enterprise organisations.

U.S. AD Network Software Market Outlook

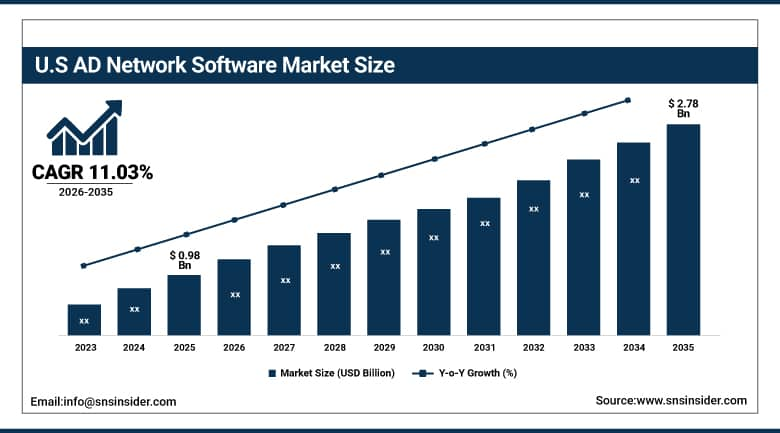

The U.S. AD Network Software Market was valued at approximately USD 0.98 Billion in 2025 and is expected to reach approximately USD 2.78 Billion by 2035, growing at a CAGR of approximately 11.03%.

Demand in the U.S. market is driven by the country’s position as the world’s most commercially advanced digital advertising market, combining the highest digital ad spending per capita globally with the largest concentration of both buy-side and sell-side ad technology companies. Google AdSense and Amazon Publisher Services dominate the publisher monetisation layer, while PubMatic, Magnite, Equativ, InMobi, Criteo, and AppLovin compete actively for mid-market and specialised inventory categories. Third-party cookie deprecation in Chrome and Safari is compelling platform operators to invest in privacy-preserving audience targeting alternatives including contextual intelligence, first-party data clean rooms, and universal identity solutions that maintain campaign performance within regulatory frameworks.

Google’s early 2024 Ads Power Pair initiative combining Search and Performance Max AI tools demonstrated the commercial direction of the largest platform toward increasingly automated, AI-directed campaign management that reduces advertiser reliance on manual bidding strategy configuration, validating the market’s broader trajectory toward AI-first programmatic operations that independent ad network platforms are also pursuing through their own machine learning investment programmes.

AD Network Software Market Segment Analysis

-

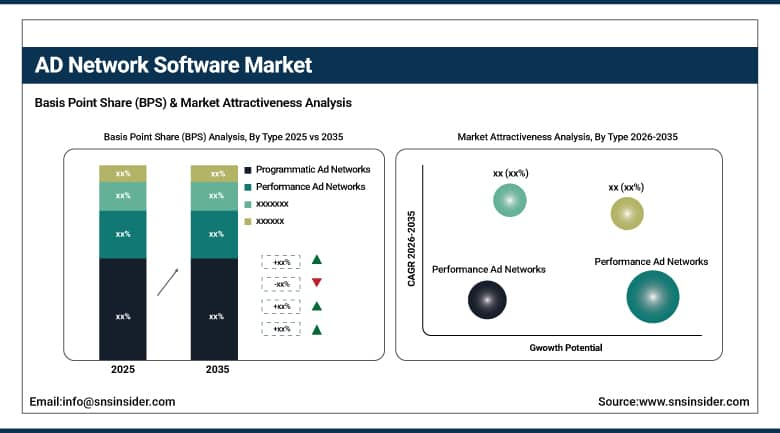

By Type, programmatic ad networks dominated with approximately 69% share in 2024 and are the fastest-growing segment at a CAGR of 11.71% through 2035.

-

By Deployment, cloud-based deployment dominated the market in 2025 through its scalability to process billions of ad auctions daily, automatic feature updates, and cost efficiency relative to maintaining proprietary on-premises programmatic infrastructure.

-

By Enterprise Size, large enterprises dominated the market in 2025 through their higher programmatic budgets, more complex multi-channel campaign management requirements, and greater investment in data integration, analytics, and brand safety infrastructure. SMEs are the fastest-growing segment.

-

By End User, retail and e-commerce dominated the market in 2025 through the sector’s high digital advertising investment, product-level audience targeting requirements, and strong ROI attribution from performance ad networks. Media and entertainment is the fastest-growing end user.

By Type, programmatic ad networks dominate and grow fastest

Programmatic ad networks retained the dominant type position with approximately 69% of the ad network software market in 2024, a dominance reflecting the industry’s decisive transition to automated ad buying as the default transaction model for digital inventory across virtually every publisher category and ad format. The commercial logic of programmatic’s dominance is grounded in the genuine efficiency advantages it delivers to both sides of the transaction: advertisers achieve more precise audience targeting, real-time performance optimisation, and transparent cost measurement than direct-sold media provides, while publishers achieve higher effective CPMs through auction-based competition that reveals true market clearing prices superior to the negotiated rate cards that direct sales teams historically achieved at the cost of significant operational overhead.

Programmatic ad networks are simultaneously the fastest-growing segment at a CAGR of 11.71% through 2035, driven by ongoing expansion into connected TV, digital out-of-home, audio streaming, and in-app mobile environments that were previously served primarily through direct-sold or non-programmatic models. InMobi’s research confirming that high-attention programmatic placements delivered up to 5x higher click-through rates and 50% higher view-through rates than standard placements quantifies the performance premium that optimised programmatic delivery achieves over alternatives, providing the advertiser outcome data that sustains programmatic’s continuing displacement of traditional ad buying models. Generative AI integration into programmatic creative optimisation is adding a creative automation capability to programmatic’s existing bidding and targeting automation that further expands the efficiency advantage it delivers.

By End User, retail & e-commerce dominates, media & entertainment grows fastest

Retail and e-commerce retained the dominant end user position in the ad network software market in 2025, reflecting the sector’s extraordinary investment in performance digital advertising whose ROI is directly measurable through conversion tracking from ad impression through to purchase transaction, creating the closed-loop attribution that justifies above-average digital advertising investment per dollar of sales. The retail sector’s product catalogue advertising requirements, where individual SKU-level targeting and dynamic product feed-based ad serving must operate at scale across millions of product-consumer matching combinations, create particularly intensive demand for programmatic ad network infrastructure. Amazon Publisher Services and the growing retail media network ecosystems of Target, Walmart, and Kroger are reshaping the competitive landscape by creating closed retail media environments whose first-party purchase data advantages attract advertiser budget.

Media and entertainment is the fastest-growing end user segment, driven by the commercial expansion of connected TV and OTT streaming advertising whose programmatic buying infrastructure is developing rapidly as platforms including Netflix, Disney+, Peacock, and Paramount+ monetise their advertising-supported subscriber bases. The structural shift of television advertising spend from linear broadcast to connected TV environments is creating the most commercially significant new programmatic inventory category of the current decade, combining premium brand-safe content environments with superior audience targeting relative to linear TV that is attracting major brand advertising budgets into the programmatic trading environment that ad network software platforms enable.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

55.2% |

|

Middle East & Africa |

UAE |

32.1% |

|

Latin America |

Brazil |

44.2% |

North America AD Network Software Market Insights

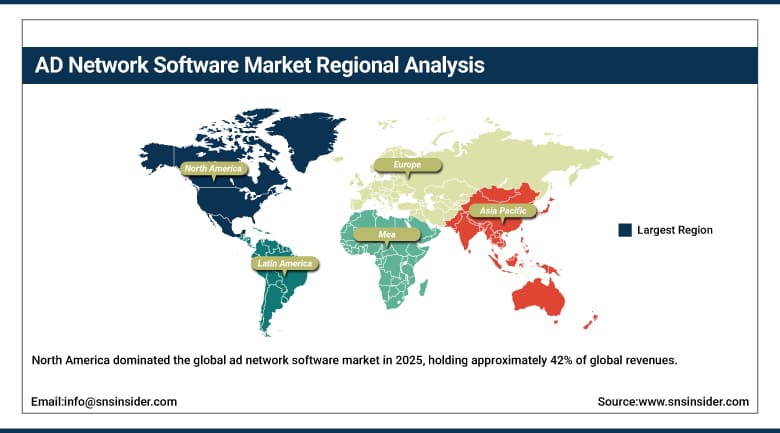

North America dominated the global ad network software market in 2025, holding approximately 42% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s leadership is grounded in its concentration of the world’s most valuable digital advertising inventory, the highest digital ad spending per capita of any regional market, and the headquarters locations of every major ad network platform company whose product development decisions propagate globally from North American market experience. The structural advantages of North America’s digital advertising ecosystem, including its mature programmatic trading infrastructure, sophisticated advertiser data management capabilities, and transparent auction environment, consistently define global platform standards.

Canada contributes approximately 12.6% of North American revenues through a digital advertising market that mirrors U.S. programmatic adoption trends at slightly lower absolute scale, with Canadian publishers and advertisers progressively adopting the same AI-powered ad network platforms whose U.S. commercial precedent provides the adoption confidence driving Canadian enterprise and SME programmatic transition.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe AD Network Software Market Insights

Europe is a commercially significant ad network software market where GDPR’s data protection framework has fundamentally reshaped programmatic advertising operations, compelling ad network platforms to develop privacy-preserving audience targeting technologies, consent management infrastructure, and data minimisation practices that comply with regulators’ interpretation of lawful digital advertising data processing. Germany accounts for approximately 22.3% of European revenues as the region’s largest national digital advertising market, combining the continent’s most active e-commerce sector, a mature publisher ecosystem, and strict data protection enforcement by the Bundesdatenschutzbehörde creating the most demanding regulatory compliance environment for ad network software operations.

The United Kingdom and France are significant secondary European markets where the advertising technology ecosystem is commercially active and technically sophisticated. Equativ, headquartered in Paris, completed the full integration of Sharethrough in 2025 following its 2024 acquisition, creating an independent end-to-end media platform combining Equativ’s supply-side technology with Sharethrough’s high-attention native and CTV advertising formats that provides European publishers with a credible alternative to the Google-Amazon duopoly at the supply-side platform layer.

Asia Pacific AD Network Software Market Insights

Asia Pacific is the fastest-growing regional ad network software market, driven by the explosive growth of mobile digital advertising across China, India, Southeast Asia, Japan, and South Korea whose combined smartphone user base exceeding 2.5 billion creates the world’s largest mobile advertising inventory pool. China accounts for approximately 55.2% of Asia Pacific revenues through its domestic digital advertising ecosystem dominated by Alibaba’s Alimama, ByteDance’s advertising platform, and Tencent’s social and gaming inventory that collectively represent a programmatic trading environment of a scale and sophistication rivalling North America’s, operating primarily through domestic platforms.

India and Southeast Asia represent the most commercially significant emerging market growth opportunities for international ad network software companies, as rapid growth of digital content consumption, e-commerce, and mobile app usage among hundreds of millions of first-time internet users creates expanding publisher inventory supply and advertiser demand that programmatic ad network infrastructure is progressively capable of monetising through the mobile-first platform designs that the region’s demographic profile demands.

MEA & Latin America AD Network Software Market Insights

The Middle East and Africa and Latin America are growing ad network software markets where rising digital media consumption, expanding e-commerce sectors, and the entry of global programmatic platforms seeking frontier growth market commercial reach are creating structured demand beyond the established North American, European, and Asian markets. UAE leads MEA revenues at approximately 32.1% of the regional total through its position as the region’s most digitally sophisticated economy, the concentration of international advertiser marketing operations in Dubai, and the above-average digital advertising investment per capita sustained across retail, automotive, financial services, and travel advertising categories.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its status as Latin America’s most commercially active digital advertising market, whose large social media usage base, growing e-commerce sector, and active programmatic trading infrastructure create the conditions for sustained ad network software market development. Google’s dominant ad network presence, Meta’s social advertising inventory, and performance ad network platforms serving direct response advertisers collectively drive programmatic adoption independently of brand advertising budget cycles.

Market Dynamics

Growth Drivers: Rising programmatic advertising adoption, AI-powered campaign optimisation, and mobile and connected TV inventory expansion driving global ad network software demand

The structural shift of digital advertising spend toward programmatic automation is the primary commercial driver, as both large enterprise advertisers seeking campaign efficiency and SMEs gaining first-time access to sophisticated audience targeting through self-serve platforms collectively expand the addressable market. AI integration is simultaneously expanding what ad network software can deliver, with machine learning-powered bidding algorithms, generative AI creative optimisation, and predictive audience modelling each improving campaign performance outcomes relative to manually configured alternatives in ways that create durable commercial value justifying platform subscription.

The connected TV and mobile advertising growth vectors are adding substantial new programmatic inventory categories that create additional ad network software deployment opportunities with commercial economics superior to traditional web display formats whose viewability and engagement metrics have plateaued. Each new CTV or mobile app inventory unit entering the programmatic marketplace creates incremental auction volume that sustains the real-time bidding infrastructure demand that ad network software serves, independently of any growth in overall advertiser spending levels.

Restraints: Third-party cookie deprecation disrupting audience targeting infrastructure, ad fraud reducing campaign ROI confidence, and data privacy regulation adding compliance complexity

The deprecation of third-party cookie tracking across major browsers is disrupting the audience targeting data infrastructure that the majority of programmatic ad network platforms were built upon, requiring substantial investment in privacy-preserving alternative technologies including contextual targeting, first-party data integration, universal identity solutions, and clean room data collaboration infrastructure whose development timelines are creating commercial uncertainty for both platform providers and their advertiser and publisher customers during the transition period.

Ad fraud remains a persistent restraint, as invalid traffic, click fraud, domain spoofing, and ad stacking collectively divert an estimated 22% of programmatic advertising spend toward fraudulent inventory, compelling ongoing investment in traffic quality verification and fraud detection technology that adds operational cost without directly generating advertiser audience reach. The cumulative compliance cost of GDPR, CCPA, and emerging state and national data privacy regulations adds legal overhead that smaller ad network software vendors struggle to sustain alongside competitive feature development.

Opportunities: Retail media network programmatic expansion, AI-generated creative automation, and emerging market mobile advertising growth creating new revenue development

Retail media networks represent the most commercially significant near-term opportunity expansion, as major retailers’ first-party purchase data advantages over general-purpose programmatic platforms are attracting brand advertising budgets whose scale is transforming retail media into a USD 150 billion global market whose programmatic trading infrastructure requirements create substantial ad network software demand from both the retailers building network capabilities and the technology vendors supplying the underlying platforms.

The integration of generative AI into ad creative automation is creating a new functional category within ad network software that enables platforms to generate, test, and optimise creative variants automatically across audience segments, adding creative production efficiency to the bidding and targeting automation that has historically defined programmatic’s value proposition. Emerging market mobile advertising growth in Southeast Asia, India, and Latin America is simultaneously creating first-time programmatic adoption demand that expands the global addressable market.

Recent Developments:

-

2025: Equativ fully integrated Sharethrough into its unified operations and brand in 2025, creating an independent end-to-end media platform combining Equativ’s supply-side technology with Sharethrough’s high-attention native and CTV advertising formats that expanded Equativ’s publisher reach and advertiser audience quality capabilities across North American and European programmatic markets following the 2024 acquisition.

-

2025: Equativ launched Maestro by Equativ in January 2025, an AI-powered programmatic platform developed following feedback from over 500 clients that automates campaign optimisation, audience segmentation, and inventory allocation through machine learning algorithms designed to improve publisher yield and advertiser performance simultaneously within a single independent platform architecture.

-

2024: Google Ads launched its Ads Power Pair initiative in early 2024, combining Search and Performance Max AI-powered tools to enhance campaign bidding strategy and audience reach across Google’s owned and operated advertising inventory, demonstrating the largest platform’s commercial direction toward increasingly automated, AI-directed campaign management that reduces dependency on manual advertiser configuration.

AD Network Software Market Key Players

-

Google LLC (Google AdSense, Google Ad Manager)

-

Amazon Publisher Services

-

AppLovin Corporation

-

InMobi Group

-

Equativ (formerly Smart AdServer)

-

PubMatic Inc.

-

Smaato Inc.

-

Criteo S.A.

-

Media.net (Miteno Communication Technology)

-

Sharethrough Inc. (Equativ)

-

SmartyAds SSP

-

Magnite Inc.

-

CJ Affiliate (Publicis Groupe)

-

MaxBounty Inc.

-

Tradedoubler AB

-

Digital Media Solutions Inc.

-

AdColony (Digital Turbine)

-

Verizon Media (Yahoo Advertising)

-

TripleLift Inc.

-

MoPub (Twitter/X)

AD Network Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.33 Billion |

| Market Size by 2035 | USD 6.63 Billion |

| CAGR | CAGR of 11.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Programmatic Ad Networks, Performance Ad Networks, Display Ad Networks, Mobile Ad Networks, Video Ad Networks, Others) • By Deployment (Cloud-Based, On-Premises) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End User (Retail & E-commerce, Media & Entertainment, BFSI, Healthcare, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Google LLC (Google AdSense, Google Ad Manager), Amazon Publisher Services, AppLovin Corporation, InMobi Group, Equativ (formerly Smart AdServer), PubMatic Inc., Smaato Inc., Criteo S.A., Media.net (Miteno Communication Technology), Sharethrough Inc. (Equativ), SmartyAds SSP, Magnite Inc., CJ Affiliate (Publicis Groupe), MaxBounty Inc., Tradedoubler AB, Digital Media Solutions Inc., AdColony (Digital Turbine), Verizon Media (Yahoo Advertising), TripleLift Inc., MoPub (Twitter/X) |

Frequently Asked Questions

The AD Network Software Market is expected to grow at a CAGR of 11.13% from 2026 to 2035.

The AD Network Software Market was valued at USD 2.33 Billion in 2025.

Ans: Key growth is driven by rising programmatic advertising, increasing demand for personalized ads, and mobile-video ad expansion across digital platforms.

Programmatic Ad Networks dominated with approximately 69% of revenues in 2024 and are also the fastest-growing segment at a CAGR of 11.71% through 2035.

North America dominated the AD Network Software Market in 2025, holding approximately 42% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch