Wearable Devices Supporting Line-of-Business Applications Market Report Scope & Overview:

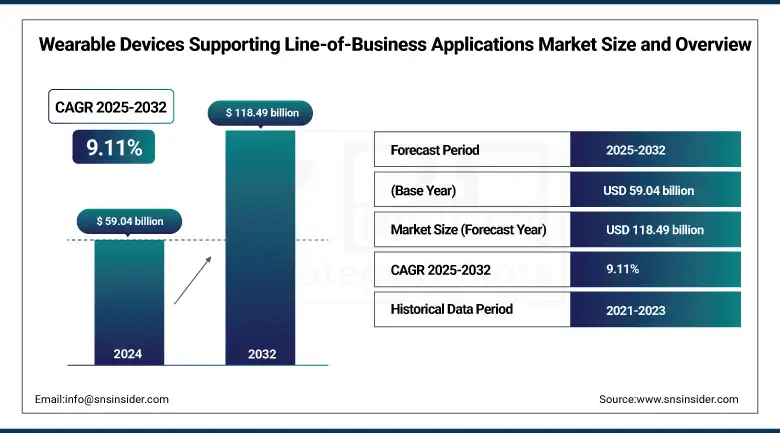

The Wearable Devices Supporting Line-of-Business Applications market size was valued at USD 59.04 billion in 2024 and is expected to reach USD 118.49 billion by 2032, expanding at a CAGR of 9.11% over the forecast period of 2025-2032.

Wearable Devices Supporting Line-of-Business Applications Market is expanding at a significant pace due to the rising adoption in the industry to enable smartwatches, fitness trackers, smart glasses, and health monitors. Products including these enable productivity, employee safety, and real-time data access in wearable devices supporting line-of-business applications market industry, such as healthcare, manufacturing, logistics, or construction. With support for wireless technologies, such as Bluetooth, Wi-Fi, cellular, and NFC, and cloud-based deployments, the RP-500 is designed for seamless integration and scalability. Americas dominates the market, the U.S. is the driving market, and APAC is the fastest growing, with the most opportunities. Main wearable devices supporting the line-of-business applications market companies, such as Apple, Samsung, Alphabet, Garmin, and Xiaomi continue to drive innovation as organizations move to insert wearables into the heart of their business in a way that is much more present and unique than in the past.

According to research, organizations using wearable devices have reported up to an 8.5% boost in workforce productivity, a 7.2% drop in operational errors, and a 30% reduction in workplace incidents, while asset-tracking wearables have cut inventory losses by up to 27%.

To Get more information On Wearable Devices Supporting Line-of-Business Applications Market - Request Free Sample Report

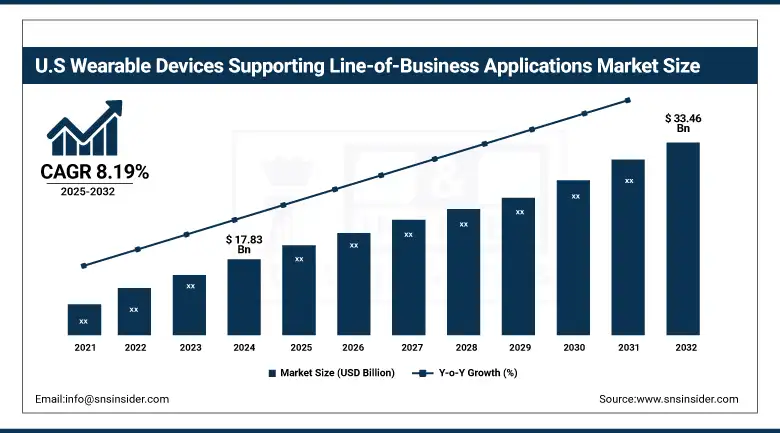

The U.S Wearable Devices Supporting Line-of-Business Applications market size reached USD 17.83 billion in 2024 and is expected to reach USD 33.46 billion in 2032 at a CAGR of 8.19% from 2025 to 2032.

The U.S. market is dominant due to the presence of a large number of technological firms, a high acceptance rate of enterprises for deploying these devices, and a number of big players, such as Apple, Alphabet, and Qualcomm. Wearables in the jobs industry, 67 American companies in healthcare, manufacturing, and logistics are embracing wearables for workforce surveillance, OSHA compliance, and operational efficiency. The country's advanced cloud infrastructure, high connectivity penetration, and government backing accelerate adoption. Coupled with big bets on R&D and early adoption of new technologies, the U.S. remains at the forefront of enterprise wearables and will drive share and growth in the coming years.

Market Dynamics:

Drivers:

-

Increasing Integration of Wearables to Improve Workforce Efficiency and Safety Across Industrial Sectors

The growing demand for real-time tracking, efficiency improvement, and safety adherence is encouraging the deployment of corporate wearable devices. Smartwatches, smart glasses, and health monitors are being put to use in sectors from manufacturing and healthcare to logistics and construction, to track employee activity, maintain safety standards, and facilitate the smooth running of operations. Such solutions contribute to minimizing operational downtime, improving decision-making, and providing the ability to manage a remote workforce. A significant trend is the use of AI and IoT in wearables, delivering predictive analytics and automating data-driven actions. More recently, wearable hardware vendors have teamed with industrial software companies to make it easier to integrate with ERP systems and cloud services.

According to research, organizations using smart wearables for safety compliance and remote monitoring have achieved a 30–40% drop in workplace accidents and up to 25% savings in field management costs across key industries.

Restraints:

-

Data Privacy and Security Concerns Limit the Full-Scale Adoption of Enterprise Wearable Technologies

Despite their advantages, wearable devices face significant concerns related to data security and employee privacy. The constant collection of personal and operational data poses risks of data breaches and non-compliance with data protection laws, such as GDPR and HIPAA. Enterprises are cautious about adopting these devices due to legal implications and employee resistance. The lack of standardized security protocols and end-to-end encryption across wearable platforms exacerbates these concerns. Recent incidents of data leaks from fitness apps and wearable platforms have heightened regulatory scrutiny and emphasized the need for stricter governance frameworks before broader enterprise adoption can be realized.

Opportunities:

-

Growing Use of Wearables in Healthcare for Remote Patient Monitoring and Clinical Workflow Optimization Creates Market Potential

A major growth opportunity lies in the expanding use of wearable devices in clinical environments. Healthcare providers are increasingly relying on wearables for remote patient monitoring, chronic disease management, and real-time vitals tracking, which helps reduce hospital readmissions and improve patient outcomes. Integration with EHR systems and telehealth platforms is also enabling streamlined clinical workflows. Recent wearable devices supporting line-of-business applications market trend include the FDA’s support for medical-grade wearables and investment by hospital networks in enterprise wearables. Companies including Apple and Alphabet are enhancing their healthcare-focused wearable capabilities, signaling a promising future for clinical adoption beyond consumer fitness use.

Challenges:

-

Lack of Standardization in Wearable Device Platforms Hampers Interoperability Across Enterprise Systems

A persistent challenge in the market is the absence of standardization across wearable platforms, which limits interoperability with enterprise applications such as ERP, CRM, and HRM systems. Many devices operate on proprietary software, complicating integration and increasing costs for customization. This fragmentation creates barriers for large-scale deployment and reduces scalability. Enterprises struggle to maintain consistent performance and data accuracy when managing diverse wearable ecosystems. Recent feedback from enterprise IT leaders highlights integration complexity as a top concern when evaluating wearable investments. Efforts are ongoing to develop universal APIs and industry-wide standards, but full harmonization remains a long-term hurdle.

Segment Analysis:

By Device Type

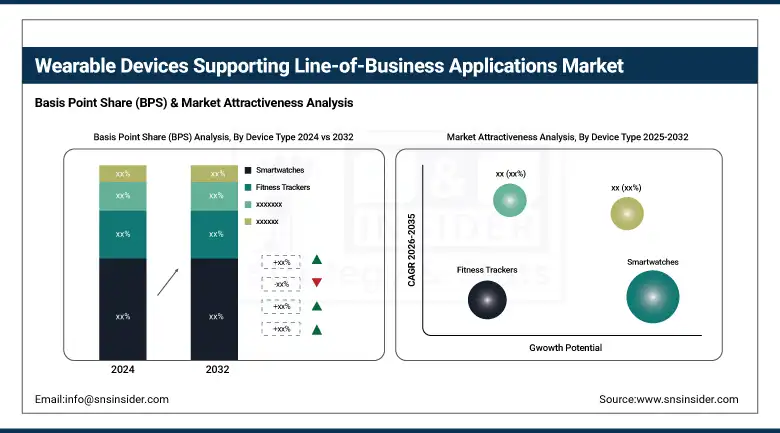

Smartwatches dominate the device type segment, accounting for 41.36% of revenue in 2024, driven by their multifunctionality in workforce productivity, real-time communication, and health monitoring. Enterprises across sectors use smartwatches for tracking employee movement, scheduling tasks, and ensuring safety compliance. Apple’s continued updates to its Apple Watch Series with enhanced biometric sensors and Samsung’s Galaxy Watch integrations with business management platforms exemplify ongoing innovation. These devices' ability to integrate seamlessly with enterprise systems through apps and APIs enhances workflow efficiency. The surge in remote workforces and health-centric workplace policies fuels demand, making smartwatches integral to enterprise wearable strategies.

Fitness trackers are experiencing the fastest CAGR at 10.14%, owing to their cost-effectiveness, ease of use, and growing deployment in health-centric enterprises. These devices are increasingly used in labor-intensive industries for monitoring employee wellness, fatigue levels, and physical exertion. Companies including Fitbit (under Alphabet) and Xiaomi have launched enterprise-focused trackers with extended battery life and enhanced health insights. Garmin's workplace wellness solutions are also gaining traction. The growing focus on occupational health and the integration of fitness trackers with workforce analytics tools are driving this segment’s rapid growth within the Wearable Devices Supporting Line-of-Business Applications Market.

By End-User Industry

Healthcare leads among end-user industries with a 35.72% revenue share in 2024 due to the rising deployment of wearables in clinical settings. Devices like smartwatches and health monitors are used for real-time vital monitoring, chronic condition management, and post-operative care. Apple and Fitbit have expanded their ECG and SpO2 monitoring capabilities, gaining interest from hospital networks and digital health platforms. The push for remote patient monitoring and value-based care drives this growth. Additionally, partnerships between wearable manufacturers and EHR vendors facilitate seamless health data integration, making wearables critical in modern healthcare delivery models.

The logistics and supply chain segment is growing at the fastest CAGR of 10.53%, propelled by the need for real-time tracking, hands-free communication, and workforce safety. Wearable devices including smart glasses and GPS-enabled smartwatches are being deployed to monitor driver health, optimize routes, and reduce downtime. Zebra Technologies and RealWear have launched rugged wearables tailored to logistics environments. The growing e-commerce and global supply chain complexities demand continuous data flow and operational visibility, making wearable integration vital for boosting productivity and minimizing human error across logistics operations.

By Application Area

Health and safety compliance is the leading application, holding a 39.29% share in 2024, fueled by stringent workplace safety regulations and increased emphasis on employee well-being. Wearables including heart rate monitors and smart helmets help detect fatigue, environmental hazards, and physiological stress in real-time. Companies, such as Kenzen and StrongArm Tech have launched wearables that proactively alert users and supervisors to potential health risks. These applications are particularly prevalent in industries including construction and manufacturing. The rising regulatory pressure and growing employer liability concerns make health and safety a cornerstone in enterprise wearable adoption.

Asset tracking is expanding at a CAGR of 10.53%, driven by the increasing use of wearable technology for equipment monitoring and location-based services. Devices embedded with RFID and GPS functionalities help track inventory and tools in real-time, reducing loss and improving asset utilization. Companies, such as Ubimax and ProGlove are innovating in smart gloves and AR wearables for inventory management. The growth of Industry 4.0 and the demand for automation in asset-intensive sectors, such as logistics and field services are significant drivers, as businesses seek to minimize errors and optimize asset visibility through wearable integration.

By Connectivity Technology

Bluetooth holds the largest market share at 49.27% due to its widespread compatibility, low power consumption, and ease of deployment. Most enterprise wearables utilize Bluetooth for data transfer between devices and mobile/desktop platforms. Recent enhancements in Bluetooth Low Energy (BLE) have extended battery life and improved data transmission speed. Companies including Qualcomm and Nordic Semiconductor continue to enhance Bluetooth chipsets for enterprise-grade wearables. As wearables require continuous communication with management systems and smartphones, Bluetooth’s reliability and cost-effectiveness make it the default connectivity standard in enterprise deployments.

NFC is growing at the fastest CAGR of 10.87%, largely driven by its secure, contactless capabilities ideal for payment authentication and access control in enterprises. NFC-enabled wearables allow employees to enter secure zones, track attendance, or authorize transactions seamlessly. Companies, such as Sony and NXP Semiconductors are embedding advanced NFC features into wearable chips, while Apple’s recent enhancements in Apple Watch NFC capabilities highlight the trend. The adoption of contactless technologies post-COVID and the integration of wearables into enterprise security systems are propelling NFC adoption across sectors such as retail, healthcare, and finance.

By Deployment Type

Cloud-based deployment dominates with 28.48% revenue share in 2024, driven by scalability, accessibility, and centralized data management. Cloud platforms allow real-time data sync across devices and analytics dashboards, making them ideal for large-scale enterprises. Companies including Microsoft Azure and AWS offer wearable-compatible cloud services, while Fitbit’s enterprise health solutions are integrated with Google Cloud. With the increasing reliance on real-time health, location, and performance data, cloud-based models provide the flexibility and computational power enterprises need to maximize the ROI of wearable technologies.

Hybrid deployment is the fastest-growing segment with a CAGR of 10.51%, as it offers a balance between on-premises control and cloud scalability. Enterprises with stringent data regulations or latency concerns prefer hybrid models to safeguard sensitive data locally while leveraging cloud-based analytics. Companies, such as IBM and Cisco are developing hybrid cloud environments tailored to wearable integration. The trend is especially relevant in sectors including healthcare and defense, where data privacy is critical. Hybrid deployments enable customized configurations, ensuring compliance without compromising on the functionality or responsiveness of wearable systems.

Regional Analysis:

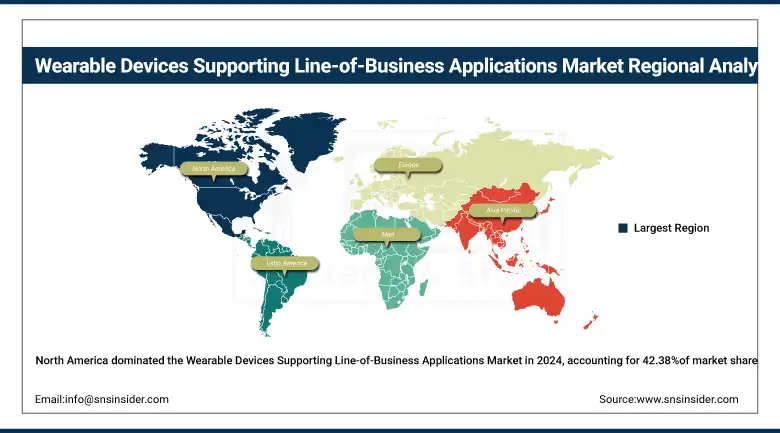

North America dominates the wearable devices supporting line-of-business applications market share of 42.38% in 2024. The region benefits from early technology adoption, strong investments in digital transformation, and mature infrastructure supporting IoT and connected devices. High demand for productivity, health monitoring, and safety compliance tools in industries including healthcare and logistics continues to boost adoption across enterprises. The U.S. leads the region due to its advanced technology landscape, significant R&D spending, and widespread use of enterprise wearables in critical sectors, such as healthcare, manufacturing, and field services.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe holds a substantial share of the market, driven by increasing emphasis on worker safety, stringent regulatory standards, and digital innovation in key industries, such as logistics and manufacturing. Enterprises are increasingly deploying wearables for health monitoring, compliance, and real-time performance tracking. Germany stands as the leading country in Europe, attributed to its industrial strength, focus on smart manufacturing (Industry 4.0), and integration of wearable technologies into production and workforce management systems.

Asia Pacific is the fastest-growing region, with a projected growth rate of 20.62% CAGR over 2025-2032. This growth is driven by industrial expansion, strong government support for digitalization, and a growing demand for cost-efficient wearable solutions across sectors like logistics, healthcare, and field services. China dominates the region due to its vast manufacturing ecosystem, significant investment in enterprise IoT, and leadership in wearable device production and deployment across industries.

The Middle East & Africa and Latin America regions are witnessing steady growth in enterprise wearable adoption, driven by demand in hazardous industries, healthcare, and logistics. Government-backed digital initiatives in the UAE and Brazil's industrial and health-tech expansion support early adoption. Growing safety awareness and mobile infrastructure also contribute to wearable devices supporting the line-of-business applications wearable devices supporting line-of-business applications market growth across both regions.

Key Players:

The major key players operating in the Wearable Devices Supporting Line-of-Business Applications Market are Apple Inc., Samsung Electronics Co., Ltd., Alphabet Inc. (via Google and Fitbit), Garmin Ltd., Xiaomi Corporation, LG Electronics Inc., Sony Corporation, Qualcomm Technologies, Inc., Fitbit Inc. (now part of Google/Alphabet), Adidas AG, and others.

Key Developments:

-

In June 2025, Samsung Electronics unveiled the Galaxy Ring, Galaxy Watch7, and Galaxy Watch Ultra, integrating Galaxy AI for enhanced health monitoring features such as sleep tracking, Energy Scores, and advanced wellness insights.

-

In April 2025, Xiaomi emerged as the global leader in wearable bands, shipping 8.7 million units in Q1 2025 a 44% YoY growth driven by its HyperOS integration, continuous product innovation, and strong market demand.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 59.04 Billion |

| Market Size by 2032 | USD 118.49 Billion |

| CAGR | CAGR of 9.11% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Device Type (Smartwatches, Fitness Trackers, Smart Glasses, Health Monitors, Wearable Payment Devices) •By End User Industry (Healthcare, Manufacturing, Retail, Logistics and Supply Chain, Construction) •By Application Area (Employee Monitoring, Health and Safety Compliance, Asset Tracking, Field Service Management, Business Process Optimization) •By Connectivity Technology (Bluetooth, Wi-Fi, Cellular, NFC (Near Field Communication), RFID (Radio Frequency Identification)) •By Deployment Type (On-Premises Deployment, Cloud-Based Deployment, Hybrid Deployment) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Apple Inc., Samsung Electronics Co., Ltd., Alphabet Inc. (via Google and Fitbit), Garmin Ltd., Xiaomi Corporation, LG Electronics Inc., Sony Corporation, Qualcomm Technologies, Inc., Fitbit Inc. (now part of Google/Alphabet), Adidas AG |

Frequently Asked Questions

Ans: North America dominated the market in 2024 with a 42.38% share, driven by strong digital infrastructure, early adoption of enterprise wearables, and significant R&D investment in technologies, such as IoT and cloud computing.

Ans: Smartwatches dominated the device type segment, accounting for 41.36% of the market revenue in 2024, due to their multifunctionality in health monitoring, task management, and seamless enterprise system integration.

Ans: A key growth driver is the increasing integration of wearable technologies to improve workforce productivity, safety, and real-time decision-making, particularly through AI and IoT-enabled functionalities across industrial sectors.

Ans: The market was valued at USD 59.04 billion in 2024, reflecting strong enterprise adoption and demand for connected workforce technologies.

Ans: The market is expected to expand at a CAGR of 9.11% during the forecast period over 2025-2032, supported by innovations in wearable devices, rising safety standards, and increased demand for real-time operational visibility.

Get in Touch