Aerospace and Defense Electronic Manufacturing Services Market Report Scope & Overview:

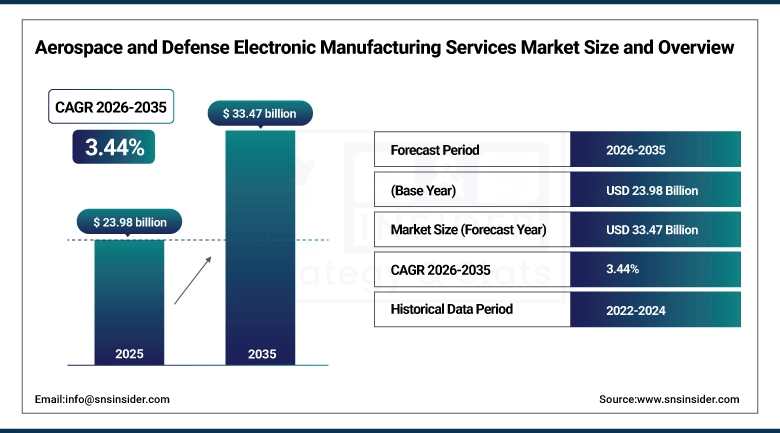

The Aerospace and Defense Electronic Manufacturing Services Market was valued at USD 23.98 billion in 2025 and is expected to reach USD 33.47 billion by 2035, growing at a CAGR of 3.44% from 2026-2035.

The Aerospace and Defense Electronic Manufacturing Services Market is growing due to the rising demand for advanced avionics, UAVs, satellites, and defense electronics. The increase in commercial air deliveries, military modernization, and outsourcing of complex PCB assemblies, integration, and testing services contribute to the growth of this market. The advancement in technology, incorporation of AI, IoT, and investments in defense and space sectors across the globe contribute to the growth of this industry.

AeroVironment, Inc. acquired an aerospace engineering firm, ESAero, in an approximately $200 million deal, which enhances the company's capabilities in unmanned aircraft and defense electronics in response to growing global demand, which is a key driver in electronics manufacturing and integration services.

Aerospace and Defense Electronic Manufacturing Services Market Size and Forecast

-

Market Size in 2025: USD 23.98 Billion

-

Market Size by 2035: USD 33.47 Billion

-

CAGR: 3.44% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Aerospace and Defense Electronic Manufacturing Services Market - Request Free Sample Report

Aerospace and Defense Electronic Manufacturing Services Market Trends

-

Rising demand for advanced avionics, communication, and defense electronics is driving the aerospace and defense electronic manufacturing services (EMS) market.

-

Growing adoption of outsourcing for PCB assembly, system integration, and testing is boosting market growth.

-

Expansion of military aircraft, satellites, UAVs, and radar systems is fueling EMS service requirements.

-

Increasing focus on miniaturization, reliability, and high-performance electronic components is shaping adoption trends.

-

Advancements in automation, precision manufacturing, and quality assurance technologies are enhancing production efficiency.

-

Rising defense modernization programs and government contracts are supporting market expansion.

-

Collaborations between EMS providers, OEMs, and defense contractors are accelerating innovation and global adoption.

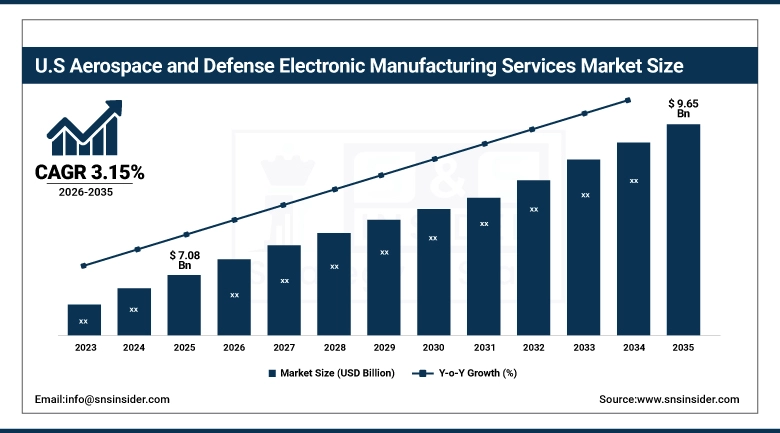

U.S. Aerospace and Defense Electronic Manufacturing Services Market was valued at USD 7.08 billion in 2025 and is expected to reach USD 9.65 billion by 2035, growing at a CAGR of 3.15% from 2026-2035.

The US Aerospace & Defense Electronic Manufacturing Services Market is growing with increasing defense modernization, commercial aircraft production, adoption of sophisticated electronic systems, UAVs, and outsourcing of complex electronic assembly, integration, and testing services by original equipment manufacturers and defense contractors.

Aerospace and Defense Electronic Manufacturing Services Market Growth Drivers:

-

Rapid expansion of aerospace production and complex supply chains is encouraging growth of EMS providers globally across multiple applications

The constant increase in the delivery of commercial airplanes, upgrading military airplanes, and the increase in satellite launches are contributing to the growth in demand for EMS services. Original Equipment Manufacturers (OEMs) are increasingly depending on EMS providers to carry out PCB assemblies, cabling, and harnessing due to the complexity and cost efficiency. The increase in demand for automation, miniaturization, and high-performance electronic components in aerospace systems is also contributing to the growth in EMS demand. The complex supply chain and precision manufacturing require EMS partnerships, which is contributing to the growth in the industry, thus enhancing the EMS networks across the globe.

In 2025, Airbus delivered 793 commercial aircraft, up from 766 in 2024, and is targeting an even higher delivery rate in 2026, reflecting strong OEM production momentum.

Boeing is increasing production, planning about 500 aircraft deliveries in 2026, including ramped-up 737 MAX output amid ongoing supply chain challenges indicating growing production rates for commercial aviation platforms and reinforcing EMS demand globally.

Aerospace and Defense Electronic Manufacturing Services Market Restraints:

-

Stringent regulatory compliance and defense security protocols pose challenges for widespread EMS service implementation across regions

Aerospace and defense sector EMS companies face the challenge of adhering to government and military regulations that are quite stringent in terms of security of information, export control regulations, and component traceability. Companies face operational complexities in adhering to regulations such as those under the US government's ITAR and EAR regulations, as well as defense compliance regulations across the world. Non-adherence to these regulations can result in penalties that limit business opportunities through contract restrictions and access to clients. There is also a need for rigorous auditing to obtain certifications for defense electronics manufacturing services, causing market entry to be delayed.

Aerospace and Defense Electronic Manufacturing Services Market Opportunities:

-

Integration of AI, IoT, and advanced electronics in aerospace platforms is driving significant EMS business expansion worldwide

The aerospace and defense industry is increasingly using smart electronics, IoT technology, and AI technology in their avionic systems. Therefore, there is a high requirement for complex EMS capabilities. The latest aircraft, defense vehicles, and space technology require high-precision PCBs, microelectronic devices, and sensors. EMS companies can leverage this opportunity by providing value-added services in testing, calibration, and integration. Industry 4.0 technology also increases the efficiency, reliability, and customization capabilities of EMS companies. These technological developments provide opportunities for EMS companies to work in partnership with OEMs and defense contractors in the latest aerospace electronics, which can be used in both commercial and military applications.

Integration of AI, IoT, and Advanced Electronics in Aerospace Platforms

|

Platform |

Detailed Integration |

|

Boeing 737 MAX & 787 Dreamliner |

AI-enabled flight control systems that optimize aircraft handling, predictive maintenance sensors monitoring engine and system health in real time, and IoT connectivity for continuous data exchange with ground systems and airline operations. |

|

Lockheed Martin F-35 Lightning II |

Advanced avionics suite integrating radar systems, electronic warfare capabilities, multi-sensor fusion, and AI-assisted threat detection to support autonomous mission functions and real-time battlefield awareness. |

|

Airbus A350 XWB |

IoT-enabled systems for fuel efficiency optimization, predictive diagnostics of onboard systems, adaptive environmental controls, and real-time data monitoring for operational efficiency and sustainability. |

|

Northrop Grumman MQ-9 Reaper UAV |

AI-based autonomous navigation systems, IoT-enabled telemetry for live mission data transfer, and integration of advanced sensor payloads for surveillance, reconnaissance, and intelligence operations. |

|

European Space Agency Satellites |

AI-assisted onboard processing for Earth observation, IoT-based communication modules for satellite networking, and high-performance sensor electronics for data acquisition, environmental monitoring, and system reliability in space. |

Aerospace and Defense Electronic Manufacturing Services Market Segment Highlights

-

By Service Type, PCB Assembly Services dominated the Aerospace and Defense Electronic Manufacturing Services Market with ~28% share in 2025; System Integration Services fastest growing (CAGR).

-

By End-Users, Commercial dominated the Aerospace and Defense Electronic Manufacturing Services Market with ~44% share in 2025; Military fastest growing (CAGR).

-

By Component Type, Microelectronics dominated the Aerospace and Defense Electronic Manufacturing Services Market with ~28% share in 2025; Semiconductors fastest growing (CAGR).

-

By Application, Aero Structure dominated the Aerospace and Defense Electronic Manufacturing Services Market with ~34% share in 2025; Satellites fastest growing (CAGR).

-

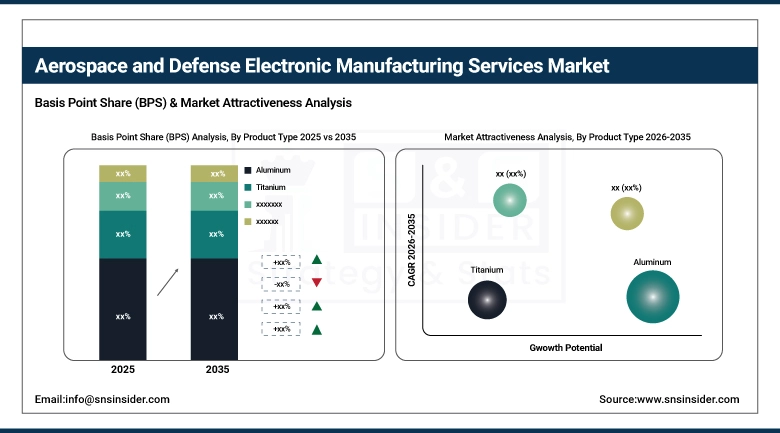

By Product Type, Aluminum dominated the Aerospace and Defense Electronic Manufacturing Services Market with ~28% share in 2025; Composites fastest growing (CAGR).

Aerospace and Defense Electronic Manufacturing Services Market Segment Analysis

By Product Type, Aluminum segment dominates the Market, Composites segment expected to grow fastest

The aluminum segment accounted for the highest share of the Aerospace and Defense Electronic Manufacturing Services Market in 2025. This is due to the fact that aluminum-based components are highly used in aircraft structures, avionic components, and defense electronic enclosures. This material is highly durable, cost-effective, and can be easily integrated into electronic components.

The composites segment is expected to witness the highest growth rate during the period of 2026-2035. This growth can be attributed to the increasing use of composite materials in the latest aircraft, UAVs, and space vehicles. Composite materials have a high strength-to-weight ratio, corrosion resistance, and design flexibility, which are beneficial for the integration of electronic components, thus increasing the growth of the electronic manufacturing services industry.

By Service Type, PCB Assembly Services segment dominates the Market, System Integration Services segment expected to grow fastest

PCB Assembly Services segment held the largest share of the Aerospace and Defense Electronic Manufacturing Services Market in 2025, driven by the high demand for precision electronics used in aircraft and defense systems. The need for complex electronics, including radar systems, electronic warfare systems, and sophisticated avionics, has increased the demand for PCB Assembly Services, which has become a major contributor of revenues for EMS providers globally.

System Integration Services segment of the Aerospace and Defense Electronic Manufacturing Services Market will register the fastest CAGR during the forecast period of 2026-2035, driven by the growing demand for sophisticated electronics, including IoT-enabled systems, AI-based electronics, and sophisticated avionics, which are being increasingly used in aerospace and defense systems.

By End-Users, Commercial segment dominates the Market, Military segment expected to grow fastest

Commercial segment accounted for the largest share in the Aerospace and Defense Electronic Manufacturing Services market in 2025. The segment is driven by the requirement for high-quality avionics, cabin, and communication systems in the rising deliveries of new aircraft. The OEMs prefer EMS companies for the assembly and testing of their products due to efficiency, precision, and cost control, thus providing the highest revenue contribution in the commercial segment of aerospace electronic manufacturing services.

Military segment is expected to grow at the highest CAGR in the range of 2026-2035. The segment is driven by the rising defense modernization programs, fighter aircraft, and UAVs. The requirement for high-quality electronic systems, communication, and electronic warfare equipment is expected to drive the market at a high rate in military applications, thus accelerating the adoption of electronic manufacturing services in defense electronics manufacturing.

By Component Type, Microelectronics segment dominates the Market, Semiconductors segment expected to grow fastest

The microelectronics segment accounted for the largest market share in the Aerospace and Defense Electronic Manufacturing Services Market in 2025. This is because microchips, sensors, and control modules are the most basic components of avionics, satellites, and defense equipment. The increased need for reliable, compact, and performance-critical electronic components will continue to make microelectronics assemblies a significant segment for generating revenues for electronic manufacturing services companies serving the aerospace and defense industries.

The Semiconductors Segment is expected to register the highest CAGR in the Aerospace and Defense Electronic Manufacturing Services Market from 2026 to 2035 due to increasing integration of power management, signal processing, and high-performance computing in Aerospace and Defense Electronics. Increasing demand for compact, efficient, and reliable semiconductor devices in next-generation aircraft, UAVs, and space systems is driving high EMS adoption in semiconductor assembly and testing.

By Application, Aero Structure segment dominates the Market, Satellites segment expected to grow fastest

The Aero Structure segment accounted for the highest share of the Aerospace and Defense Electronic Manufacturing Services Market in 2025. This is because structural electronic systems, such as avionics wiring, control circuits, and electronic systems, are critical to aircraft performance. Therefore, the Aero Structure segment accounts for the highest share of the overall electronic manufacturing services market.

The Satellites segment will have the highest growth rate during the period from 2026 to 2035. This is due to an increase in satellite launches for various purposes, such as communication, surveillance, and defense. Satellite electronic systems have critical requirements for compactness, reliability, and electronic systems. Therefore, there will be a significant growth rate of electronic manufacturing services for satellite electronic systems. This growth will be fueled by an increase in satellite investment worldwide.

Aerospace and Defense Electronic Manufacturing Services Market Regional Analysis

North America Aerospace and Defense Electronic Manufacturing Services Market Insights

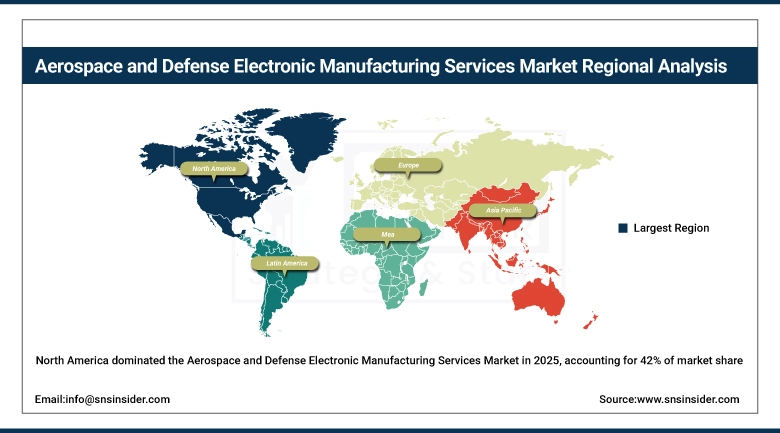

North America held the largest share in the Aerospace and Defense Electronic Manufacturing Services Market in terms of revenue at about 42% in 2025. This is because the region is home to a large number of OEMs and EMS companies in the aerospace and defense sector. The high defense expenditure in the region, coupled with the availability of advanced technology infrastructure and strong demand for aircraft electronics in both the commercial and defense sectors, is also responsible for the high market share held by North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Aerospace and Defense Electronic Manufacturing Services Market Insights

Asia Pacific region is expected to grow with the highest CAGR of 4.86% during 2026-2035 due to increasing aerospace manufacturing activities, defense modernization initiatives, and growth in commercial aviation in countries like China and India. Factors like rapid urbanization, growth in airline fleets, and investments in UAVs, satellites, and avionics electronics contribute to increased EMS demand in this region. New entrants in EMS service providers and favorable government initiatives along with increased outsourcing of complex electronics assembly contribute to this region’s highest growth in the global Aerospace & Defense EMS market.

Europe Aerospace and Defense Electronic Manufacturing Services Market Insights

Europe, in the Aerospace and Defense Electronic Manufacturing Services Market, has a strong position owing to the presence of major aerospace original equipment manufacturers as well as defense contractors. The presence of superior technological infrastructure, high adoption of avionics as well as defense electronics, and strong R&D activities are some of the factors that have helped the region maintain its position, thus contributing positively towards the growth of the Aerospace and Defense Electronic Manufacturing Services Market.

Middle East & Africa and Latin America Aerospace and Defense Electronic Manufacturing Services Market Insights

Middle East & Africa and Latin America in the Aerospace and Defense Electronic Manufacturing Services Market are growing steadily with an increase in defense modernization initiatives, growth in commercial air transportation, and a surge in the demand for sophisticated avionics technology. Government spending, partnerships with international EMS vendors, and the growth in aerospace manufacturing activities contribute to the growth in this industry. The emergence of EMS infrastructure in these regions is another factor contributing to the growth in the industry.

Aerospace and Defense Electronic Manufacturing Services Market Competitive Landscape:

Honeywell International Inc.

Honeywell International Inc., with headquarters in Charlotte, North Carolina, is a technology and manufacturing company with global operations in the aerospace, defense, industrial, and safety markets. The company's aerospace business offers avionics, propulsion, and electronics manufacturing services (EMS) to the defense and commercial air markets. The company is focused on scaling production capacity, supply chain support to flight-critical electronics, and helping to deliver advanced defense capabilities with integrated manufacturing solutions.

-

2026: Honeywell reports robust defense and aviation demand driving expanded production capacity to support aerospace suppliers, reflecting broader EMS support for defense electronics and flight-critical manufacturing segments.

Jabil Inc.

Jabil Inc., a St. Petersburg, Florida-based global electronics manufacturing services (EMS) provider, offers design, engineering, and production capabilities in the aerospace, defense, healthcare, and industrial industries. The EMS capabilities of Jabil include high-reliability electronics manufacturing for flight critical and defense applications, as well as investments in facilities and technology to increase its manufacturing capabilities, efficiency, and supply chain responsiveness in the aerospace and defense industries.

-

2025: Jabil continued investments and manufacturing capacity expansions, including new facilities, to support its broad aerospace and defense EMS capabilities.

Key Players

Some of the Aerospace and Defense Electronic Manufacturing Services Market Companies

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Raytheon Technologies Corporation

-

Thales Group

-

BAE Systems plc

-

Honeywell International Inc.

-

General Dynamics Corporation

-

Airbus SE

-

Boeing Company

-

Jabil Inc.

-

Celestica Inc.

-

Sanmina Corporation

-

Benchmark Electronics, Inc.

-

Plexus Corp.

-

Kimball Electronics, Inc.

-

Creation Technologies LP

-

Integrated Micro‑Electronics, Inc.

-

NEO Tech Inc.

-

Absolute EMS, Inc.

-

Sonic Manufacturing Technologies

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.98 Billion |

| Market Size by 2035 | USD 33.47 Billion |

| CAGR | CAGR of 3.44% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Aluminum, Titanium, Composites, Super Alloys, Steel) • By Application (Aero Structure, Components, Propulsion System, Cabin Interiors, Satellites) • By Service Type (PCB Assembly Services, Cables and Harness Assembly, System Integration Services, Repair, Refurbishment, and Maintenance) • By Component Type (Microelectronics, Semiconductors, Passive Components, Connectors and Cabling, Printed Circuit Boards (PCBs)) • By End-Users (Commercial, Business & General Aviation, Military) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Thales Group, BAE Systems plc, Honeywell International Inc., General Dynamics Corporation, Airbus SE, Boeing Company, Jabil Inc., Celestica Inc., Sanmina Corporation, Benchmark Electronics, Inc., Plexus Corp., Kimball Electronics, Inc., Creation Technologies LP, Integrated Micro‑Electronics, Inc., NEO Tech Inc., Absolute EMS, Inc., Sonic Manufacturing Technologies |

Frequently Asked Questions

North America dominated the Aerospace and Defense Electronic Manufacturing Services Market in 2025.

The Aluminum segment dominated the Aerospace and Defense Electronic Manufacturing Services Market in 2025.

Rapid expansion of aerospace production and complex supply chains is encouraging growth of EMS providers globally across multiple applications.

The Aerospace and Defense Electronic Manufacturing Services Market was valued at USD 23.98 billion in 2025.

The Aerospace and Defense Electronic Manufacturing Services Market is expected to grow at a CAGR of 3.44% from 2026 to 2035.

Get in Touch