Military-grade RF Market Report Scope & Overview:

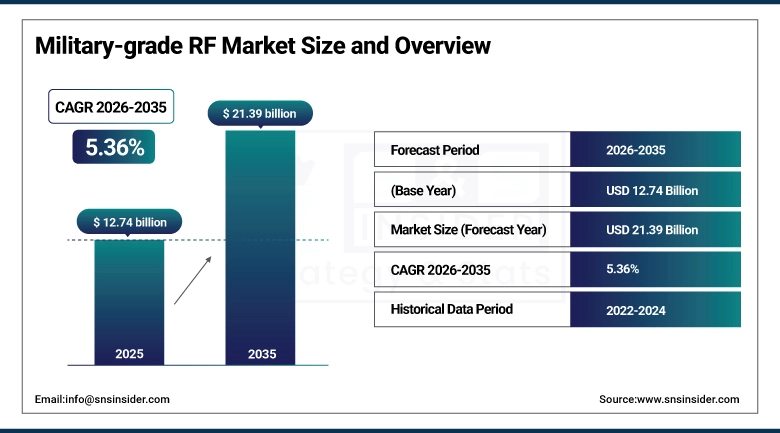

The Military-grade RF Market size was valued at USD 12.74 Billion in 2025 and is projected to reach USD 21.39 Billion by 2035, growing at a CAGR of 5.36% during 2026–2035.

The Military-Grade RF Market is expanding with an increase in global defense spending, military modernization, and the adoption of reliable, high-performance RF communication systems for air, land, and naval military applications. Advances in satellite communications, radar, and millimeter-wave RF technologies, as well as the need for reliable military communications and military modernization, are contributing to the continued growth of the Military-Grade RF Market.

Military-grade RF Market Size and Forecast:

-

Market Size in 2025: USD 12.74 Billion

-

Market Size by 2035: USD 21.39 Billion

-

CAGR: 5.36% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Military-grade RF Market - Request Free Sample Report

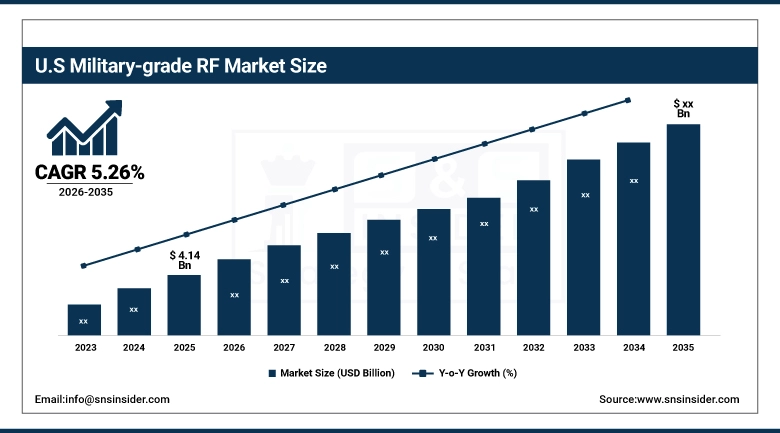

The U.S. Military-grade RF Market was valued at USD 4.14 Billion in 2025 and is growing at a CAGR of 5.26% through 2035. The United States remains the single largest national market, driven by the combination of the largest defense RF procurement budget globally spanning tactical radios, aircraft radar systems, shipboard electronic warfare suites, and satellite communications terminals and the active modernization programs across Army, Navy, Marine Corps, and Air Force platforms that are replacing Cold War-era RF equipment with software-defined radio architectures and electronically-scanned antenna arrays.

Military-grade RF Market Trends:

-

Peer adversary electronic warfare capability particularly China’s and Russia’s demonstrated ability to jam GPS, tactical communications, and radar systems is driving a fundamental reassessment of military RF system design requirements, prioritizing anti-jam performance, frequency agility, and low probability of intercept waveforms over raw throughput.

-

Software-defined radio is the most consequential technology transition in the military tactical communications segment, replacing fixed-function hardware radios with field-programmable platforms that can implement new waveforms through software updates, dramatically extending operational life and adaptability.

-

Proliferation of unmanned aerial vehicles in all military services has created growing RF demand for drone communications datalinks, EW payloads on drone platforms, and counter-UAS detection and jamming systems that all require specialized military-grade RF components.

-

Active electronically scanned arrays (AESA) are displacing mechanically scanned radar antenna systems across aerospace defense platforms, with AESA’s simultaneous multi-beam, rapid beam-steering, and low radar cross-section advantages making it the radar architecture of choice for new fighter aircraft, maritime patrol aircraft, and ground-based air defense systems.

-

Millimeter-wave RF is gaining ground in military applications, particularly for high-bandwidth, short-range tactical communications and sensor systems where the frequency’s limited propagation range is an operational advantage for low probability of intercept requirements.

Military-grade RF Market Drivers:

-

Rising Defense Spending, Advanced RF Technologies, and Geopolitical Tensions Propel Military‑Grade RF Market

The driving factors of the market include an increase in global defense spending, which fuels the demand for military communication systems. The need for communication systems that provide security, high-speed communication, and reliability across air, land, and naval domains will drive the market. The advancements in radar, satellite communication, and millimetre wave RF will also drive the military communication systems market. In addition, geopolitical tensions will drive the military communication systems market.

China maintained a 7.2 % military budget increase in 2025, reaching about USD 246 billion, underscoring heightened investment in defense capabilities amidst strategic competition further pressuring RF communications modernization worldwide

Military-grade RF Market Restraints:

-

High Costs, Integration Complexity, and Regulatory Challenges Restrain Military‑Grade RF Market Growth

The market is challenged by the high cost of developing and procuring sophisticated RF systems. This acts as a barrier to the adoption of such technologies. Furthermore, the complexity of integration of various platforms, which are multi-domain systems, adds to the overall cost of operations. Also, regulatory requirements, spectrum-related problems, and security concerns related to the use of RF-based communication may hinder the growth of the market. Geopolitical factors, as well as the pace of defense modernization programs, may impede the growth of the market.

Military-grade RF Market Opportunities:

-

Adoption of Advanced RF Technologies and Modernization Programs Drive Growth Opportunities in Military‑Grade RF Market

The Military Grade RF Market has tremendous potential to expand in the near future with the adoption of advanced communication technologies such as millimetre wave RF, 5G-based tactical networks, and space-based communication technologies. With the rising modernization trends in emerging defense markets, unmanned and autonomous platforms, and battlefield communications, there exist tremendous potential to expand in the near future. With defense contractors and technology companies joining hands to deliver integrated RF solutions, there exist tremendous potential to expand in the near future.

Satellite communications (SATCOM) continue expanding in military use, with SES securing a ~USD 90 million contract to support U.S. Army space‑based communication infrastructure

Military-grade RF Market Segment Highlights:

-

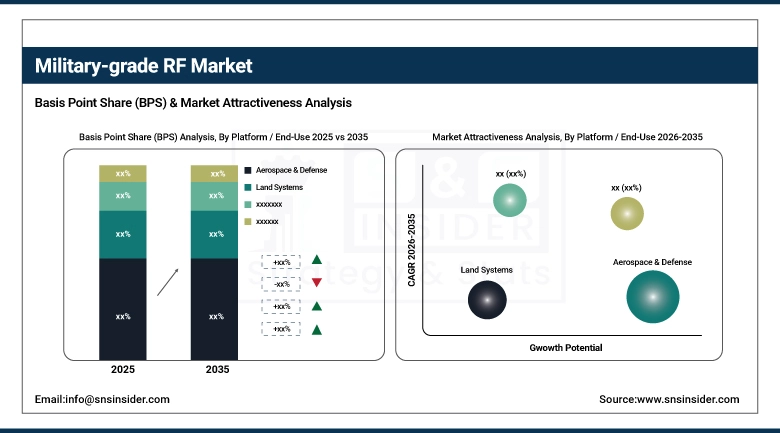

By Platform / End-Use: Dominant – Aerospace & Defense (41.25% in 2025, CAGR 5.24%); Fastest-Growing – Naval Systems (CAGR 5.62%)

-

By Frequency Band / Technology: Dominant – VHF/UHF (32.48% in 2025, CAGR 5.17%); Fastest-Growing – X-Band / Ku-Band / Ka-Band (CAGR 5.65%)

-

By Component Type: Dominant – Transmitters & Receivers (34.72% in 2025, CAGR 5.17%); Fastest-Growing – Antennas & Arrays (CAGR 5.52%)

-

By End-User: Dominant – Armed Forces (52.36% in 2025, CAGR 5.24%); Fastest-Growing – Homeland Security & Border Protection (CAGR 5.66%)

Military-grade RF Market Segment Analysis:

Aerospace & Defense Leads Platforms; Naval Systems Drives Fastest Growth

The Aerospace & Defense segment holds a large market share due to its usage in aircraft, UAVs, and satellite communications. The land systems are also important in armored vehicles and land defense systems. The naval systems are growing very rapidly with increased usage in ships and submarines. The communication and intelligence systems are continuously growing with increased usage in command and control systems.

VHF/UHF Leads Frequency Bands; X-Band / Ku-Band / Ka-Band Drives Fastest Growth

The traditional military communications are based on VHF/UHF frequencies. The L-Band and S-Band are also popular in radar and satellite communication systems. The new frequency bands like X-Band, Ku-Band, and Ka-Band are growing very rapidly with increased usage in satellite communications and missile guidance systems. The new frequency bands are growing very rapidly with increased usage in satellite communications and missile guidance systems. Millimeter waves are also growing very rapidly with increased usage in next-generation secure communication systems.

Transmitters & Receivers Lead Components; Antennas & Arrays Drive Fastest Growth

Transmitters and receivers are at the core of the RF communication system for the military, thereby contributing to market leadership. Antennas and arrays are experiencing rapid adoption due to the growing need for efficient transmission and reception of RF signals. RF amplifiers and filters continue to be crucial for maintaining the quality of RF signals. Modulators and demodulators are gaining significance with the development of advanced waveforms for secure communication for air, land, and naval forces.

Armed Forces Lead End-Users; Homeland Security & Border Protection Drives Fastest Growth

Armed forces continue to be the main users of RF technology, thereby driving the market for various RF technologies. Organizations involved in defense research and development contribute to the growth of RF technology. Homeland security agencies and organizations responsible for protecting borders are experiencing rapid growth in RF technology for secure communication. Defense contractors are critical for the deployment of integrated RF solutions.

Military-grade RF Market Regional Analysis:

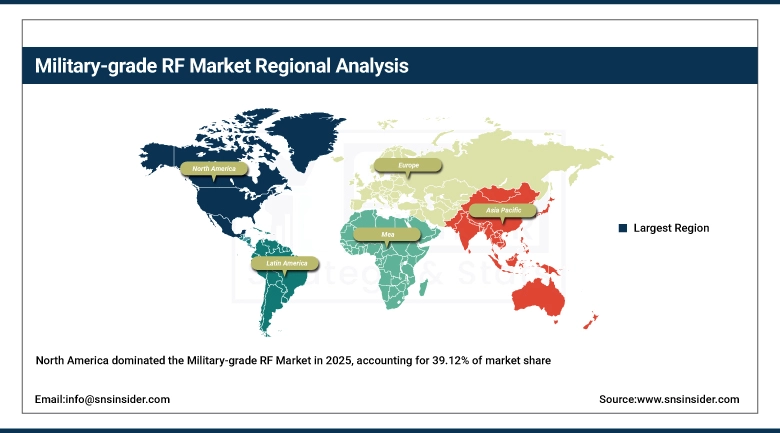

North America Military-grade RF Market Insights

North America dominated in 2025 at USD 4.98 Billion (39.12%), projected to reach USD 8.31 Billion by 2035 at a CAGR of 5.28%. The region’s leadership reflects the scale of U.S. defense RF procurement, the depth of the U.S. defense industrial base in RF manufacturing and system integration, and active modernization programs across all service branches. The F-35 AN/APG-81 AESA radar, the Army’s Integrated Tactical Network radios, and Navy radar replacement programs collectively represent multi-billion dollar RF procurement commitments extending through the 2030s.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Military-grade RF Market Insights

The United States dominates North American military RF demand through the world’s largest defense RF procurement program spanning AESA radar upgrades, software-defined radio fielding across all service branches, and satellite communications terminal modernization, supported by Raytheon, L3Harris, Northrop Grumman, and specialized GaN component manufacturers.

Europe Military-grade RF Market Insights

Europe held a 25.48% share in 2025 at USD 3.25 Billion, growing to USD 5.39 Billion by 2035 at a CAGR of 5.24%. European military RF investment is growing in response to post-2022 defense spending increases. Germany’s Zeitenwende buildup, Poland’s rearmament program, and France’s Rafale radar and electronic warfare modernization are generating sustained procurement demand. The European Defence Fund programs coordinating cross-border investment have also allocated funding to next-generation radar and communications systems.

Germany Military-grade RF Market Insights

Germany leads European military-grade RF investment through its Bundeswehr modernization program, encompassing AESA radar systems for Eurofighter and future combat aircraft, digital tactical communication network upgrades, and electronic warfare system procurement aligned with NATO interoperability requirements.

Asia Pacific Military-grade RF Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 5.55%, rising from USD 3.02 Billion in 2025 to USD 5.16 Billion by 2035. Japan and South Korea are dominant procurement markets, driven by their F-35 fleet expansions and indigenous fighter and destroyer programs incorporating domestic RF technology. India’s defense indigenization programs are generating RF procurement from domestic manufacturers with Bharat Electronics Limited and DRDO leading radar and communications system development.

Japan Military-grade RF Market Insights

Japan leads Asia Pacific military-grade RF investment through its F-35 fleet sustainment, the Mitsubishi F-X program requiring domestic AESA radar development, Aegis destroyer modernization, and the largest Japanese defense budget in postwar history following the 2022 national security strategy revision.

Latin America and Middle East & Africa Military-grade RF Market Insights

Latin America held a 6.03% share in 2025 at USD 0.77 Billion, growing at a CAGR of 5.57% to USD 1.32 Billion by 2035. Brazil leads through its F-39 Gripen fleet acquisition bringing AESA radar requirements and domestic radar development through the SISFRON border monitoring system. Middle East & Africa held a 5.70% share at USD 0.73 Billion, growing at 5.36% CAGR to USD 1.22 Billion by 2035. Saudi Arabia and the UAE lead MEA military RF procurement through active fighter fleet modernizations and regional air defense network expansion. Saudi Arabia leads MEA military RF investment through F-15SA and future fighter radar and electronic warfare modernization, Patriot air defense RF upgrades, and Vision 2030-aligned defense industrialization programs developing domestic RF electronics manufacturing through joint ventures with Western defense primes.

Military-grade RF Market Competitive Landscape:

Raytheon Technologies (RTX)

Raytheon is the world’s largest military radar and missile guidance RF system manufacturer, with its Intelligence & Space and Missiles & Defense divisions producing AESA radar systems for the F-15, F-22, and F/A-18, the SPY-6 family of naval radar systems for U.S. Navy destroyers, and the Patriot PAC-3 radar serving as the primary air and missile defense sensor for the United States and numerous allied militaries. Its internal GaN-on-SiC power amplifier module manufacturing gives it control over the most performance-critical RF component in modern phased array systems.

In February 2025, Raytheon completed delivery of the first AN/SPY-6(V)1 Air and Missile Defense Radar for installation aboard the USS Jack H. Lucas, the first Flight III Arleigh Burke-class destroyer, providing a signal processing capability over 35 times more powerful than the AN/SPY-1D it replaces through a GaN AESA architecture that is now the benchmark for naval RF radar systems.

L3Harris Technologies Inc.

L3Harris is the dominant supplier of military tactical communications RF systems to U.S. and allied armed forces, with its Falcon family of software-defined radios representing the most widely deployed military communications platform in the Western alliance. Its electronic warfare division produces the AN/ALQ-214 integrated defensive countermeasures suite and AN/ALQ-257 Integrated Viper EW Suite, giving it significant RF content on U.S. and allied fighter and bomber platforms.

In January 2025, L3Harris delivered the first production-standard RF-9150A software-defined radios to U.S. Special Operations Command under the Multi-Function Advanced Data Link program, providing SOCOM units with a compact, software-reprogrammable platform supporting satellite communications, beyond-line-of-sight networking, and anti-jam waveforms from a single multi-mission system sized for individual operator carry.

Military-grade RF Market Key Players:

-

Raytheon Technologies

-

Northrop Grumman

-

BAE Systems

-

Lockheed Martin

-

Thales

-

L3Harris Technologies

-

Leonardo

-

Rohde & Schwarz

-

Qorvo

-

Mercury Systems

-

Cobham

-

Elbit Systems

-

Hensoldt

-

Saab

-

Teledyne Technologies

-

General Dynamics

-

Analog Devices

-

Microchip Technology

-

Honeywell

-

Viasat

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.74 Billion |

| Market Size by 2035 | USD 21.39 Billion |

| CAGR | CAGR of 5.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform / End-Use (Aerospace & Defense (Aircraft, UAVs, Satellites), Land Systems (Armored Vehicles, Ground Defense), Naval Systems (Ships, Submarines), and Communication & Intelligence Systems) • By Frequency Band / Technology (VHF/UHF, L-Band / S-Band, X-Band / Ku-Band / Ka-Band, and Millimeter-Wave & Advanced RF) • By Component Type (Transmitters & Receivers, Antennas & Arrays, RF Amplifiers & Filters, and Modulators / Demodulators) • By End-User (Armed Forces (Army, Navy, Air Force), Defense Research & Development Organizations, Homeland Security & Border Protection, and Defense Contractors & System Integrators) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Raytheon Technologies, Northrop Grumman, BAE Systems, Lockheed Martin, Thales, L3Harris Technologies, Leonardo, Rohde & Schwarz, Qorvo, Mercury Systems, Cobham, Elbit Systems, Hensoldt, Saab, Teledyne Technologies, General Dynamics, Analog Devices, Microchip Technology, Honeywell, Viasat. |

Get in Touch