Aerospace and Defense Materials Market Report Scope & Overview:

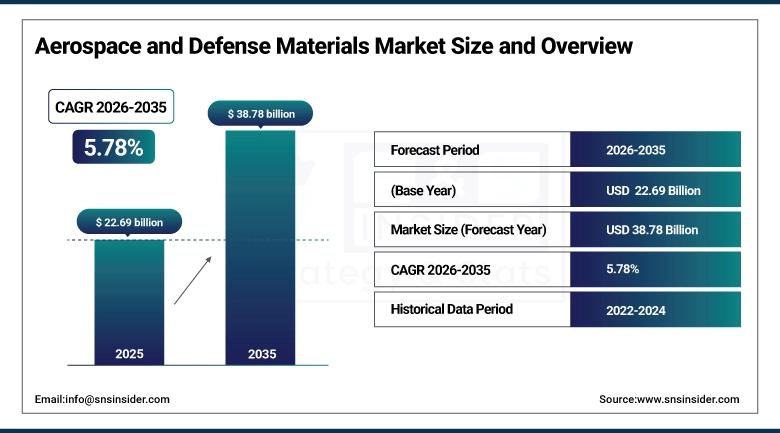

The Aerospace and Defense Materials Market was valued at USD 22.69 Billion in 2025 and is expected to reach USD 38.78 Billion by 2035, growing at a CAGR 5.78% of from 2026-2035.

The Aerospace and Defense Materials Market is witnessing steady growth, driven by rising demand for lightweight, high-strength materials in commercial aircraft, military platforms, and space programs. Increasing defense modernization, expanding global air travel, advancements in composites and titanium alloys, and growing adoption of additive manufacturing are accelerating material innovation. Additionally, sustainability initiatives, fuel-efficiency requirements, and long-term aircraft fleet replacement programs are supporting sustained market expansion across major regions.

In 2025, aerospace and defense materials were utilized across more than 50 countries, enabling aircraft and defense manufacturers to achieve up to 22% weight reduction and 18% improvement in fuel efficiency and operational performance through the adoption of advanced composites, titanium alloys, and high-performance materials across structural and propulsion applications.

Aerospace and Defense Materials Market Report Size and Forecast

-

Market Size in 2025: USD 22.69 Billion

-

Market Size by 2035: USD 38.78 Billion

-

CAGR: 5.78%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Aerospace and Defense Materials Market - Request Free Sample Report

Trends in the Aerospace and Defense Materials Market

-

Integration of advanced composites and lightweight alloys to improve fuel efficiency and structural performance in aerospace and defense platforms.

-

Rising adoption of additive manufacturing and 3D-printed metal components for complex, high-precision aerospace parts.

-

Growing demand for high-temperature and hypersonic-grade materials to support next-generation defense and space systems.

-

Advancements in ceramic matrix composites (CMCs) and titanium alloys for engine, turbine, and propulsion applications.

-

Increased focus on sustainable, recyclable, and low-carbon materials to meet environmental and regulatory requirements.

-

Greater collaboration between OEMs and material suppliers to accelerate material qualification and certification timelines.

U.S. Aerospace and Defense Materials Market Insights:

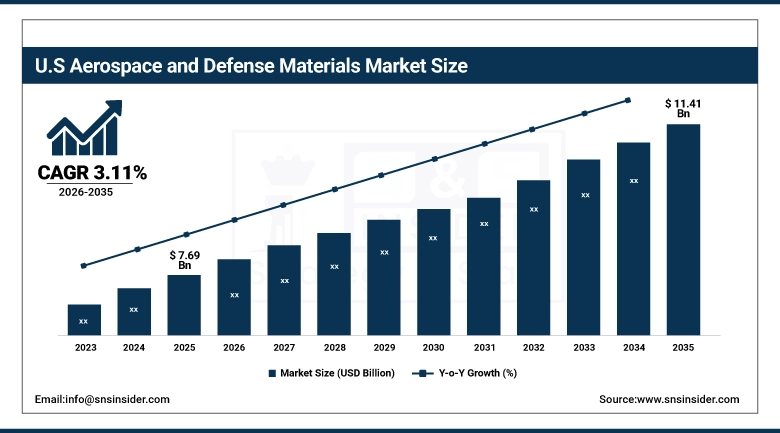

The Aerospace and Defense Materials Market is projected to grow from USD 7.69 Billion in 2025 to USD 11.41 Billion by 2035, at a CAGR of 3.11%. The growth of the U.S. Aerospace and Defense Materials Market is driven by ongoing defense modernization, increased spending on advanced aircraft and space programs, and steady replacement of aging fleets. Strong domestic OEM presence, rising adoption of lightweight composites and titanium alloys, and continuous R&D investment further support long-term market expansion.

Aerospace and Defense Materials Market Growth Drivers:

-

Rising Demand for Lightweight, High-Strength Materials Driving Aerospace Efficiency

The increasing need to improve fuel efficiency, payload capacity, and operational performance in commercial and military aircraft is driving strong demand for lightweight, high-strength materials such as advanced composites, aluminum alloys, and titanium. Aircraft manufacturers are increasingly replacing traditional steel components with composite airframes and next-generation alloys to meet stringent performance and emission standards. These materials enable reduced aircraft weight, improved durability, and enhanced corrosion resistance, making them critical for next-generation aerospace platforms.

Modern composite-intensive aircraft such as the Boeing 787 and Airbus A350 use over 50% composite materials by weight, achieving 20% lower fuel burn compared to previous-generation aircraft.

Aerospace and Defense Materials Market Restraints:

-

High Material Costs and Complex Certification Processes Limiting Adoption

Advanced aerospace materials such as carbon fiber composites, titanium alloys, and ceramic matrix composites involve high raw material costs, energy-intensive production, and complex processing techniques. In addition, strict certification and qualification requirements imposed by aviation authorities significantly extend material approval timelines. These factors increase manufacturing costs and limit rapid adoption, particularly for small and mid-sized suppliers.

Qualification of a new aerospace-grade material can take 7–10 years, increasing development costs and slowing commercialization.

Aerospace and Defense Materials Market Opportunities:

- Expansion of Space Programs and Commercial Spaceflight Creating New Demand

Rapid growth in space exploration, satellite constellations, reusable launch vehicles, and commercial spaceflight is creating strong opportunities for advanced aerospace materials. Space applications require ultra-lightweight, radiation-resistant, and high-temperature materials to ensure mission durability and cost efficiency. Increased public and private investment in space programs is accelerating innovation in composites, heat-resistant alloys, and advanced coatings.

Over 6,500 active satellites were in orbit by 2024, with next-generation constellations driving sustained demand for lightweight structural and thermal materials.

Aerospace and Defense Materials Market Segment:

-

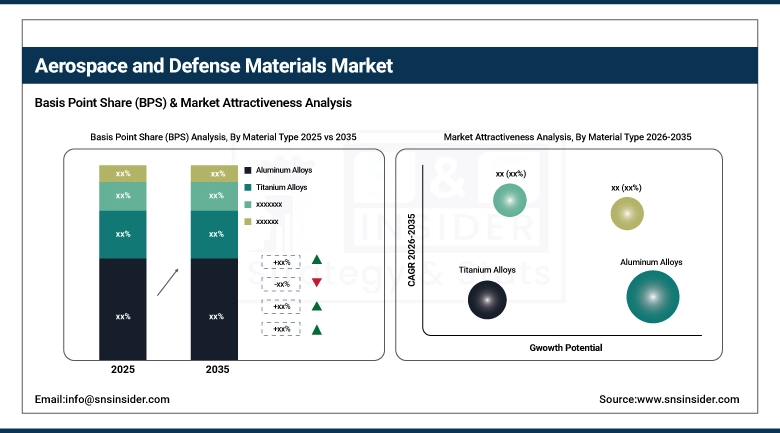

By Material Type: In 2025, aluminum alloys dominated the market with the largest share; composites are projected to be the fastest-growing material segment during 2026–2035.

-

By Manufacturing Technology: In 2025, advanced machining & forging led the market; additive manufacturing (3D printing) is expected to be the fastest-growing technology during 2026–2035.

-

By Application: In 2025, airframe & structural components accounted for the highest share; engine & propulsion systems are anticipated to be the fastest-growing application during 2026–2035.

-

By End User: In 2025, commercial aviation dominated the market; space & satellite systems are projected to be the fastest-growing end-user segment during 2026–2035.

Aerospace and Defense Materials Market Segment Analysis:

By Material Type: Aluminum Alloys Lead as Composites Emerge as the Fastest-Growing Segment

Aluminum alloys dominate the material type segment due to their widespread use in airframes, fuselage structures, wings, and structural components across commercial and military aircraft. Their favorable strength-to-weight ratio, corrosion resistance, cost efficiency, and ease of fabrication make aluminum alloys a preferred choice for high-volume aerospace manufacturing. Continuous demand from narrow-body and wide-body aircraft production sustains their leadership globally.

Composites represent the fastest-growing segment, driven by the aerospace industry’s shift toward lightweight materials to improve fuel efficiency and reduce emissions. Increasing use of carbon fiber reinforced polymers (CFRP) in next-generation aircraft, UAVs, and space structures is accelerating composite adoption, supported by advancements in material performance and manufacturing scalability.

By Manufacturing Technology: Advanced Machining & Forging Lead as Additive Manufacturing Gains Rapid Traction

Advanced machining and forging dominate the manufacturing technology segment due to their established role in producing high-strength, safety-critical aerospace components. These processes are extensively used for aluminum, titanium, and superalloy parts requiring precise tolerances, structural integrity, and regulatory compliance. Their reliability and qualification maturity ensure continued dominance across OEM and Tier-1 supplier operations.

Additive manufacturing is the fastest-growing technology segment, driven by its ability to produce complex geometries, reduce material waste, and shorten production lead times. Growing adoption of 3D-printed metal and polymer components in aircraft interiors, engine parts, and space applications is accelerating its integration into aerospace manufacturing workflows.

By Application: Airframe & Structural Components Dominate as Engine & Propulsion Systems Grow Rapidly

Airframe and structural components lead the application segment due to high material consumption in fuselage sections, wings, frames, and load-bearing structures. These components require large volumes of aluminum alloys, composites, and titanium to meet durability, fatigue resistance, and safety standards, making them the primary driver of material demand across aerospace platforms.

Engine and propulsion systems are the fastest-growing application segment, supported by increasing demand for high-temperature-resistant materials such as titanium alloys, superalloys, and ceramic matrix composites. Growth in advanced jet engines, hypersonic platforms, and fuel-efficient propulsion systems is accelerating material innovation in this segment.

By End User: Commercial Aviation Leads as Space & Satellite Systems Expand at the Fastest Pace

Commercial aviation dominates the end-user segment due to sustained aircraft deliveries, fleet modernization programs, and rising global air passenger traffic. Continuous demand for lightweight and fuel-efficient materials in narrow-body and wide-body aircraft supports strong material consumption across commercial aerospace manufacturing.

Space and satellite systems represent the fastest-growing end-user segment, driven by increasing satellite launches, space exploration missions, and commercial spaceflight initiatives. Demand for ultra-lightweight, high-strength, and thermal-resistant materials in launch vehicles and satellite structures is accelerating growth across this rapidly expanding segment.

Aerospace and Defense Materials Market - Regional Analysis

North America Aerospace and Defense Materials Market Insights:

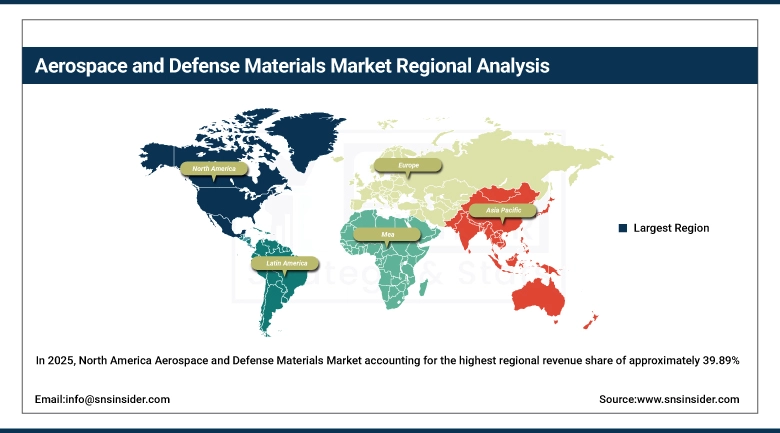

In 2025, North America Aerospace and Defense Materials Market accounting for the highest regional revenue share of approximately 39.89%. This dominance is driven by North America’s strong aerospace manufacturing base, high defense spending, and the presence of major aircraft OEMs and material suppliers. Sustained investments in military modernization programs, advanced fighter aircraft, UAVs, and space systems, along with rapid adoption of lightweight composites, titanium alloys, and additive manufacturing technologies, further reinforce the region’s leadership. Robust R&D infrastructure, stringent quality standards, and long-term government procurement contracts continue to support North America’s dominant position in the global aerospace and defense materials market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Aerospace and Defense Materials Market Insights:

Asia-Pacific is the fastest-growing region, expected to grow at a CAGR 8.87% during the forecast period 2026-2035. This rapid growth is driven by expanding commercial aviation fleets, rising defense budgets, and large-scale indigenous aircraft and defense manufacturing programs across China, India, Japan, and South Korea. Increasing investments in space missions, UAVs, and missile systems, along with growing adoption of composites, aluminum, and titanium alloys, and supportive government initiatives under “Make in Asia” policies, are accelerating demand for advanced aerospace and defense materials across the region.

Europe Aerospace and Defense Materials Market Insights:

Europe represents a significant share of the Aerospace and Defense Materials Market, supported by a strong aerospace manufacturing base and advanced defense capabilities. The presence of major aircraft OEMs, engine manufacturers, and Tier-1 suppliers, along with sustained investments in military modernization, space programs, and lightweight composite materials, continues to drive steady market growth across the region.

Latin America Aerospace and Defense Materials Market Insights:

Latin America is witnessing steady growth in the Aerospace and Defense Materials Market, driven by gradual expansion of commercial aviation, fleet modernization, and rising regional air travel demand. Increasing defense procurement, maintenance and overhaul activities, and emerging local aerospace manufacturing hubs—particularly in Brazil and Mexico—are supporting demand for aluminum alloys, composites, and advanced structural materials across the region.

Middle East & Africa Aerospace and Defense Materials Market Insights:

The Middle East & Africa region is experiencing moderate growth in the Aerospace and Defense Materials Market, supported by rising defense spending, fleet upgrades, and increasing focus on indigenous defense manufacturing. Investments in military aircraft, UAVs, and space programs, particularly across the Gulf countries, along with expanding MRO activities and strategic partnerships with global aerospace OEMs, are driving demand for advanced aluminum, titanium, and composite materials.

Aerospace and Defense Materials Market Competitive Landscape:

Toray Industries Inc., headquartered in Tokyo, Japan, is a leading global supplier of advanced aerospace materials, with a strong portfolio of carbon fiber composites, prepregs, and high-performance thermoplastic materials used in commercial aircraft, military platforms, and space applications. Toray’s materials are widely adopted in airframes, wings, fuselages, and engine components due to their superior strength-to-weight ratio, fatigue resistance, and fuel-efficiency benefits. Long-term supply agreements with major aircraft OEMs and continuous R&D investments strengthen its competitive position.

-

June 2025, Toray expanded its aerospace-grade carbon fiber and composite prepreg production capacity to support next-generation commercial aircraft and defense programs, focusing on lightweight and low-emission aviation platforms.

Hexcel Corporation, headquartered in Stamford, Connecticut, U.S., is a key player in advanced composite materials for aerospace and defense applications. The company specializes in carbon fibers, resin systems, honeycomb structures, and engineered composite solutions used extensively in airframes, rotorcraft, engines, and defense systems. Hexcel benefits from strong demand across commercial aviation recovery, military modernization, and space programs, supported by close collaboration with leading OEMs and Tier-1 suppliers.

-

May 2025, Hexcel announced new investments in high-performance composite materials and automation technologies to enhance production efficiency and meet growing demand from defense aircraft, space launch systems, and next-generation air mobility platforms.

Solvay S.A., headquartered in Brussels, Belgium, is a major supplier of specialty polymers, high-performance composites, and advanced materials for aerospace and defense applications. Solvay’s thermoset and thermoplastic composites, adhesives, and high-temperature polymers are widely used in structural components, interiors, and engine systems, offering weight reduction, thermal stability, and chemical resistance. Its strong innovation pipeline and focus on sustainable materials reinforce its market standing.

-

April 2025, Solvay launched next-generation aerospace thermoplastic composite materials aimed at improving recyclability and reducing lifecycle emissions, aligning with aircraft OEM sustainability targets and future defense platform requirements.

Aerospace and Defense Materials Market Key Players

-

Toray Industries, Inc.

-

Solvay S.A.

-

Constellium SE

-

Allegheny Technologies Incorporated (ATI)

-

Carpenter Technology Corporation

-

Teijin Limited

-

Materion Corporation

-

Howmet Aerospace Inc.

-

Alcoa Corporation

-

Novelis Inc.

-

VSMPO-AVISMA Corporation

-

Kobe Steel Ltd.

-

AMG Advanced Metallurgical Group N.V.

-

SGL Carbon SE

-

Huntsman International LLC

-

3M Company

-

Rogers Corporation

-

SABIC (Saudi Basic Industries Corporation)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 22.69 Billion |

| Market Size by 2035 | USD 38.78 Billion |

| CAGR | CAGR of 5.78% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Material Type:(Aluminum Alloys, Titanium Alloys, Composites, Others) •By Manufacturing Technology:(Additive Manufacturing (3D Printing), Advanced Machining & Forging, Composite Layup & Filament Winding, Others) •By Application:(Airframe & Structural Components, Engine & Propulsion Systems, Interior & Cabin Components, Others) •By End-Use Industry:(Commercial Aviation, Military & Defense, Space & Satellite Systems, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Toray Industries, Inc., Hexcel Corporation, Solvay S.A., Constellium SE, Allegheny Technologies Incorporated (ATI), Carpenter Technology Corporation, Teijin Limited, Materion Corporation, Arconic Corporation, Howmet Aerospace Inc., Alcoa Corporation, Novelis Inc., VSMPO-AVISMA Corporation, Kobe Steel Ltd., AMG Advanced Metallurgical Group N.V., SGL Carbon SE, Huntsman International LLC, 3M Company, Rogers Corporation, SABIC (Saudi Basic Industries Corporation). |

Frequently Asked Questions

Key drivers of the Aerospace and Defense Materials Market include rising demand for lightweight, high-strength materials to improve fuel efficiency and performance, along with increasing defense modernization and military spending.

North America dominated the Aerospace and Defense Materials Market in 2025.

The composites segment dominated the Aerospace and Defense Materials Market due to their high strength-to-weight ratio.

The market was valued at USD 22.69 Billion in 2025 and is projected to reach USD 38.78 Billion by 2035.

The Aerospace and Defense Materials Market is expected to grow at a CAGR of 5.78% during 2026-2035.

Get in Touch