AI Consulting Services Market Report Scope & Overview:

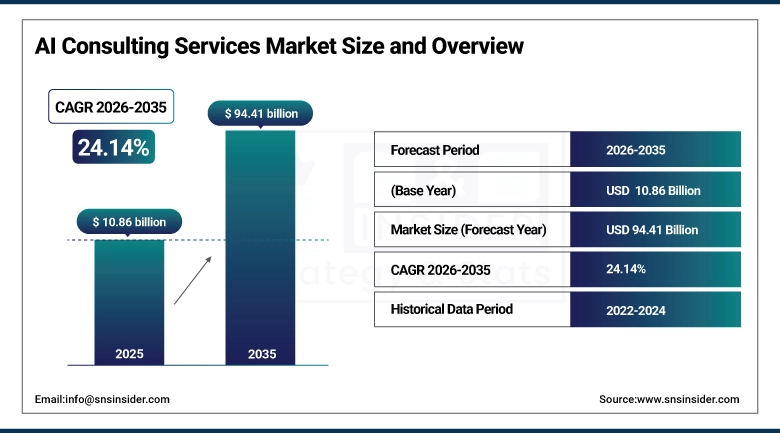

The AI Consulting Services Market was valued at USD 10.86 billion in 2025 and is expected to reach USD 94.41 billion by 2035, growing at a CAGR of 24.14% from 2026–2035.

It can be stated that there is a growing tendency towards fast-growing development of demand for AI consulting services since a great number of companies from different sectors of economy resorted to AI technologies in order to raise their efficiency and save money due to their use of innovations. AI consultants may assist organizations not only in implementing AI but also give consultations on a variety of matters associated with it, among which are: formulation of AI strategies, data engineering, building machine learning models, and integrating systems. As the approaches to business, such as machine learning and automation, become more popular, more organizations search for specialists in this field.

In accordance with data from the same industry, the number of property management companies using AI technologies has increased from 21% in 2020 to over 34% by 2023, while about 80% of all organizations will depend heavily on evidence-based decisions by 2025 with the help of AI consultancy firms.

AI Consulting Services Market Size and Forecast

-

Market Size in 2025: USD 10.86 Billion

-

Market Size by 2035: USD 94.41 Billion

-

CAGR: 24.14% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on AI Consulting Services Market - Request Free Sample Report

AI Consulting Services Market Trends

-

Rapidly increasing enterprise adoption of generative AI and large language models driving unprecedented demand for AI strategy consulting and implementation services across all industry verticals.

-

The rising importance of AI governance, AI risks, and ethical AI encouraging organizations to use the expertise of consultants in order to use AI in a safe manner and follow the regulations.

-

Deployment of AI technology together with cloud computing and other methods of data engineering to make consultations more cost-efficient due to making AI technology available for medium market companies.

-

Demand for AI technology customized for different sectors like healthcare, BFSI, and manufacturing, thereby increasing the sector-based customization of AI projects for consultations.

-

More use of AI as a Service (AIaaS) technology will allow the consulting companies to avail their services including fast prototyping, piloting, and management of AI projects.

-

More investments from companies in training of their AI professionals, upskilling, and change management consulting to ensure the success and sustainability of AI deployment within their organizations.

-

The growing demand for consulting in the area of AI analytics in industries to convert big data into useful insights for decision-making.

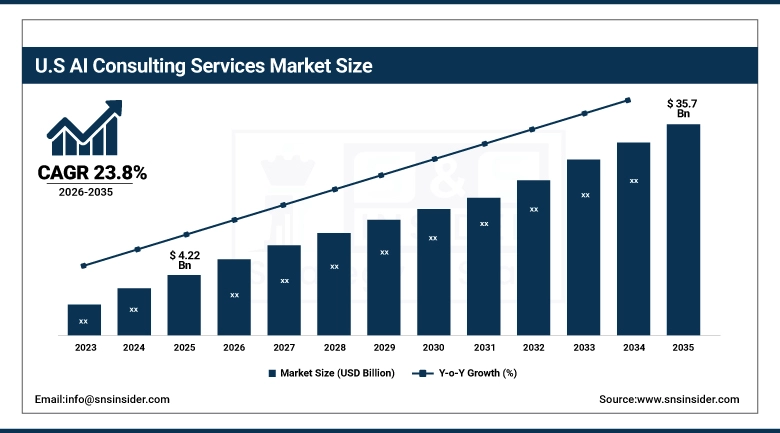

U.S. AI Consulting Services Market was valued at USD 4.22 billion in 2025 and is expected to reach USD 35.7 billion by 2035, registering a CAGR of 23.8% during 2026–2035.

Being one of the most advanced economies in the world, the USA is a dominant player in the global AI consulting services market due to the maturity of the digital landscape, high adoption rate of AI technology among enterprises, as well as the existence of reputable firms, such as McKinsey & Co., Deloitte, Accenture, and IBM, that offer AI consulting. The North American region holds about 39% of global market revenues in 2025, thanks to the strong presence of investments in AI R&D, cloud computing systems, and supportive regulations.

The global strategy consulting market is expected to experience an average annual growth rate of 26.51% during the period between 2026 and 2035 owing to the requirement of businesses to integrate their AI investments with business goals and return on investment, making this segment one of the most promising ones in the consulting industry.

AI Consulting Services Market Segment Insights

-

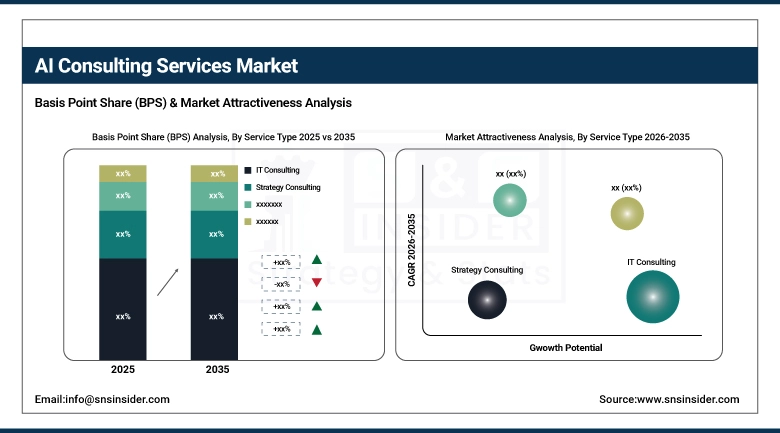

Based on Service Type, IT Consulting accounted for the largest market share (~28%) in 2025; Strategy Consulting expected to be the fastest-growing segment (CAGR of 26.51%).

-

Based on Enterprise Size, Large Enterprises accounted for the largest market share (~65%) in 2025; SMEs expected to be the fastest-growing segment (CAGR of 25.70%).

-

Based on End-User, Finance & Banking accounted for the largest market share (~19%) in 2025; Healthcare expected to be the fastest-growing segment (CAGR of 25.81%).

AI Consulting Services Market Segment Analysis

By Service Type, IT Consulting dominates, Strategy Consulting expected to grow fastest

IT Consulting held the dominant position in the AI consulting services market with approximately 28% revenue share in 2025. This leadership is attributed to IT consulting's role as the foundational enabler for end-to-end AI integration — from infrastructure planning and system compatibility assessment to data migration, platform scalability, and deployment. As organizations undergo digital transformation, IT consultants serve as one of the critical bridge between business objectives and technical AI implementation. This makes it the most relied-upon consulting discipline among all other sectors.

The segment that is estimated to register the highest CAGR of 26.51% over the forecast period from 2026 to 2035 is Strategy Consulting. With a rise in the requirement for organizations to align their AI investments with their business objectives, the demand for strategy consulting services is expected to pick up pace in the coming years. Strategy consulting enables businesses to transform their business model and find AI use cases that provide ROI.

By Enterprise Size, Large Enterprises dominate, SMEs expected to grow fastest

Large Enterprises is the dominant player in the AI Consulting Services market. It accounted for approximately 65% of market share by revenue in 2025. This is due to the highly digitized, huge IT budget, and operations in a complex business ecosystem. Large enterprises use AI for different applications that includes automation, predictive analysis, and natural language processing, requiring customized AI consulting services.

It is estimated that SMEs will account for the largest market growth rate at a CAGR of 25.70% during 2026–2035. Increasing recognition of the advantages of AI in business, the availability of cloud AI solutions with easier access, and affordable third-party consulting services are empowering SMEs to focus on digital transformation. Government initiatives and flexible AI consulting services are contributing to SME uptake.

By End-User, Finance & Banking dominates, Healthcare expected to grow fastest

With almost 19% revenue contribution in 2025, Finance & Banking has been the first industry to apply AI due to its use in risk evaluation, fraud detection, trading models, and personalization. The need for regulatory compliance and real-time data analysis makes the banking sector one of the largest buyers of AI consulting services.

The healthcare segment is anticipated to witness the fastest growth rate of 25.81% during the forecast period, thanks to rising deployment of AI in diagnostics, patient care optimization, and improving operational efficiencies. The requirement to manage compliance regulations, AI integration within EHR systems, and implementation of ethical frameworks for the use of AI in clinical settings creates strong demand for consultancy services.

AI Consulting Services Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

39% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

China |

40% |

|

Middle East & Africa |

UAE |

30% |

|

Latin America |

Brazil |

45% |

North America AI Consulting Services Market Insights

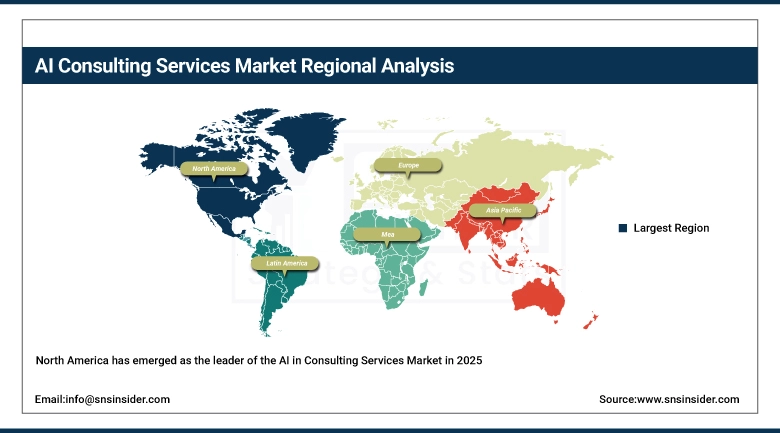

North America has emerged as the leader of the AI in Consulting Services Market in 2025, owing to high adoption of AI by enterprises, highly developed digital infrastructures, and the existence of major global players in consulting and technology space. The United States is responsible for a significant chunk of regional demand with businesses adopting AI aggressively for strategic consultations, operations management, risk assessment, and digital transformation initiatives. Large amounts of investment in generative AI, machine learning, and AI governance models have been driving market growth. Some prominent industry verticals that leverage AI consulting are BFSI, healthcare, retail, and IT services. The region is well-endowed with an active start-up environment and robust cloud infrastructures, which facilitate AI implementation on an expansive scale.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI Consulting Services Market Insights

Asia Pacific is the region witnessing the fastest growth in the market for AI consulting services owing to its fast digital transformation, rising adoption by small to medium-sized enterprises, and AI initiatives being spearheaded by the governments of countries such as China, India, Japan, South Korea, and Singapore. Enterprises in these countries are using AI consulting services to automate their processes effectively, make decisions based on data analysis, and provide enhanced customer experience. There are several factors behind this growth, including the availability of a large pool of talent, increasing use of cloud computing technology, and the emergence of startups focusing on AI.

Europe AI Consulting Services Market Insights

The European region plays a prominent role in the AI consultation services market, due to having highly developed industrial regions, stringent regulations, and high focus on the deployment of AI ethically. Regions like Germany, UK, France, and Nordics are adopting AI consultation solutions for various verticals including manufacturing, automotive, financial services, and public sector digitization. The rising number of requests for AI consultations to comply with EU AI Act and GDPR regulations is expected to generate huge demand for AI governance, risk assessment, and responsible AI consultations.

Middle East & Africa and Latin America AI Consulting Services Market Insights

Middle East & Africa is emerging as a high-potential market for AI consulting services, driven by large-scale smart city projects, digital government initiatives, and economic diversification strategies. The UAE, Saudi Arabia, and South Africa are at the forefront of the adoption of AI consulting, especially in industries such as oil & gas, BFSI, healthcare, and public services. Companies are using AI consulting services for predicting trends, automation, and increasing efficiencies in their operations.

Growth in the AI consulting services market is witnessed consistently in Latin America as a result of increased digitization and adoption of cloud computing technology by companies. Some of the top nations where there is demand for AI consulting services include Brazil, Mexico, and Chile. The demand arises in sectors such as banking, retail, telecommunications, and governments. Companies require AI consulting services for creating an enhanced customer experience, fraud detection, supply chain management, and data-driven decisions.

AI Consulting Services Market Growth Drivers:

Surging organizational demand for AI transformation expertise across all verticals fuels consulting market growth

In the market of AI consulting services, there is significant growth, driven by high enterprise demand for the expertise related to AI transformation in all industries. Enterprises are rapidly adopting artificial intelligence-based technologies to enhance their operational efficiency, make sound decisions, and offer personalized experiences to their customers, thus fueling the demand for consulting services. The integration of generative AI, large language models, and automated machine learning functions in the enterprise environment is generating new consulting needs, including AI strategy development, implementation planning, and governance design. At the same time, enterprises seek consulting services that will help them deploy AI models, manage their lifecycles, and optimize their performance. Lastly, novel trends, such as ethical AI advising, compliance advising, and risk mitigation consulting, have broadened the scope of AI consulting services.

AI Consulting Services Market Restraints

High Implementation Complexity and Talent Shortage Limits AI Consulting Scalability

The complex nature of implementing AI solutions across the entire organization is another important constraint in the AI Consulting Services Market. Since many companies do not have adequate infrastructures, standard procedures, and AI-friendly environments to facilitate smooth AI solution implementation, they tend to rely more on external consultancy services. This not only leads to higher costs but also results in delays in the overall implementation process. Additionally, expensive consulting fees limit the scope for smaller businesses and SMEs in developing countries from adopting AI technologies. Uncertainties related to data privacy laws, algorithmic fairness, and ethical AI practices add further regulatory constraints.

AI Consulting Services Market Opportunities

Expansion of Generative AI, Enterprise Automation, and AI Governance Consulting

There are several notable growth opportunities that will be observed in the AI Consulting Services Market due to the rise of generative AI and enterprise automation solutions. Businesses are increasingly looking for professional assistance for incorporating AI solutions in their operations, marketing, finance, and other processes that can benefit from AI capabilities. In addition to this, the rising popularity of large language models and multimodal AI solutions opens up an opportunity for offering custom AI integration and deployment services. Moreover, there is a strong opportunity in the areas of AI governance and AI regulation and advisory services due to the introduction of strict rules and guidelines regarding AI usage in several countries. BFSI, healthcare, manufacturing, and retail sectors are rapidly investing in AI initiatives, thus widening the consulting scope.

Recent Developments:

-

2026: Accenture significantly expanded its generative AI consulting portfolio by integrating AI agents into enterprise transformation programs across banking, retail, and manufacturing sectors. The company is focusing on large-scale deployment of AI-driven workflow automation, cloud migration, and intelligent enterprise solutions, while also upskilling its workforce in generative AI tools to support client adoption at scale.

-

2026: IBM Consulting has fortified its strategy of providing AI-driven consulting services by incorporating watsonx-enabled solutions within enterprise advisory and implementation services. In 2026, the organization has made strides towards an emphasis on AI governance, model management throughout its life cycle, and specialized AI solutions for regulated industries such as healthcare and financial institutions, enabling companies to adopt credible AI systems.

-

2026: The Deloitte Organization introduced new services in the area of AI-driven consulting in 2026, including AI governance, responsible AI adoption, and generative AI transformation strategies. Deloitte is working on enhancing generative AI capabilities in finance, supply chains, and the overall customer experience.

AI Consulting Services Market Key Players

Some of the AI Consulting Services Market Companies are:

-

Accenture

-

Deloitte

-

McKinsey & Company

-

IBM Consulting

-

PricewaterhouseCoopers (PwC)

-

Boston Consulting Group (BCG)

-

Booz Allen Hamilton

-

KPMG

-

Ernst & Young (EY)

-

Capgemini

-

Cognizant

-

Infosys

-

Wipro

-

HCLTech

-

Tata Consultancy Services (TCS)

-

SAP SE

-

Microsoft

-

Google Cloud

-

Amazon Web Services

-

Avanade

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.86 Billion |

| Market Size by 2035 | USD 94.41 Billion |

| CAGR | CAGR of 24.41% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (IT Consulting, Strategy Consulting, Analytics Consulting, AI Customization, Cognitive Integration) • By Enterprise Size (Large Enterprises, SMEs) • By End-User (Finance & Banking, Healthcare, Retail, Manufacturing, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Accenture, Deloitte, McKinsey & Company, IBM Consulting, PricewaterhouseCoopers (PwC), Boston Consulting Group (BCG), Booz Allen Hamilton, KPMG, Ernst & Young (EY), Capgemini, Cognizant, Infosys, Wipro, HCLTech, Tata Consultancy Services (TCS), SAP SE, Microsoft, Google Cloud, Amazon Web Services, Avanade |

Frequently Asked Questions

North America dominated the AI Consulting Services Market in 2025, accounting for approximately 39% of global market revenue, driven by a well-established digital ecosystem, high enterprise AI adoption, and the presence of world-leading consulting and technology firms.

The Large Enterprises segment dominated the AI Consulting Services Market in 2025 with approximately 65% revenue share, driven by advanced digital maturity, substantial IT budgets, and complex operational needs requiring tailored AI consulting for implementation, transformation strategies, and governance.

The IT Consulting segment dominated the AI Consulting Services Market in 2025, accounting for approximately 28% of global revenue, owing to its critical role in enabling end-to-end AI integration including infrastructure planning, system compatibility, data migration, and platform scalability.

The surging enterprise adoption of AI across all industries, combined with increasing demand for customized AI strategies, risk assessments, ethical AI frameworks, and regulatory compliance consulting is the primary structural driver of sustained market growth through 2035.

The AI Consulting Services Market was valued at USD 10.86 billion in 2025.

The AI Consulting Services Market is expected to grow at a CAGR of 24.14% from 2026 to 2035.

Get in Touch