Video Game Market Report Scope & Overview:

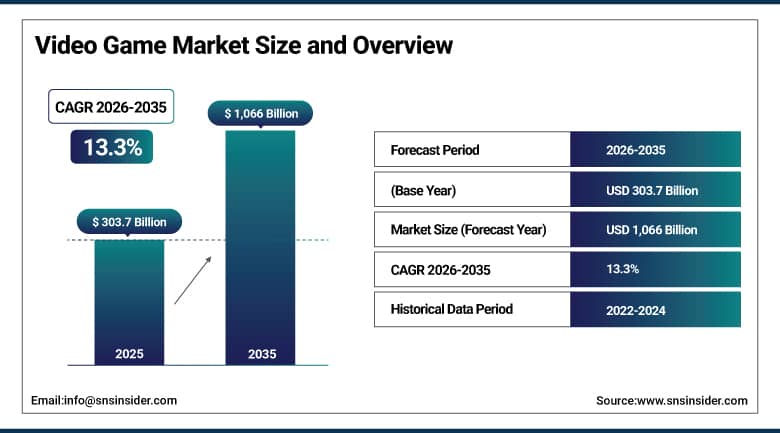

Video Game Market was valued at USD 303.7 billion in 2025 and is expected to reach USD 1,066 billion by 2035, growing at a CAGR of 13.3% from 2026-2035.

The Video Game Market is witnessing a quick expansion, owing to the sudden spike in the use of the internet across the globe, increased use of smartphones, and access to top-notch gaming consoles at reasonable prices. The desire of consumers for immersive content through cloud gaming, virtual reality, and augmented reality technologies is making a substantial contribution to the speedy expansion of the Video Game Market. Additionally, the rising adoption of video games by professional gamers, streamers, and multiplayer online video games is helping the Video Game Market become more profitable.

Video Game Market Size and Forecast

-

Market Size in 2025: USD 303.7 Billion

-

Market Size by 2035: USD 1,066 Billion

-

CAGR: 13.3% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Video Game Market - Request Free Sample Report

Video Game Market Trends

-

Rising global demand for interactive entertainment is driving the video game market.

-

Growing adoption across mobile, console, and PC platforms is boosting market growth.

-

Expansion of online multiplayer gaming and esports ecosystems is fueling engagement.

-

Increasing focus on immersive experiences through AR, VR, and cloud gaming is shaping adoption trends.

-

Advancements in game engines, graphics technologies, and AI-driven gameplay are enhancing user experience.

-

Rising monetization models such as in-game purchases, subscriptions, and live services are supporting market expansion.

-

Collaborations between game developers, publishers, and technology providers are accelerating innovation and global adoption.

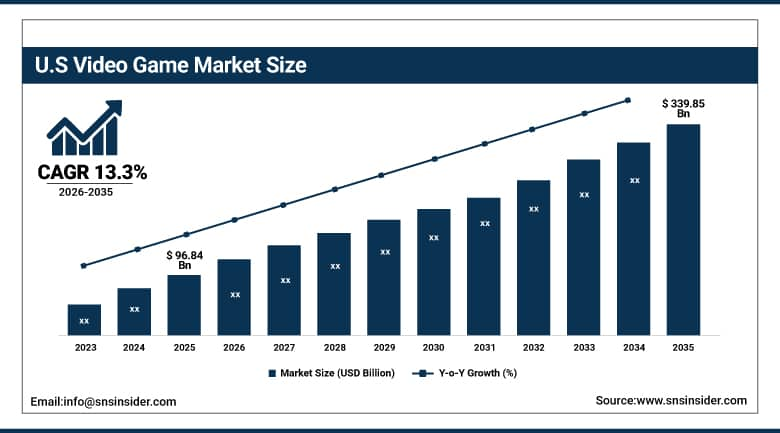

U.S. Video Game Market was valued at USD 96.84 billion in 2025 and is expected to reach USD 339.85 billion by 2035, growing at a CAGR of 13.3% from 2026-2035.

The expansion of the U.S. Video Game Market driven by massive investments made by consumers on digital products, availability of smartphones, consoles, and personal computers, and rapid increase in the base of online video games. Furthermore, e-sports, game subscriptions, and cloud gaming have become an increasing trend that drives the demand for the industry. Additionally, technology development, internet accessibility, and participation of major companies also play a role in market growth.

Video Game Market Segment Analysis

-

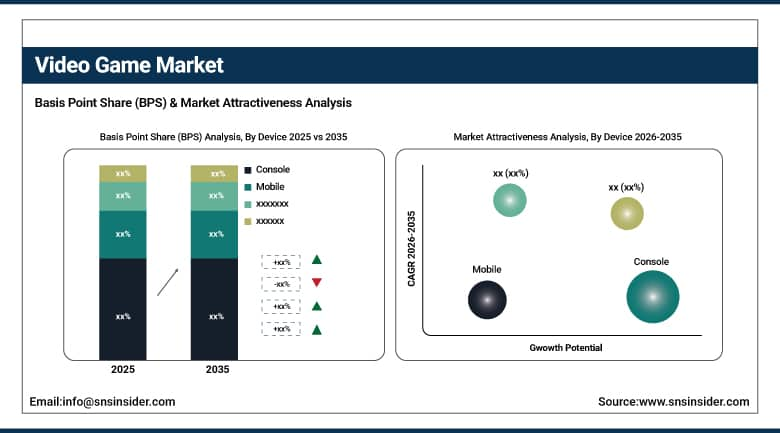

By Device, Mobile segment dominated the Video Game Market in 2025 with 52% share; Console segment fastest growing (CAGR).

-

By Type, Offline segment dominated the Video Game Market in 2025 with 55% share; Online segment is fastest growing (CAGR).

By Device, Mobile segment dominates the Video Game Market, Console segment expected to grow fastest.

The mobile gaming sector is expected to account for the highest market revenue share in 2025 due to its easy accessibility through smartphones with reasonable prices. Reasons like smartphone penetration rate, free/freemium business model of games, and growth of casual gaming apps will help in the development of the market. Mobile gaming platforms provide advantages like affordability, consistent software upgradeability, and wide reach among other factors that make them the most popular gaming platform today.

The console segment is projected to experience rapid growth CAGR from 2026 to 2035 because of rising demand for virtual gaming and enhanced performances. The continuous innovations made in the hardware capabilities of the gaming consoles, the availability of more games, and the establishment of online gaming platforms would drive consumers toward using consoles. In addition, the preferences shown by consumers towards exclusive and high-quality gaming content would increase demand for the next generation of consoles.

By Type, Offline segment dominates the Video Game Market, Online segment expected to grow fastest.

Offline Segment is the segment that dominated the Video Game Market share in 2025, capturing a share of approximately 55% due to the growing demand for offline games, such as single-player games and downloadable games. Consumers prefer playing offline video games since no internet connection is required, which can be particularly advantageous in locations where internet connectivity is either erratic or nonexistent. Offline video games offer uninterrupted gaming experience without having to worry about utilizing data.

Online segment will witness the highest CAGR growth throughout the forecast period from 2026 to 2035 due to the emergence of various multiplayer game platforms, professional e-sports competitions, and live service games. The growing availability of faster internet connectivity along with better social features within video games has driven consumer engagement. The regular updating of game content, in-game purchases, and cross-play capabilities have also influenced the adoption rate.

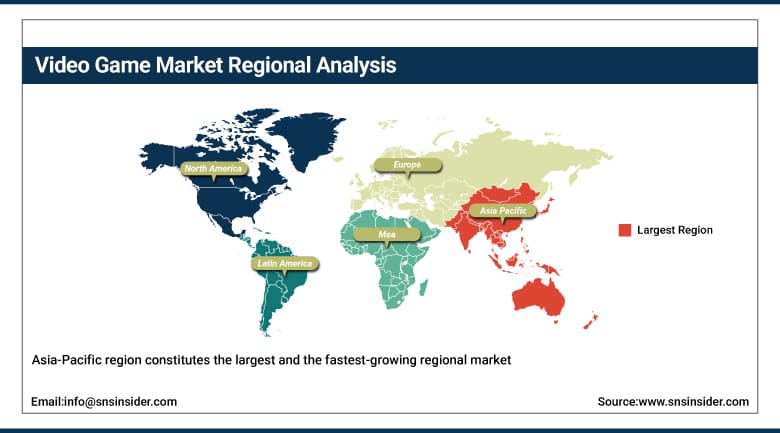

Video Game Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

89% |

|

Europe |

United Kingdom |

24% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

48% |

Asia Pacific Video Game Market Insights

Asia-Pacific region constitutes the largest and the fastest-growing regional market for Video Games due to China's immense player base, South Korea's pre-eminent status as an esporting powerhouse, Japan's unique console game tradition, and the quick growth of mobile gaming in South-East Asia and India. The Chinese gaming market, being the largest in the world in terms of active gamers, is dominated by Tencent's suite of games available in its WeChat Games platform as well as games developed by the firm and its subsidiaries. South Korea's global impact on esporting infrastructure development, such as designated arenas for esporting events and certified esporting players by governmental bodies, has been crucial for competitive gaming culture around the world.

China's National Press and Publication Administration regulates video game approvals with a licensing system that affects foreign title market access. South Korea's Korea Game Society reports that esports generates over USD 5 billion annually in commercial activity including advertising, sponsorship, and broadcast rights across Korean professional leagues.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Video Game Market Insights

North America Video Game Market is fuelled by high consumer spending power, availability of key publishers and game developers, and extensive use of cutting-edge game technology. The region capitalizes on its huge base of console, computer, and mobile gamers, boosted by high internet connectivity and digital distribution channels. Cloud gaming, esports, and subscription-based games are creating additional opportunities for the market. Consistent advancements in immersive gaming like virtual reality and cross-platform gaming are fostering customer engagement and ensuring steady demand among gaming enthusiasts.

Europe Video Game Market Insights

The Europe Video Game Market is defined by its diversity in gamers, well-established regulations, and a robust digital environment. Growth in mobile gaming, esports, and online multiplayer gaming is contributing towards market expansion. Also, the presence of an active indie games development community along with increased investments in video game companies is aiding in the development of the market. Technological innovations in gaming industry coupled with the rising popularity of interactive entertainment is boosting player engagement. Furthermore, the availability of robust broadband networks and digital payment system is enabling gaming in the region.

Middle East & Africa and Latin America Video Game Market Insights

Video Game Market in Middle East & Africa and Latin America is witnessing stable growth fueled by high levels of smartphone usage, improved internet connections, and a growing youth demographic. The rising trend towards mobile gaming and online gaming is one of the primary reasons behind the growing demand for video games in both the Middle East & Africa and Latin America regions. The development in the gaming industry including esport, payment systems, and local games also contributes to user participation.

Video Game Market Growth Drivers:

-

Mobile gaming expansion and cloud gaming accessibility removing hardware barriers driving global video game market growth

The growth of the gaming industry's market is inherently about growing the pool of gamers and the amount they spend on gaming. In terms of players, mobile gaming has already pushed the pool from hundreds of millions of players to billions of players, while its expansion into developing countries proceeds as smartphones reach people who had not been able to participate in gaming before. Cloud gaming creates the conditions for the next round of growth by making it possible that once someone has a fast enough internet connection to play games with console-quality graphics without a console, the hardware barrier that had stopped billions of gamers from enjoying premium gaming content has been overcome. This is made easier by the subscription model, which changes the psychology of gamers away from making large payments on irregular occasions toward smaller, more frequent payments that better suit consumers' spending patterns.

GSMA Intelligence reports that mobile internet subscriptions will reach 5.9 billion globally by 2025, with the majority of new connections in Asia Pacific and Sub-Saharan Africa where mobile gaming adoption is accelerating. Microsoft's Game Pass subscription service surpassed 34 million subscribers globally in 2023, validating the subscription gaming model at commercial scale.

Video Game Market Restraints:

-

Rising development costs and cybersecurity concerns creating financial and trust challenges for video game market growth

The growing cost of development and security threats are the major constraints in the Video Game Market industry. Game developers need to invest more money and effort in order to have high-quality images, powerful engines, talented teams, and timely upgrades. However, security breaches, hacking, stolen accounts, and cheating are becoming a serious problem for users and video game companies. The problem affects gamers’ confidence and imposes costs associated with security measures, which makes the video games business expensive. Small businesses find it hard to participate in the competition, thus restraining growth in the video game market.

Video Game Market Opportunities:

-

VR gaming maturation and AI-generated content creating new commercial frontiers for global video game growth

VR gaming has been consistently hyped as the new frontier in the gaming industry for more than a decade now. But the business truth has been evolving slower than expectations have projected. The introduction of VR headsets that do not require a separate computer and are available at affordable prices like the Meta Quest 3 at USD 499 along with a growing number of VR-only games in their catalogues is now creating a ground reality where VR gaming for consumers actually becomes viable rather than remaining confined to being only a niche hobby for enthusiasts. In terms of generating game content using AI technology, there can be opportunities in making individualized worlds for each gamer, NPCs who converse contextually instead of following dialogue trees pre-programmed into the game, and dynamic difficulties that keep challenging the gamer based on his skill level. All these possibilities are achievable using existing technologies, even if in an incipient form, and are starting to find a place in some commercial

Recent Developments:

-

2026: Microsoft launched Xbox Game Pass Ultimate's cloud gaming expansion to 50 additional countries, enabling console-quality gaming on any device with a broadband internet connection without hardware purchase, targeting the billions of smartphone users in Latin America, Southeast Asia, and Africa who have been unable to access Xbox-quality gaming due to console cost barriers.

-

2025: Sony Interactive Entertainment released PlayStation 5 Pro with an AI-enhanced graphics processor delivering 4K gaming at frame rates previously achievable only at lower resolutions, using PlayStation Spectral Super Resolution upscaling that makes games look and play better without requiring developers to rebuild existing titles for the new hardware.

-

2025: Epic Games launched Unreal Engine 5.4 with integrated AI-assisted level design tools that allow developers to describe environments in natural language and receive AI-generated 3D geometry drafts as starting points for human artist refinement representing a fundamental shift in game environment creation workflows.

Video Game Market Key Players

Some of the Video Game Market Companies

-

Microsoft Corporation

-

Sony Group Corporation

-

Nintendo Co., Ltd.

-

Tencent Holdings Limited

-

Electronic Arts Inc.

-

Take-Two Interactive Software Inc.

-

NetEase Inc.

-

Epic Games Inc.

-

Ubisoft Entertainment SA

-

SEGA Corporation

-

Bandai Namco Entertainment Inc.

-

Square Enix Holdings Co., Ltd.

-

Capcom Co., Ltd.

-

2K Games (Take-Two)

-

Valve Corporation (Steam)

-

Roblox Corporation

-

Krafton Inc.

-

Nexon Corporation

-

Konami Holdings Corporation

-

Gearbox Software LLC

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 303.7 Billion |

| Market Size by 2035 | USD 1,066 Billion |

| CAGR | CAGR of 13.3 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device (Console, Mobile, Computer) • By Type (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles |

Microsoft Corporation, Sony Group Corporation, Nintendo Co., Ltd., Tencent Holdings Limited, Electronic Arts Inc., Take-Two Interactive Software Inc., NetEase Inc., Epic Games Inc., Ubisoft Entertainment SA, SEGA Corporation, Bandai Namco Entertainment Inc., Square Enix Holdings Co., Ltd., Capcom Co., Ltd., 2K Games (Take-Two), Valve Corporation (Steam), Roblox Corporation, Krafton Inc., Nexon Corporation, Konami Holdings Corporation, Gearbox Software LLC |

Frequently Asked Questions

North America dominated the Video Game Market in 2025.

The Mobile segment dominated the Video Game Market with approximately 42% share in 2025.

The major growth factor of the video game market is the rising adoption of digital gaming, cloud gaming, and immersive technologies like AR/VR, driven by increasing internet penetration and mobile gaming expansion.

The Video Game Market was valued at USD 303.7 billion in 2025.

The Video Game Market is expected to grow at a CAGR of 13.3% from 2026 to 2035.

Get in Touch