AI in Aviation Market Report Scope & Overview:

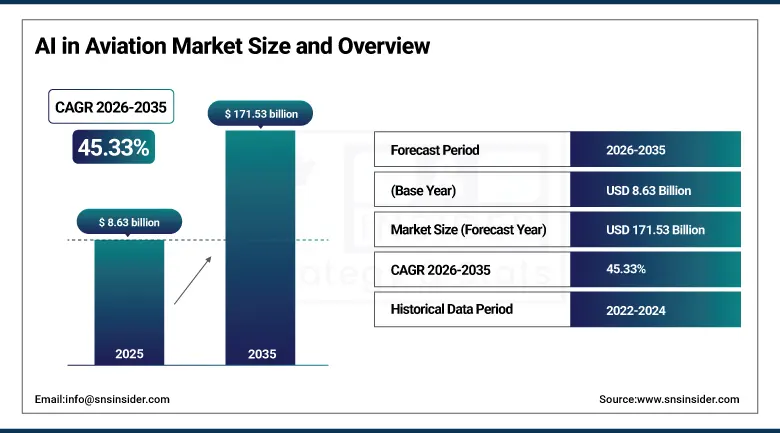

The AI in Aviation Market was valued at USD 8.63 Billion in 2025 and is expected to reach USD 171.53 Billion by 2035, growing at a CAGR of 45.33% from 2026 to 2035.

AI technology is changing the aviation industry in every way. It affects the design and manufacturing of airplanes, the flying process, air traffic control, maintenance, and the management of passenger experience. The unique operating environment of the aviation industry, where there is the need for extremely high levels of safety, multi-stakeholder cooperation, generation of huge volumes of sensor and operational data globally continuously, and efforts to reduce costs and improve customer experience, makes the aviation industry uniquely suited for the implementation of AI solutions. In terms of data that relates to safety, the aviation industry generates more structured data per dollar revenue than other industries with similar profiles.

Airbus launched its AI-powered Skywise predictive maintenance intelligence platform expansion in 2025, processing flight data recorder and aircraft sensor telemetry from over 10,000 connected aircraft across more than 100 airline customers globally.

Market Size and Forecast

-

Market Size in 2026E: USD 12.55 Billion

-

Market Size by 2035: USD 171.53 Billion

-

CAGR: 45.33% from 2026 to 2035

-

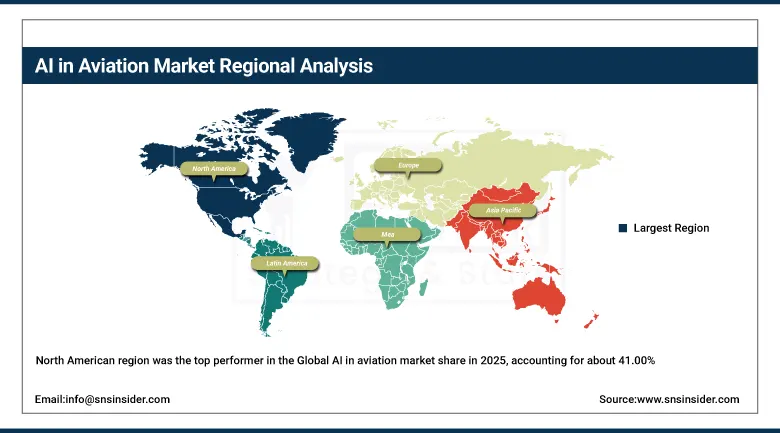

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on AI in Aviation Market - Request Free Sample Report

AI in Aviation Market Trends

-

Generative AI is rapidly expanding in aviation for cockpit support, maintenance automation, passenger service chatbots, and pilot training simulations.

-

Growth of autonomous and remotely piloted aircraft is increasing demand for AI-based navigation, detect-and-avoid, and air traffic management systems.

-

AI-powered digital twins are improving predictive and condition-based aircraft maintenance through real-time sensor data analysis.

-

Airlines are adopting AI-driven revenue management systems for dynamic pricing, demand forecasting, and ancillary revenue optimization.

-

Aviation regulators including FAA, EASA, and ICAO are developing AI certification and safety standards to support wider AI deployment in aviation.

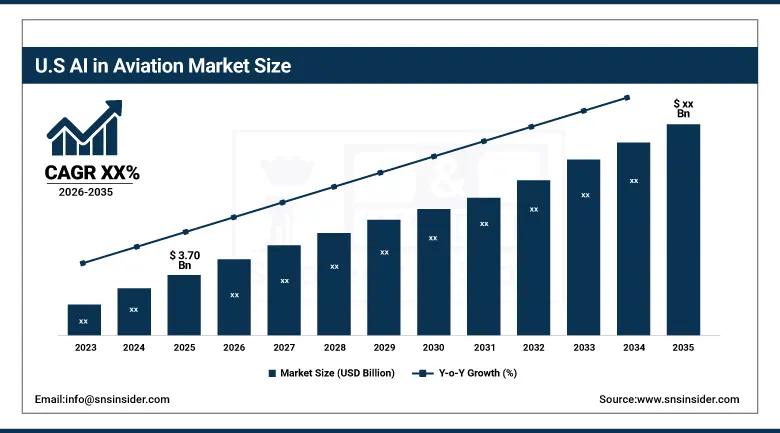

The U.S. AI in Aviation Market Outlook

The U.S. AI in Aviation Market was valued at approximately USD 3.70 Billion in 2025 and is projected to grow significantly through 2035, growing at an above-average CAGR driven by the world's most commercially advanced aviation industry and technology sector.

The United States is also the leading commercially active AI in aviation market due to the presence of many airline companies such as American Airlines, Delta Airlines, United Airlines, and Southwest Airlines, whose operations have led to sufficient generation of operational efficiency through high volume data for making a business case for their AI programs. The United States leads in designing and manufacturing AI-based aircraft systems and engines, spearheaded by Boeing. The USA has also invested in building the world's largest air traffic control system run by FAA which incorporates AI in its NextGen project. Aviation start-ups such as Palantir, C3.ai, SparkCognition, and Honeywell have developed aviation AI platforms which have already created significant commercial acceptance among US aviation firms and are increasingly being adopted by international aviation firms.

Delta Air Lines announced a multi-year technology partnership with Palantir Technologies in 2025, deploying Palantir's Foundry AI platform across Delta's operational planning, crew management, and maintenance data systems to improve flight schedule recovery from disruption events and reduce maintenance-related delay incidents.

AI in Aviation Market Segmentation Analysis

-

By Application, Predictive maintenance held the largest market share of 28.45% in 2025, while passenger experience enhancement is expected to grow at the fastest CAGR of 52.14% during 2026–2035.

-

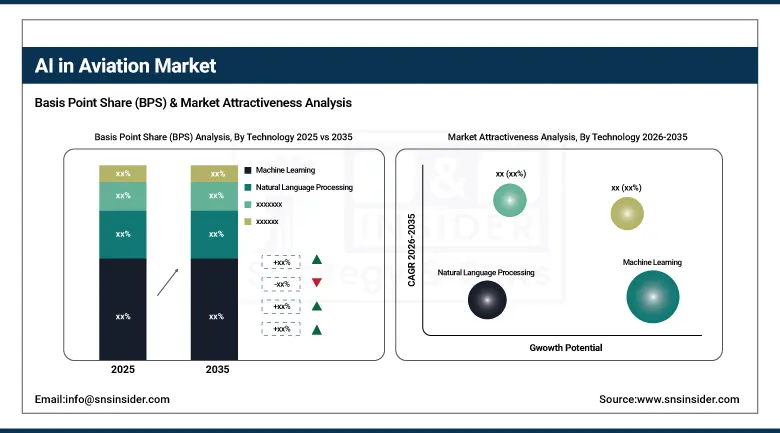

By Technology, Machine Learning dominated with a 34.12% share in 2025, while computer vision is projected to expand at the fastest CAGR of 54.06% during the forecast period.

-

By Component, Software accounted for the highest market share of 41.25% in 2025, while services are anticipated to record the fastest CAGR of 51.27% through 2026–2035.

-

By End User, Airlines held the largest share of 38.91% in 2025, while airports are expected to grow at the fastest CAGR of 53.45% during 2026–2035.

By Technology, machine learning dominates, computer vision grows fastest

Machine learning generated the dominant technology revenue share in 2025, accounting for 42% of AI in aviation technology revenues. Machine learning's commercial dominance reflects its broad applicability across the highest-commercial-priority AI use cases in aviation, encompassing predictive maintenance anomaly detection models, flight path optimization algorithms, revenue management demand forecast systems, and air traffic flow prediction tools that each represent mature ML application categories with documented commercial ROI at multiple airline and airport deployments globally. The technology's ability to discover performance-improving patterns in large historical datasets without explicit programming for each specific relationship makes it particularly well suited to the data-rich aviation operational environment.

Computer vision is growing fastest with a documented CAGR of 45.22%, driven by its transformative applications in aircraft visual inspection automation, ground equipment damage detection, airport security screening, and passenger processing biometrics whose implementation quality and throughput advantages over manual inspection are creating rapid adoption across maintenance, operations, and security functions.

By Application, predictive maintenance dominates, passenger experience grows fastest

Predictive maintenance accounted for 28.45% of AI in aviation market revenue in 2025, reflecting its status as the first AI application category to achieve production-scale deployment at multiple major airlines and its clearest and most directly quantifiable commercial ROI case. Every unscheduled maintenance event that AI-powered anomaly detection prevents translates directly into avoided aircraft-on-ground costs, avoided passenger compensation obligations, and preserved revenue from flights that would otherwise be cancelled or delayed.

Passenger experience enhancement is growing fastest with a CAGR of 52.14%, driven by the competitive differentiation value that personalized AI-driven service delivery creates in an industry where cabin product differentiation is increasingly difficult and customer loyalty programmes are converging.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

28.47% |

|

Latin America |

Brazil |

43.84% |

North America AI in Aviation Market Insights

The North American region was the top performer in the Global AI in aviation market share in 2025, accounting for about 41.00% of total revenue worldwide. This can be attributed to the fact that most airline operations head offices are based here, and also because of its largest air traffic management systems whose artificial intelligence modernization project makes up one of the largest single public sector investments in AI within aviation globally. Canada provides an additional market in terms of demand generated by Air Canada's operational AI projects and Nav Canada's AI in air traffic management systems investments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Aviation Market Insights

In 2025, Europe had about 24.00% of AI in aviation market shares. Europe is regarded as being an innovated AI aviation market as a result of Airbus’ Skywise, EUROCONTROL’s air traffic network optimization AI programs, and the regulatory efforts towards AI certification standards by the European Union Aviation Safety Agency. Germany, France, the UK, and the Netherlands are some of the dominant markets in Europe as they have airlines, aircrafts or ANSPs who spend huge amounts of money on their AI investments that have resulted in high revenue for the market. Examples of successful European airlines AI initiatives include Lufthansa's AI maintenance system, Air France KLM’s digital transformation program, and easyJet’s predictive maintenance system.

Asia Pacific AI in Aviation Market Insights

The fastest-growing regional AI in Aviation market is the Asia Pacific region, expected to have a CAGR of approximately 45.98% until 2035, fueled by the fast-growing global market of commercial aviation industry in addition to the considerable investments made in aviation infrastructure by various governments in China, India, Singapore, Japan, and Australia in addition to the increasing digital transformation of airlines in the Asia Pacific region. The China region alone is responsible for around 38.47% of revenues in the Asia Pacific region, owing to the implementation of smart aviation initiatives under the Civil Aviation Administration of China, AI operational investment in large-scale airlines such as Air China and China Eastern, and the development of an AI commercial aviation platform in China.

MEA & Latin America AI in Aviation Market Insights

MEA and Latin America are fast-growing AI in aviation markets, characterized by aggressive aviation infrastructure development, digital transformation spending by local airlines, and the presence of smart airport development programs, thus leading to AI growth momentum. In the UAE, Emirates' global AI investment, Dubai Airports' smart airport development program, and the UAE government's comprehensive AI strategy in which aviation is prioritized, account for an estimated 28.47% of MEA revenues. The ongoing expansion of aviation infrastructure in Saudi Arabia, guided by Vision 2030, coupled with the establishment of a new airline, namely RIYADH Air, with a digital-native operation model, is creating more Middle East AI in aviation investment. In Brazil, revenues are dominated by LATAM Airlines Group's technology spending and INFRAERO's airport digital transformation program.

Growth Drivers: Abundant aviation operational data and strong ROI from predictive maintenance and efficiency optimization are accelerating AI adoption across the aviation industry.

The unique characteristics of the aviation sector in terms of critical safety requirements, operational complexities, and cost efficiency drive an environment of AI adoption that is more commercially urgent than any other industry in comparison. The competition within commercial aviation is so intense that even a small difference in costs of operation, ranging from 1 to 2%, can be considered significant and thus provides airlines with measurable efficiency gains through their AI initiatives the ability to create competitive advantages over others. The availability of operational data and performance measurement such as on-time performance, efficiency of fuel consumption, and maintenance of aircraft further contributes to making it easier to see performance gains through AI initiatives and keep executive stakeholders interested in sustaining investments throughout the entire multiyear process of creating AI initiatives.

Restraints: Strict aviation safety regulations, certification complexity, and data privacy concerns are slowing AI deployment in critical flight operations.

The regulatory structures of FAA, EASA, and ICAS used in the certification of new aviation technology came about during an era characterized by deterministic software and hardware whose behavior could easily be tested. AI systems which behave in a probabilistic manner and whose behavior is data-dependent, coupled with potential adversarial behavior from external factors, create unique challenges when it comes to certification under these regulatory structures, hence slowing down the time it takes for these systems to enter operational use in aviation compared to the speed of their development outside the aviation industry. Privacy laws such as GDPR make it difficult for airlines to conduct certain types of passenger analysis without prior consent of the passengers, limiting the potential of personalization programs based on such analytical activities.

Opportunities: AI-driven autonomous air traffic management and sustainable aviation fuel optimization are creating major long-term growth opportunities in aviation.

Autonomous or AI-enhanced air traffic control systems that may improve the use of airspace capacity up to 15% to 30% compared to present levels limited by human air traffic controllers form one of the most commercially impactful opportunities for AI-driven aviation innovations, which are currently being pursued with great enthusiasm by agencies such as EUROCONTROL, NASA, FAA, and other providers of air navigation services. Every single percent of increased capacity at an already busy airport hub leads to extra tens of millions of dollars' worth of business generated by the airport's operations. Sustainable AI applications related to aircraft continuous descent approach optimization, optimal weather-based fuel saving routing, and sustainable aviation fuel optimization have been gaining interest as airline ESG policies put pressure on airlines to prove the emissions reducing effects of these technologies.

Recent Developments:

-

2025: Airbus expanded its Skywise predictive maintenance platform to over 10,000 connected aircraft across 100-plus airline customers, with AI models identifying maintenance needs an average of 14 days before threshold-based alerts and having prevented over 4,000 flight disruptions since platform launch.

-

2025: Delta Air Lines deployed Palantir's Foundry AI platform across operational planning, crew management, and maintenance systems, demonstrating measurable improvements in crew scheduling recovery and reduction in maintenance-related delay incidents within the first year of production deployment.

-

2024: Air France-KLM expanded its predictive maintenance AI programme to cover its full Airbus and Boeing narrowbody fleet, incorporating real-time engine performance monitoring, landing gear health tracking, and avionics system anomaly detection that reduced maintenance-related dispatch delays by approximately 20% compared to the preceding year baseline.

AI in Aviation Market Key Players are:

-

Airbus SE

-

Boeing Company

-

IBM Corporation

-

Google LLC (Alphabet Inc.)

-

GE Aviation (GE Aerospace)

-

Thales Group

-

Palantir Technologies Inc.

-

Northrop Grumman Corporation

-

Raytheon Technologies (RTX Corporation)

-

Lockheed Martin Corporation

-

SparkCognition Inc.

-

C3.ai Inc.

-

NVIDIA Corporation

-

Rolls-Royce Holdings PLC

-

Safran SA

-

CAE Inc.

-

SITA (Société Internationale de Télécommunications Aéronautiques)

-

Lufthansa Systems GmbH & Co. KG

AI in Aviation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.63 Billion |

| Market Size by 2035 | USD 171.53 Billion |

| CAGR | CAGR of 45.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Hardware, Services) • By Technology (Machine Learning, Natural Language Processing, Computer Vision, Deep Learning, Generative AI) • By Application (Predictive Maintenance, Flight Operations Optimization, Air Traffic Management, Passenger Experience Enhancement, Safety & Security, Fuel Management, Others) • By End User (Airlines, Airports, MRO Providers, Aircraft Manufacturers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus SE, Boeing Company, IBM Corporation, Microsoft Corporation, Google LLC (Alphabet Inc.), Honeywell International Inc., GE Aviation (GE Aerospace), Thales Group, Palantir Technologies Inc., Northrop Grumman Corporation, Raytheon Technologies (RTX Corporation), Lockheed Martin Corporation, SparkCognition Inc., C3.ai Inc., NVIDIA Corporation, Rolls-Royce Holdings PLC, Safran SA, CAE Inc., SITA (Société Internationale de Télécommunications Aéronautiques), Lufthansa Systems GmbH & Co. KG |

Frequently Asked Questions

The AI in Aviation Market is expected to grow at a CAGR of 45.33% from 2026 to 2035.

The AI in Aviation Market was valued at USD 8.63 Billion in 2025.

The primary growth factors are aviation's extraordinary operational data richness enabling high-accuracy AI model training, the directly quantifiable commercial ROI of predictive maintenance AI in reducing unscheduled maintenance events and flight disruptions.

The predictive maintenance segment dominated the AI in Aviation Market with 28.45% share in 2025.

North America dominated the AI in Aviation Market in 2025, holding approximately 41.00% of global revenues, with the United States accounting for approximately 84.73% of North American revenues.

Get in Touch