Supply Chain Resilience Market Report Scope & Overview:

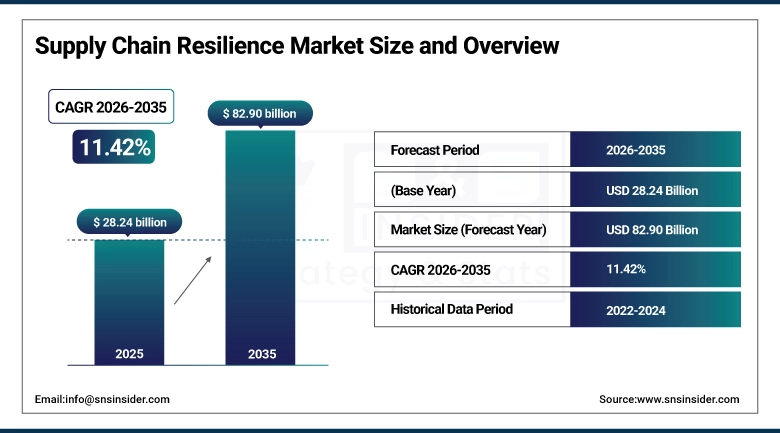

The Supply Chain Resilience Market size was valued at USD 28.24 Billion in 2025 and is projected to reach USD 82.90 Billion by 2035, growing at a CAGR of 11.42% during 2026–2035.

The Supply Chain Resilience Market refers to the ecosystem of technologies, strategies, and services that enable organizations to anticipate, withstand, and recover from disruptions across supply networks. It includes solutions for risk management, real-time visibility, predictive analytics, and contingency planning to ensure business continuity. This market supports industries in mitigating risks from geopolitical events, natural disasters, and demand volatility, enhancing agility, flexibility, and operational stability while maintaining efficient and reliable end-to-end supply chain performance.

Supply Chain Resilience Market Size and Forecast:

-

Market Size in 2025: USD 28.24 Billion

-

Market Size by 2035: USD 82.90 Billion

-

CAGR: 11.42% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Supply Chain Resilience Market - Request Free Sample Report

Key Supply Chain Resilience Market Trends:

-

Real-time supply chain visibility platforms connecting multi-tier supplier networks beyond Tier 1 suppliers into Tier 2 and Tier 3 are becoming the operational baseline for large manufacturers, replacing the episodic assessment processes that left companies without early warning of upstream disruptions until they materialized as production stoppages.

-

AI-driven demand sensing and inventory optimization are reducing the trade-off between service level and working capital by improving forecast accuracy at the SKU and location level, allowing companies to hold less safety stock while maintaining higher fill rates than rule-based replenishment systems delivered.

-

Supply chain digital twins that mirror physical networks in software are enabling scenario planning at a detail level that was previously available only through expensive manual modeling, allowing companies to simulate the impact of supplier failures, transportation disruptions, and demand shocks before committing to reconfiguration decisions.

-

Supplier risk monitoring platforms that aggregate financial health, geopolitical exposure, regulatory compliance, and ESG performance data across supplier bases are being embedded into procurement workflows, converting supply chain risk assessment from a periodic audit exercise into a continuous operational process.

-

Nearshoring and friend-shoring strategies being executed by manufacturers in response to geopolitical risk are generating secondary demand for supply chain resilience technology as companies manage the operational complexity of multi-region sourcing and manufacturing networks that their legacy single-region operations did not require.

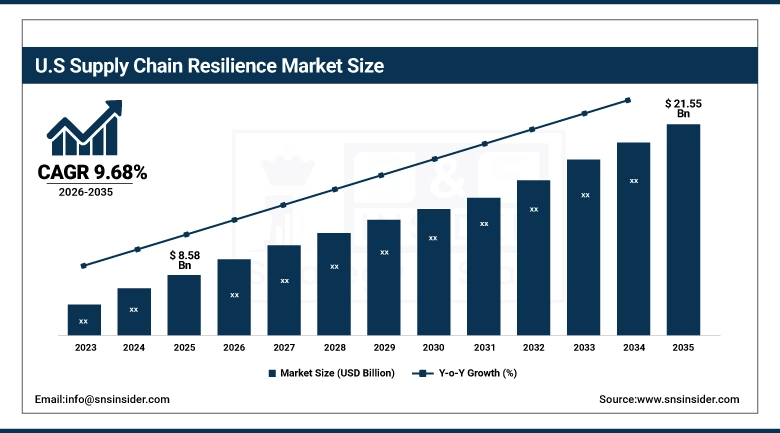

The U.S. Supply Chain Resilience Market was valued at USD 8.58 Billion in 2025 and is projected to reach USD 21.55 Billion by 2035, growing at a CAGR of 9.68% during 2026–2035. The U.S. market benefits from the concentration of large enterprise technology buyers, a mature SaaS vendor ecosystem, and federal procurement programs following executive orders on supply chain security directing agencies to assess vulnerabilities in pharmaceutical, semiconductor, and defense supply chains.

Supply Chain Resilience Market Growth Drivers:

-

Recurring Geopolitical Disruptions, Regulatory Supply Chain Disclosure Requirements, and the Proven ROI of Resilience Technology Investments Are Sustaining Enterprise Demand Across All Major Industry Verticals

Enterprise investment in supply chain resilience technology is no longer primarily crisis response. The pandemic investment wave has transitioned into a durable procurement pattern driven by three forces operating independently. First, geopolitica the frequency and diversity of supply chain disruption events since 2020 have persuaded executive and board-level stakeholders that resilience investment is not optional. Second, regulatory the EU Corporate Sustainability Reporting Directive, the U.S. Uyghur Forced Labor Prevention Act, and the German Supply Chain Due Diligence Act require companies to demonstrate knowledge of their supplier networks, creating compliance-driven demand for supply chain mapping and monitoring technology. Third, demonstrated ROI companies that invested early in visibility and risk management platforms have documented the cost avoidance their systems delivered during specific disruptions, building internal business cases for expanded investment and making budget approvals faster than when the category was less established.

Supply Chain Resilience Market Restraints:

-

Data Sharing Reluctance Across Supplier Networks, Integration Complexity with Legacy ERP Systems, and Organizational Change Management Challenges Are Limiting Full Platform Adoption

Supply chain resilience technology delivers maximum value when it has visibility across the entire network not just the buyer’s own operations but suppliers, logistics providers, and sub-suppliers. The practical obstacle is that suppliers have competitive and legal reasons to be cautious about sharing operational data with customers, and the data sharing agreements needed to enable multi-tier visibility require legal and relationship management work that generates real friction. Integration with legacy ERP systems compounds the challenge: large enterprises have supply chain processes embedded in SAP or Oracle platforms customized over years, and connecting new resilience platforms to these systems requires middleware and API development that adds cost and extends time-to-value. Organizational barriers are frequently the most underestimated constraint resilience technology changes who sees what, which touches organizational politics around data ownership, and technically sound implementation projects regularly stall when change management is inadequately resourced.

Supply Chain Resilience Market Opportunities:

-

SME-Accessible SaaS Platforms, Sector-Specific Resilience Solutions, and Emerging Market Supply Chain Modernization Are Creating Growth Pathways Beyond the Large Enterprise Market That Has Led Initial Adoption

Cloud-native SaaS delivery has reduced the implementation cost and complexity of supply chain visibility and risk management tools to the point where mid-market companies can now afford deployments that previously required enterprise software budgets. Sector-specific resilience platforms are developing for pharmaceutical cold chain management, food safety traceability, semiconductor supply chain monitoring, and defense industrial base risk management each addressing the specific data types and regulatory requirements of their vertical in ways that horizontal platforms do not. Emerging market manufacturing hubs in Vietnam, Indonesia, Mexico, and India are building supply chain management capability as they absorb production shifted from China under diversification strategies, creating demand from buyers and suppliers who are new to the category and lack the legacy integration burden that established enterprise buyers carry.

Supply Chain Resilience Market Segment Analysis:

-

By Solution Type, Risk Management & Monitoring Solutions held the largest market share of 31.64% in 2025, while Inventory & Warehouse Management Solutions are expected to grow at the fastest CAGR of 12.92% during 2026–2035.

-

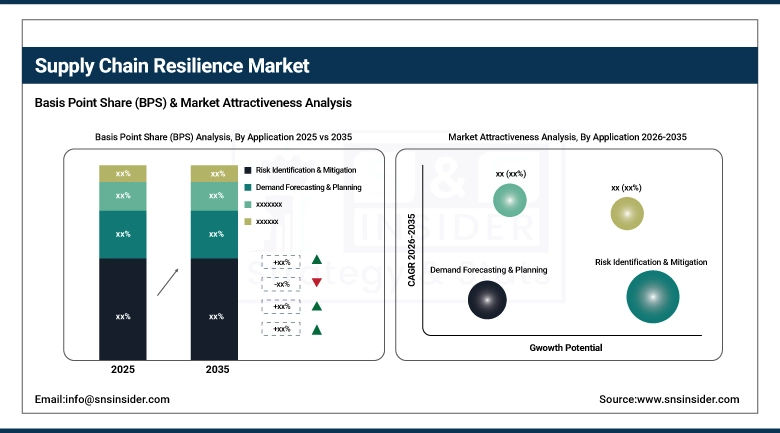

By Application, Risk Identification & Mitigation accounted for the highest market share of 34.57% in 2025, while Supplier Risk & Performance Management is anticipated to expand at the fastest CAGR of 12.34% during the forecast period.

-

By End-User, Manufacturing captured the largest share of 36.48% in 2025, while Healthcare & Pharmaceuticals is expected to grow at the fastest CAGR of 12.55% through 2026–2035.

-

By Deployment Mode, On-Premise solutions held the largest market share of 55.12% in 2025, while Cloud-Based solutions are projected to grow at the fastest CAGR of 12.89% during 2026–2035.

By Application, Risk Identification & Mitigation Dominates While Supplier Risk & Performance Management Is Fastest Growing:

Risk Identification & Mitigation dominates the market due to its role in proactively detecting potential supply chain disruptions and enabling timely response strategies. These solutions help organizations enhance visibility, improve planning, and minimize operational risks across complex global networks. Supplier Risk & Performance Management is the fastest-growing application, focusing on monitoring supplier reliability, compliance, and efficiency. Growing global sourcing and interdependent supply chains drive demand for tools that evaluate supplier performance and mitigate potential vulnerabilities.

By Solution Type, Risk Management & Monitoring Solutions Dominate While Inventory & Warehouse Management Solutions Are Fastest Growing:

Risk Management & Monitoring Solutions dominate as they provide essential capabilities for identifying, monitoring, and mitigating supply chain disruptions. Organizations rely on these solutions to maintain operational continuity, ensure compliance, and respond effectively to unforeseen risks across global supply networks. Inventory & Warehouse Management Solutions are the fastest-growing segment, driven by the need for efficient inventory control, warehouse automation, and real-time analytics to optimize operations, reduce costs, and strengthen supply chain agility.

By End-User, Manufacturing Dominates While Healthcare & Pharmaceuticals Are Fastest Growing:

Manufacturing dominates the market as it involves complex, multi-tiered supply chains that require robust resilience strategies to maintain production continuity, reduce downtime, and manage risks from global disruptions. Healthcare & Pharmaceuticals is the fastest-growing end-user, driven by the critical need for resilient supply chains to ensure uninterrupted delivery of medical products, pharmaceuticals, and equipment, particularly in response to global health emergencies and rising patient demand.

By Deployment Mode, On-Premise Dominates While Cloud-Based Solutions Are Fastest Growing:

On-Premise deployment dominates due to organizations prioritizing data security, regulatory compliance, and control over supply chain operations. These solutions are often preferred by enterprises with existing IT infrastructure and dedicated resources. Cloud-Based solutions are the fastest-growing deployment mode, supported by flexibility, scalability, real-time collaboration, and advanced analytics. Cloud adoption allows organizations to enhance supply chain visibility, improve responsiveness, and integrate multiple partners seamlessly across global networks.

Supply Chain Resilience Market Regional Analysis:

North America Supply Chain Resilience Market Insights

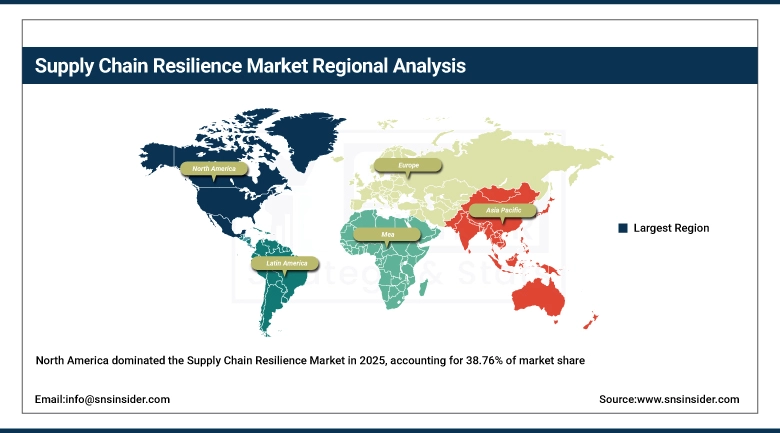

North America dominated in 2025 at USD 10.95 Billion (38.76%), projected to reach USD 28.42 Billion by 2035 at a CAGR of 10.05%. The region’s leadership reflects the concentration of large enterprise technology buyers, a mature SaaS vendor ecosystem spanning visibility, risk analytics, and digital twin platforms, and a post-pandemic policy environment in which federal supply chain security directives have sustained institutional investment in resilience capability across pharmaceuticals, semiconductors, and defense industrial supply chains.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Supply Chain Resilience Market Insights

The United States dominates North American demand through its concentration of large enterprise technology buyers, its world-leading supply chain software vendor base, and active federal procurement programs directing agencies and critical industries to assess and strengthen domestic and allied-nation supply chain vulnerabilities.

Europe Supply Chain Resilience Market Insights

Europe held a 26.41% share in 2025 at USD 7.46 Billion, growing to USD 21.28 Billion by 2035 at a CAGR of 11.10%. Regulatory compliance requirements the EU Corporate Sustainability Reporting Directive, the German Supply Chain Due Diligence Act, and the forthcoming EU supply chain due diligence directive are converting supply chain transparency from a corporate responsibility aspiration into a legal obligation, generating compliance-driven technology procurement that operates independently of pure risk management motivation.

Germany Supply Chain Resilience Market Insights

Germany leads European supply chain resilience investment as the continent’s largest manufacturing economy, facing immediate compliance obligations under its own supply chain due diligence legislation and running deeply integrated automotive and industrial machinery sectors that require sophisticated multi-tier visibility technology.

Asia Pacific Supply Chain Resilience Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 13.75%, rising from USD 6.17 Billion in 2025 to USD 22.33 Billion by 2035. The region’s growth leadership reflects the scale of manufacturing activity across China, Japan, South Korea, and Southeast Asia that is simultaneously the source of global supply chain disruption risk and the primary adopter of technology to manage it. Government-led supply chain modernization programs in Japan, South Korea, and India add institutional investment alongside the commercial technology adoption that regional enterprises pursue independently.

China Supply Chain Resilience Market Insights

China leads Asia Pacific supply chain resilience investment through the scale of its manufacturing and logistics operations, state investment in domestic supply chain technology vendors, and the growing recognition among Chinese exporters that supply chain visibility is essential for maintaining customer relationships with global enterprises demanding supplier transparency.

Latin America and Middle East & Africa Supply Chain Resilience Market Insights

Latin America held a 7.92% share in 2025 at USD 2.24 Billion, growing to USD 6.20 Billion by 2035 at a CAGR of 10.78%. Brazil leads through technology investment by its large manufacturing and agri-food export sectors, with retail companies driving supply chain visibility adoption as they manage distribution across a geographically diverse national market. Middle East & Africa held a 5.06% share in 2025 at USD 1.43 Billion, growing at a faster CAGR of 12.60% to USD 4.67 Billion by 2035, driven by Gulf state supply chain diversification programs and UAE-based trade and logistics operators investing in digital supply chain capability.

Competitive Landscape for Supply Chain Resilience Market:

IBM Corporation

IBM participates in the supply chain resilience market through its Sterling Supply Chain Suite, Watson AI-powered supply chain management capabilities, and global consulting services that help enterprises implement and integrate resilience technology across complex multi-system environments. The company’s competitive position combines platform technology with deep consulting practice, addressing both the software procurement and the organizational implementation challenges that determine whether resilience investments deliver value.

In March 2025, IBM announced the integration of its Sterling Intelligent Promising platform with generative AI capabilities enabling supply chain planners to query inventory and order management data in natural language, reducing the time to identify fulfillment risks and generate alternative sourcing recommendations from hours to minutes.

Kinaxis

Kinaxis is a Canadian supply chain management software company that built its market position through the RapidResponse platform, which combines supply chain planning, execution monitoring, and scenario simulation in a concurrent planning environment. The platform’s distinguishing capability is continuous what-if analysis against live data, allowing planners to see the downstream impact of any supply or demand change immediately rather than waiting for batch planning cycles a capability that has been validated in large manufacturer deployments across automotive, aerospace, pharmaceutical, and consumer goods sectors.

In February 2025, Kinaxis acquired MPO (Management of Procurement and Operations), a supply chain orchestration platform specializing in multi-party logistics visibility and execution, extending Kinaxis’ capability from supply chain planning into real-time logistics execution and addressing customer demand for a platform that bridges strategic planning and day-to-day fulfillment management.

Supply Chain Resilience Market Key Players:

-

Schneider Electric

-

Cisco Systems

-

Microsoft

-

IBM

-

SAP

-

Oracle

-

Infor

-

Kinaxis

-

Blue Yonder

-

Manhattan Associates

-

Coupa Software

-

E2open

-

Project44

-

FourKites

-

Resilinc

-

Everstream Analytics

-

Accenture

-

Deloitte

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 28.24 Billion |

| Market Size by 2035 | USD 82.90 Billion |

| CAGR | CAGR of 11.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution Type (Risk Management & Monitoring Solutions, Supply Chain Planning & Analytics, Inventory & Warehouse Management Solutions, Supplier & Logistics Management Solutions) • By Application (Risk Identification & Mitigation, Demand Forecasting & Planning, Supplier Risk & Performance Management, Logistics & Transportation Optimization) • By End-User (Manufacturing, Retail & E-commerce, Healthcare & Pharmaceuticals, Logistics & Transportation) • By Deployment Mode (On-Premise, Cloud-Based) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schneider Electric, Cisco Systems, Microsoft, IBM, Honeywell International, SAP, Oracle, Infor, Kinaxis, Blue Yonder, Manhattan Associates, Coupa Software, Descartes Systems Group, E2open, Project44, FourKites, Resilinc, Everstream Analytics, Accenture, Deloitte |

Frequently Asked Questions

North America dominated the Supply Chain Resilience Market in 2025

Port & Critical Infrastructure Security dominated the Supply Chain Resilience Market

Increasing supply chain disruptions, growing demand for real-time visibility, rising adoption of digital technologies, and the need for risk mitigation and business continuity are driving the Supply Chain Resilience Market.

The Supply Chain Resilience Market size was USD 28.24 Billion in 2025 and is expected to reach USD 82.90 Billion by 2035.

The Supply Chain Resilience Market is expected to grow at a CAGR of 11.42% from 2026–2035.

Get in Touch