AI in Construction Market Report Scope & Overview:

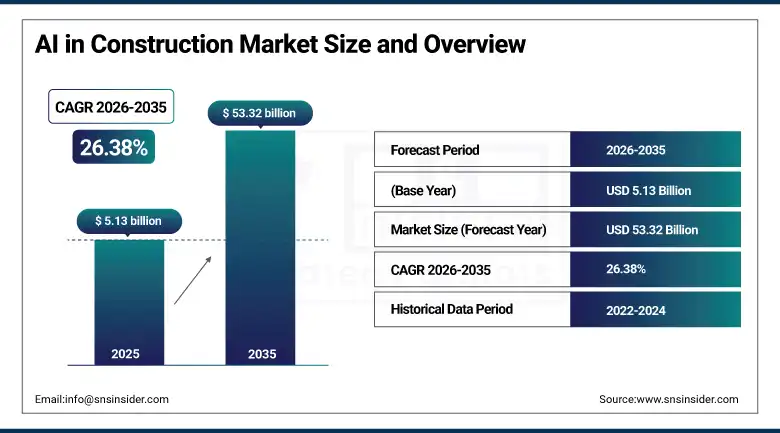

The AI in Construction market was valued at USD 5.13 billion in 2025 and is expected to reach USD 53.32 billion by 2033, growing at a CAGR of 26.38% from 2026–2035.

Artificial Intelligence (AI) is revolutionizing the construction industry across the world in record time. The applications of AI technology range from planning and scheduling to safety and inspection and even resource management. Construction projects have traditionally been marked by poor productivity levels and high project cost overruns. The implementation of AI technology is specifically solving these problems. Machine learning algorithms predict project schedules more accurately than traditional predictive models. Computer vision helps monitor safety issues continuously within construction sites. Robots perform routine and laborious construction processes without error. The fusion of AI technology with Building Information Management platforms is generating seamless integrated construction management across the globe. Early adopters are recording productivity gains of between 15% and 25%. Industry experts have categorized AI as essential technology until 2035.

Women's healthcare visits reached 1.2 billion in 2025, driven by rising demand for reproductive, fertility, and preventive care globally. AI in construction is similarly driven by structural demand: over 40 million construction workers globally face skills shortages that automation is addressing.

Market Size and Forecast

-

Market Size in 2026E: USD 6.48 Billion

-

Market Size by 2035: USD 53.32 Billion

-

CAGR: 26.38% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On AI in Construction Market - Request Free Sample Report

AI in Construction Market Trends

-

Predictive analytics, powered by AI, is helping in mitigating the risks of cost overruns during projects. The real-time data collected through IoT sensors helps in proactively managing budgets and schedules.

-

The monitoring of site safety using computer vision technology has been increasingly adopted. Cameras combined with AI technologies help in identifying any violations of PPEs and risky behaviors at construction sites.

-

Generative AI technology is increasingly helping in designing buildings faster. Using AI technology helps architects design building models in hours instead of days and weeks.

-

AI technology is increasingly used in autonomous machines performing construction tasks such as site preparation, digging trenches, laying pipes, and pouring concrete.

-

The construction sector has increasingly adopted digital twins for mega-projects. AI-enabled digital twin technology helps simulate the construction process digitally.

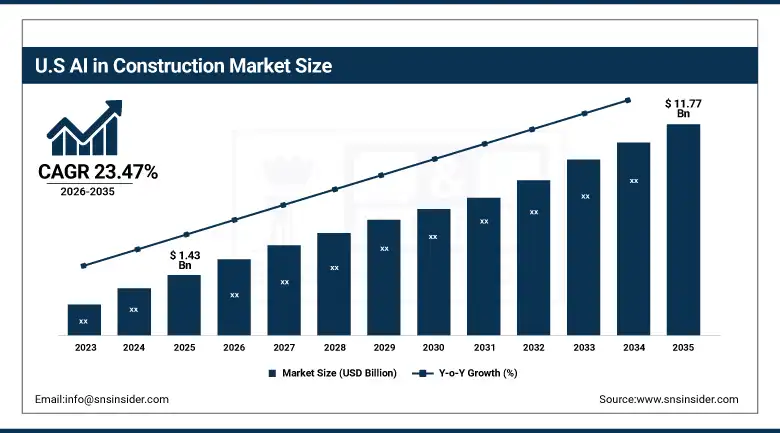

The U.S. AI in Construction Market Outlook

The U.S. AI in Construction Market was valued at approximately USD 1.43 billion in 2025 and is expected to reach approximately USD 11.77 billion by 2035, growing at a CAGR of 23.47%.

The United States is a leader when it comes to advanced AI technology in the construction industry. It is ranked highest when it comes to the number of start-ups involved in construction technology and also high when it comes to the investment in venture capital in construction technology. The Infrastructure Investment and Jobs Act ensures the consistent demand for advanced construction technology in public works. In the U.S., there is a labour shortage problem in the construction industry because there are more than 500,000 construction jobs that remain open by 2025. The big construction companies like Turner Construction Company and Bechtel have also started using AI technology. The implementation of AI technology in the U.S. is driven by the integration between construction technology vendors and big contractors.

OSHA recordable incident rates in U.S. construction remain significantly above other industries. AI-powered safety monitoring systems are demonstrating measurable incident rate reductions of 20 to 35% in early commercial deployments across major project sites.

AI in Construction Market Segment Analysis

-

By Type of Offering, in 2025, the major share was held by Software (57.42%) that uses AI technologies to plan projects, manage safety, and conduct predictive analysis; meanwhile, the fastest growing type is the one involving Services with a CAGR of 32.84%, which requires integration and implementation efforts.

-

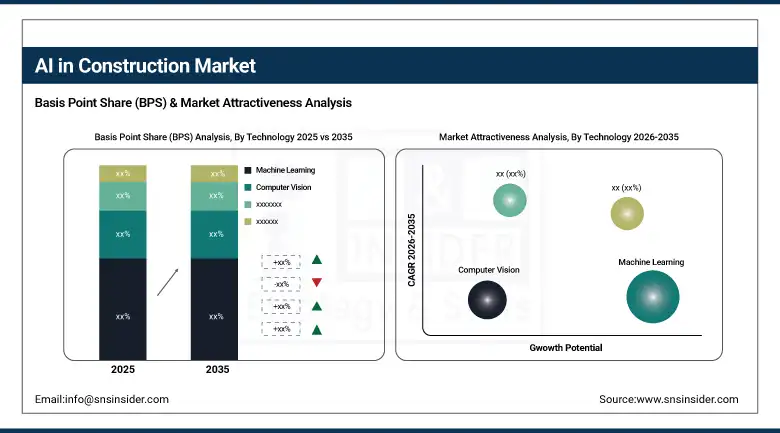

By Type of Technology, in 2025, Machine Learning Technologies had the biggest share (45.18%) of all available types using the technologies to make automatic decisions, predict resources and costs of projects; on the other hand, Robotics Technologies had the highest growth rate (CAGR of 35.67%), offering services with robotic bricklayers, autonomous vehicles, and drones.

-

By Application, in 2025, Project Planning & Design occupied the first position with the share of 38.72% using technologies for modeling, project scheduling, and resource optimization; at the same time, Safety & Risk Management became the fastest growing application area with CAGR of 36.21%.

-

By End-Use, Infrastructure held the largest share in 2025 through government investment in roads, bridges, and energy projects; Commercial construction is the fastest-growing end-use driven by smart building adoption and cost efficiency pressure.

By Technology, Machine Learning dominates, Robotics is expected to grow fastest

Machine Learning remained the leading technology segment, accounting for roughly 45.18% share of the revenue in AI in Construction Market in 2025. Machine learning models analyze large amounts of data associated with the construction projects and detect patterns, make predictions regarding potential project delays and allocate resources efficiently. The application of machine learning in construction is facilitated through project management software systems utilized by big global contractors. Machine learning-based cost estimation models allow achieving better cost estimates than conventional manual ones. Project schedule optimization algorithms can detect the critical path and suggest necessary changes. The diversity of applications and opportunities of machine learning in construction explains its widespread adoption among all construction sectors.

Robotics is the fastest growing technology sub-segment with a CAGR of 35.67% till 2033. Robotic brick laying devices from firms such as Construction Robotics and FBR are capable of laying bricks at three times faster than their human counterparts. Autonomous earthwork equipment is making earthworks processes more efficient by lowering their cost and increasing accuracy levels. Automated drone inspection devices perform surveys on a construction site within hours compared to the several days it would take for human inspections. The dual factors of labour shortage and low costs of robotic equipment have sped up implementation processes.

By Application, Project Planning & Design dominates, Safety & Risk Management is expected to grow fastest

Project Planning and Design was the leading application with revenue shares of around 38.72% in 2025. The use of AI-based BIM systems enables collaboration in real-time between architects, engineers, and constructors during complex projects' design. Generative design systems offer several viable design alternatives by AI that satisfy structural, energy, and cost requirements simultaneously. Schedule simulations detect problems related to conflict and improper sequencing even before any site activities commence. AI algorithms provide solutions to proper labor force, machinery, and materials allocation. The widespread use of the application in practice is confirmed by high rates of adoption by top tier contractors worldwide.

Safety and Risk Management application is expected to show the highest growth rate with 36.21% CAGR over 2025-2033 period. The construction industry is among the most dangerous in the world concerning fatalities and severe injuries. AI-driven computer vision algorithms analyze video footage constantly looking for violations such as failure to wear protective clothing and unsafe behavior. AI near miss analysis helps to prevent accidents in a proactive way. Monitoring of workers' fatigue through biometrics sensors allows detecting risk conditions immediately. Compliance reports generation is automated through logs analysis of the monitoring process.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.7% |

|

Europe |

Germany |

25.4% |

|

Asia Pacific |

China |

48.3% |

|

Middle East & Africa |

UAE |

29.7% |

|

Latin America |

Brazil |

43.6% |

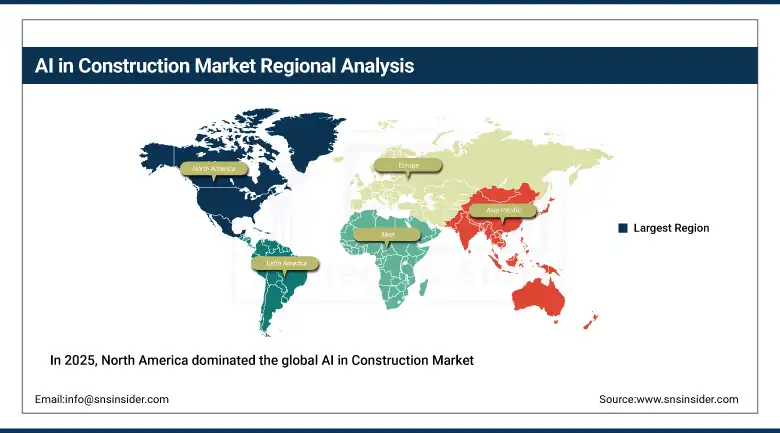

North America AI in Construction Market Insights

In 2025, North America dominated the global AI in Construction Market. It is estimated that the United States makes up roughly 83.7% of the North American share. Significant government investments in infrastructure projects have spurred considerable demand for AI-driven project management software. The presence of numerous construction technology startups and venture capital funding ensures fast-paced innovation cycles. Labor shortage remains the chief business reason behind adopting automation solutions in any size and type of project. Leading tier-one contractors are implementing AI-driven solutions consistently throughout their entire project portfolio around the globe. Canada continues its growth due to heavy investment programs related to transportation, energy, and housing infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Construction Market Insights

Europe is a technically sophisticated AI in construction market. Germany accounts for approximately 25.4% of European revenues through its strong industrial automation culture. The EU's Green Deal is driving demand for AI tools that optimise building energy performance during design. BIM mandates across several European countries are creating the data infrastructure that AI analytics requires. The UK, France, and Netherlands are all recording strong AI construction platform adoption. European construction companies are investing heavily in digital transformation to compete on cost efficiency.

Asia Pacific AI in Construction Market Insights

Asia Pacific is the fastest-growing AI in construction market globally. China accounts for approximately 48.3% of Asia Pacific revenues through its vast construction activity and smart city programmes. China's Belt and Road infrastructure projects are deploying AI project management at unprecedented geographic and financial scale. India's smart city mission and infrastructure expansion are creating large and sustained AI construction demand. Japan and South Korea are deploying advanced robotics and AI to offset aging and shrinking construction labour forces. Australia's major mining and infrastructure projects are early adopters of AI monitoring and autonomous machinery systems. Government-backed digitalisation incentives across the region are accelerating platform adoption timelines significantly. The region's extraordinary construction activity volume creates the largest single-region AI construction technology opportunity globally.

MEA & Latin America AI in Construction Market Insights

The Middle East & Africa and Latin America are developing artificial intelligence in construction. In MEA, UAE accounts for around 29.7% of revenues thanks to its extensive programmes of building smart cities and mega-projects. Saudi Arabia's Vision 2030 programme is investing in large amounts of infrastructure and NEOM projects, which use AI in construction. In Latin America, the largest share goes to Brazil, accounting for around 43.6% due to big infrastructure and housing projects. The urbanisation of both regions has led to continuous construction, where artificial intelligence plays a key role.

Market Dynamics

Growth Drivers: Construction labour shortages, safety imperatives, and government infrastructure investment are driving global AI in construction market growth.

Labour shortages in the construction industry are affecting more than 40 million jobs worldwide. The labor shortage crisis is making an interesting and measurable ROI case for investment in automation and robotics solutions using AI. There is substantial infrastructure spending on government projects in the US, EU, and Asia that have benefited and will continue to benefit from AI tools used in construction. Safety requirements are becoming stricter worldwide, and there is an increasing need for AI solutions that can monitor and comply with these requirements. Projects are becoming increasingly complex, and construction is becoming more ambitious with regard to performance and sustainable objectives. This means that it is important for any contractor to adopt AI in their construction planning process and reduce risks. On average, large projects exceed the budget by 80%. AI technologies have been able to provide a clear ROI through fewer reworks, faster scheduling, and fewer incidents.

Restraints: High implementation costs, data quality challenges, and workforce resistance are restraining AI in construction market adoption across smaller firms.

Implementing AI involves substantial expenditure on the required infrastructure. The smaller contractors and sub-contractors may have budgetary constraints leading to delayed uptake of technology. Construction project data reliability varies among project management systems and contractor organizations. Old processes and conservative approaches of established contractor firms may be an impediment to implementing technology. Connected construction sites cybersecurity weaknesses become another potential threat category. Qualified individuals for implementing AI are few compared to the growing demands in the industry. Standardization of the data used by AI platforms is yet another major issue in the process of adopting AI. Showing the ROI for the skeptics involved in construction projects would involve substantial expenditures.

Opportunities: Integration of AI with BIM, drone inspection automation, and smart infrastructure programmes create significant growth opportunities globally.

AI integration with Building Information Modelling platforms creates fully connected design-to-delivery project management ecosystems. Drone-based automated inspection programmes reduce site survey costs by 60 to 80% versus manual methods. Smart city infrastructure programmes across Asia, Middle East, and North America create large-scale AI construction demand. Prefabrication and modular construction growth is creating new AI quality control and logistics optimisation applications. Insurance and bonding companies are beginning to reward AI safety programme adoption with premium reductions. These incentives accelerate adoption among cost-conscious mid-market contractors who are price-sensitive to new technology investment. Carbon accounting and embodied carbon optimisation tools powered by AI are creating a new design-phase application category. Construction financiers are progressively requiring AI risk monitoring as a loan covenant condition on large infrastructure projects.

Recent Developments:

-

2025: Autodesk extended its Construction IQ platform that uses artificial intelligence to offer prediction-based safety and scheduling risks analytics to construction projects.

-

2025: Trimble introduced AI-enabled versions of its SketchUp and Tekla BIM platforms that come with generative design tools. The software enables engineers to generate hundreds of viable design iterations at once.

-

2025: Hilti Group began implementing an AI-based tool tracking and predictive maintenance system in its fleet management system, leading to a 30% reduction in downtime and automated documentation for construction contractors.

-

2025: Built Robotics announced a wider roll-out of its autonomous excavation systems based on artificial intelligence. These machines spent over 500,000 autonomous earthwork hours in operation at commercial construction sites.

-

2025 July: Komatsu presented a next-gen SmartConstruction platform with the latest drones, AI earthworks planning, and autonomous machine guidance. The platform cut the project setup time in half during trials.

AI in Construction Market Key Players are:

-

Autodesk Inc.

-

Trimble Inc.

-

Oracle Corporation (Aconex)

-

Procore Technologies Inc.

-

Bentley Systems Inc.

-

Komatsu Ltd. (SmartConstruction)

-

Built Robotics Inc.

-

Hilti Group

-

Doxel Inc.

-

Buildots Ltd.

-

Nemetschek Group

-

Hexagon AB

-

Topcon Corporation

-

Skanska AB

-

Turner Construction Company

-

IBM Corporation

-

Microsoft Corporation (Azure)

-

Amazon Web Services Inc.

-

NVIDIA Corporation

-

Palantir Technologies Inc.

AI in Construction Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.13 Billion |

| Market Size by 2035 | USD 53.32 Billion |

| CAGR | CAGR of 26.38% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Software, Services, Hardware) • By Technology (Machine Learning, Computer Vision, Natural Language Processing, Robotics, Others) • By Application (Project Planning & Design, Safety & Risk Management, Asset Monitoring, Supply Chain Management, Others) • By End-Use (Commercial, Residential, Industrial, Infrastructure) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Autodesk Inc., Trimble Inc., Oracle Corporation (Aconex), Procore Technologies Inc., Bentley Systems Inc., Komatsu Ltd. (SmartConstruction), Built Robotics Inc., Hilti Group, Doxel Inc., Buildots Ltd., Nemetschek Group, Hexagon AB, Topcon Corporation, Skanska AB, Turner Construction Company, IBM Corporation, Microsoft Corporation (Azure), Amazon Web Services Inc., NVIDIA Corporation, Palantir Technologies Inc. |

Frequently Asked Questions

North America dominated the AI in Construction Market in 2025.

Machine Learning dominated with approximately 45.18% of revenues in 2025.

Construction labour shortages, tightening safety regulations, and government infrastructure investment are the primary growth drivers. AI tools are demonstrating measurable ROI through reduced cost overruns and incident rates.

The AI in Construction Market was valued at USD 5.13 billion in 2025.

The AI in Construction Market is expected to grow at a CAGR of 26.38% from 2026 to 2035.

Get in Touch