AI in Financial Services Market Report Scope & Overview:

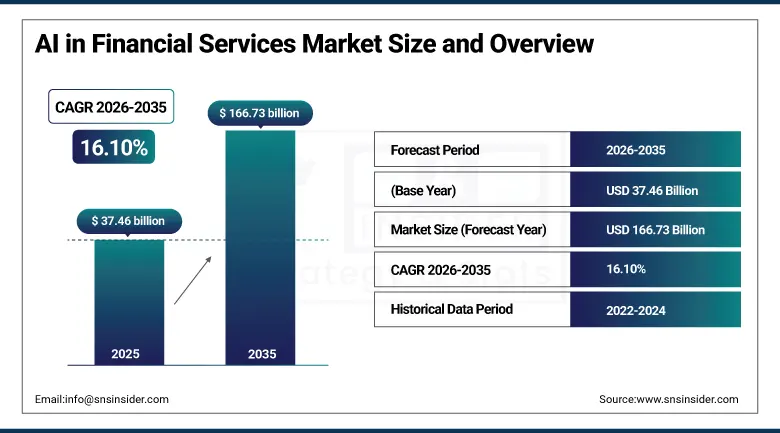

The AI in Financial Services Market was valued at USD 37.46 Billion in 2025 and is expected to reach USD 166.73 Billion by 2035, growing at a CAGR of 16.10% from 2026–2035.

The global AI in financial services market is advancing rapidly. Financial institutions are deploying AI to automate processes, enhance fraud detection, personalise customer service, and improve investment decision-making at a scale and speed that human analyst teams cannot match. In 2024, 85% of financial institutions had adopted or were piloting AI across at least one business function. Machine learning dominates as the primary technology, enabling predictive analytics, credit scoring improvement, and fraud pattern recognition that rule-based systems cannot achieve.

JPMorgan Chase deployed its IndexGPT AI financial advisory service and expanded its COiN contract intelligence platform in 2024, using LLMs to extract and classify data from financial agreements at a rate equivalent to 360,000 man-hours of legal analysis annually. The deployment reflects the extraordinary commercial leverage that AI delivers in financial document processing, creating a competitive differentiation in operational efficiency that sustains above-average technology investment commitment from the world’s most profitable financial institution.

Market Size and Forecast

-

Market Size in 2026E: USD 43.47 Billion

-

Market Size by 2035: USD 166.73 Billion

-

CAGR: 16.10% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On AI in Financial Services Market - Request Free Sample Report

AI in Financial Services Market Trends

-

Generative AI adoption in financial services is accelerating across document processing, regulatory report generation, customer-facing conversational banking.

-

AI-powered fraud detection systems using real-time transaction behavioural analytics are reducing false positive rates while improving detection accuracy.

-

Explainable AI regulation for credit decisioning is creating structured investment in model interpretability, bias auditing, and regulatory documentation capability.

-

Autonomous AI agents for portfolio management and algorithmic trading are progressing from rule-based execution to adaptive learning systems that adjust strategy parameters in response to real-time market microstructure data.

-

AI-native challenger banks and embedded finance platforms are deploying AI as foundational infrastructure rather than an overlay, creating commercial pressure on incumbent institutions to accelerate their own AI transformation programmes.

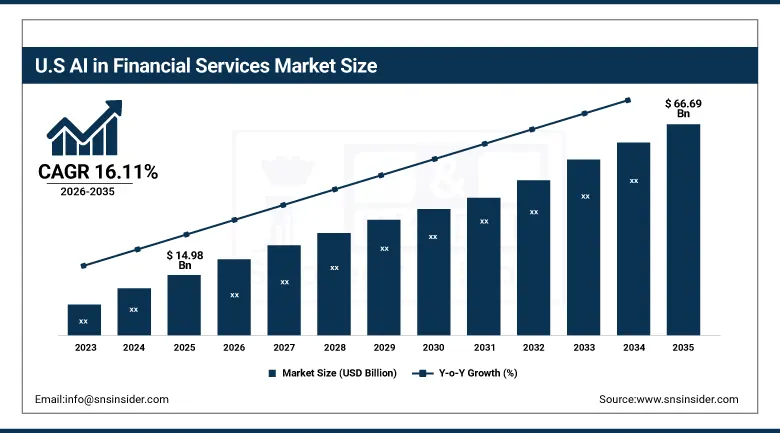

U.S. AI in Financial Services Market Outlook

The U.S. AI in Financial Services Market was valued at approximately USD 14.98 Billion in 2025 and is expected to reach approximately USD 66.69 Billion by 2035, growing at a CAGR of approximately 16.11%.

The U.S. is the world’s largest AI in financial services market. JPMorgan Chase, Goldman Sachs, Citigroup, and Bank of America collectively invest billions annually in AI across fraud prevention, trading, compliance, and customer service. Regulatory guidance from OCC, SEC, and CFPB on AI fairness, explainability, and model risk management is creating compliance investment in AI governance capability alongside operational AI programmes.

Goldman Sachs expanded its GS AI Platform in 2025, deploying LLM-powered tools for equity research summarisation, regulatory filing analysis, and internal knowledge management across its investment banking and asset management divisions. The platform reduces analyst time on information retrieval by an estimated 40%, enabling senior professionals to focus on judgment-intensive tasks whose strategic value justifies the technology investment cost at scale.

AI in Financial Services Market Segment Analysis

-

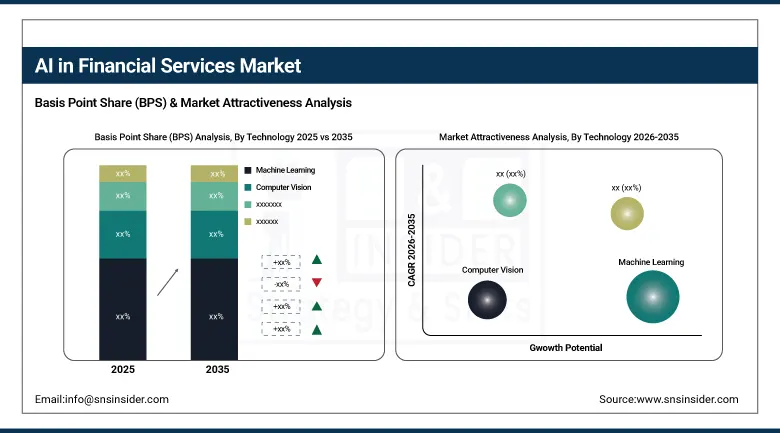

By Technology, the Machine Learning segment dominated the AI in Financial Services Market with approximately 46.00% share in 2025, while the Natural Language Processing segment is the fastest growing with a CAGR of approximately 18.90% during the forecast period.

-

By Deployment, the On-Premise segment dominated the AI in Financial Services Market with approximately 57.00% share in 2025, while the Cloud-Based segment is the fastest growing with a CAGR of approximately 18.20% during the forecast period.

-

By Size of Financial Institution, the Large Enterprises segment dominated the AI in Financial Services Market with approximately 69.00% share in 2025, while the SMEs segment is the fastest growing with a CAGR of approximately 19.40% during the forecast period.

-

By Application, the Fraud Detection & Prevention segment dominated the AI in Financial Services Market with approximately 28.00% share in 2025, while the Regulatory Compliance segment is the fastest growing with a CAGR of approximately 19.80% during the forecast period.

By Technology, machine learning dominates, NLP grows fastest

Machine learning retained the dominant technology position in the AI in financial services market in 2024. Its commercial primacy reflects ML’s decades of production deployment in credit scoring, fraud detection, and algorithmic trading whose proven commercial ROI creates institutional confidence that newer AI techniques have not yet matched across the full breadth of financial application categories. ML models that continuously retrain on transaction data, market pricing, and customer behaviour provide the adaptive pattern recognition capability that rule-based systems cannot sustain as financial crime and market conditions evolve.

NLP is the fastest-growing technology at approximately 18.90% CAGR because generative AI’s commercial maturation has created viable NLP applications across financial services that were previously prohibitively expensive or technically inadequate. LLM-powered contract analysis, regulatory filing review, earnings call summarisation, and conversational banking are each commercial use cases whose deployment is accelerating across institutional and retail banking segments simultaneously. The SEC’s acceptance of AI-assisted regulatory filing preparation and the CFPB’s conversational AI guidance create regulatory precedent that sustains NLP programme investment confidence.

By Application, fraud detection dominates, regulatory compliance grows fastest

Fraud detection and prevention retained the dominant application position in the AI in financial services market in 2025. Its commercial leadership reflects the quantifiable and immediate financial return that AI-powered fraud prevention delivers. AI fraud detection systems using behavioural biometrics, device fingerprinting, and transaction graph analysis identify fraudulent activity with 20-30% lower false positive rates than rule-based predecessors while improving detection coverage. Each percentage point of fraud loss reduction translates directly into measurable financial improvement whose ROI calculation sustains consistent AI investment across banking, card payments, and insurance claims management.

Regulatory compliance is the fastest-growing application because the scope and complexity of financial regulation continue expanding across Basel IV, DORA, MiFID II reporting, AML/KYC requirements, and ESG disclosure obligations that collectively create compliance workloads whose manual management cost is growing faster than compliance staffing budgets can accommodate. AI systems that automatically extract, classify, and map regulatory data to reporting templates, monitor transaction flows for sanctions and AML patterns, and generate audit-ready compliance documentation create operational leverage that compliance-intensive financial institutions require to manage expanding regulatory obligations within controlled headcount.

By Deployment, on-premise dominates, cloud grows fastest

On-premise deployment retained the dominant position with approximately 57% of the AI in financial services market in 2025. Financial services’ regulatory requirements, data sovereignty obligations, and cybersecurity standards create institutional preference for AI infrastructure that maintains complete data control within institutional boundaries. Model risk management frameworks from OCC and Federal Reserve require explainable, auditable AI whose on-premise deployment enables the monitoring, logging, and validation infrastructure that model risk governance requires.

Cloud-based AI deployment is the fastest-growing model because cloud platforms’ AI infrastructure, pre-trained model availability, and consumption-based pricing create compelling economics for financial services applications that do not process regulated personal financial data. Market data processing, investment research aggregation, internal knowledge management, and customer-facing chatbot infrastructure are increasingly cloud-deployed as financial institutions distinguish between regulated workloads that require on-premise control and non-regulated workloads where cloud AI economics and capability exceed on-premise alternatives.

By Institution Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant institution size position in the AI in financial services market in 2025. Their leadership reflects the direct relationship between institutional scale and AI deployment advantage. Large banks possess the extensive historical transaction data whose volume enables effective ML model training, the data science talent whose expertise enables sophisticated model development, and the technology investment budget whose scale enables proprietary model development beyond what off-the-shelf AI products deliver.

SMEs are the fastest-growing segment because the AI-as-a-service model is making enterprise-grade financial AI commercially accessible to community banks, credit unions, insurance brokers, and wealth management firms whose budgets previously excluded them from the AI investment that large institutions treat as standard infrastructure. Fraud detection APIs, automated credit underwriting services, and conversational banking platforms whose per-account pricing makes AI economically viable at SME transaction volumes are creating first-time AI adoption across a customer segment whose aggregate count substantially exceeds the large institution market.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

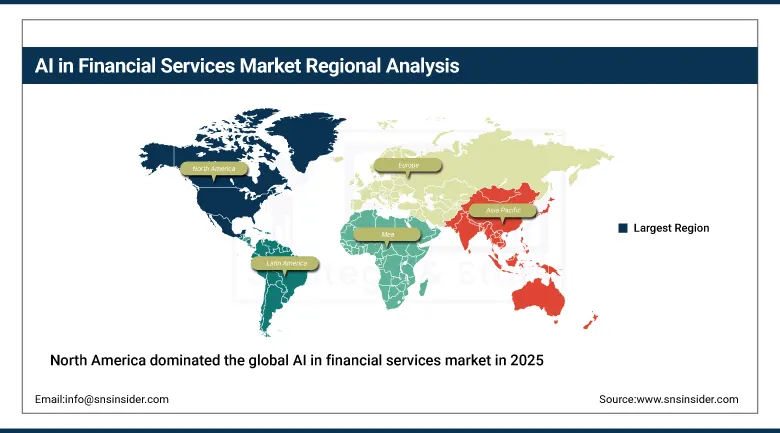

North America AI in Financial Services Market Insights

North America dominated the global AI in financial services market in 2025 with approximately 40% of global revenues. The United States accounts for approximately 87.4% of North American revenues. The world’s largest financial institutions, most sophisticated fintech ecosystem, and the most advanced regulatory framework for AI model risk governance collectively define the U.S. market’s commercial leadership. JPMorgan Chase, Goldman Sachs, Visa, Mastercard, and PayPal are each deploying AI at a scale whose institutional investment creates the market’s technology benchmark.

Canada contributes approximately 12.6% of North American revenues through its major banks’ AI investment programmes in fraud detection and customer analytics, the Toronto and Montreal fintech ecosystems, and the federal government’s AI strategy whose financial services applications create structured institutional procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe AI in Financial Services Market Insights

Europe is a sophisticated AI in financial services market where the EU AI Act’s risk classification for AI credit scoring and insurance pricing models, GDPR’s automated decision-making constraints under Article 22, and DORA’s operational resilience requirements collectively create a compliance-conscious AI deployment environment that prioritises explainability and governance. Germany accounts for approximately 22.3% of European revenues through its large banking sector’s AI investment, Deutsche Bank and Allianz’s AI programme leadership, and the Frankfurt fintech corridor’s active application development.

The United Kingdom and Switzerland are significant secondary markets where the FCA’s AI regulatory framework, London’s fintech investment concentration, and the private banking sector’s AI-powered wealth management adoption create consistent above-average AI financial services investment that sustains market growth independently of EU regulatory trajectory.

Asia Pacific AI in Financial Services Market Insights

Asia Pacific is the fastest-growing regional AI in financial services market, driven by China’s fintech ecosystem’s scale, India’s digital financial services transformation, and Japan and South Korea’s incumbent banking sector AI modernisation. China accounts for approximately 44.8% of Asia Pacific revenues through Alibaba’s Ant Group, Tencent’s WeChat Pay ecosystem, and the domestic banking sector’s AI deployment scale that serves 1.4 billion consumers whose digital financial data creates the largest AI training dataset of any national financial market.

India is the most commercially dynamic emerging market within Asia Pacific. The UPI payment infrastructure’s real-time transaction data, the OCEN open credit framework, and the fintech sector’s AI credit scoring deployment for previously unbanked populations are creating commercially innovative AI financial applications whose global precedent value is progressively recognised by international financial institutions seeking proven models for emerging market AI deployment.

MEA & Latin America AI in Financial Services Market Insights

The Middle East and Africa and Latin America are growing AI in financial services markets where mobile-first financial services, growing fintech investment, and government financial inclusion mandates are creating structured AI adoption. UAE leads MEA revenues at approximately 38.4% through the DIFC fintech ecosystem, CBUAE AI financial innovation programme, and global financial institution headquarters operations whose international AI standards require UAE operations to maintain equivalent capability.

Brazil leads Latin American revenues at approximately 44.2% through its Pix instant payment ecosystem, Nubank’s AI-native challenger bank model, and the BCB Open Finance framework whose data portability creates AI training data infrastructure that sustains fintech and incumbent AI investment across the Latin American region’s most commercially sophisticated financial market.

Market Dynamics

Growth Drivers: Fraud loss reduction delivering measurable AI ROI and LLM deployment creating new financial services automation applications

Quantifiable fraud loss reduction is the AI in financial services market’s most commercially irresistible growth driver. The global financial fraud cost exceeds USD 5 trillion annually. AI detection systems that demonstrably reduce fraud loss by even fractional percentages deliver financial returns that dwarf their implementation cost. This ROI calculation sustains AI investment through economic cycle variation because fraud loss reduction directly improves financial institution profitability without requiring revenue growth. Each basis point of fraud rate improvement creates measurable earnings improvement whose board-level visibility sustains technology investment commitment.

LLM-powered automation is creating a second wave of AI in financial services adoption that extends beyond established fraud and credit applications into the knowledge work domains of investment research, regulatory compliance, legal review, and customer advisory that collectively represent the majority of high-cost professional labour in financial services. Each successful LLM deployment that demonstrably reduces analyst or compliance officer time on routine information processing tasks creates a reference case whose documented ROI accelerates adoption across peer institutions whose cost structures face the same operational efficiency pressure.

Restraints: Model risk governance complexity and EU AI Act explainability requirements limiting autonomous AI decision-making

Model risk governance frameworks from OCC, Federal Reserve, and equivalent national regulators require financial institutions to validate, document, and monitor every AI model used in credit decisioning, trading, and customer-facing applications. This governance overhead creates implementation cost and timeline extension that slows AI programme scaling. Institutions must demonstrate that AI models perform as expected, do not exhibit discriminatory bias, and can be explained to regulators and customers whose adverse action notifications require model decision reasoning.

The EU AI Act’s classification of credit scoring, insurance pricing, and employment finance applications as high-risk AI systems requiring transparency, human oversight, and bias documentation creates additional compliance investment requirements for European financial services AI programmes. Institutions whose AI models cannot satisfy Article 13 transparency or Article 14 human oversight requirements face regulatory prohibition from deploying those systems in EU markets, creating commercial constraints that do not apply in less stringent regulatory jurisdictions.

Opportunities: GenAI financial advisory at scale and embedded finance AI creating new commercial models

Generative AI financial advisory represents the most commercially transformative near-term opportunity in the AI in financial services market. LLM-powered advisory systems that provide personalised investment guidance, tax optimisation suggestions, and retirement planning scenarios to retail customers at institutional quality and at marginal technology cost per interaction fundamentally change the economics of financial advisory whose traditional model limited quality advice to high-net-worth customers who could justify human advisor fees.

Embedded finance AI is creating new commercial models by integrating financial services decisioning into non-financial application contexts. Buy-now-pay-later decisioning within e-commerce checkout flows, SME credit underwriting within accounting software, and insurance pricing within vehicle purchase flows each deploy AI financial services capabilities where customer conversion probability is highest. Each embedded finance integration creates a new distribution channel for AI-powered financial products whose commercial performance improves with each data learning cycle.

Recent Developments:

-

2024: JPMorgan Chase expanded its COiN contract intelligence platform and deployed IndexGPT AI financial advisory in 2024, using LLMs to process financial agreements at a rate equivalent to 360,000 man-hours of legal analysis annually and deliver AI-powered investment recommendations to retail customers.

-

2025: Goldman Sachs expanded its GS AI Platform in 2025 with LLM-powered equity research summarisation, regulatory filing analysis, and internal knowledge management tools, reducing analyst information retrieval time by an estimated 40% across investment banking and asset management divisions.

-

2025: Visa expanded its AI-powered risk and fraud management capabilities in 2025, deploying real-time deep learning models across its global payment network that analyse over 500 data elements per transaction to distinguish legitimate from fraudulent activity within 100 milliseconds of each transaction initiation.

AI in Financial Services Market Key Players

-

JPMorgan Chase

-

Goldman Sachs

-

IBM

-

Microsoft

-

Google

-

Amazon Web Services

-

Salesforce

-

Oracle

-

SAP

-

Visa

-

Mastercard

-

PayPal

-

Nuance Communications

-

FICO

-

SAS Institute

-

Temenos

-

Thought Machine

-

Featurespace

-

Behavox

-

Kensho Technologies

AI in Financial Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 37.46 Billion |

| Market Size by 2035 | USD 166.73 Billion |

| CAGR | CAGR of 16.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Technology (Machine Learning, Natural Language Processing, Robotic Process Automation, Computer Vision) • by Deployment (Cloud-Based, On-Premise) • by Size of Financial Institution (Large Enterprises, SMEs) • by Application (Fraud Detection & Prevention, Customer Service & Chatbots, Credit Scoring & Risk Management, Algorithmic Trading, Wealth Management & Robo-Advisors, Regulatory Compliance, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | JPMorgan Chase, Goldman Sachs, IBM, Microsoft, Google, Amazon Web Services, Salesforce, Oracle, SAP, Visa, Mastercard, PayPal, Nuance Communications, FICO, SAS Institute, Temenos, Thought Machine, Featurespace, Behavox, Kensho Technologies |

Frequently Asked Questions

The AI in Financial Services Market is expected to grow at a CAGR of 16.10% from 2026 to 2035.

The AI in Financial Services Market was valued at USD 37.46 Billion in 2025.

Quantifiable fraud loss reduction delivering immediate and measurable AI ROI that sustains investment through economic cycles, and LLM deployment creating new automation opportunities across investment research, regulatory compliance, and customer advisory that previously required expensive professional labour.

Fraud Detection & Prevention dominated the AI in Financial Services Market in 2025 as the highest-ROI and most universally deployed AI application across banking, insurance, and payment processing organisations globally.

North America dominated the AI in Financial Services Market in 2025 with approximately 40% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch