Aircraft Water and Waste Systems Market Report Scope & Overview:

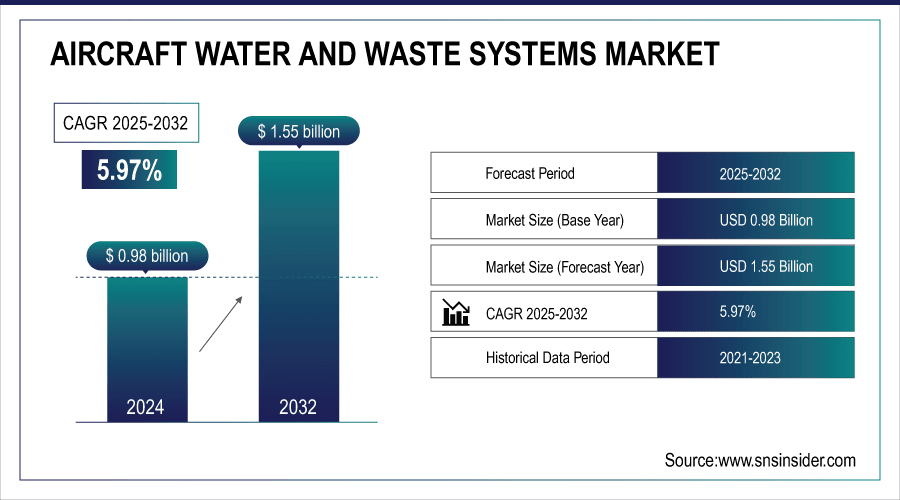

The Aircraft Water and Waste Systems Market size was valued at USD 1.04 Billion in 2025 and is projected to reach USD 1.85 Billion by 2035, growing at a CAGR of 5.97% during 2026-2035.

The Aircraft Water and Waste Systems Market is expanding steadily, owing to the increasing number of air travelers and the increasing standards of hygiene. These critical systems ensure that the passengers have access to clean drinking water on the aircraft, as well as efficient waste management, which has a direct impact on the comfort and health of the passengers. Research and development is headed in the direction of using lighter materials to reduce fuel consumption, automation for ease of maintenance, and antimicrobial technology to enhance hygiene.

To Get More Information On Aircraft Water and Waste Systems Market - Request Free Sample Report

Key Aircraft Water and Waste Systems Market Trends:

-

Growing air passenger traffic is increasing demand for reliable and hygienic onboard sanitation systems.

-

Rising stringency of international health and sanitation regulations is driving system upgrades and replacements.

-

Advances in lightweight composite materials are reducing system weight and improving aircraft fuel efficiency.

-

Integration of IoT and smart sensors is enabling predictive maintenance and real-time system monitoring.

-

Increasing focus on water conservation is promoting the development of more efficient water management systems.

-

Expansion of long-haul and ultra-long-haul routes is necessitating more robust and higher-capacity systems.

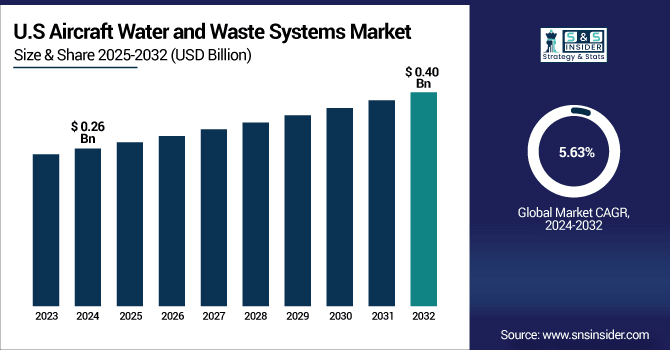

The U.S. Aircraft Water and Waste Systems Market size was valued at USD 0.27 Billion in 2025 and is projected to reach USD 0.47 Billion by 2035, growing at a CAGR of 5.63% during 2026-2035. The U.S. Aircraft Water and Waste Systems Market is driven by a 15% year-over-year increase in mandated health and safety inspections, compelling airlines to upgrade aging infrastructure. The growth in the market is being driven by a 15% year-over-year increase in required health and safety inspections, which is encouraging airlines to upgrade their outdated infrastructure. This challenge presents an opportunity to invest in cutting-edge, automated disinfection technology that can reduce maintenance downtime by as much as 20%. In this regard, manufacturers are focusing on research and development to create lighter and more efficient components that can address both requirements and regulations.

Aircraft Water and Waste Systems Market Driver:

-

Stringent International Health and Safety Regulations Mandate System Modernization and Compliance

The main force behind this is the increasing pressure from aviation authorities, such as FAA and EASA, to adopt stricter global health regulations. These have strict standards for drinking water safety and waste management, which are intended to prevent contamination and slow the spread of diseases. This creates a definite need for airlines to upgrade their aircraft with systems that meet these standards and for manufacturers to incorporate new technologies into their aircraft designs. Thus, you witness a constant, regulation-induced demand for improved water purification systems, automated flushing, and leak-proof waste tanks, which keeps the market demand steadily on the rise.

In response to updated FAA advisory circulars in April 2025, a major U.S. airline announced a fleet-wide retrofit program to install new-generation water filters and UV sterilization units across its narrow-body aircraft to ensure continuous compliance and enhance passenger safety.

Aircraft Water and Waste Systems Market Restraint:

-

High Installation and Maintenance Costs Limit Retrofit and Upgrade Initiatives

The market is hindered by the high cost of implementing new water and waste infrastructure—or even upgrading the existing infrastructure. This is because of the specialized components, the cost of engineering, and the aircraft downtime required for the job. This high barrier to entry will cause airlines to tread carefully, especially those that are flying on thin margins or have aging fleets. They will be tempted to delay non-essential upgrades even when forced by regulators to do so. This means that the cycle for the sale of aftermarket solutions will be protracted, and customers will be more sensitive to prices, which will slow down the adoption of new technologies.

A low-cost carrier deferred its planned lavatory system modernization for its A320 fleet in late 2023 after analysis showed the project would require an average of 3 days of downtime per aircraft, resulting in an unacceptable loss of revenue during a peak travel season.

Aircraft Water and Waste Systems Market Opportunity:

-

Development of Lightweight and Smart IoT-Enabled Systems Presents Growth Avenues

The cause is the aviation industry's relentless pursuit of fuel efficiency and operational excellence, coupled with the proliferation of IoT technology. This dual focus swings a huge door for innovation and differentiation by the manufacturers. As a result, the market is expanding rapidly for advanced composite systems that reduce weight, and smart components with sensors that monitor water quality, levels, and potential errors in real time. The aircraft industry can move from reactive, on-time maintenance to predictive maintenance, reducing downtime and lowering operating costs in the long run, thus carving a high-value market niche.

In May 2024, a leading system manufacturer unveiled a new smart water tank module with integrated sensors that provide real-time data on water quality and consumption to ground crews via a cloud platform, enabling proactive maintenance and enhancing operational efficiency.

Aircraft Water and Waste Systems Market Segmentation Analysis:

By System Type: Water Supply Systems Lead Market While Lavatory Systems Register Fastest Growth

The Water Supply Systems segment dominates the global Aircraft Water and Waste Systems Market, capturing a 35% revenue share in 2025. This dominance is caused by the critical and non-negotiable requirement for providing safe, potable water for drinking and sanitation on every flight, coupled with stringent and frequently updated health regulations. The effect is that these systems require regular maintenance, part replacements, and occasional upgrades to meet standards, generating consistent and recurring revenue streams for manufacturers and MRO providers, thus securing their leadership position. The Lavatory Systems segment is projected to grow at the fastest CAGR of 6.91%. This rapid growth is caused by increasing passenger expectations for hygiene and comfort, the introduction of higher-capacity aircraft, and the need for more efficient and reliable vacuum toilet technology. The effect is that airlines are investing in modern, touchless, and easier-to-service lavatory systems to improve the passenger experience and reduce turn-around times, driving accelerated growth in this segment.

By Aircraft Type: Commercial Aircraft Leads Market While Business & Private Jets Register Fastest Growth

The Commercial Aircraft segment dominates the global Aircraft Water and Waste Systems Market, accounting for a 55% revenue share in 2025. This leadership is caused by the vast size of the global commercial fleet, which includes thousands of aircraft each requiring multiple complex water and waste systems. The effect is a strong, stable demand profile: the fact that there is little new production of aircraft, combined with a busy aftermarket for maintenance and retrofits, ensures that revenue in the sector remains high. In this environment, Business & Private Jets is well-positioned to take the lead, growing at a CAGR of 6.70%, which is the highest in its category. This is because more and more wealthy individuals and companies are turning to private aviation in order to enjoy luxurious and highly reliable capabilities. As a result, manufacturers are installing state-of-the-art, customized systems in these aircraft.

By Component: Tanks & Reservoirs Lead Market While Sensors & Control Units Register Fastest Growth

The Tanks & Reservoirs segment leads the international Aircraft Water and Waste Systems Market, capturing around 30% of the market’s revenue in 2025. This is due to the fundamental requirement for robust, light, and corrosion-resistant containers to store fresh water and waste in every aircraft. In essence, this segment represents the essential, high-value parts of every system, but they are subject to wear and tear, necessitating periodic replacements. This cycle sustains the segment’s leading market share. On the other hand, the Sensors & Control Units segment is forecasted to record the highest growth rate, at a CAGR of 6.53%. This growth is caused by the accelerating trend towards digitalization and predictive maintenance in aviation, aimed at improving operational efficiency and reliability. The effect is that airlines are increasingly adopting smart systems equipped with sensors to monitor water quality, quantity, and system health in real-time, driving rapid investment in these advanced electronic components.

By End-User: Airlines & Commercial Operators Lead Market While Business Jet Operators Register Fastest Growth

As of 2025, Airlines and Commercial Operators maintain a dominant 63.75% share of the Aircraft Water and Waste Systems market, driven by their busy schedules and stringent water and waste management requirements on board. On the other hand, Business Jet Operators are projected to register the highest CAGR during the period from 2026 to 2035, driven by the increasing demand for luxury air travel, the development of efficient water and waste management systems, and the growing need for passenger comfort.

Aircraft Water and Waste Systems Market Regional Analysis:

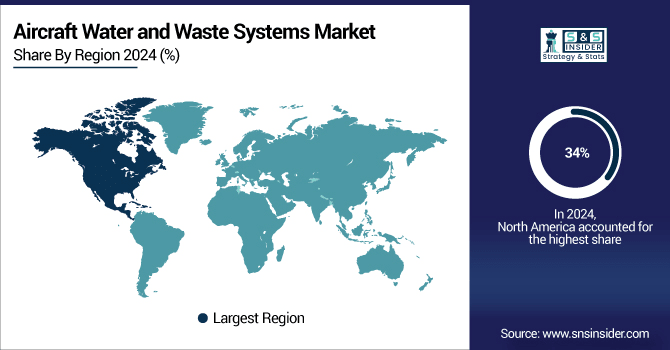

North America Dominates the Aircraft Water and Waste Systems Market in 2025

North America is the dominant region, holding an estimated 34% market share in 2025. North America dominates the Aircraft Water and Waste Systems market due to its large commercial and military aircraft fleet. High regulatory standards, advanced aviation infrastructure, and continuous fleet modernization drive steady demand. The region’s focus on passenger comfort, safety, and sustainable water and waste management solutions makes it a mature and influential market for system manufacturers and service providers.

Get Customized Report as Per Your Business Requirement - Enquiry Now

United States Leads Aircraft Water and Waste Systems Market in North America

The United States has a leading presence in the regional market, due to its group of leading aircraft manufacturers such as Boeing, its system suppliers, and its fleet of some of the largest airlines in the world operating large, old aircraft. The strict FAA regulations and the strong focus on maintenance, repair, and overhaul (MRO) ensure a continuous demand for new installations, upgrades, and replacement parts. This makes the U.S. market the largest and most mature market in the world.

Asia Pacific is the Fastest-Growing Region in Aircraft Water and Waste Systems Market in 2025

Asia Pacific is the fastest-growing region with an estimated CAGR of 6.43%. The Asia Pacific region is leading in terms of growth in the Aircraft Water and Waste Systems market in 2025. This is due to the growing commercial aviation industry, increased demand for air travel, and modernization of the aviation industry. Increased development of airport infrastructure, strict hygiene standards, and the implementation of cutting-edge water and waste technology are driving the market and making this region an area of interest.

China Leads Aircraft Water and Waste Systems Market Growth in Asia Pacific

China dominates the regional market growth driven by its rapidly expanding commercial airline fleet to serve its growing middle class, the establishment of its own aerospace manufacturing capabilities (COMAC), and significant government investment in aviation infrastructure. This rapid fleet modernization and expansion create substantial demand for new aircraft outfitted with modern water and waste systems, making China the primary growth engine in the region.

Europe Aircraft Water and Waste Systems Market Insights

In 2025, Europe holds a significant share of the Aircraft Water and Waste Systems Market. Stringent EASA regulations and presence of Airbus drive a high standard for system innovation and safety. Germany is a key leader, supported by its strong aerospace manufacturing base, home to major system suppliers like Diehl, and a focus on engineering excellence and compliance with rigorous environmental and safety standards.

Middle East & Africa and Latin America Market Insights

The Aircraft Water and Waste Systems Market in Latin America and MEA is developing, driven by airline fleet expansions and modernization efforts. In Latin America, Brazil leads with its established aviation market. The MEA growth is centered around the Gulf carriers, which operate large, modern fleets and require advanced systems for their long-haul operations, though the market is smaller compared to other regions.

Aircraft Water and Waste Systems Market Competitive Landscape:

RTX Corporation

RTX Corporation (formerly Raytheon Technologies), through its Collins Aerospace business, is a U.S.-based global leader in aerospace and defense systems. The company provides a comprehensive range of water and waste management systems, including vacuum toilets, water heaters, and waste tanks, for both commercial and military aircraft. Its role is that of a tier-1 integrated systems supplier, leveraging its vast engineering resources and long-standing relationships with major airframers to develop advanced, reliable, and compliant solutions for next-generation aircraft platforms.

-

Collins Aerospace was selected in early 2024 to supply the integrated water and waste system for a new variant of a popular single-aisle aircraft, highlighting its continued innovation in lightweight and efficient design.

Safran SA

Safran SA is a French multinational aerospace and defense company and a key player in aircraft systems. Its Safran Cabin division specializes in interior solutions, including lavatories and water systems. Safran's role is that of a systems integrator, offering complete lavatory modules and advanced water treatment technologies that focus on passenger comfort, hygiene, and significant weight reduction. The company emphasizes innovation in water conservation and smart monitoring systems to enhance airline operations.

-

Safran introduced a new touchless lavatory control system in April 2024, focusing on enhanced hygiene and passenger peace of mind for post-pandemic travel.

Diehl Stiftung & Co. KG

Diehl Stiftung & Co. KG is a German diversified industrial group with a strong aerospace division, Diehl Aviation. The company is a renowned manufacturer of high-quality aircraft cabin interiors and systems, including water and waste components. Diehl's role is that of a precision manufacturer and reliable supplier, known for its engineering expertise and focus on producing durable, lightweight, and compliant tanks, valves, and control units for a wide range of aircraft programs.

-

Diehl Aviation extended a long-term contract with a major European airline in 2024 to supply spare parts and maintenance support for its water system components, underscoring its role in the aftermarket.

JAMCO Corporation

JAMCO Corporation is a Japan-based leading manufacturer of aircraft interior products and systems. The company specializes in the design, development, and production of lavatories, monuments, and water/waste system components. JAMCO's role is that of a specialized and trusted supplier, particularly strong in the Asia-Pacific region, known for its high manufacturing quality, efficiency, and ability to meet the stringent demands of both commercial airframers and airline operators.

-

JAMCO announced a new production line for composite waste tanks in March 2024, aiming to increase capacity and meet growing demand from aircraft manufacturers in the region.

Aircraft Water and Waste Systems Market Key Players:

Some of the Aircraft Water and Waste Systems Market Companies

-

RTX Corporation

-

Safran SA

-

Diehl Stiftung & Co. KG

-

JAMCO Corporation

-

AeroControlex Group Inc.

-

Collins Aerospace Inc.

-

Parker-Hannifin Corporation

-

Honeywell International Inc.

-

FACC AG

-

Stelia Aerospace SAS

-

General Electric Company

-

Eaton Corporation plc

-

Elbit Systems Ltd.

-

Smiths Group plc

-

T. Controls Ltd.

-

Zodiac Aerospace (now part of Safran)

-

Woodward, Inc.

-

Meggitt PLC

-

Yokohama Rubber Co., Ltd.

-

Geven S.p.A.

| Report Attributes | Details |

| Market Size in 2025 | USD 1.04 Billion |

| Market Size by 2035 | USD 1.85 Billion |

| CAGR | CAGR of 5.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By System Type (Water Supply Systems, Lavatory Systems, Waste Management Systems) • By Aircraft Type (Commercial Aircraft, Business & Private Jets, Military Aircraft) • By Component (Tanks & Reservoirs, Valves & Pipes, Sensors & Control Units, Others) • By End-User (Airlines & Commercial Operators, Business Jet Operators, Military) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | RTX Corporation, Safran SA, Diehl Stiftung & Co. KG, JAMCO Corporation, AeroControlex Group Inc., Collins Aerospace Inc., Parker-Hannifin Corporation, Honeywell International Inc., FACC AG, Stelia Aerospace SAS, General Electric Company, Eaton Corporation plc, Elbit Systems Ltd., Smiths Group plc, T. Controls Ltd., Zodiac Aerospace, Woodward, Inc., Meggitt PLC, Yokohama Rubber Co., Ltd., Geven S.p.A. |

Frequently Asked Questions

North America dominated the Aircraft Water and Waste Systems Market in 2025.

Water Supply Systems segment dominated the Aircraft Water and Waste Systems Market.

Rising air travel, fleet expansion, stringent hygiene regulations, and adoption of advanced water and waste management technologies are the key drivers of the Aircraft Water and Waste Systems Market.

The Aircraft Water and Waste Systems Market size was USD 1.04 Billion in 2025 and is expected to reach USD 1.85 Billion by 2035.

The Aircraft Water and Waste Systems Market is expected to grow at a CAGR of 5.97% from 2026-2035.

Get in Touch