Naval Communication Market Report Scope & Overview:

To get more information on Naval Communication Market - Request Free Sample Report

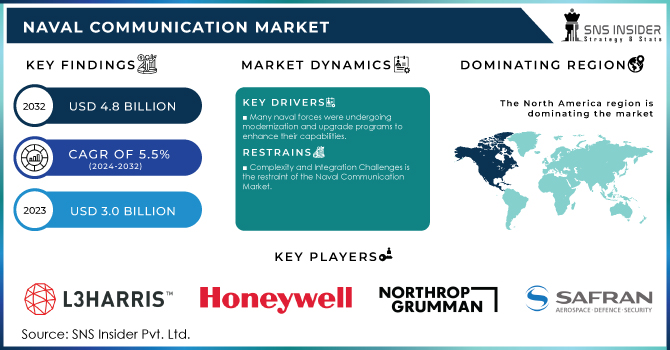

The Naval Communication Market Size was valued at USD 3.0 billion in 2023, and is expected to reach USD 4.8 billion by 2032, and grow at a CAGR of 5.5% over the forecast period 2024-2032.

The constant updating and implementation of a series of resolutions and codes on navigation issues and performance standards for shipborne navigational and radiocommunications equipment, namely the SOLAS, STCW, and COLREG, necessitated the development of new navigation and communication systems to ensure the safety of naval assets at sea. The ongoing research and development towards the development of advanced maritime technologies, such as stealth submarines and unmanned marine systems, is intended to inspire potential investments in the development and implementation of sophisticated navigation systems, to ensure vessel safety, and high-performance communication systems that can ensure the swift, stealthy, and encrypted flow of telemetry data between the naval fleet and the control station.

Geopolitical concerns and national defence expenditures have a considerable impact on the naval communication industry. The geopolitical context, which includes international conflicts, territorial disputes, and regional security concerns, has a direct influence on the demand for naval communication systems. To protect their maritime interests and preserve a competitive advantage, naval forces across the world prioritise the development and upgrade of their communication capabilities. The requirement for sophisticated communication systems to assist naval operations is driven by geopolitical considerations such as greater military presence, territorial claims, and evolving security concerns.

The naval communication market encompasses a range of technologies and solutions designed to facilitate communication and information exchange within naval fleets and between naval units and command centers. This includes communication between ships, submarines, aircraft, and shore-based facilities. The market is driven by the increasing need for secure and reliable communication systems in the face of evolving maritime threats, geopolitical tensions, and the advancement of naval technology.

The market has seen advancements including improved satellite communication systems, communication technologies, secure data networks, high-frequency radio systems, and encrypted communication protocols. Navies have been transitioning toward network-centric warfare strategies, which require seamless integration of communication systems to share real-time data, intelligence, and situational awareness among different units. This drives the demand for advanced networking solutions.

As communication systems become more digitized and interconnected, there is an increasing need to address cybersecurity threats that could potentially compromise sensitive military information and disrupt operations. Satellites play a crucial role in naval communication, enabling long-range and secure communication in remote maritime areas. Advancements in satellite technology have improved coverage and bandwidth capabilities.

MARKET DYNAMICS

DRIVERS:

-

Many naval forces were undergoing modernization and upgrade programs to enhance their capabilities.

-

Network-centric warfare is the driver of the Naval Communication Market.

The shift toward network-centric warfare emphasized the need for seamless communication and data sharing among different naval assets. This approach enhances decision-making and operational effectiveness by enabling real-time information exchange.

RESTRAIN:

-

Defense budgets of many nations are finite, and naval communication systems compete for funding with other critical defense needs.

-

Complexity and Integration Challenges is the restraint of the Naval Communication Market.

Integrating new communication systems with existing naval infrastructure and platforms can be complex and costly. Compatibility issues and technical challenges might arise when trying to ensure seamless communication across various platforms and networks.

OPPORTUNITY:

-

The integration of unmanned systems into naval operations offers opportunities for communication systems.

-

Technological Innovation is an opportunity for the Naval Communication Market.

Ongoing technological advancements create opportunities for the development of more efficient, secure, and interoperable naval communication systems. Innovations such as software-defined radios, advanced signal processing, and cognitive communication techniques could lead to enhanced capabilities.

CHALLENGES:

-

Communicating effectively underwater poses unique challenges due to the limitations of traditional radio waves.

-

Interoperability and Standardization are the challenges of the Naval Communication Market.

Ensuring interoperability between communication systems from different nations and different branches of the military is a complex challenge. Lack of standardized protocols and equipment can hinder coordination during joint operations.

IMPACT OF RUSSIA-UKRAINE WAR

The Ukraine conflict is suffocating trade and logistics in Ukraine and the Black Sea area. The hunt for alternative trade channels for Ukrainian commodities has expanded significantly the need for land and maritime transportation infrastructure and services. Many goods must now be procured from further afield for Ukraine's trading partners. This has boosted worldwide vessel demand and the expense of global transportation. Grains are of special relevance because of the Russian Federation's and Ukraine's dominant positions in agrifood markets, as well as their link to food security and poverty alleviation. Grain prices and transportation costs have been rising since 2021, but the Ukraine crisis has worsened this trend and reversed a recent drop in shipping prices.

The cost of transporting dry bulk items, such as grains, is expected to rise by over 60% by 2022. Concurrent increases in grain prices and freight costs would result in a nearly 4% increase in worldwide consumer food prices. Higher shipping costs account for nearly half of this impact. The Russian Federation is a global powerhouse in the markets for fuel and fertiliser, both of which are critical inputs for farmers globally. Supply disruptions can result in reduced grain yields and higher prices, with major ramifications for global food security. In this conflict, the naval communication market gained less profit up to 1.1-1.5%.

IMPACT OF ONGOING RECESSION

As a result of the worldwide economic slump, the international shipping sector has seen a significant slowdown, with excess shipping capacity, personnel being paid off, fewer earnings, and shipowners looking to cut expenses. This study discusses the consequences of these changes for maritime security. These include an increase in the number of ships anchored in areas that may be vulnerable to pirate assault, as well as the possibility that ships may be less adequately maintained and operated. However, the most significant consequences are felt by seafarers, who face lower salaries and working conditions. The International Maritime Organisation (IMO), industry groups, and shipowners are being urged to solve these challenges before safety and security suffer as a result of rising risks of maritime accidents and pollution. In the ongoing recession, the Naval Communication Market lost up to 3.4-4.5%

KEY MARKET SEGMENTATION

By Application

-

Intelligence Surveillance and Reconnaissance (ISR)

-

Command and Control

-

Routine Operations

-

Others

By Platform

-

Submarines

-

Ships

-

Unmanned Systems

By System Technology

-

Naval Radio Systems

-

Naval Satcom Systems

-

Communication Management Systems

-

Naval Security Systems

REGIONAL ANALYSIS

North America: North America has a vast network of naval bases, command centres, and research facilities that stimulate innovation and fuel demand for naval communication systems. The region's emphasis on maritime security, sea lanes protection, and naval force projection drives market expansion even further. While other areas, such as Europe and Asia-Pacific, have considerable naval capabilities and defence spending, North America is likely to dominate the market owing to its sophisticated naval forces, defence industry experience, and significant resources allocated to naval modernization. The region's substantial presence of major defence contractors reinforces its market dominance.

Asia Pacific: The strengthening of strategic military alliances between the United States and several Asia-Pacific sovereign nations, as well as subsequent reinforcement of military deployment and intervention, has resulted in a complex scenario whereby regional countries, such as China, have been encouraged to modernise their defense capabilities quickly for the sake of protecting their interests. China hopes to have the Type 093B SHANG-class guided-missile nuclear attack submarine in service by the mid-2020s.

Need any customization research on Naval Communication Market - Enquiry Now

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key players

The Major Players are Honeywell International Inc., Northrop Grumman Corporation, Safran SA, FLIR Systems, Inc., Thales Group, General Dynamics Corporation, Bae Systems plc, Lockheed Martin Corporation, L3Harris Technologies, Inc., Raytheon Technologies Corporation and other players.

RECENT DEVELOPMENT

In 2022: BAE Systems was given a contract by the US Defence Advanced Research Projects Agency (DARPA) to create management software that combines military sensors with land, air, and marine weapons. The contract, for a total of USD 24.9 million, is part of the service's Mission-Integrated Network Control (MIC) initiative to develop a secure network overlay to handle multi-domain kill webs. The programme would leverage secure control of any available communications or networking resources in disputed contexts to guarantee that vital data reaches the correct user at the right time.

In 2021: Lockheed Martin purchased Ultra Electronics' naval systems business, which expanded navy communication and electronic warfare capabilities by providing sophisticated solutions for communication, surveillance, and electronic countermeasures in marine environments.

In 2021: Honeywell has introduced two new robust navigation systems: the Honeywell Compact Inertial Navigation System and the Honeywell Radar Velocity System.

| Report Attributes | Details |

| Market Size in 2023 | US$ 3.0 Bn |

| Market Size by 2032 | US$ 4.8 Bn |

| CAGR | CAGR of 5.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Intelligence Surveillance and Reconnaissance (ISR), Command and Control, Routine Operations, Others) • By Platform (Submarines, Ships, Unmanned Systems) • By System Technology (Naval Radio Systems, Naval Satcom Systems, Communication Management Systems, Naval Security Systems) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Honeywell International Inc., Northrop Grumman Corporation, Safran SA, FLIR Systems, Inc., Thales Group, General Dynamics Corporation, Bae Systems plc, Lockheed Martin Corporation, L3Harris Technologies, Inc., Raytheon Technologies Corporation |

| Key Drivers | • Many naval forces were undergoing modernization and upgrade programs to enhance their capabilities. • Network-centric warfare is the driver of the Naval Communication Market. |

| Market Restraints | • Defense budgets of many nations are finite, and naval communication systems compete for funding with other critical defense needs. • Complexity and Integration Challenges is the restraint of the Naval Communication Market. |

Frequently Asked Questions

Ans. The ships category is predicted to develop significantly in the naval communication market, with a large CAR. Ships play an important part in naval operations as platforms, and they require powerful communication systems to support their coordination and command duties. The growing emphasis on marine security, as well as the necessity to confront new threats, has increased demand for advanced communication solutions in the ship segment. Naval modernization programmes aiming at improving operational capabilities add to the need for efficient and dependable communication systems.

Ans. In the naval communication industry, the command-and-control sector is expected to have the biggest market share. In naval operations, command and control systems are critical for successful coordination, situational awareness, and decision-making. As the complexity of naval operations grows, so does the need for modern command and control technologies.

Ans. The Naval Communication Market is anticipated to reach USD 2.98 Billion by 2022.

Ans. USD 4.57 Billion is the projected Naval Communication Market size of the market by 2030.

Ans. The Compound Annual Growth rate for the Naval Communication Market over the forecast period is 5.5%.

Get in Touch