Airflow Management Market Report Scope & Overview:

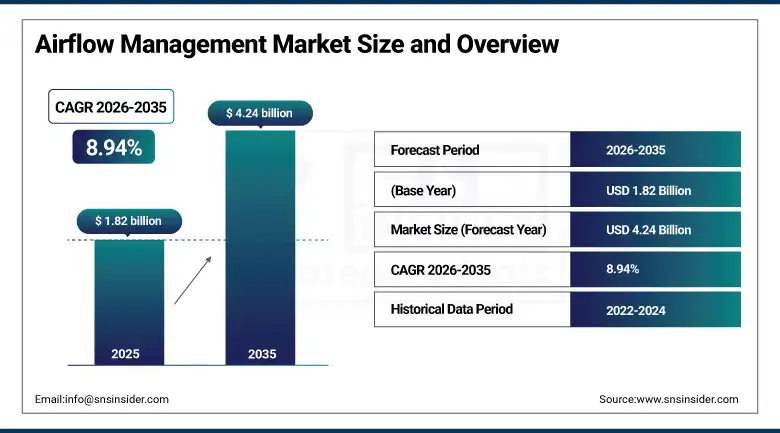

The airflow management market was valued at USD 1.82 billion in 2025 and is expected to reach USD 4.24 billion by 2035, growing at a CAGR of 8.94% from 2026–2035.

Data centers are running hotter than ever. With each generation of AI accelerator chips, the power density per rack has climbed, what was once a 5 kW rack has become a 30 kW rack for AI inference workloads, and some liquid-cooled GPU clusters push beyond 100 kW per rack. Airflow management sits at the center of every attempt to prevent that heat from becoming a catastrophic failure. Containment systems, blanking panels, hot-aisle enclosures, raised floor plenums, and the software platforms that orchestrate them collectively make up a market that is no longer just about moving air, it is about optimizing energy and preserving the hardware reliability of infrastructure that increasingly runs the global economy.

The forces driving the market are not subtle. The International Energy Agency estimated that data centers globally consumed roughly 460 TWh of electricity in 2024, a figure that is rising fast as hyperscale operators expand their AI compute capacity and enterprise customers migrate more workloads to cloud infrastructure. Every percentage point improvement in power usage effectiveness (PUE) that a data center achieves through better airflow management translates to meaningful reductions in energy costs and carbon output. That financial and environmental calculus has elevated airflow management from a facilities afterthought to a boardroom-level investment priority. Regulatory pressure from the EU's Energy Efficiency Directive and comparable U.S. EPA data center energy requirements reinforces the commercial momentum further still.

Market Size and Forecast

-

Market Size 2026E: USD 1.98 Billion

-

Market Size 2035: USD 4.24 Billion

-

CAGR: 8.94% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Airflow Management Market - Request Free Sample Report

Airflow Management Market Trends

-

The rapid increase in rack power density driven by AI and GPU workloads is pushing data center operators to adopt targeted hot-aisle containment and precision in-row cooling solutions that conventional room-based airflow systems cannot adequately handle.

-

AI-powered computational fluid dynamics (CFD) modeling tools are replacing manual airflow audits, giving operators real-time visibility into air circulation patterns, hot spots, and opportunities to reduce cooling energy without compromising equipment reliability.

-

Edge data center proliferation is creating demand for compact, pre-engineered airflow management solutions that can be deployed quickly in space-constrained locations including cell towers, retail back offices, and manufacturing floors.

-

The convergence of liquid cooling and airflow management is reshaping product design, hybrid systems that use air for room-level thermal management while applying direct liquid cooling to high-density AI clusters are now the dominant design philosophy among hyperscale operators.

-

Sustainability reporting requirements are accelerating data center investment in airflow analytics software that can generate auditable PUE improvement documentation and carbon reduction metrics for ESG compliance and regulatory disclosure purposes.

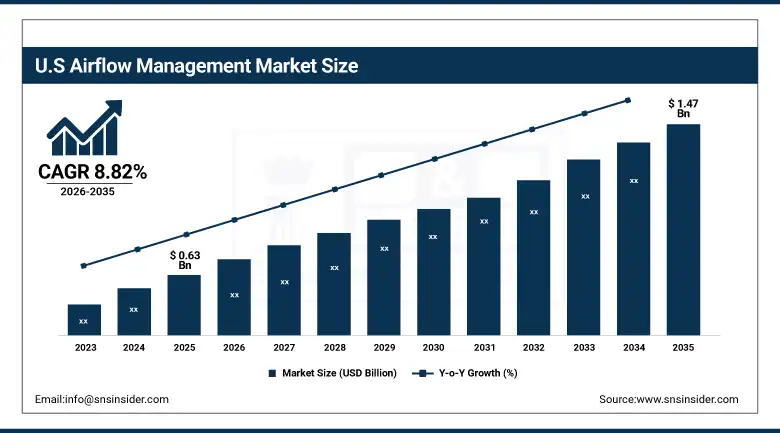

The U.S. Airflow Management Market Size Outlook

The U.S. airflow management market was valued at USD 0.63 billion in 2025 and is expected to reach around USD 1.47 billion by 2035, growing at a CAGR of 8.82% from 2026–2035.

The United States hosts more data center capacity than any other country, and that lead is widening. Hyperscale campuses in Northern Virginia which has earned the title of the world's largest data center market along with major concentrations in Arizona, Texas, Oregon, and Georgia are generating sustained and growing demand for airflow management products and services. The explosion of AI infrastructure spending by Microsoft, Google, Amazon, Meta, and Oracle is translating directly into new data center construction that requires sophisticated containment systems and precision airflow controls from the day it opens. Enterprise data center consolidation, driven by hybrid cloud adoption, is simultaneously creating a retrofit market as existing facilities are upgraded to improve energy performance and handle higher rack densities.

Schneider Electric's EcoStruxure Data Center Solutions platform expanded its AI-driven airflow optimization module in 2025, integrating real-time sensor fusion from thermal imaging arrays with predictive CFD modeling to dynamically adjust cooling infrastructure in response to workload shifts. Deployments at several North American hyperscale facilities demonstrated PUE improvements averaging 0.08 points, a meaningful efficiency gain at the scale of a 100 MW data center campus validating the commercial case for software-led airflow management investment.

Airflow Management Market Segment Analysis

-

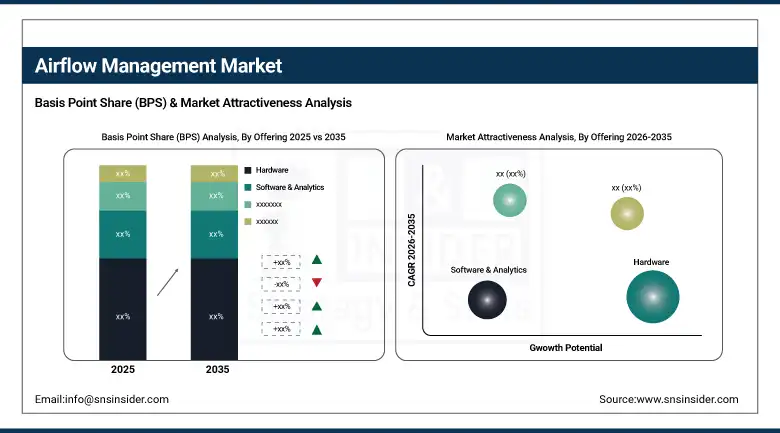

By Offering, the hardware segment dominated the airflow management market with 58.74% share in 2025, while software & analytics is the fastest growing offering.

-

By Data Center Type, the hyperscale segment dominated the airflow management market with 46.38% share in 2025, while edge data centers are the fastest growing segment.

-

By Cooling System, the hot aisle/cold aisle containment segment dominated the airflow management market with 52.63% share in 2025, while liquid cooling integration is the fastest growing cooling system.

-

By End User, the IT & telecommunications segment dominated the airflow management market with 44.52% share in 2025, while the BFSI segment is the fastest growing end user.

By Offering, the hardware segment dominates the airflow management market, while software & analytics is the fastest-growing offering.

Hardware products generated 58.74% of airflow management market revenue in 2025, and that dominance reflects a straightforward physical reality: you cannot manage airflow without the physical infrastructure to shape it. Blanking panels, containment curtains and doors, grommets, raised floor tiles, chimney cabinets, and in-row cooling units are the tangible building blocks of every airflow management deployment. These products are consumed in large quantities across new data center construction and retrofit projects alike, and with global data center construction spending exceeding USD 50 billion in 2025 the addressable market for hardware components is enormous. The standardization of rack unit specifications has also made blanking panels and containment accessories a commodity-driven high-volume category that generates consistent revenue for leading hardware suppliers.

Software and analytics are where the growth curve is steepest. As data centers have become more complex with AI workloads creating unpredictable thermal spikes alongside stable enterprise computing loads static airflow configurations that were set once and rarely revisited are being replaced by dynamic systems that continuously optimize air distribution based on real-time sensor data. CFD modeling tools, digital twin platforms, and AI-driven anomaly detection systems that predict hot-spot formation before it triggers a thermal shutdown are delivering quantifiable ROI through energy savings and avoided downtime. Operators who have deployed these systems report that software-guided airflow optimization often achieves better PUE results than physical hardware upgrades alone, which is accelerating software investment even at facilities where hardware infrastructure is already mature.

By Data Center Type, the hyperscale segment dominates the airflow management market, while edge data centers are the fastest-growing segment.

Hyperscale data centers accounted for 46.38% of market revenue in 2025. The logic is straightforward: a 500 MW hyperscale campus spends more on airflow management products and services than a hundred enterprise server rooms combined. Hyperscale operators have also been at the forefront of airflow management innovation, developing proprietary hot-aisle containment systems, custom blanking solutions for non-standard rack configurations, and advanced CFD-guided cooling designs that push PUE closer to the theoretical minimum. Their scale gives them the procurement leverage to influence product design and specification, which means suppliers who establish hyperscale reference deployments tend to see their solutions adopted broadly across the rest of the market as design standards.

Edge data centers are growing the fastest as computing infrastructure moves closer to where data is generated. A manufacturing plant processing real-time quality control images, a retail distribution center running AI-driven inventory optimization, or a 5G base station handling mobile edge compute workloads each of these is a micro or edge data center that requires effective thermal management in a space that was often never designed to house IT equipment. Pre-packaged, self-contained airflow management solutions that can be deployed quickly without specialized facilities engineering are the product category most directly aligned with edge growth, and suppliers developing modular, edge-ready airflow management systems are well positioned to capture this expanding opportunity.

By Cooling System, hot aisle/cold aisle containment dominates the airflow management market, while liquid cooling integration is the fastest-growing segment.

Hot aisle and cold aisle containment held the largest share of 52.63% in 2025, firmly established as the operational baseline for any professionally managed data center. The concept is straightforward keep cold supply air from mixing with hot exhaust air but the execution ranges from basic plastic curtains separating rack rows to fully enclosed cages with precision airflow controls and integrated monitoring. The return on investment from containment is well documented: most data centers achieve PUE improvements of 0.1 to 0.3 points after implementing proper aisle containment, which at scale translates to millions of dollars in annual energy savings. That clarity of ROI has made aisle containment the default first step in any data center energy efficiency program, sustaining high and consistent product demand.

Liquid cooling integration is growing faster than any other cooling system category, driven almost entirely by the AI compute buildout. When a rack is drawing 40 kW or more which is routine for GPU clusters running large language model training air cooling simply cannot remove the heat efficiently enough. Direct liquid cooling (DLC) solutions that attach directly to processors, rear-door heat exchangers that capture heat before it escapes the rack, and immersion cooling tanks for the densest deployments are moving from niche to mainstream with remarkable speed. The challenge for data center operators is integrating liquid cooling alongside existing air-based airflow management infrastructure, and the hybrid systems that address this integration challenge are among the most rapidly evolving product categories in the market.

By End User, the IT & telecommunications segment dominates the airflow management market, while BFSI is the fastest-growing end user.

IT and telecommunications accounted for 44.52% of airflow management market revenue in 2025. Hyperscale cloud providers, telecommunications carriers operating central office and edge compute infrastructure, and managed hosting providers collectively represent the broadest and most commercially significant customer base for airflow management products. These organizations operate large, densely packed facilities around the clock and are systematically motivated to reduce cooling energy costs. Telecom carriers are additionally investing in airflow management for their distributed 5G and fiber network infrastructure, where maintaining reliable thermal conditions in unmanned equipment cabinets is essential for network uptime.

The BFSI sector is growing the fastest among end users, reflecting the financial services industry's accelerating investment in private cloud infrastructure, AI-powered trading and risk analytics platforms, and real-time payments processing systems that impose extreme reliability requirements on the data center thermal environment. Banks and insurance companies are also under growing regulatory scrutiny for operational resilience, and thermal management failures that cause system downtime carry regulatory consequence beyond financial cost. This regulatory pressure has elevated data center thermal management including airflow to a risk management imperative rather than a facilities management consideration.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

27.84% |

|

Asia Pacific |

China |

42.36% |

|

Middle East & Africa |

UAE |

24.53% |

|

Latin America |

Brazil |

44.82% |

North America Airflow Management Market Insights

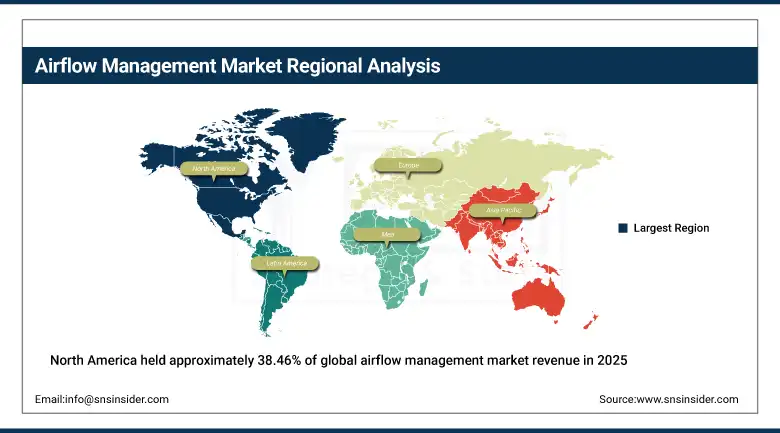

North America held approximately 38.46% of global airflow management market revenue in 2025, anchored by the United States' position as the world's largest data center market by installed capacity and capex investment. The concentration of hyperscale facilities in Northern Virginia, Phoenix, Dallas, and Seattle generates extraordinary purchasing volumes for containment products, in-row cooling systems, and CFD-driven thermal management software. Canadian data center expansion in Toronto and Montreal contributes supplementary regional demand, supported by favorable electricity costs and a growing cloud provider presence. Federal mandates for energy efficiency at U.S. government data center facilities and state-level data center sustainability regulations in California and New York add regulatory urgency to the commercial drivers already present.

The U.S. CHIPS and Science Act's data infrastructure provisions and the Inflation Reduction Act's clean energy investment incentives are channeling multi-billion-dollar capital flows into domestic semiconductor fabrication and supporting data center infrastructure, including advanced thermal management systems. Several major cloud providers committed to specific PUE targets in their 2025 sustainability reports, creating direct demand for airflow management upgrades across their U.S. portfolio as they work toward published efficiency commitments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Airflow Management Market Insights

Europe accounted for approximately 24.73% of global airflow management market revenue in 2025. The European Union's Energy Efficiency Directive and associated data center sustainability reporting requirements have made airflow management investment a compliance necessity rather than a purely commercial decision for many European data center operators. Germany, the Netherlands, the United Kingdom, Ireland, and France are the dominant national markets each hosting major hyperscale campuses operated by AWS, Microsoft, Google, and regional providers. The EU's publication of industry-specific energy benchmarks for data centers has created a market for airflow management audit services and software that can document compliance progress, adding a services revenue dimension that supplements the established hardware product market.

The Netherlands' Amsterdam data center market one of Europe's largest implemented stricter energy efficiency requirements in 2024, capping new data center construction approvals at facilities achieving below a PUE threshold. This regulatory constraint is driving existing operators to invest in airflow management upgrades as a path to improving PUE without adding new physical footprint, creating a retrofit demand wave that benefits established European airflow management hardware and services providers.

Asia Pacific Airflow Management Market Insights

Asia Pacific is the fastest-growing regional airflow management market, forecast to expand at a CAGR of approximately 10.24% during 2026–2035. China is the dominant national market, with domestic hyperscale cloud providers Alibaba Cloud, Tencent Cloud, Huawei Cloud, and ByteDance investing heavily in new data center campuses across Tier-1 and Tier-2 cities. The Chinese government's dual carbon targets have imposed energy efficiency requirements on new data center construction that make sophisticated airflow management an explicit design requirement rather than an option. India is growing at the fastest pace within the region, driven by rapid digital adoption, 5G rollout, and significant foreign hyperscale investment in colocation capacity across Mumbai, Pune, Hyderabad, and Chennai.

Singapore's revised data center sustainability framework which resumed new data center approvals in 2022 after a moratorium requires applicants to demonstrate PUE performance targets and water usage efficiency commitments that explicitly mandate advanced airflow management systems. This regulatory model is influencing data center policy design across Southeast Asia, with Malaysia, Thailand, and Indonesia developing analogous frameworks as they seek to attract hyperscale investment while managing energy and water resource implications.

Middle East & Africa and Latin America Airflow Management Market Insights

The Middle East and Latin American markets are smaller in scale but boast some of the best growth rates due to heavy investment in data centers and digital infrastructure development initiatives. The UAE, which is one of the Middle East’s data center hubs, operates hyperscale facilities in both Dubai and Abu Dhabi by companies like Microsoft, AWS, and local data centers that require premium airflow management systems for operation under high ambient temperatures. There are also initiatives like Saudi Arabia’s NEOM smart cities project and Vision 2030 digital infrastructure development projects, which have been funding new data center capacities. In Latin America, the top market is Brazil, where São Paulo has the most data center infrastructure density, and Chile and Colombia make up a fast-emerging secondary market.

The UAE's extreme summer ambient temperatures regularly exceeding 40°C make airflow management and thermal control engineering significantly more demanding than in temperate climates. Data center operators in the region invest proportionately more in containment, precision airflow controls, and cooling redundancy than their counterparts in Northern Europe or the U.S. Pacific Northwest, giving airflow management solution providers a higher-value opportunity per megawatt of installed capacity in the Gulf region.

Market Dynamics

Growth Drivers: Exploding AI compute power density and data center sustainability mandates are converging to make effective airflow management a critical operational and regulatory priority globally.

The step-change in rack power density driven by AI accelerator hardware has rewritten the economics of data center thermal management. A server room designed in 2018 for 8 kW racks cannot efficiently cool a 2025 AI inference cluster drawing 40 kW from the same footprint without significant airflow management investment. This hardware evolution is creating a large and persistent retrofit demand wave that affects not only new data center construction but also the vast installed base of existing facilities. The financial scale of this market driver is amplified by the pace of AI infrastructure investment hyperscale capex in North America alone exceeded USD 200 billion in 2025 and every dollar of that spending generates downstream demand for the thermal management infrastructure that keeps the hardware operational.

Restraints: High upfront implementation costs and the technical complexity of retrofitting airflow management into legacy data center facilities constrain adoption, particularly among smaller enterprise operators.

A comprehensive aisle containment retrofit for a mid-sized enterprise data center can require significant capital investment in containment hardware, raised floor modifications, and software monitoring systems, with payback periods that may stretch beyond budget planning horizons for cost-constrained IT organizations. Legacy data center designs particularly older raised-floor facilities with irregular rack layouts and non-standard aisle widths present genuine engineering challenges for containment system installation that require customized solutions and specialized installation expertise. Smaller operators often lack the in-house facilities engineering capability to properly design and commission airflow management systems, creating a dependency on external consultants and system integrators that adds both cost and implementation time.

Opportunities: The convergence of digital twin technology and AI-driven thermal modeling is creating a high-value software layer atop the physical airflow management product market.

Data center digital twins’ real-time virtual models of a facility's physical thermal environment are transitioning from research curiosity to operational tool as sensor costs have declined and computing power to run continuous CFD simulations has become cost-effective. Airflow management software vendors that can build and maintain accurate digital twins of customer facilities, delivering continuous optimization recommendations and predictive failure alerts, are creating a recurring software revenue model that significantly improves on the transactional economics of hardware-only product sales. The operators of hyperscale facilities are already deploying these systems at scale, and as the technology matures and implementation costs decrease the enterprise and colocation segments represent a large and largely untapped software monetization opportunity.

Recent Developments

-

2025: Vertiv launched an expanded AI-optimized airflow management solution set incorporating machine learning-driven containment control and predictive hot-spot analytics, deployed at multiple hyperscale data center campuses in North America and Europe, demonstrating measurable PUE improvements that validated the commercial ROI case for software-led thermal management investment.

-

2025: Schneider Electric extended its EcoStruxure data center management platform with enhanced airflow visualization and digital twin capabilities, integrating real-time thermal imaging sensor feeds with AI-driven optimization algorithms to provide dynamic cooling recommendations that adapt automatically to changing workload distributions.

-

2024: Upsite Technologies introduced next-generation hot-aisle containment systems engineered specifically for high-density AI compute rack deployments, featuring modular assembly designs that accommodate rapid hardware refresh cycles and cable management configurations suited to the high-bandwidth interconnect requirements of GPU clusters.

-

2024: Panduit expanded its data center airflow management product portfolio with a comprehensive edge-ready containment system designed for pre-manufactured micro data center deployments, addressing the fast-growing edge computing infrastructure segment that requires compact, rapidly deployable thermal management solutions.

-

2023: Kingspan Group completed the acquisition of a specialist data center airflow management hardware supplier, expanding its raised floor and containment product range and establishing a direct presence in the North American hyperscale data center market to complement its established European customer base.

Airflow Management Market Key Players are:

-

Schneider Electric

-

Vertiv Holdings

-

Eaton Corporation

-

Upsite Technologies

-

Panduit Corporation

-

Subzero Engineering

-

Kingspan Group

-

Chatsworth Products (Legrand)

-

Crenlo LLC

-

Geist (Vertiv)

-

AFCO Systems (Legrand)

-

nVent SCHROFF

-

Rittal GmbH

-

CommScope

-

Tripp Lite (Eaton)

-

APC by Schneider Electric

-

Huawei Digital Power

-

Delta Electronics

-

Elliptical Mobile Solutions (EMS)

-

Airedale International Air Conditioning

Airflow Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.82 Billion |

| Market Size by 2035 | USD 4.24 Billion |

| CAGR | CAGR of 8.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Offering (Hardware, Software & Analytics, Services) • By Data Center Type (Hyperscale, Colocation, Enterprise, Edge Data Centers) • By Cooling System (Hot Aisle/Cold Aisle Containment, In-Row Cooling, Raised Floor Systems, Liquid Cooling Integration, Others) • By End User (IT & Telecommunications, BFSI, Healthcare, Government & Defense, Retail & E-Commerce, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Schneider Electric, Vertiv Holdings, Eaton Corporation, Upsite Technologies, Panduit Corporation, Subzero Engineering, Kingspan Group, Chatsworth Products (Legrand), Crenlo LLC, Geist (Vertiv), AFCO Systems (Legrand), nVent SCHROFF, Rittal GmbH, CommScope, Tripp Lite (Eaton), APC by Schneider Electric, Huawei Digital Power, Delta Electronics, Elliptical Mobile Solutions (EMS), Airedale International Air Conditioning |

Frequently Asked Questions

North America dominated the Airflow Management market in 2025 with approximately 38.46% of total global market revenue.

The primary growth driver is the rapid increase in data center rack power density driven by AI compute workloads, which is making effective airflow management a critical operational requirement, combined with regulatory energy efficiency mandates across the United States, European Union, and Asia Pacific that are compelling data center operators to invest in advanced containment and thermal optimization systems.

The Airflow Management market is expected to grow at a CAGR of 8.94% from 2026 to 2035.

Get in Touch