Farm Management Software Market Report Scope & Overview:

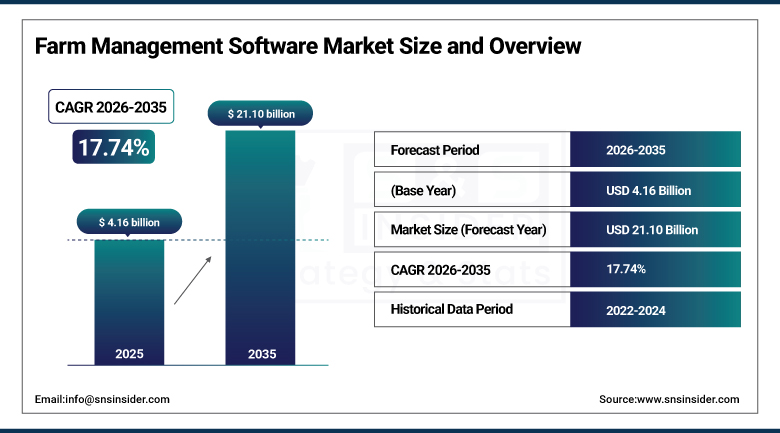

The Farm Management Software Market was valued at USD 4.16 Billion in 2025 and is expected to reach USD 21.10 Billion by 2035, growing at a CAGR of 17.74% from 2026 to 2035.

Insights into the statistical aspects of the farm management software market demonstrate changes in the adoption of digitization in agriculture. The use of precision farming solutions has grown due to the need to make decisions based on information. Trends in terms of usage suggest the growing involvement of mid-size farms and young and tech-savvy farmers, which demonstrates the generational shift occurring in the agricultural sector. Moreover, integration with other solutions has become much easier due to the connection of various platforms with IoT devices, drones, and ERP systems. The use of all the mentioned technologies increases efficiency, allowing for more accurate forecasting and reducing costs.

In May 2024, Cooperative Ventures declared an investment in Traction Ag, Inc., a provider of agricultural accounting technology offering solutions to farmers across the U.S. A joint venture between two leading agricultural cooperatives, GROWMARK and CHS, Cooperative Ventures focuses on the rising mutually beneficial business relationships between cooperative partners and startups. Traction Ag's USD 10 million Series A funding round was led by Cooperative Ventures, with participation from Plymouth Development and existing investors, reflecting the strong investor confidence in farm financial management software platforms serving the U.S. agricultural cooperative ecosystem.

Market Size and Forecast

-

Market Size in 2026E: USD 4.90 Billion

-

Market Size by 2035: USD 21.10 Billion

-

CAGR: 17.74% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Farm Management Software Market - Request Free Sample Report

Farm Management Software Market Trends

-

Rising adoption of precision agriculture is driving demand for farm management software, with over 55% of large farms using digital tools to optimize inputs and improve yields.

-

Increasing integration of IoT, sensors, and drones is enabling real time farm monitoring, with connected agriculture devices growing at a CAGR of over 12% globally.

-

Growing focus on data driven decision making is improving farm productivity, with software adoption helping increase crop yields by 15 to 20 percent on average across adopting farms.

-

Expansion of cloud-based platforms and mobile apps is accelerating adoption, with over 60% of new deployments being cloud enabled for remote farm management.

-

Government support and subsidies for smart farming technologies are boosting adoption, particularly in emerging markets, contributing to over 25% growth in digital agriculture investments.

U.S. Farm Management Software Market Outlook

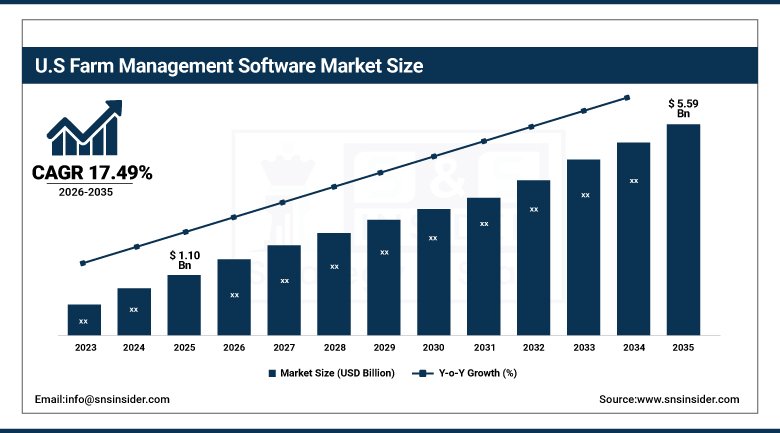

The U.S. Farm Management Software Market was valued at approximately USD 1.10 Billion in 2025 and is expected to reach approximately USD 5.59 Billion by 2035, growing at a CAGR of approximately 17.49%.

The growth of the U.S. economy is associated with the widespread adoption of precision agriculture methods combined with advanced technologies such as IoT and AI that increase efficiency and productivity. This is facilitated by various government programs aimed at sustainable farming. The development of farm consolidation and agribusiness in North America gives rise to the necessity of developing new and more complex software for farm management. The farms have become larger and more complex, therefore, more efficient and advanced software is needed to manage everything starting from field production up to financial modeling.

In March 2025, Trimble Inc. expanded its Trimble Ag Software platform with AI powered yield prediction and automated variable rate application modules, aiming to improve farmer self service capabilities and agronomic decision support. The platform enhancement demonstrates Trimble's continued investment in next generation farm management capability whose predictive analytics and automation reduce the manual data interpretation burden that conventional precision agriculture platforms have historically required from farm operators.

Farm Management Software Market Segment Analysis

-

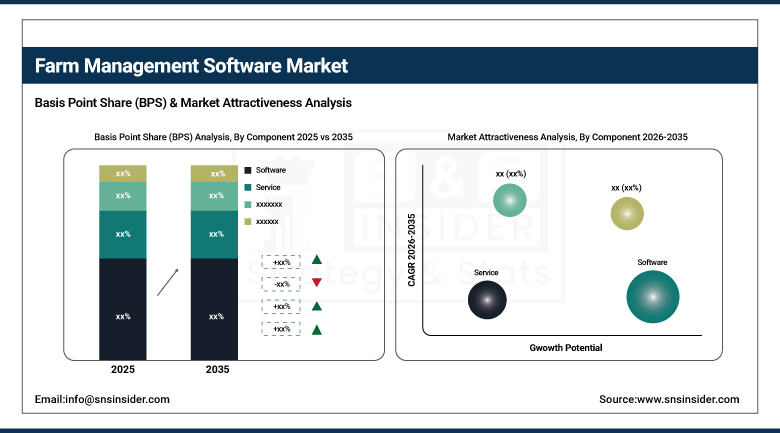

By Component, the Software segment dominated the market with approximately 66.00% share in 2025, while the Services segment is the fastest growing.

-

By Agriculture Type, the Precision Farming segment dominated the market with approximately 42.00% share in 2025, while the Smart Greenhouse segment is the fastest growing.

-

By Deployment, the Cloud-based segment dominated the market with approximately 61.00% share in 2025, while the Web-based segment continues to maintain adoption across cost-sensitive agricultural operations.

By Component, software dominates, service grows alongside

The software segment dominated the farm management software market with a revenue share of over 65% in 2025. The incorporation of IoT and cloud-based solutions drives this leadership position, with these tools collecting and processing data from sensors measuring soil moisture, temperature, nutrient levels, and weather patterns. Farmers benefit from remote access, real time monitoring, and automated reporting that these integrated platforms provide. Each farm operation that adopts a comprehensive software platform for field production, financial modeling, inventory management, and labor oversight creates structured software procurement whose commercial aggregate across the global agricultural sector sustains the component's commanding market position.

Subscription based models such as software as a service are rising rapidly within the service segment, where ongoing support, updates, troubleshooting, and cybersecurity services are boosting demand for managed solutions. Each farm operation who’s limited in house technical capability creates dependence on vendor provided implementation, training, and ongoing support services contributes to growing service segment procurement. The increasing complexity of integrating IoT devices, drones, and ERP systems within unified farm management platforms creates structured demand for professional implementation services that complement the core software investment.

By Agriculture Type, precision farming dominates, smart greenhouse grows fastest

Precision farming dominated the farm management software market and accounted for a significant revenue share in 2025. The precision farming market is expanding as a result of the increasing trend of data driven farming. Big data is not something new, as there is an increasing amount of big data available, farmers can base their decision making on thorough data analysis instead of relying on conventional farming approaches. This includes leveraging weather information, soil conditions, and crop health monitor reports obtained via sensors and remote sensing technologies. Each large commercial farm whose operational scale justifies investment in sensor networks, variable rate application equipment, and yield mapping software creates precision farming software procurement whose commercial aggregate sustains this agriculture type's dominant market position.

Smart greenhouse is expected to grow at the fastest CAGR during the forecast period, leading to increased use of smart greenhouses as demand for fresh, locally grown produce rises. As more consumers seek out fresh, high-quality produce grown without hazardous chemicals, there is a rising demand for sustainable and organic farming. Each controlled environment agriculture facility whose climate control, irrigation automation, and crop monitoring requirements create demand for integrated greenhouse management software contributes to this segment's accelerating commercial growth trajectory as urban and peri urban food production expands globally.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Farm Management Software Market Insights

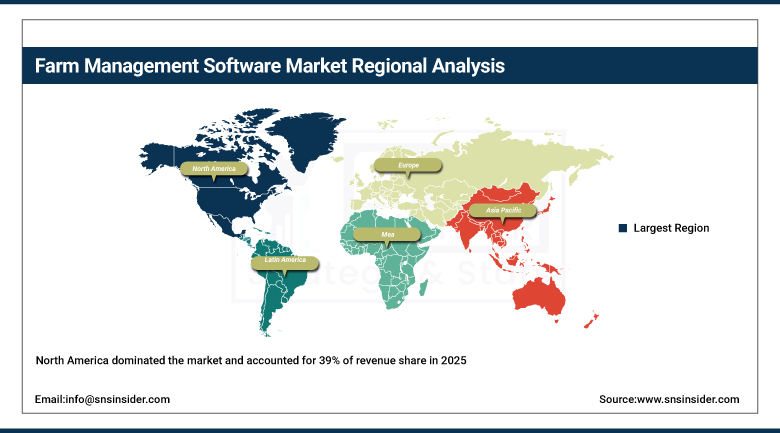

North America dominated the market and accounted for 39% of revenue share in 2025. Farm consolidation and the growth of agribusiness in North America are creating demand for more sophisticated and holistic farm management software. These farms are becoming bigger and more complicated, requiring better and sharper software to handle everything from field production through financial modeling. Agribusinesses can leverage farm management software platforms, which allow them to control operations, inventory management, labor oversight, and financial management all from a single system. The United States accounts for approximately 87.4% of North American revenues through Trimble, AGCO, Deere & Company, and Raven Industries' commercial operations.

Canada contributes complementary North American revenue through its large-scale grain and oilseed farming sector's adoption of precision agriculture platforms and growing agricultural cooperative investment in digital farm management infrastructure across the country's major agricultural provinces.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Farm Management Software Market Insights

Europe is a technically sophisticated farm management software market where the European Common Agricultural Policy's digital agriculture incentive programs and sustainability reporting requirements create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its strong agricultural machinery manufacturing base and growing precision farming technology adoption among the country's commercial farming operations.

The United Kingdom and France are significant secondary markets where government agricultural digitalization programs and large-scale commercial farming operations create consistent procurement. Agrivi's European commercial presence and other regional software providers sustain market supply across the continent's farm management software landscape.

Asia Pacific Farm Management Software Market Insights

Asia Pacific is expected to register the fastest CAGR during the forecast period in the farm management software market. The market growth in the region is driven by the increasing concern for environmental sustainability and the effect of climate change on agriculture. As extreme weather events, including droughts, floods, and storms, continue to increase in frequency and severity, farmers have no choice but to explore methods to make farming more resilient and data driven. China accounts for approximately 44.8% of Asia Pacific revenues through its large-scale agricultural modernization investment and growing domestic agricultural technology manufacturing base.

India represents the most commercially dynamic emerging market within Asia Pacific where the country's burgeoning agricultural sector and the rapid increase in population create rising demand for agricultural products, driving farmers to embrace farm management software solutions in precision agriculture, livestock monitoring, and aquaculture farms across the country's extensive agricultural base.

MEA & Latin America Farm Management Software Market Insights

South Africa leads MEA revenues through its advanced agricultural sector's adoption of precision farming technology and growing investment in digital agriculture initiatives supporting commercial crop and livestock operations across the country. The UAE's growing investment in controlled environment agriculture and food security initiatives adds complementary regional demand. Brazil leads Latin American revenues through its large-scale commercial agriculture sector's adoption of farm management platforms supporting soybean, corn, and sugarcane production. Mexico's growing agricultural technology adoption and Argentina's commercial farming sector collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Rising adoption of data-driven tools and precision agriculture technology

The introduction of precision agriculture is transforming the way farming is being done with the help of information, which enables farmers to enhance their yield and manage their resources effectively. The information required at the agriculture business end is obtained from an array of tools such as sensors, drones, and satellites through farm management software, which is an important part of the farmer's tool kit in the current times when there is pressure on the farmers to produce maximum while creating minimum impact on the environment.

Incentives offered by governments and increasing awareness are fueling the adoption of this technology in the U.S. and other developed economies, where farm management software has become a vital part of the farmer's tool kit. Programs launched by governments to encourage smart farming along with increased awareness regarding efficiency in resource utilization have ensured good adoption in both developed and emerging economies, leading to sustained structural growth of the demand.

Restraints: High setup costs and low digital literacy among small farmers

The high initial cost of farm management software and the associated infrastructure for its functioning, including hardware integration and connectivity, forms a major hurdle, especially for small scale farmers. Moreover, some farmer segments having low levels of digital literacy also make effective use of the software difficult. This may result in a longer time period to realize the return on investment and deter adoption in areas with low access to finances and/or broadband facilities.

Vendor companies have to provide a solution that is both affordable and easy-to-use to overcome these hurdles and widen their customer base. Every single small scale farmer who does not adopt the software because of his/her financial and technological limitations makes up for a new market segment for the vendor to target.

Opportunities: AI, IoT, and big data analytics enabling smarter operations

Emerging technologies like artificial intelligence, Internet of Things, and big data analytics provide great scope for growth in the farm management software market. Such technologies enable farmers to make decisions based on predictions, automation of processes, and even weather forecasts, making their operations much more efficient. In light of increasing digitalization of farms, farm management software will definitely see increasing demand for solutions providing real-time, actionable insights and seamlessly integrated with other tools.

Such conditions present great scope for innovation by software developers and agritech startups. The emergence of each new generation of yield prediction systems and technology for automated variable rate application presents clear-cut commercial opportunities for vendors who can deliver proven efficiency improvements.

Recent Developments:

-

2025: Trimble Inc. expanded its Trimble Ag Software platform in March 2025 with AI powered yield prediction and automated variable rate application modules, improving farmer self service capabilities and agronomic decision support.

-

2024: Cooperative Ventures invested in Traction Ag, Inc. in May 2024, an agricultural accounting technology provider, through a USD 10 million Series A funding round supporting farm financial management software development.

-

2024: Deere & Company expanded its Operations Center platform in 2024 with enhanced AI, machine learning, and autonomous equipment integration capabilities, supporting precision agriculture decision making across its connected equipment fleet.

-

2023: John Deere announced eight companies participating in its Startup Collaborator 2023 program in January 2023, supporting the design of precision technology integration with its agricultural equipment ecosystem.

-

2024: Agrivi expanded its modular farm management software packages in 2024 with subscription based pricing tiers, enabling small and medium sized farms in Europe and Asia Pacific to adopt digital farming tools without high upfront costs.

Farm Management Software Market Key Players

-

Trimble Inc.

-

Deere & Company

-

AGCO Corporation

-

Raven Industries Inc.

-

Topcon Positioning Systems Inc.

-

AgJunction Inc.

-

Iteris Inc.

-

Granular Inc. (Corteva Agriscience)

-

AG Leader Technology Inc.

-

Dickey-John Corporation

-

SST Development Group Inc.

-

Farmers Edge Inc.

-

Climate FieldView (Bayer)

-

Proagrica (SST Software Solutions)

-

Agrivi Ltd.

-

Conservis Corporation

-

FarmLogs Inc.

-

Cropio (1cFarm)

-

Traction Ag Inc.

-

Hexagon Agriculture

Farm Management Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.16 Billion |

| Market Size by 2035 | USD 21.10 Billion |

| CAGR | CAGR of 17.74% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Software, Service) • by Agriculture Type (Precision Farming, Livestock Monitoring, Smart Greenhouse, Others) • by Deployment (Web-based, Cloud-based) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Trimble Inc., Deere & Company, AGCO Corporation, Raven Industries Inc., Topcon Positioning Systems Inc., AgJunction Inc., Iteris Inc., Granular Inc. (Corteva Agriscience), AG Leader Technology Inc., Dickey-John Corporation, SST Development Group Inc., Farmers Edge Inc., Climate FieldView (Bayer), Proagrica (SST Software Solutions), Agrivi Ltd., Conservis Corporation, FarmLogs Inc., Cropio (1cFarm), Traction Ag Inc., Hexagon Agriculture |

Frequently Asked Questions

North America dominated the Farm Management Software Market with 39% of revenue share in 2025, while Asia Pacific is expected to register the fastest CAGR through 2035.

Software dominated the Farm Management Software Market with a revenue share of over 65% in 2025, while the Service segment continues growing as subscription-based models accelerate.

The adoption of precision agriculture changing how farmers approach their work, using data from sensors, drones, and satellite imagery to make better decisions, increase yields, and use inputs more efficiently, alongside government incentives and increasing awareness propelling adoption across developed and emerging markets.

The Farm Management Software Market was valued at USD 4.16 Billion in 2025.

Get in Touch