Artificial Intelligence In Military Market Report Scope & Overview:

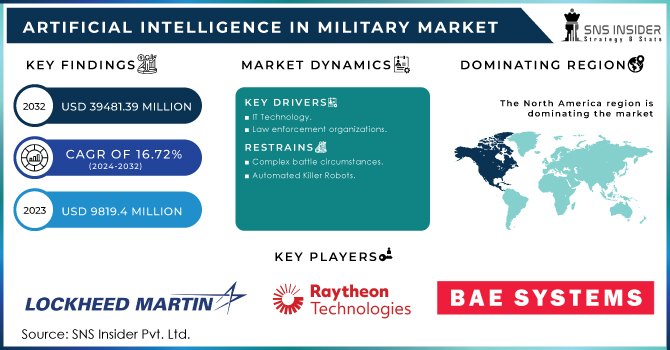

The Artificial Intelligence In Military Market Size was valued at US$ 9819.4 million in 2023, is expected to reach USD 39481.39 million by 2032, and grow at a CAGR of 16.72% over the forecast period 2024-2032.

In terms of innovation, the artificial intelligence segment is expected to lead the market from 2022 to 2028. The developing demand for AI-coordinated frameworks and the rising usage of cloud-based apps and superior computers can be attributed to the growth of the market for A.I. in military areas. In any event, protectionist tactics and a lack of standard conventions, which result in limited admittance to military stages, are limiting the development of this artificial intelligence (A.I.) in the military market.

Military intelligence refers to the integration of the latest and most advanced technologies with military equipment to increase its efficiency and effectiveness. In the developed world, the military industry is a sector, which receives the highest investment. This investment is utilized through the R&D of new technological advances and the development of advanced equipment that will be used during the war. AI-armed military systems are capable of handling large amounts of data efficiently. In addition, these programs have improved self-control and self-control due to their improved computer skills and decision-making ability. Independent weapon systems use computer detection technology to identify and track objects. Artificial intelligence can assist in extracting useful information from machines such as radars and automated diagnostic systems. Therefore, the development of military equipment, weapons, and equipment with the latest technology drives artificial intelligence to grow the military market.

Market Size and Forecast:

-

Market Size in 2023: USD 9,819.4 Million

-

Market Size by 2032: USD 39,481.39 Million

-

CAGR: 16.72% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

To get more information on Artificial Intelligence In Military Market - Request Free Sample Report

Artificial Intelligence in Military Market Trends:

-

Increasing adoption of AI-powered autonomous weapons systems and unmanned platforms is driving market expansion.

-

Rising defense budgets across major economies are accelerating investments in AI-based surveillance, cybersecurity, and intelligence systems.

-

Growing demand for real-time battlefield data analysis and predictive maintenance solutions is boosting AI integration in military operations.

-

Expansion of advanced technologies such as machine learning, computer vision, and natural language processing is enhancing decision-making capabilities.

-

Strengthening focus on border security, threat detection, and modern warfare strategies is increasing AI deployment.

-

Strategic collaborations between defense agencies and AI technology providers are fostering innovation and large-scale implementation.

Market Dynamics

Key Drivers

-

IT Technology

-

Law enforcement organizations

-

Defense agencies

Restraints

-

Complex battle circumstances

-

Automated Killer Robots

-

Lack of trained people

Opportunities

-

Superposition

-

Entanglement connection

Challenges

-

Rising Conflicts between Countries

-

High maintenance

The Impact of Covid-19

Although the COVID-19 epidemic is affecting the global economy, creating more difficulties, Artificial Intelligence in the military market has continued to grow. This can be seen on both sides of the demand and supply chain, as automakers such as Lockheed Martin, IBM, Northrop Grumman, and others continue to put great effort into creating A.I. skills, and governments continue to invest primarily in acquiring these structures. This can be attributed to governments that understand the capabilities of the A.I. systems that provide up to a defense arsenal such as the global A.I. the arm race is fierce.

However, despite the development of A.I. proof-of-extension technology, standard A.I. the system detected a stroke. This has been the result of a lack of immature material due to disruption of the production network. Continuity, integration, and solicitation depend on the level of national exposure to COVID-19, the level at which production operations are performed, and export guidelines, among other components. Although organizations may, however, take orders, delivery plans are unlikely to be adjusted.

During the forecast period, the space sector of the Artificial Intelligence in military market is predicted to develop at the quickest CAGR. according to the platform. CubeSats and satellites make up the space AI section. Artificial intelligence systems for space platforms include satellite components that serve as the foundation for numerous communication systems. AI integration with space platforms improves communication between spacecraft and base stations. The airborne platform segment is projected to have the biggest revenue share and dominate the global market in the near future. The increasing development of artificial intelligence-based aerial machinery, particularly in unmanned aerial vehicles, by important global market players is a key element supporting the expansion of the airborne segment in the next ten years.

According to the offer, the Software category is expected to grow at the fastest rate during the projection period. AI technological developments have led to the creation of advanced AI software and related software development kits. AI software embedded in computer systems is in charge of performing complex functions. It combines input from hardware systems and processes it in an AI system to produce an intelligent answer. The software category is expected to grow at the fastest rate due to the importance of AI software in improving IT architecture and preventing security breaches.

The United States and Canada are major countries for market study in the North American area. Because of growing expenditures on AI technology by governments in this region, this region is predicted to lead the market from 2024 to 2032. This market is dominated by the United States, which is boosting its investment in AI systems in order to preserve its military supremacy and overcome the risk of possible threats to computer networks. The United States intends to raise military spending on artificial intelligence in order to acquire a competitive advantage over other countries.

Key Market Segmentation

By Technology

-

Machine Learning

-

Computer vision

By Application

-

Information Processing

-

Cyber Security

-

Future Unmanned Aircraft System (FUAS)

-

Logistics

-

Others

By Offering

-

Software

-

Hardware

-

Services

By Installation Type

-

New Procurement

-

Upgrade

By Platform

-

Land

-

Naval

-

Airborne

Regional Analysis

In the North American military market study, the United States and Canada are significant nations considered for artificial intelligence (A.I.). This region is expected to lead the market from 2022 to 2028, owing to increased demand for A.I. advancements by countries nearby. This market is driven by the United States, which is increasingly investing in A.I. frameworks to maintain its fight dominance and counter the threat posed by computer organizations. The United States aims to increase military spending on artificial intelligence in order to gain a strategic advantage over other countries.

Need any customization research on Artificial Intelligence In Military Market - Enquiry Now

Regional Coverage

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

Key Players

The Major Players are Lockheed Martin, Raytheon, Spark Cognition, BAE Systems, Leidos, IBM, Northrop Grumman, Thales Group, Charles River Analytics, General Dynamics, L3 Harris Technologies, Rafael Advanced Defense Systems Ltd and other players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 9819.4 Million |

| Market Size by 2032 | US$ 39481.39 Million |

| CAGR | CAGR of 16.72% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Machine Learning, Computer vision) • By Application (Information Processing, Cyber Security, Future Unmanned Aircraft System (FUAS), Logistics, Others) • By Offering (Software, Hardware, Services) • By Installation Type • By Platform |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lockheed Martin, Raytheon, Spark Cognition, BAE Systems, Leidos, IBM, Northrop Grumman, Thales Group, Charles River Analytics, General Dynamics, L3 Harris Technologies, Rafael Advanced Defense Systems Ltd |

| DRIVERS | • IT Technology • Law enforcement organizations • Defense agencies |

| RESTRAINTS | • Complex battle circumstances • Automated Killer Robots • Lack of trained people |

Frequently Asked Questions

North America region dominated the Artificial Intelligence in Military Market.

The Covid-19 pandemic impacted the Artificial Intelligence in Military Market significantly. The detailed analysis is included in the final report.

The key players of the Artificial Intelligence in Military Market are Lockheed Martin Raytheon, Spark Cognition, BAE Systems Leidos, IBM, Northrop Grumman Thales Group, Charles River Analytics, General Dynamics L3 Harris Technologies, and Rafael Advanced Defense Systems Ltd.

The market size of the Artificial Intelligence in Military Market is expected to reach USD 39481.39 million by 2032.

The growth rate of the Artificial Intelligence in Military Market is 16.72% over the forecast period 2024-2032.

Get in Touch