Key Market Insights & Future Outlook:

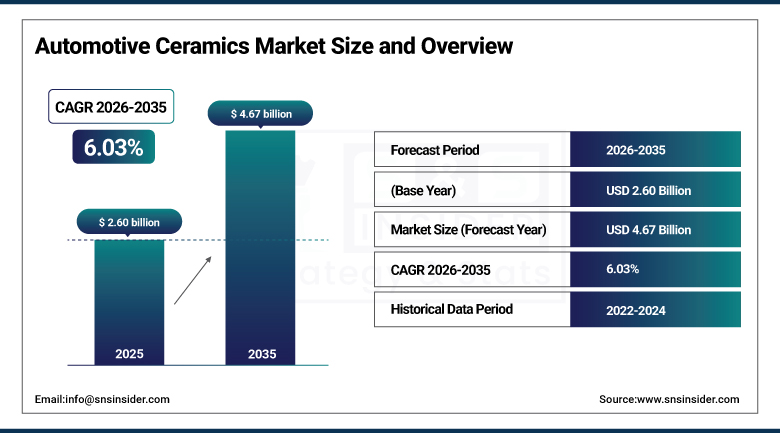

The Global Automotive Ceramics Market size was valued at USD 2.60 Billion in 2025 and is projected to reach USD 4.67 Billion by 2035, expanding at a CAGR of 6.03% during the forecast period 2026–2035.

Rapid advancements in vehicle electrification, increasing demand for thermal resistant materials and stringent global emission norms that are driving advanced ceramic integration throughout the automotive manufacturing ecosystem. High-performance ceramics are increasingly being incorporated into exhaust systems, sensors, battery insulation components, engine systems and power electronics by automotive OEMs to improve durability, thermal stability, fuel efficiency and emission control capabilities. In addition, the rising commercial use of electric vehicles and next-generation mobility platforms is driving investment in lightweight ceramic technologies.

Automotive component manufacturers invested in advanced ceramic substrate and EV power electronics insulation technologies for next-gen electric mobility architectures in 2026.

Market Size and Forecast

-

Market Size 2026E: USD 2.76 Billion

-

Market Size 2035: USD 4.67 Billion

-

CAGR: 6.03% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Automotive Ceramics Market - Request Free Sample Report

Automotive Ceramics Market Trends

-

Rising adoption of ceramic substrates across electric vehicle power electronics.

-

Increasing deployment of lightweight thermal-resistant automotive materials.

-

Growing commercialization of ceramic-based emission control technologies.

-

Expansion of automotive sensor integration across connected vehicle platforms.

-

Increasing investments in advanced braking and thermal management systems.

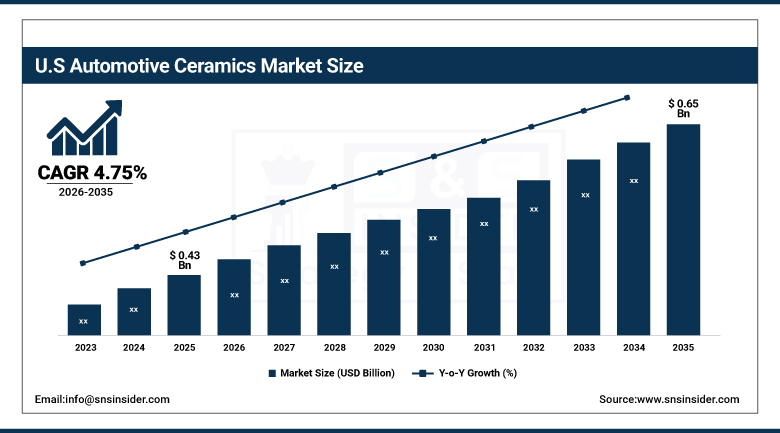

The U.S. Automotive Ceramics Market Size Outlook

The U.S. Automotive Ceramics Market was valued at USD 0.43 billion in 2025 and is expected to reach approximately USD 0.65 billion by 2035, expanding at a CAGR of 4.75% during 2026–2035.

The U.S. continues to be a technologically advanced automotive ceramics market with growing electric vehicle manufacturing and strong automotive R&D spending, and rapid adoption of advanced thermal management technologies across premium vehicle platforms. Automakers are using more ceramic materials in catalytic converters, braking systems, high-temperature sensors and EV battery insulation applications to boost vehicle efficiency and meet regulatory compliance. Also, increasing investments in semiconductor-driven automotive electronics are driving demand for advanced ceramic components in domestic supply chains.

A number of U.S. based automotive suppliers announced in 2025–2026 that they are expanding their ceramic substrate production capacities for EV power electronics and emission-control applications.

Automotive Ceramics Market Segment Analysis

-

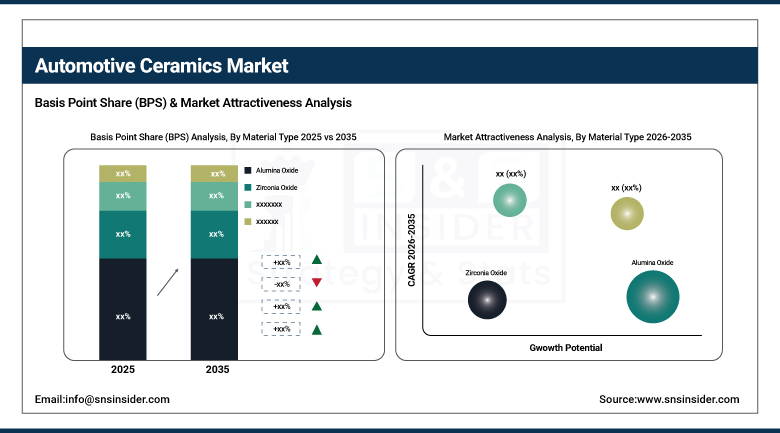

By Material Type, Alumina Oxide dominated the market with 42.00% share in 2025, while Zirconia Oxide is projected to witness the fastest growth with 7.02% CAGR during the forecast period.

-

By Vehicle Type, Passenger Vehicles dominated the market with 69.00% share in 2025, while Electric Vehicles are projected to witness the fastest growth with 8.68% CAGR during the forecast period.

-

By Application, Exhaust Systems dominated the market with 40.00% share in 2025, while Automotive Electronics are projected to witness the fastest growth with 9.73% CAGR during the forecast period.

By Material Type, Alumina Oxide dominated, while Zirconia Oxide is the fastest-growing segment.

The Alumina Oxide segment held the largest market share of 42.00% in 2025 due to its wide application in exhaust systems, spark plug insulators, catalytic converter substrates, and thermal-resistant automotive parts. It is still economical, has high dielectric strength and is durable, all of which continue to drive its widespread use in the automotive sector in both conventional and hybrid vehicles.

Zirconia Oxide is anticipated to record the highest CAGR of 7.02% owing to the growing adoption across oxygen sensors, EV power electronics, thermal barrier coatings, and advanced braking systems. The rising trends of electrification and the demand for high temperature stability are driving the commercial adoption across the globe. In 2025-2026, automotive component suppliers boosted investments in zirconia-based ceramic technologies supporting EV thermal management and intelligent sensor applications.

By Vehicle Type, Passenger Vehicles dominated, while Electric Vehicles are the fastest-growing segment.

The Passenger Vehicles segment accounted for the largest share of 69.00% of the market in 2025, owing to the high global production of passenger vehicles and increasing adoption of ceramic materials in exhaust systems, engine parts, braking systems, and onboard electronics. Growing consumer appetite for fuel-efficient, low-emission vehicles continues to spur the use of ceramics in mainstream automotive platforms.

The Electric Vehicles segment is growing owing to the rising use of ceramic substrates, battery insulation systems, semiconductor protection materials and thermal management technologies across the EV architecture. In 2026, some electric vehicle (EV) manufacturers extended their supply contracts for advanced ceramics used in battery safety systems and high-voltage automotive electronics.

By Application, Exhaust Systems dominated, while Automotive Electronics are the fastest-growing segment.

The Exhaust Systems segment held the largest revenue share of 40.00% in 2025 because of the widespread application of ceramic substrates in catalytic converters and emission-control systems. Increasingly stringent global emission standards are resulting in the growing demand for high-temperature resistant ceramic components that can enhance the efficiency of exhaust filtration and reduce vehicular pollutants.

The Automotive Electronics segment is anticipated to register the fastest CAGR of 9.73% owing to increasing semiconductor integration, EV electrification, autonomous driving technologies, and connected vehicle systems. Ceramic materials are finding ever-broader applications in sensors, circuit protection systems, capacitors and electronic insulation components. In 2025-2026, automotive electronics suppliers sped up commercialization of ceramic-based semiconductor protection technologies for next-generation electric mobility platforms.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

91.00% |

|

Europe |

Germany |

24.00% |

|

Asia Pacific |

China |

52.00% |

|

Middle East & Africa |

UAE |

3.00% |

|

Latin America |

Brazil |

3.00% |

North America Automotive Ceramics Market Insights

The North America region held 18.00% share of the automotive ceramics market in 2025, due to increasing adoption of electric vehicles, stringent emission regulations for automotive, and robust investments in advanced automotive manufacturing technologies. Automotive OEMs in the US and Canada are incorporating ceramic substrates, high temperature sensors and thermal management materials into next generation mobility platforms to enhance efficiency and emission compliance. The growth of regional markets will also be supported by higher semiconductor investments and expansion of EV battery manufacturing.

In 2026, several North American automotive suppliers expanded their ceramic substrate production capacities to support EV and emission-control uses.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Automotive Ceramics Market Insights

Strict carbon emission regulations, increasing adoption of electric vehicles and growing commercialization of lightweight automotive technologies in Europe accounted for around 24.00% of the global market in 2025. Germany, France and Italy are increasingly using ceramic materials in advanced braking systems, catalytic converters and automotive electronics to achieve vehicle efficiency improvements and sustainability goals.

In 2025-2026 several European automotive manufacturers increased investments into ceramic-based thermal insulation and EV semiconductor protection technologies.

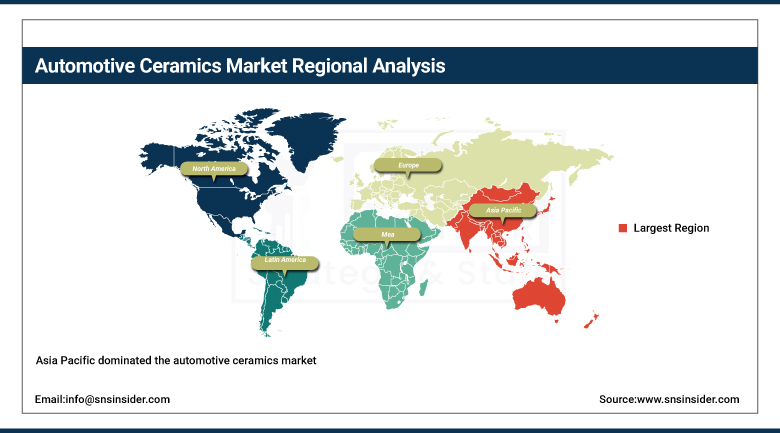

Asia Pacific Automotive Ceramics Market Insights

The Asia Pacific dominated the automotive ceramics market and is expected to remain the fastest growing regional market during the forecast period. The scale of ceramic adoption is being driven by strong vehicle manufacturing ecosystems, rapid EV commercialization and government supported electrification programmes across China, Japan, South Korea and India. Car makers are increasingly relying on ceramic battery insulation systems, emission-control substrates and thermally resistant components to ensure their vehicles are safe to operate and in compliance with regulations.

In 2026, many Asia Pacific EV manufacturers fast-tracked the roll-out of ceramic-integrated battery safety systems and high-performance automotive sensors.

Middle East & Africa and Latin America Automotive Ceramics Market Insights

The Middle East & Africa market is expected to witness gradual growth with the rising automotive imports, increasing infrastructure modernization, and growing adoption of fuel-efficient vehicles across GCC economies. Car service companies are increasingly using ceramic-based technologies for controlling emissions and managing heat to make vehicles last longer in very hot or very cold climates.

In 2025, Latin America held a 3.00% market share due to the growing automotive production activities in Brazil and Mexico, along with the gradual expansion of emission-control regulations. Growing demand for budget friendly passenger vehicles and expanding automotive component manufacturing capacities across the region are bolstering the market growth.

Market Dynamics

Growth Drivers: Rising electric vehicle production and strict emission regulations.

Ceramic materials have become popular in the automotive industry due to the emergence of tough emission requirements and rise in the production of electric vehicles worldwide. Automotive manufacturers are increasingly adopting ceramic substrates, insulation technology, catalytic converter products, and high temperature electronics to enhance energy efficiency, comply with emissions laws, and improve durability. Ceramic electronic components and thermal solutions are gaining increased prominence due to the rise in electric vehicles with semiconductor-based design architecture.

A number of automotive parts suppliers introduced advanced ceramic substrates for electric-vehicle power electronics in 2025.

Restraints: The costs of production are high and the manufacturing processes are complex.

Despite the strong long-term growth prospects, high manufacturing costs and complex ceramic processing technologies remain key challenges for this industry. Advanced ceramic materials require specialized production infrastructure, precision engineering and energy-intensive manufacturing processes, which increases overall operational costs for automotive suppliers. Profitability and large-scale commercialization in all cost-sensitive vehicle segments may also be affected by supply chain volatility of rare-earth materials and advanced industrial ceramics.

In 2026, the automotive component manufacturers will focus on enhancing the efficiency of ceramic production and supply-chain localization strategies to reduce operational costs.

Opportunities: EV power electronics and advanced thermal management systems expansion.

The rapid commercialization of electric, self-driving and connected vehicles presents significant growth opportunities for advanced ceramics manufacturers in automotive applications. Furthermore, the increasing use of ceramic parts in semiconductor protection systems, battery insulation and high temperature sensors improves the performance, safety and efficiency of cars. Other business opportunities are investments in lightweight cars and semiconductor production for EVs.

In 2025-2026, some automotive technology companies introduced advanced thermal management systems for electric vehicles based on ceramics.

Recent Developments

-

2026: Kyocera Corporation expanded its U.S. fine ceramics manufacturing operations in North Carolina by adding new cold isostatic pressing capabilities to support high-performance ceramic component production for automotive and semiconductor applications.

-

2026: Kyocera Corporation commercialized multilayer ceramic core substrates designed for advanced semiconductor packaging supporting AI-enabled automotive electronics and next-generation mobility systems.

-

2025: NGK Insulators Ltd. announced plans to triple translucent alumina wafer production capacity by 2027 to address growing semiconductor and autonomous vehicle electronics demand.

-

2025: CoorsTek Inc. expanded technical ceramics R&D programs focused on customized high-temperature ceramic solutions for automotive electronics, EV systems, and industrial thermal management applications.

Automotive Ceramics Market Key Players are:

-

Kyocera Corporation

-

CeramTec GmbH

-

Corning Incorporated

-

Saint-Gobain

-

NGK Insulators Ltd.

-

CoorsTek Inc.

-

Morgan Advanced Materials plc

-

Ibiden Co., Ltd.

-

Murata Manufacturing Co., Ltd.

-

3M Company

-

Elan Technology

-

Rauschert GmbH

-

Ferrotec Holdings Corporation

-

Ceradyne Inc.

-

Dyson Technical Ceramics

-

Superior Technical Ceramics

-

Maruwa Co., Ltd.

-

Blasch Precision Ceramics Inc.

-

McDanel Advanced Ceramic Technologies

-

International Syalons Ltd.

Automotive Ceramics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.60 Billion |

| Market Size by 2035 | USD 4.67 Billion |

| CAGR | CAGR of 6.03% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Retail Automation Assessment, Smart Checkout Technology Trends, AI-Enabled Retail Infrastructure Analysis, DROC & SWOT Analysis, Investment Trends, Supply Chain Evaluation, Consumer Transaction Technology Assessment, and Future Market Opportunity EvaluationChain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Material Type (Alumina Oxide, Zirconia Oxide, Titanate Oxide, Others) • By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles) • By Application (Exhaust Systems, Engine Parts, Automotive Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Kyocera Corporation, CeramTec GmbH, Corning Incorporated, Saint-Gobain, NGK Insulators Ltd., CoorsTek Inc., Morgan Advanced Materials plc, Ibiden Co., Ltd., Murata Manufacturing Co., Ltd., 3M Company, Elan Technology, Rauschert GmbH, Ferrotec Holdings Corporation, Ceradyne Inc., Dyson Technical Ceramics, Superior Technical Ceramics, Maruwa Co., Ltd., Blasch Precision Ceramics Inc., McDanel Advanced Ceramic Technologies, International Syalons Ltd. |

Frequently Asked Questions

The global automotive ceramics market was valued at USD 2.60 billion in 2025 and is expected to reach USD 4.67 billion by 2035, growing at a CAGR of 6.03%. This growth is fueled by rising electric vehicle production, stricter emission regulations, and the increasing use of advanced ceramic materials in modern vehicles.

Passenger vehicles accounted for the largest share of the automotive ceramics market in 2025, representing 69% of total revenue. High production volumes and the growing integration of ceramic components in engines, exhaust systems, braking systems, and vehicle electronics continue to support this segment's leadership.

Asia Pacific leads the global automotive ceramics market, supported by its strong automotive manufacturing industry and growing electric vehicle production. Countries such as China, Japan, South Korea, and India continue to drive regional demand through expanding production capacity and investments in advanced automotive technologies.

Get in Touch