Automotive LiDAR Market Report Scope & Overview:

The Automotive LiDAR Market size was estimated at USD 1.17 Billion in 2025 and is expected to reach USD 20.99 Billion by 2035 and grow at a CAGR of 33.53% over the forecast period of 2026-2035.

The Automotive LiDAR market delivers precise 3D sensing and object detection technologies for ADAS and autonomous vehicles, enabling features such as collision avoidance, adaptive cruise control, and automated parking. Market growth is fueled by increasing adoption of advanced driver assistance systems, expanding autonomous vehicle development, innovations in solid-state LiDAR, and rising demand for safer, efficient, and reliable vehicle perception. Leading players prioritize OEM partnerships, scalable solutions, and cost-effective LiDAR integration across passenger, commercial, and autonomous platforms.

Market Size and Forecast

-

Market Size in 2025: USD 1.17 Billion

-

Market Size by 2035: USD 20.99 Billion

-

CAGR: 33.53%

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Automotive LiDAR Market - Request Free Sample Report

Trends in the Automotive LiDAR Market

-

Rising ADAS Integration: Increasing adoption of advanced driver assistance systems in passenger and commercial vehicles is driving LiDAR demand.

-

Shift to Solid-State LiDAR: Solid-state LiDAR is replacing mechanical systems due to compact design, durability, and cost efficiency.

-

Autonomous Vehicle Development: Expansion of Level 3–5 autonomous driving programs is boosting LiDAR deployment.

-

OEM Partnerships & Series Production: Collaborations between LiDAR providers and automakers are accelerating factory-fitted integration.

-

Cost Reduction & Scalability: Technological advancements are lowering LiDAR prices, enabling mass-market adoption across vehicle segments.

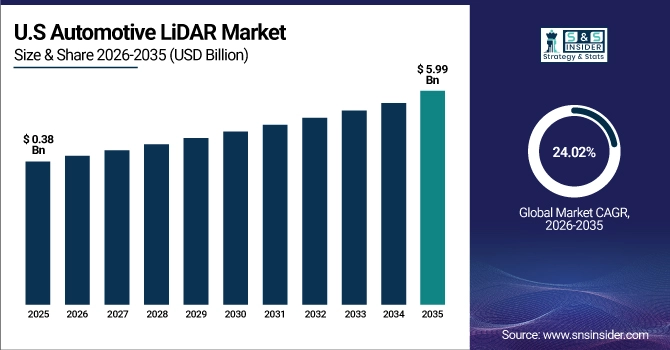

U.S. Automotive LiDAR Market Outlook:

The U.S. Automotive LiDAR Market is projected to grow from USD 0.38 Billion in 2025 to USD 5.99 Billion by 2035, at a CAGR of 24.02%. Growth is driven by rising adoption of ADAS, increasing autonomous vehicle development, advancements in solid-state LiDAR, supportive government regulations, and expanding OEM partnerships for next-generation mobility solutions.

Automotive LiDAR Market Growth Drivers:

-

Rising Adoption of ADAS and Autonomous Vehicles

The increasing integration of Advanced Driver Assistance Systems (ADAS) in new vehicles is a major growth driver for the Automotive LiDAR market. Globally, over 35% of new vehicles in 2025 are equipped with some ADAS features, such as lane-keeping assist, adaptive cruise control, and automatic emergency braking. This trend is complemented by rapid development of autonomous vehicles, with pilot programs for Level 3–5 autonomy expanding across multiple regions. LiDAR is essential for these technologies, enabling precise 3D perception and enhancing safety and reliability in modern vehicles.

Automotive LiDAR Market Restraints:

-

High Cost of LiDAR Sensors Limits Mass-Market Adoption

The high manufacturing and integration costs of LiDAR sensors remain a key challenge for widespread adoption in mass-market vehicles. Premium LiDAR systems, particularly mechanical variants, are expensive due to complex components and precision engineering requirements. This cost barrier makes it difficult for automakers to include LiDAR in entry-level and mid-range vehicles without significantly increasing vehicle prices. As a result, many manufacturers are prioritizing cost-effective solid-state LiDAR solutions or limiting deployment to premium and autonomous vehicle segments.

Automotive LiDAR Market Opportunities:

-

Expansion of OEM Partnerships for Factory-Fitted LiDAR Integration

Automakers are increasingly partnering with LiDAR technology providers to integrate sensors directly into vehicles at the factory level. Factory-fitted LiDAR ensures better system calibration, reliability, and seamless integration with vehicle electronics and ADAS platforms. These collaborations allow OEMs to offer advanced safety and autonomous features as standard or optional packages, accelerate time-to-market for new models, and scale LiDAR adoption across multiple vehicle platforms. Such partnerships are becoming a key strategy for mass-producing cost-efficient, high-performance LiDAR-equipped vehicles.

Automotive LiDAR Market Segmentation Analysis:

-

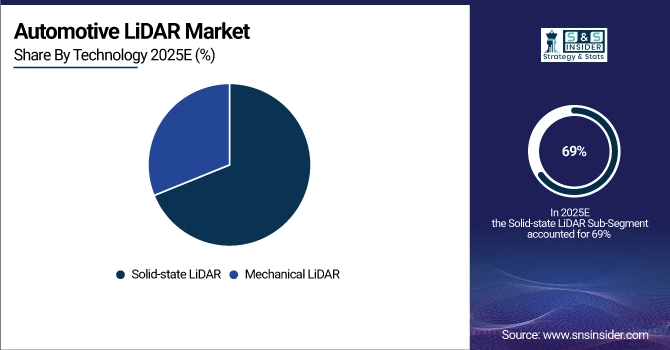

By Technology: In 2025, Solid-state LiDAR dominated with 69% share; it is also the fastest growing segment during 2026-2035

-

By Range: In 2025, Long-range LiDAR dominated with 47% share; Mid-range LiDAR fastest growing segment during 2026-2035

-

By Vehicle Type: In 2025, Passenger Cars dominated with 72% share; Robo-taxis & Autonomous Shuttles fastest growing segment during 2026-2035

-

By Application: In 2025, ADAS dominated with 58% share; Fully Autonomous Driving fastest growing segment during 2026-2035

By Technology: Solid-State LiDAR Dominates and Remains the Fastest-Growing Segment

Solid-state LiDAR dominates the automotive LiDAR technology segment due to its compact form factor, lower manufacturing cost, higher durability, and suitability for large-scale OEM integration. The absence of moving parts enables improved reliability and easier vehicle integration, supporting mass production across passenger and electric vehicles.

Solid-state LiDAR is also the fastest-growing technology, driven by rapid advancements in MEMS and flash LiDAR designs, increasing ADAS adoption, and automakers’ focus on scalable, cost-efficient sensing solutions for next-generation autonomous platforms.

By Range: Long-Range LiDAR Dominates as Mid-Range LiDAR Shows Accelerated Growth

Long-range LiDAR dominates the range segment as it enables early detection of vehicles, pedestrians, and obstacles at highway speeds, which is critical for advanced ADAS functions and autonomous driving beyond urban environments. These systems support forward-looking perception required for adaptive cruise control, lane-keeping, and collision avoidance.

Mid-range LiDAR is the fastest-growing segment, driven by its increasing use in urban driving scenarios, including intersection navigation, blind-spot detection, and automated parking. OEMs favor mid-range solutions due to cost optimization and their suitability for city-centric mobility applications.

By Vehicle Type: Passenger Cars Dominate as Robo-Taxis & Autonomous Shuttles Expand Rapidly

Passenger cars dominate the vehicle type segment due to rising safety regulations, increasing consumer awareness, and OEM efforts to differentiate vehicles through advanced safety and semi-autonomous features. Premium and electric vehicle segments are leading LiDAR adoption, with gradual penetration into mid-priced models.

Robo-taxis and autonomous shuttles are the fastest-growing vehicle category, supported by government-backed pilot programs, smart city initiatives, and mobility-as-a-service investments. These vehicles require multiple LiDAR units per platform, significantly increasing sensor demand per vehicle.

By Application: ADAS Dominates as Fully Autonomous Driving Gains Momentum

ADAS dominates the application segment as LiDAR is increasingly integrated to enhance object detection accuracy, depth perception, and redundancy alongside cameras and radar. Applications such as automatic emergency braking, pedestrian detection, and traffic jam assist are driving large-scale deployment.

Fully Autonomous Driving represents the fastest-growing application segment, driven by advances in AI-based perception, sensor fusion algorithms, and real-world validation data. As autonomous systems move closer to commercialization, LiDAR’s role as a critical safety sensor continues to strengthen.

Regional Insights

North America Automotive LiDAR Market Insights:

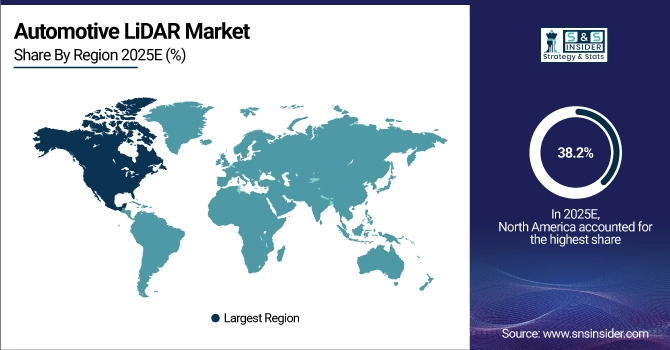

In 2025, North America dominates the global Automotive LiDAR market, accounting for approximately 38.2% of the total market share. The region’s leadership is driven by strong adoption of ADAS, early autonomous vehicle development, and the presence of leading LiDAR technology providers. OEMs actively collaborate with sensor manufacturers to integrate high-precision LiDAR, enhancing vehicle safety, perception, and autonomous driving capabilities across passenger and commercial vehicles.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Automotive LiDAR Market Insights:

Europe holds a significant share of the Automotive LiDAR market, driven by stringent vehicle safety regulations, rising adoption of ADAS, and growing autonomous vehicle initiatives. European OEMs are increasingly integrating factory-fitted LiDAR systems to enhance vehicle safety and perception capabilities. Strong collaborations between automakers and LiDAR technology providers support innovation, ensuring reliable, high-performance LiDAR solutions for passenger and commercial vehicles across the region.

Asia-Pacific Automotive LiDAR Market Insights:

Asia-Pacific is the fastest-growing Automotive LiDAR market, projected to expand at a CAGR of approximately 38.06% during 2026-2035. Growth is fueled by rapid adoption of ADAS, increasing autonomous vehicle development, and strong investments in smart mobility initiatives. OEMs and LiDAR providers are collaborating to integrate cost-effective, solid-state LiDAR solutions, supporting both passenger and commercial vehicles while meeting rising safety and technology demands in the region.

Latin America Automotive LiDAR Market Insights:

Latin America represents a smaller share of the Automotive LiDAR market. Growth is driven by gradual ADAS adoption, increasing awareness of vehicle safety, and emerging collaborations between regional automakers and LiDAR technology providers for advanced sensing solutions.

Middle East & Africa Automotive LiDAR Market Insights:

Middle East & Africa holds a smaller share of the Automotive LiDAR market. Growth is supported by rising interest in smart mobility, gradual adoption of ADAS features, and pilot autonomous vehicle programs in urban centers, encouraging LiDAR integration.

Automotive LiDAR Market Competitive Landscape:

Luminar Technologies, headquartered in Orlando, Florida, USA, is a leading player in the automotive LiDAR market, specializing in long-range LiDAR sensors designed for advanced driver assistance systems (ADAS) and autonomous driving applications. The company focuses on high-performance LiDAR hardware integrated with perception software to enable high-speed highway autonomy and enhanced vehicle safety, working closely with global automotive OEMs to support series production programs.

-

In April 2025: Luminar Technologies expanded its OEM partnerships by advancing series-production deployments of its next-generation Iris LiDAR platform, enhancing long-range detection capabilities and scalability for passenger vehicles.

Velodyne Lidar, headquartered in San Jose, California, USA, is a prominent contributor to the automotive LiDAR market, offering a broad portfolio of LiDAR sensors used across ADAS, autonomous vehicles, and intelligent transportation systems. The company leverages its expertise in 3D sensing, real-time perception, and sensor fusion to support automotive OEMs and mobility solution providers with reliable and cost-effective LiDAR technologies.

-

In April 2025: Velodyne Lidar strengthened its automotive product portfolio by introducing enhanced solid-state LiDAR solutions optimized for mass-market vehicles, focusing on improved resolution, reduced power consumption, and lower manufacturing costs.

Automotive LiDAR Market Key Players

-

Luminar Technologies

-

Velodyne Lidar

-

Ouster

-

Valeo SA

-

Continental AG

-

Quanergy Systems

-

AEye Inc.

-

Cepton Inc.

-

Robosense (Suteng Innovation Technology)

-

Ibeo Automotive Systems

-

Aeva Technologies

-

Baraja Pty Ltd

-

LeddarTech

-

Zvision Technologies

-

Seyond (formerly Innovusion)

-

Opsys Tech

-

Benewake

-

Scantinel Photonics

Automotive LiDAR Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.17 Billion |

| Market Size by 2035 | USD 20.99 Billion |

| CAGR | CAGR of 33.53% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology: (Mechanical LiDAR, Solid-state LiDAR (MEMS, Flash, Optical Phased Array)) • By Range: (Short-range LiDAR, Mid-range LiDAR, Long-range LiDAR) • By Vehicle Type: (Passenger Cars, Commercial Vehicles, Robo-taxis & Autonomous Shuttles) • By Application: (Advanced Driver Assistance Systems (ADAS), Semi-autonomous Driving (Level 2–3), Fully Autonomous Driving (Level 4–5)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Luminar Technologies, Velodyne Lidar, Ouster, Valeo SA, Hesai Technology, Innoviz Technologies, Continental AG, Quanergy Systems, AEye Inc., Cepton Inc., Robosense (Suteng Innovation Technology), Ibeo Automotive Systems, Aeva Technologies, Baraja Pty Ltd, LeddarTech, Zvision Technologies, Seyond (formerly Innovusion), Opsys Tech, Benewake, Scantinel Photonics |

Frequently Asked Questions

North America dominated the Automotive LiDAR Market in 2025.

The “solid-state LiDAR” segment dominated during the projected period.

The key drivers of the Automotive LiDAR Market include rising ADAS adoption, autonomous vehicle development, advancements in solid-state LiDAR technology, stricter safety regulations, and expanding OEM partnerships enabling scalable, cost-efficient integration.

The market was valued at USD 1.17 Billion in 2025 and is projected to reach USD 20.99 Billion by 2035.

The Automotive LiDAR Market is expected to grow at a CAGR of 33.53% during 2026–2035.

Get in Touch