Automotive Microcontrollers Market Report Scope & Overview:

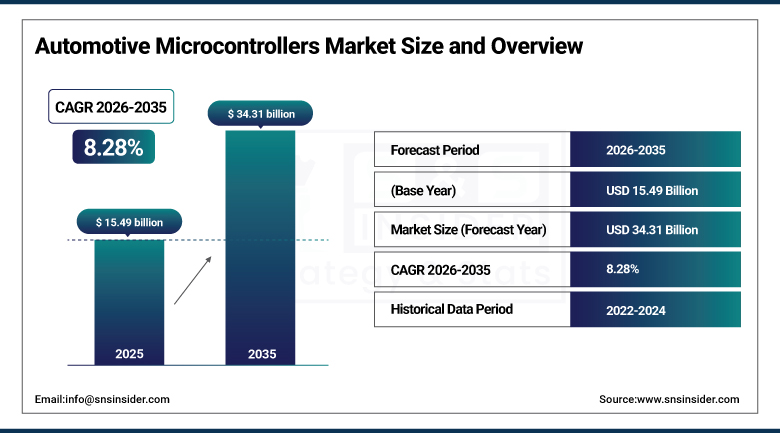

The Automotive Microcontrollers Market size was valued at USD 15.49 Billion in 2025 and is expected to reach USD 34.31 Billion by 2035, growing at a CAGR of 8.28% from 2026–2035.

Automotive microcontrollers are the embedded processing units that manage everything from engine timing to airbag deployment inside a modern vehicle. Automakers now fit dozens of these chips into a single car, and that number keeps climbing as vehicles take on more electronic functions. Growth in this market is closely tied to the spread of advanced driver-assistance systems, the shift toward electric powertrains, and rising consumer expectations for connected, software-driven vehicles. Passenger cars built today carry far more silicon than those sold a decade ago, and premium and electric models push that figure even higher because battery management, regenerative braking, and autonomous features all depend on dedicated controllers working in tandem.

On March 11, 2025, NXP Semiconductors introduced its S32K5 family of automotive microcontrollers, described as the industry's first 16-nanometer FinFET MCU with embedded magnetic RAM. Built to extend NXP's CoreRide platform, the S32K5 line targets zonal and electrification architectures for software-defined vehicles, giving automakers a pre-integrated path toward centralized vehicle computing. The launch signals how leading suppliers are racing to combine smaller process nodes with automotive-grade reliability as OEMs consolidate dozens of legacy electronic control units into fewer, more capable domain controllers.

Market Size and Forecast

-

Market Size in 2026E: USD 16.77 Billion

-

Market Size by 2035: USD 34.31 Billion

-

CAGR: 8.28% from 2026 to 2035

-

Fastest Growing Region: North America

-

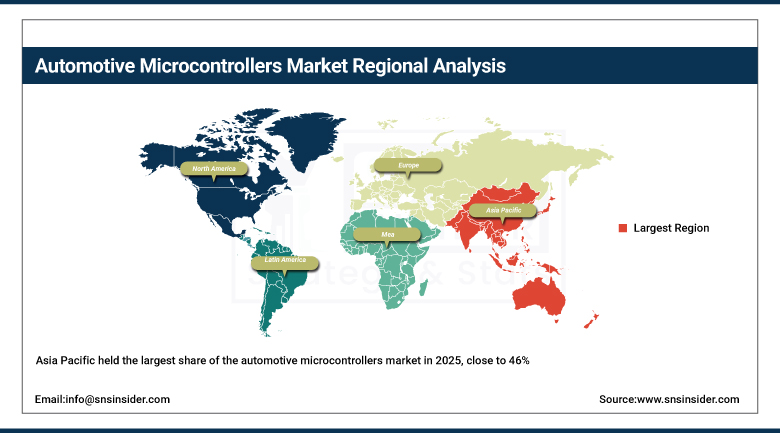

Largest Region: Asia Pacific

To Get more information on Automotive Microcontrollers Market - Request Free Sample Report

Automotive Microcontrollers Market Trends

-

Vehicles are carrying more microcontrollers per unit than ever, particularly in electric and premium models where multiple domain-specific MCUs coordinate battery, motor, and cabin functions.

-

Automakers are consolidating dozens of separate electronic control units into fewer, higher-performance zonal controllers, a shift that favors 32-bit MCUs capable of running multiple software functions at once.

-

Edge AI is moving into the vehicle itself, with microcontrollers now running machine learning models directly for tasks like driver monitoring and object recognition instead of relying on cloud processing.

-

Certification timelines for safety-critical MCUs remain a persistent bottleneck, as ISO 26262 and AEC-Q100 compliance can take well over a year to complete for new silicon.

-

Suppliers are investing in smaller process nodes and embedded memory technologies, such as magnetic RAM, to pack more performance into automotive-grade chips without sacrificing reliability.

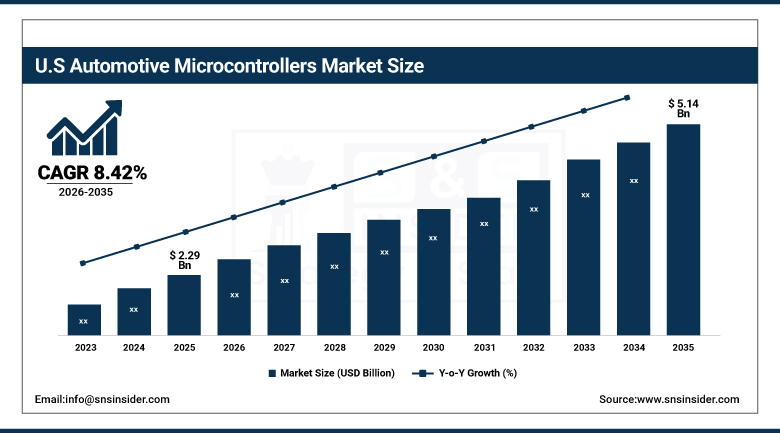

U.S. Automotive Microcontrollers Market Size Outlook

The U.S. Automotive Microcontrollers Market was valued at approximately USD 2.29 Billion in 2025 and is expected to reach approximately USD 5.14 Billion by 2035, growing at a CAGR of approximately 8.42%.

The United States remains one of the most technically advanced automotive microcontroller markets in the world, supported by a dense cluster of chipmakers, Tier-1 suppliers, and automakers investing heavily in electrification and driver-assistance technology. Texas Instruments, Microchip Technology, and On Semiconductor all maintain significant domestic design and manufacturing operations, while federal incentives under the CHIPS Act have encouraged new fabrication capacity aimed partly at automotive-grade chips. Rising EV adoption, tighter safety regulations, and growing demand for connected car features continue to push automakers toward higher microcontroller counts per vehicle.

In December 2024, Texas Instruments secured USD 1.6 billion in CHIPS Act funding to support the construction of three 300-millimeter fabrication plants in Utah and Texas, expanding domestic capacity for automotive-grade semiconductors. The investment reflects a broader push by U.S. chipmakers to reduce reliance on offshore foundries for safety-critical automotive components, a priority that gained urgency following the semiconductor shortages of recent years.

Automotive Microcontrollers Market Segment Analysis

-

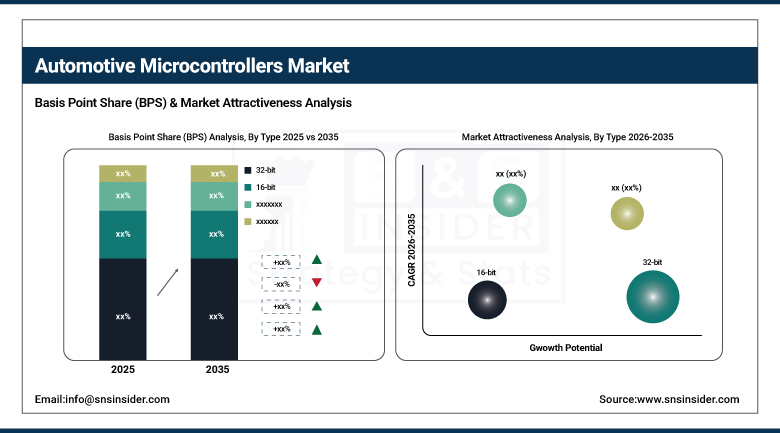

By Type, the 32-bit segment dominated the Automotive Microcontrollers Market with approximately 55% share in 2025, while the 16-bit segment is the fastest growing.

-

By Vehicle Type, the Passenger ICE Vehicle segment dominated the Automotive Microcontrollers Market with approximately 58% share in 2025, while the Electric Vehicle segment is the fastest growing.

-

By Technology, the Adaptive Cruise Control segment dominated the Automotive Microcontrollers Market with approximately 31% share in 2025.

-

By Application, the Chassis & Powertrain segment dominated the Automotive Microcontrollers Market with approximately 42% share in 2025, while the Infotainment & Telematics segment is the fastest growing.

By Type, 32-bit dominates, 16-bit grows fastest

The 32-bit segment accounted for about 55% of revenue share of the automotive microcontrollers market in 2025, owing to its ability to handle huge amounts of sensor data fast enough for ADAS applications, infotainment, and powertrain control systems. As opposed to 8-bit and 16-bit MCUs, 32-bit devices provide substantially larger computing power, and as vehicles become smarter and adopt more features driven by artificial intelligence, the need for such MCUs becomes apparent. Scalability of 32-bit MCUs across various types of vehicles ensures their dominance among both car makers and Tier-1 suppliers who produce connected and electrified vehicles.

The 16-bit segment shows the most significant growth rate compared to all other types of MCUs until 2035, being a perfect middle ground in terms of cost and performance for the body electronics, lighting, climate control system, and other mid-tier applications. As vehicles continue to be equipped with more and more electronic systems but cannot afford 32-bit MCU on each, 16-bit MCUs help to cope with that situation. Improved power management and architecture make them more suitable for electrified cars.

By Vehicle Type, passenger ICE dominates, EVs grow fastest

Passenger vehicles with internal combustion engines held about 58% of the market in 2025, simply because they still make up most vehicles sold worldwide. Every ICE vehicle needs microcontrollers to manage engine timing, transmission shifting, safety systems, and infotainment, and that broad base of demand hasn't gone away even as EV sales climb. In regions where charging infrastructure and vehicle costs still favor gasoline-powered cars, ICE vehicles will likely keep driving a large share of microcontroller demand for years to come.

Electric vehicles are the fastest-growing vehicle category for microcontroller demand, fueled by government incentives, tightening emissions rules, and rapid improvements in battery technology. EVs simply need more sophisticated electronics than conventional cars, particularly for battery management systems, power electronics, and increasingly autonomous driving features. As automakers keep pouring investment into EV platforms to meet consumer and regulatory expectations, microcontroller suppliers are seeing outsized growth from this segment relative to the broader market.

By Technology, adaptive cruise control leads, blind spot detection grows fastest

Adaptive cruise control accounted for around 31% of technology-segment revenue in 2025, reflecting how quickly this feature has moved from an expensive option to a near-standard offering on mid-range and premium vehicles alike. Consumer demand for safer, less fatiguing highway driving has pushed automakers to fit ACC across broader parts of their lineups, and the sensor fusion and AI processing required to make it work reliably keeps microcontroller content high in every vehicle equipped with the feature.

Blind spot detection is expanding quickly as regulators and safety rating agencies increasingly treat it as a baseline expectation rather than a premium add-on. The technology relies on radar or camera-based microcontrollers to monitor a vehicle's flanks continuously, and as automakers standardize it across more trims to earn top safety ratings, demand for the dedicated MCUs that run these systems is climbing at a faster pace than more established ADAS features.

By Application, chassis & powertrain dominates, infotainment grows fastest

Automotive microcontrollers used in chassis and powertrain accounted for about 42% of the total automotive MCUs market in 2025 and were the biggest application category by far. The engine management system, transmission control system, and electric powertrains all use microcontrollers, and as vehicle manufacturers continue to focus on increasing fuel efficiency and improved electric propulsion systems, this category continues to consume a sizable portion of MCU requirements.

The infotainment and telematics segment is seeing the strongest growth rate compared to other application segments due to high consumer demand for smart features inside the cabin. Infotainment systems have become very complicated in recent years due to the need for touch screens, voice assistance systems, connectivity to smartphones, and over-the-air software updates.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

45.0% |

|

North America |

United States |

85.0% |

|

Europe |

Germany |

24.0% |

|

Middle East & Africa |

Saudi Arabia |

28.0% |

|

Latin America |

Mexico |

38.0% |

Asia Pacific Automotive Microcontrollers Market Insights

Asia Pacific held the largest share of the automotive microcontrollers market in 2025, close to 46%, anchored by the region's dominant position in vehicle manufacturing. China, Japan, South Korea, and India together host the bulk of global automotive production, and each of these countries is also pushing hard into electric vehicles and driver-assistance features that require more silicon per car. China alone produces more vehicles than any other country, and its EV makers are aggressive adopters of new microcontroller platforms for battery management and autonomous driving functions. Japanese and South Korean suppliers, including Renesas and several established Tier-1 manufacturers, continue investing in regional fabrication capacity. Government support for domestic semiconductor production in China and India reinforces the region's lead and should keep Asia Pacific ahead of other markets through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Automotive Microcontrollers Market Insights

North America is expected to grow faster than any other region in the automotive microcontrollers market through 2035, driven by rapid EV adoption, expanding ADAS deployment, and a wave of new semiconductor investment inside the United States. Domestic chipmakers, including Texas Instruments, Microchip Technology, and On Semiconductor, are expanding fabrication capacity with support from CHIPS Act funding to reduce dependence on overseas foundries for safety-critical components. Automakers across Detroit and the Sun Belt are integrating more advanced driver-assistance and autonomous features into mainstream vehicles, pushing microcontroller counts higher with every model refresh. Canada contributes through its research base and growing EV supply chain, while Mexico's expanding vehicle assembly plants add further regional demand, together giving North America the fastest growth trajectory of any market covered in this report.

Europe Automotive Microcontrollers Market Insights

The European continent is still one of the developed and advanced automotive microcontrollers markets due to the presence of tough emission standards, a well-established cluster of luxury vehicle makers and early development of ADAS features. Germany takes the lion’s share of Europe's microcontrollers demand with a well-developed automotive engineering sector, where automakers and Tier-1 suppliers develop vehicles incorporating several dozen embedded control units. In addition, Germany is home to close cooperation between the local automotive industry and leading chip producers like Infineon and STMicroelectronics on new technologies for electric and self-driving cars. France, the UK and Italy complete the list of the regions with notable automotive microcontrollers demand; the increase in the number of produced EVs contributes to the growth of microcontrollers' consumption.

MEA & Latin America Automotive Microcontrollers Market Insights

The Middle East and Africa and Latin America remain smaller but steadily developing automotive microcontroller markets. Saudi Arabia leads demand in the Middle East, supported by growing vehicle assembly investment and government initiatives to build a domestic automotive manufacturing base as part of its broader industrial diversification agenda. South Africa contributes meaningfully through its established vehicle export industry. In Latin America, Mexico is the clear leader thanks to its role as a major assembly hub for North American automakers, with a rising share of exported vehicles carrying advanced driver-assistance and electrified powertrain systems that need more sophisticated microcontrollers. Brazil follows as the region's second-largest market, supported by domestic vehicle production and a gradually expanding electric vehicle segment.

Market Dynamics

Growth Drivers: ADAS adoption accelerating microcontroller demand across vehicle segments

Market growth in the automotive microcontrollers is greatly influenced by increasing adoption of advanced driver assistance systems. With the gradual adoption of driver assistance technologies such as adaptive cruise control, lane keeping assistance, and automatic emergency braking, which used to be offered only in high-end vehicles, automakers are forced to produce additional microcontrollers capable of processing camera, radar, and other sensor information in real time. Such companies as Nissan, Mobileye, and Volkswagen have already started using ADAS in their cars in recent years and there are no signs that this process will stop because of regulatory authorities imposing such systems as mandatory requirements in different countries. The transition to semi-autonomous and ultimately autonomous vehicles further adds to the demand because such a solution requires fail-safe microcontroller architecture.

Restraints: Lengthy safety certification cycles slow the pace of new MCU launches

Meeting safety and reliability standards is one of the biggest obstacles automotive microcontroller makers face. Chips used in braking systems, airbags, and driver-assistance functions must pass certifications such as ISO 26262 for functional safety and AEC-Q100 for automotive-grade reliability, and these processes are neither quick nor cheap. Depending on the complexity of the design, certification can take anywhere from six months to a year and a half, which slows how fast new chips reach production vehicles. For chipmakers trying to keep up with fast-moving trends like electrification and autonomous driving, that lag creates real competitive pressure. Smaller suppliers in particular struggle to absorb the cost and time required for certification, which can delay product launches or push them out of segments where larger competitors already have approved designs in place.

Opportunities: Edge AI processing creates demand for higher-performance automotive MCUs

Edge AI provides an important new opportunity for microcontroller makers as vehicles increasingly perform real-time processes without having to depend on cloud connection. Processing ML models at the vehicle level enables rapid responses for vital processes like object detection, driver monitoring, and predictive maintenance where milliseconds make the difference. This is leading to an increased need for high-performance microcontrollers that can process complex input data without increasing energy use and latency. With advanced driving assistance systems, infotainment, and sensor fusion solutions becoming increasingly reliant on AI technology, providers who will be able to offer highly capable edge computing chips for automobiles can expect to gain an increased market share.

Recent Developments:

-

2025: On April 9, 2025, Infineon Technologies agreed to acquire Marvell Technology's automotive Ethernet business for USD 2.5 billion, strengthening its microcontroller and networking portfolio to serve the growing demand for software-defined vehicles.

-

2025: On March 11, 2025, NXP Semiconductors launched its S32K5 family of automotive microcontrollers, the industry's first 16-nanometer FinFET MCU with embedded magnetic RAM, extending its CoreRide platform for software-defined vehicle architectures.

-

2025: Toshiba introduced seven new 32-bit microcontrollers based on the Arm Cortex-M4 core in January 2025, expanding its M4K and M470 product lines for motor control applications in consumer and industrial equipment.

Automotive Microcontrollers Companies are:

-

Infineon Technologies AG

-

STMicroelectronics NV

-

NXP Semiconductors NV

-

Texas Instruments Incorporated

-

Microchip Technology Inc.

-

Cypress Semiconductor Corporation

-

ON Semiconductor

-

Toshiba Corporation

-

Samsung Electronics

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

GlobalFoundries

-

Mitsubishi Materials Corporation

-

Advanced Micro Devices (AMD)

-

Analog Devices, Inc.

-

Robert Bosch GmbH

-

Continental AG

-

Denso Corporation

-

Koch Industries

Automotive Microcontrollers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.49 Billion |

| Market Size by 2035 | USD 34.31 Billion |

| CAGR | CAGR of 8.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (8-bit, 16-bit, 32-bit) • by Vehicle Type (Passenger ICE Vehicle, Commercial ICE Vehicle, Electric Vehicle) • by Technology (Park Assist System, Blind Spot Detection System, Adaptive Cruise Control, Tire Pressure Monitoring System) • by Application (Infotainment & Telematics, Chassis & Powertrain, Body Electronics, Safety & Security) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Infineon Technologies AG, Renesas Electronics Corporation, STMicroelectronics NV, NXP Semiconductors NV, Texas Instruments Incorporated, Microchip Technology Inc., Rohm Semiconductor Co., Ltd., Cypress Semiconductor Corporation, ON Semiconductor, Toshiba Corporation, Samsung Electronics, Taiwan Semiconductor Manufacturing Company (TSMC), GlobalFoundries, Mitsubishi Materials Corporation, Advanced Micro Devices (AMD), Analog Devices, Inc., Robert Bosch GmbH, Continental AG, Denso Corporation, Koch Industries. |

Frequently Asked Questions

The Automotive Microcontrollers Market was valued at USD 15.49 Billion in 2025.

The Automotive Microcontrollers Market is expected to grow at a CAGR of 8.28% from 2026 to 2035.

32-bit dominated with approximately 55% share in 2025, while 16-bit is the fastest growing segment.

Asia Pacific dominated the Automotive Microcontrollers Market in 2025 with approximately 46% market share, while North America is the fastest-growing region.

Rising adoption of advanced driver-assistance systems and growing vehicle electrification, both of which require more microcontrollers per vehicle for real-time sensor processing and control.

Get in Touch