Bakery Products Market Report Scope & Overview:

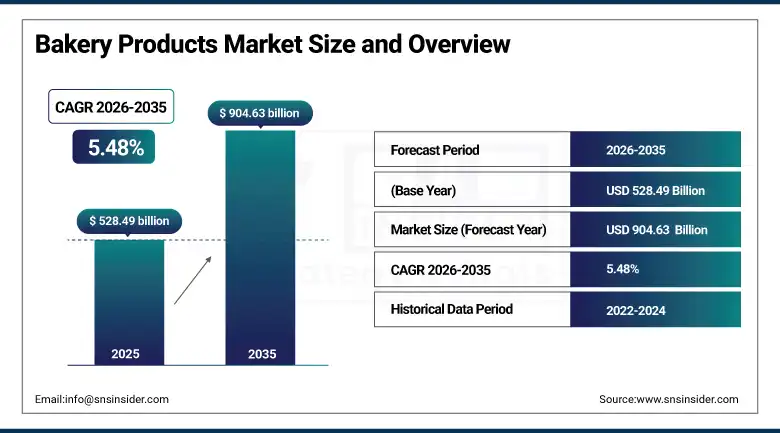

The bakery products market was valued at USD 528.49 Billion in 2025 and is expected to reach USD 904.63 Billion by 2035, growing at a CAGR of 5.48% from 2026–2035.

The global bakery products market occupies a foundational position in the global food system, serving as the daily caloric staple for billions of people across diverse cultures while simultaneously evolving into a sophisticated and innovation-driven category at the premium end where artisan, functional, and health-positioned products are commanding meaningfully higher consumer spending per occasion. The market’s resilience is structurally anchored by bread’s status as the world’s most universally consumed food product across all income demographics, yet its commercial dynamism is defined by the extraordinary pace of product innovation in specialty baked goods, free-from formulations, and premium artisan categories whose growth rates substantially exceed the mature bread market that provides the volume base. The bakery industry’s commercial landscape has been reshaped by three converging trends whose combined impact on product development, ingredient sourcing, and channel strategy is redefining competitive advantage across every market segment: the health and wellness movement demanding whole grain, high-fibre, reduced-sugar, and fortified bakery formulations whose nutritional credentials are prominently communicated through clean-label ingredient declarations; the convenience economy creating sustained demand for packaged, ready-to-eat, and on-the-go bakery formats that serve the time-compressed consumption occasions of urban professional populations; and the premiumisation current elevating consumer expectations for ingredient quality, artisanal production credentials, and gourmet flavour complexity across the cakes, pastries, and speciality bread categories that are growing fastest in value terms across both retail and foodservice channels.

The FAO’s 2025 global food security assessment confirming that wheat-based bakery products contribute more dietary calories per capita than any other processed food category underscores both the market’s humanitarian significance as a universal nutrition delivery vehicle and the commercial imperative of ensuring that bakery product innovation in the health and functional segments reaches the broad population base that consumes commodity bread and biscuits rather than remaining confined to the premium market niches where health positioning is currently most commercially developed.

Market Size and Forecast

-

Market Size in 2026E: USD 557.45 Billion

-

Market Size by 2035: USD 904.63 Billion

-

CAGR: 5.48% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

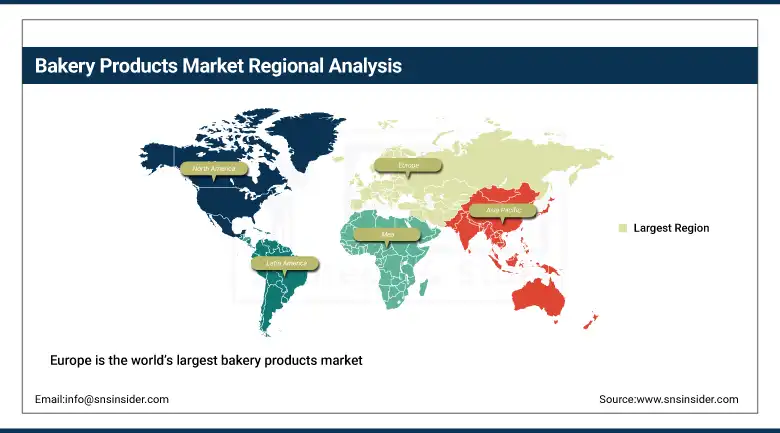

Largest Region: Europe

To Get more information On Bakery Products Market - Request Free Sample Report

Bakery Products Market Trends

-

Accelerating consumer shift toward whole grain, high-fibre, low-sugar, and fortified bakery products driven by the mainstream wellness movement’s influence on everyday food purchasing, with leading bakery manufacturers including Grupo Bimbo, General Mills, and Mondelez International reformulating core bread and biscuit lines to incorporate whole grain certification, reduced sodium content, and added functional ingredients whose nutritional credentials are prominently featured on front-of-pack labelling as primary purchase drivers for health-conscious consumer segments.

-

Growing demand for gluten-free, plant-based, and allergen-free bakery product lines that expand the accessible consumer base for premium bakery categories beyond the core wheat-tolerant majority to include the growing coeliac, gluten-sensitive, and dietary restriction-motivated consumer segments whose willingness to pay premium prices for safely formulated alternatives is driving above-average revenue growth in the free-from bakery sub-category across North American, European, and increasingly Asian retail markets.

-

Rapid expansion of the artisan and craft bakery segment whose consumers prioritise sourdough fermentation, ancient grain varieties including spelt, einkorn, and emmer, long-fermentation production methods, and locally sourced flour provenance as markers of authentic quality that mass-produced industrial bakery alternatives cannot credibly claim, creating a premium market positioning opportunity for both independent artisan bakeries and large-scale manufacturers willing to develop artisan-credentialed product lines through specialised production processes.

-

Rising investment in automated and smart bakery production technologies including AI-driven dough consistency monitoring, precision oven temperature control, robotics-assisted decoration and packaging, and supply chain visibility platforms that enable large-scale bakery operators to simultaneously improve product consistency, reduce ingredient waste, compress production lead times, and maintain the formulation flexibility required to serve the growing variety of dietary preference and occasion-specific product lines that modern retail and foodservice buyers require.

-

Significant growth of online bakery retail through e-grocery platforms, subscription-based fresh bread delivery services, and direct-to-consumer artisan bakery e-commerce that is extending premium bakery product access beyond the geographic catchment areas of physical speciality bakeries to nationwide consumer audiences whose discovery of new bakery brands through social media content is creating purchase intent that online retail channels convert without requiring physical store presence.

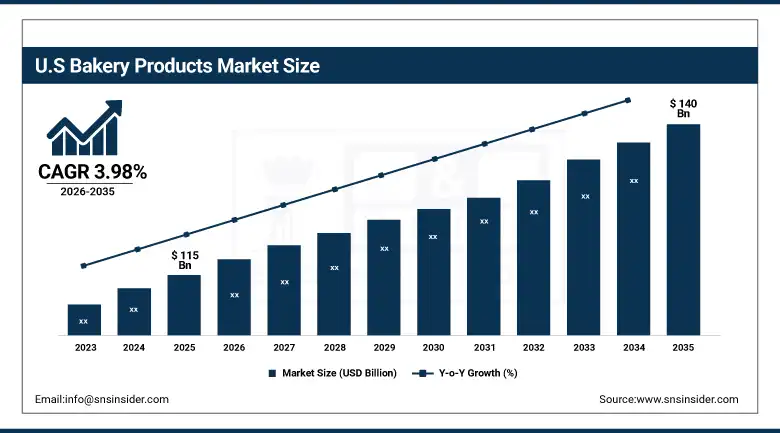

U.S. Bakery Products Market Outlook

The U.S. bakery products market was valued at approximately USD 115 Billion in 2025 and is expected to reach approximately USD 140 Billion by 2035, growing at a CAGR of approximately 3.98%.

The United States bakery market is the world’s most commercially sophisticated and innovation-intensive national bakery market, characterised by the simultaneous maturity of the volume-driven commodity bread and biscuit sector whose major producers including Bimbo Bakeries USA, Flowers Foods, and Campbell Soup’s snack division compete primarily on distribution scale and promotional pricing, and the extraordinary vitality of the premium artisan, health-positioned, and functional bakery segment whose growth rates consistently exceed the broader market.

Sara Lee’s January 2025 launch of a new white bread infused with the nutritional equivalent of one cup of vegetables, fortified with vitamins A, D, and E under the Bimbo Bakeries USA brand portfolio, exemplifies the mainstream bakery industry’s commercial response to consumer demand for nutritional density in everyday staple food formats where the functional fortification must be delivered without compromising the taste, texture, and familiar sensory characteristics that mass-market bread consumers prioritise above all other purchase considerations.

Bakery Products Market Segment Analysis

-

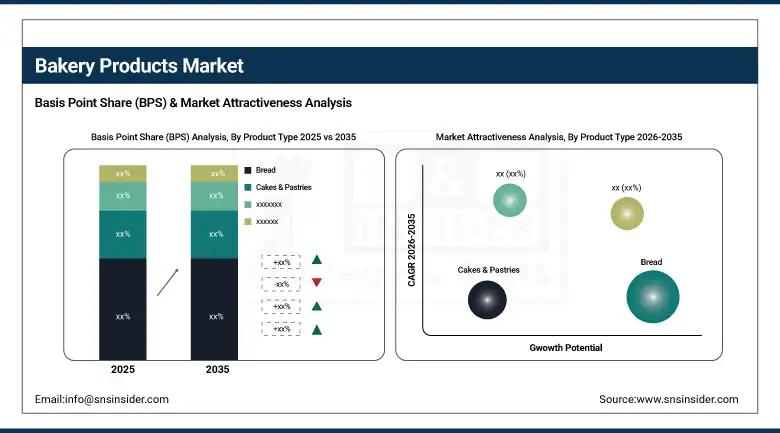

By Product Type, bread dominated with approximately 54.11% share in 2025 through its universal daily consumption status and extraordinary production volume of approximately 13.2 million tons annually; cakes & pastries are the fastest-growing product segment with 5.1 million tons output in 2025, driven by urban café culture expansion, premiumisation, and growing on-the-go consumption occasions.

-

By Ingredient Type, wheat flour led with approximately 20.5 million tons consumed in 2025 through its foundational role across every bakery product category globally; oats are the fastest-growing ingredient type driven by clean-label positioning, high-fibre health credentials, and growing consumer demand for functional breakfast bakery products with verified nutritional benefits.

-

By Form, fresh bakery dominated with approximately 15.1 million tons in 2025 driven by consumer preference for freshly baked goods in home and foodservice contexts; packaged and frozen is the fastest-growing form, driven by convenience demand, extended shelf life for on-the-go consumption, and the expansion of frozen bakery into retail channels serving time-compressed household meal planning.

-

By End Use, retail and household consumption dominated the bakery products market in 2025 as the primary channel for daily bread, biscuit, and packaged bakery product purchase across all geographies; foodservice and HoReCa is the fastest-growing end use driven by café culture expansion, quick-service restaurant bakery category development, and catering sector investment in premium baked goods.

-

By Distribution Channel, supermarkets & hypermarkets dominated with approximately 54.61% share in 2025 as the primary mass market bakery purchasing channel; online retail is the fastest-growing channel at a CAGR of approximately 7.28% driven by e-grocery integration, subscription fresh delivery services, and direct-to-consumer artisan brand development.

By Product Type, bread dominates, cakes & pastries grow fastest

Bread retained the dominant product type position with approximately 54.11% of the bakery products market in 2025, a dominance grounded in the product category’s extraordinary dual character as both a nutritional staple consumed multiple times daily across virtually every demographic and cuisine tradition globally and an increasingly dynamic innovation category at its premium tier where sourdough, ancient grain, seeded, and artisan variety bread is experiencing above-average value growth. The bread segment’s commercial leadership is reinforced by the repetitive purchase behaviour of staple food consumption, where household bread buying occurs on a weekly or more frequent basis without the deliberate purchase consideration that higher-involvement food categories require, creating a volume consistency that is unmatched by any other bakery product segment regardless of its premium growth trajectory. Industrial bread manufacturers including Grupo Bimbo’s extensive brand portfolio, Flowers Foods’ regional brand network, and Bimbo Bakeries USA’s national distribution infrastructure have built commercial ecosystems of scale and logistics efficiency that sustain the bread segment’s dominant market position through the competitive pressures of private label growth, health format expansion, and artisan premium alternatives that are progressively capturing share at the value-added end of the segment without displacing the high-volume commodity bread base that defines the category’s market size.

Cakes and pastries are the fastest-growing product segment at a CAGR exceeding the market average through 2035, driven by the convergence of several powerful consumer trends that are progressively elevating this category’s commercial importance relative to its historically secondary position behind bread in the bakery product hierarchy. The global café culture expansion across tier-one and tier-two cities throughout Asia Pacific, the Middle East, and Latin America is creating new food service consumption occasions for premium pastries, croissants, and speciality cakes that position themselves as experiential treat purchases aligned with the coffee culture socialisation occasion rather than everyday functional nutrition. Premiumisation is simultaneously transforming the retail cakes and pastries segment, with seasonal gifting collections, single-serve premium cake formats, and artisan patisserie-inspired retail products commanding per-unit retail values that substantially exceed standard supermarket cake equivalents and whose margin contribution per kilogram of finished product rivals the most commercially attractive segments in the broader food industry.

By Ingredient Type, wheat flour dominates, oats grow fastest

Wheat flour retained the dominant ingredient type position, accounting for approximately 20.5 million tons of bakery ingredient consumption in 2025, a structural dominance that reflects its irreplaceable role as the protein and starch matrix that provides the gluten network structure, gas retention capacity, and crumb formation characteristics that define bread, pastry, cake, and biscuit texture across virtually every baked good category consumed globally. The wheat flour segment’s dominance is unlikely to be significantly challenged across the forecast period, as the gluten network’s unique functional properties in bakery applications have not been replicated by any alternative flour ingredient at comparable cost and scale, ensuring that wheat flour’s foundational role in industrial bakery production remains intact even as specialty and alternative flour additions increasingly modify its functional characteristics for health and premium product formulations. The wheat flour market’s internal evolution toward higher-specification wholegrain, stone-ground, and ancient variety wheat flours whose premium pricing reflects both their enhanced nutritional profile and their differentiated production provenance is generating revenue growth within the category that partially compensates for any volume softening from consumers substituting alternative carbohydrate sources.

Oats are the fastest-growing bakery ingredient type, driven by the extraordinary commercial momentum of oat-based bakery formulations that capitalise on oats’ scientifically validated cardiovascular health benefits, FDA-approved beta-glucan soluble fibre health claim, naturally clean-label composition that requires no artificial additives to achieve functional bakery performance, and the distinctive sensory texture that consumers have come to associate with the wholesome, hearty, natural quality credentials that health-positioned bakery products need to communicate convincingly. The breakfast bakery segment is the primary commercial driver of oat ingredient growth, where oat-based granola bars, oat muffins, oat breakfast biscuits, and oat-enriched bread loaves are collectively creating a high-growth product category whose consumer base’s above-average health consciousness and willingness to pay premium prices for oat-forward formulations supports the higher ingredient cost that oat inclusion at meaningful percentages imposes on standard wheat-flour bakery economics.

By Form, fresh dominates, packaged/frozen grows fastest

Fresh bakery retained the dominant form position with approximately 15.1 million tons in 2025, reflecting the enduring consumer preference for the superior sensory experience of freshly baked goods whose crust crunch, crumb softness, aroma intensity, and flavour freshness cannot be replicated by packaged alternatives whose shelf life preservation requirements impose sensory compromises that bakery consumers consistently rank as inferior in taste and texture evaluation studies. The fresh bakery segment’s commercial strength is built on the daily traffic generation capability of in-store bakery departments in major supermarkets, the cultural centrality of the local bakery shop in European and Latin American food culture, and the operational reality that freshly baked goods’ rapid quality degradation creates a natural repeat purchase rhythm that sustains the segment’s volume dominance without requiring promotional investment. In-store bakery and artisan bakery café investment by major grocery retailers including Whole Foods, Carrefour, and REWE reflects the category’s strategic importance as a quality signalling and traffic-driving department whose premium positioning benefits the retailer’s overall brand perception alongside its direct category revenue contribution.

Packaged and frozen bakery is the fastest-growing form segment, driven by the powerful consumer convenience trend whose commercial expression in bakery is the growing demand for extended shelf-life products that can be purchased weekly rather than daily, stored at ambient temperature or in the freezer without quality degradation, and consumed on-the-go without preparation requirements that the increasingly time-constrained daily schedules of urban working populations cannot accommodate around traditional fresh bakery consumption occasions. The frozen bakery segment has been specifically transformed by the development of premium frozen croissants, frozen sourdough loaves, and frozen artisan bread rolls that can be oven-baked from frozen in minutes to deliver a fresh-baked quality experience whose sensory characteristics substantially exceed standard ambient packaged bakery alternatives, creating a compelling consumer value proposition that premium grocery retailers are building significant frozen bakery sections to service.

By Distribution Channel, supermarkets dominate, online retail grows fastest

Supermarkets and hypermarkets retained the dominant distribution channel position with approximately 54.61% of the bakery products market in 2025, a dominance reflecting their role as the primary weekly food shopping destination for the majority of global consumers whose bakery purchasing is concentrated in the regular grocery shop where bread, biscuits, cakes, and packaged bakery goods are purchased alongside other household staples without requiring a dedicated trip to a specialist bakery retailer. The supermarket channel’s bakery competitive advantage encompasses the combination of in-store bakery departments providing fresh-baked quality daily, extensive ambient packaged bakery sections offering the full brand portfolio including private label and premium branded products at competitive pricing, and the basket-building economics of bakery’s high purchase frequency that makes it a critical category anchor for the overall grocery shopping mission. Major supermarket investments in premium in-store bakery infrastructure, artisan bread programmes, and self-service patisserie counters are progressively closing the quality gap with specialist bakery retailers while maintaining the pricing and convenience advantages that general grocery retail provides to the consumer.

Online retail is the fastest-growing distribution channel at a CAGR of approximately 7.28% through 2035, driven by the structural expansion of e-grocery penetration across all major markets combined with the specific commercial dynamics of subscription-based fresh bread delivery, artisan bakery direct-to-consumer e-commerce, and meal kit integration of premium baked goods that are creating new consumer engagement models for bakery products that did not exist at commercial scale five years ago. The premium artisan bakery direct-to-consumer segment is particularly commercially dynamic, as sourdough subscription services, monthly artisan bread box clubs, and speciality bakery online shops are building subscription-revenue business models whose recurring purchase economics and direct customer relationship advantages substantially exceed the wholesale margin and promotional cost structures of traditional retail channel distribution.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

54.6% |

|

Europe |

Germany |

21.8% |

|

Asia Pacific |

China |

43.5% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

38.7% |

North America Bakery Products Market Insights

North America is the world’s second-largest bakery products market by value, with the United States accounting for approximately 54.6% of North American revenues and approximately 20% of global bakery product revenues, driven by the extraordinary scale of the country’s branded packaged bakery sector whose distribution infrastructure, marketing investment, and production efficiency collectively define the commercial template that global bakery companies benchmark against for operational excellence. The U.S. market’s commercial dynamics are defined by the tension between the mature, volume-driven commodity bread and biscuit sector where market share is contested through pricing, distribution, and promotional investment, and the rapidly growing premium and health-positioned bakery segment where product innovation, clean-label formulation, and brand storytelling create the differentiation that justifies premium pricing and sustains consumer loyalty beyond the transactional repeat purchase that commodity bakery products generate. Canada contributes the remaining approximately 45.4% of North American bakery revenues through a market that mirrors U.S. health and premium trends with a particular emphasis on clean-label formulations and artisan-positioned products that align with Canadian consumers’ above-average environmental and health consciousness.

Europe Bakery Products Market Insights

Europe is the world’s largest bakery products market by value and the region where bakery culture is most deeply embedded in national culinary identity, with France’s boulangerie tradition, Germany’s extraordinary bread diversity encompassing over 3,000 registered bread varieties, Italy’s regional artisan bread and pastry heritage, and the UK’s strong packaged bread and biscuit consumption culture collectively creating the world’s most commercially sophisticated and quality-conscious bakery consumer base. Germany accounts for approximately 21.8% of European bakery revenues as the region’s largest national market, with the world’s most diverse and technically sophisticated bread culture that has generated a premium artisan bakery segment of extraordinary depth alongside the industrial packaged bread sector whose automation investment and production efficiency standards benchmark with any global bakery market. The European bakery market’s regulatory environment is simultaneously shaping product formulation through the EU’s clean-label and nutritional labelling requirements, which are driving reformulation of mainstream bread and biscuit lines to reduce salt, sugar, and saturated fat content while expanding whole grain and fibre inclusion to comply with progressively tightening EU food quality standards.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Bakery Products Market Insights

Asia Pacific is the fastest-growing regional bakery products market, driven by the extraordinary pace of dietary Westernisation across China, India, Southeast Asia, and South Korea whose urban middle-class populations are progressively integrating bread, pastry, and packaged biscuit consumption into daily eating patterns that were historically centred on rice, noodle, and local grain-based staples. China accounts for approximately 43.5% of Asia Pacific bakery revenues through its combination of the world’s largest urban middle-class consumer population whose growing breakfast bakery adoption, café culture engagement, and premium pastry purchasing are collectively driving above-market bakery category growth rates alongside a large and growing industrial biscuit and packaged snack bakery sector that serves the country’s vast snacking occasion. India represents the most commercially significant emerging bakery market in Asia Pacific, as the country’s extraordinary demographic scale and rapidly rising urban disposable incomes are creating the conditions for structural bakery market growth whose pace is being supported by organised retail infrastructure expansion, Western fast food chain penetration that normalises bread consumption occasions, and domestic bread manufacturer investment from companies including Britannia Industries and Parle Products in distribution network and production capacity that extends bakery product accessibility to tier-two and tier-three city consumer populations.

MEA & Latin America Bakery Products Market Insights

The Middle East and Africa and Latin America are growing bakery products markets where the combination of young and growing urban populations, rising disposable incomes, expanding organised retail infrastructure, and the strong cultural traditions of bread and bakery product consumption in both regions are creating sustained market growth across both everyday staple bakery categories and premium artisan segments that are growing fastest in the major metropolitan areas of each region. Saudi Arabia leads Middle East and Africa bakery revenues at approximately 31.2% of the regional total through its combination of a young, Westernisation-influenced consumer population with substantial discretionary food spending capacity, a developed organised grocery retail sector providing wide bakery product distribution, and the significant café and foodservice sector that has expanded rapidly alongside tourism, entertainment sector development, and the social liberalisation policies of Vision 2030 that are creating new public leisure occasions for premium bakery consumption. Brazil leads Latin American bakery revenues at approximately 38.7% of the regional total through the country’s extraordinary bread culture where the daily pão de queijo and fresh bread consumption traditions sustain high per-capita bakery product consumption alongside a growing premium pastry and artisan bread segment serving major urban centres.

Market Dynamics

Growth Drivers: Rising consumer demand for health-positioned and functional bakery innovation, convenience and on-the-go format expansion, and premiumisation driving average unit price growth across artisan and speciality bakery segments

The primary structural growth drivers for the bakery products market are the health and wellness movement’s commercial transformation of consumer bakery purchasing from a purely habitual staple food decision into an active nutritional choice where whole grain, fibre content, reduced sugar, and clean-label formulation credentials are evaluated alongside price and taste, creating a value-added innovation opportunity that is simultaneously improving the category’s revenue per unit economics and sustaining consumer engagement with bakery products in markets where health-driven dietary restriction might otherwise reduce consumption frequency. The convenience economy’s influence on bakery consumption occasions is creating growing demand for portion-controlled, individually packaged, long-shelf-life, and breakfast-ready bakery formats whose distribution through convenience, petrol station, and on-the-go retail channels extends the category’s commercial reach into purchase occasions where traditional supermarket bakery formats cannot compete. The globalisation of café culture into emerging markets across Asia Pacific, the Middle East, and Latin America is simultaneously expanding the foodservice bakery channel by creating new premium pastry and speciality bread consumption occasions among urbanising populations whose income growth is enabling discretionary food experiences that artisan and branded bakery products serve.

Restraints: Wheat and commodity ingredient price volatility creating cost pressure, health concerns around ultra-processed foods affecting mass market segment image, and competitive intensity from private label reducing branded bakery pricing power

A significant restraint on the bakery products market is the commodity input cost volatility that characterises the bakery industry’s procurement economics, where wheat flour, edible oil, dairy, sugar, and energy costs that collectively represent 40 to 60% of total bakery production cost are subject to price fluctuations driven by agricultural season variability, currency movements, energy price cycles, and geopolitical supply chain disruptions that create margin pressure for bakery manufacturers whose retail pricing cannot always be adjusted quickly enough to recover input cost increases without volume loss in price-sensitive consumer segments. The growing consumer and media discourse around ultra-processed food health concerns, where mass-produced industrial bread and packaged bakery products are increasingly cited alongside confectionery and sugary beverages in health advocacy campaigns opposing high-additive food categories, creates a reputational challenge for mainstream bakery brands whose formulation complexity and long ingredient lists position poorly against the clean-label narrative that is progressively defining premium bakery product quality standards.

Opportunities: Functional and fortified bakery innovation for health-positioned premium segments, frozen premium bakery convenience growth, and Asia Pacific first-time bakery consumption expansion in emerging urban markets

The functional and fortified bakery innovation opportunity represents the most commercially significant near-term product development direction for established bakery manufacturers, as the demonstrated consumer willingness to pay premium prices for bread, biscuits, and pastry products with clinically validated nutritional benefits including beta-glucan cholesterol reduction, high-protein muscle health support, probiotic digestive benefit, and micronutrient fortification creates a high-margin product development pathway that simultaneously addresses health-conscious consumer demand and defends the bakery category’s competitive position against the protein bars, functional snacks, and meal replacement products that compete for the same health-motivated food occasion budget that functional bakery can serve with the taste familiarity and cultural embeddedness advantages that entirely new food format competitors cannot replicate.

Recent Developments:

-

2025: Bimbo Bakeries USA launched a new fortified white bread under the Sara Lee brand in January 2025, incorporating the nutritional equivalent of one cup of vegetables per loaf alongside vitamins A, D, and E fortification, addressing mainstream consumer demand for nutritional density in everyday staple bread without compromising the familiar taste and texture expectations of the mass-market white bread consumer segment.

-

2025: General Mills expanded its gluten-free bakery range with new Betty Crocker and Pillsbury certified gluten-free product lines across retail channels in North America, responding to growing coeliac disease awareness and the broader gluten-free dietary preference trend that has expanded the commercially addressable free-from bakery consumer segment beyond medically diagnosed patients into the larger wellness-motivated lifestyle choice population.

-

2025: Grupo Bimbo accelerated its sustainability-led reformulation programme across its global bread portfolio, reducing sodium content in core bread lines across its U.S., Latin American, and European brand portfolio and introducing paper-based packaging for premium bread lines in markets where plastic packaging regulation and consumer sustainability expectations are creating commercial motivation for packaging innovation investment.

-

2025: Mondelez International launched premium artisan-positioned biscuit collections under its Belvita and LU brand portfolios in European markets, incorporating ancient grain ingredients including spelt and rye and adopting artisan-credential packaging design that positions the products in the premium speciality biscuit segment alongside independent artisan producers rather than competing as standard industrial biscuit alternatives.

-

2025: Flowers Foods invested in automated production line technology upgrades across multiple U.S. baking facilities, implementing AI-driven dough quality monitoring and precision oven control systems that reduce batch-to-batch consistency variation, improve production yield, and enable more rapid new product development iteration for the company’s growing range of speciality and health-positioned bread products.

Bakery Products Market Key Players

-

Grupo Bimbo S.A.B. de C.V.

-

Mondelez International Inc.

-

General Mills Inc.

-

Flowers Foods Inc.

-

Britannia Industries Ltd.

-

Parle Products Pvt. Ltd.

-

ITC Limited

-

Campbell Soup Company (Pepperidge Farm)

-

Hostess Brands Inc.

-

Puratos Group

-

Associated British Foods plc (Allied Bakeries)

-

Kellogg Company

-

Aryzta AG

-

Dawn Food Products Inc.

-

Rich Products Corporation

-

Harry Brot GmbH

-

Mestemacher GmbH

-

Finsbury Food Group plc

-

Lantmännen Unibake

-

Barilla Group

Bakery Products Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 528.49 Billion |

| Market Size by 2035 | USD 904.63 Billion |

| CAGR | CAGR of 5.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Bread, Cakes & Pastries, Cookies & Biscuits, Morning Goods, Others) • By Ingredient Type (Wheat Flour, Sugar & Sweeteners, Fats & Oils, Oats, Others), • By Form (Fresh, Packaged/Frozen) • By End Use (Retail/Household, Foodservice/HoReCa) • By Distribution Channel (Supermarkets & Hypermarkets, Specialty Bakeries, Convenience Stores, Online Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Grupo Bimbo S.A.B. de C.V., Mondelez International Inc., General Mills Inc., Flowers Foods Inc., Britannia Industries Ltd., Parle Products Pvt. Ltd., ITC Limited, Campbell Soup Company (Pepperidge Farm), Hostess Brands Inc., Puratos Group, Associated British Foods plc (Allied Bakeries), Kellogg Company, Aryzta AG, Dawn Food Products Inc., Rich Products Corporation, Harry Brot GmbH, Mestemacher GmbH, Finsbury Food Group plc, Lantmännen Unibake, Barilla Group |

Frequently Asked Questions

Europe dominated the bakery products market in 2025, with germany as the largest national market within the region.

Bread dominated with approximately 54.11% of the bakery products market in 2025.

Rising consumer demand for health-positioned and functional bakery innovation in whole grain, high-fibre, fortified, and free-from product categories, combined with the convenience economy’s expansion of packaged and on-the-go bakery format demand and the premiumisation trend elevating average unit prices through artisan, speciality, and clean-label product development across cakes, pastries, and speciality bread segments.

The bakery products market was valued at USD 528.49 billion in 2025.

The bakery products market is expected to grow at a CAGR of 5.48% from 2026 to 2035.

Get in Touch