Battery Management IC Market Report Scope & Overview:

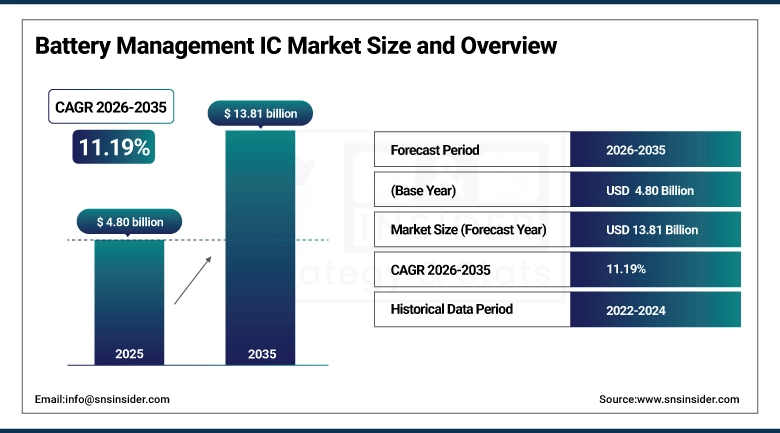

The Battery Management IC Market size was valued at USD 4.80 Billion in 2025 and is projected to reach USD 13.81 Billion by 2035, growing at a CAGR of 11.19% during 2026–2035.

Every rechargeable battery system from the lithium cell in a wireless earbud to the 100 kWh pack in an electric vehicle needs a semiconductor layer between the chemistry and the load. Battery management ICs are that layer they track state-of-charge, prevent overcharge and deep-discharge damage, authenticate cells against counterfeits, and balance charge distribution across multi-cell strings. Growing battery system volumes are not the only commercial driver here. The rising performance expectations placed on those batteries longer EV range, faster consumer-device charging, longer grid-storage calendar life are pushing IC specifications upward and replacing simpler designs with more complex, higher-value architectures across every end market.

Battery Management ICs (BMICs) Market Size and Forecast:

-

Market Size in 2025: USD 4.80 Billion

-

Market Size by 2035: USD 13.81 Billion

-

CAGR: 11.19% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Battery Management IC Market - Request Free Sample Report

Key Battery Management IC Market Trends:

-

EV battery pack architectures shifting to higher cell counts and 800V topologies are requiring cell balancing and monitoring ICs with sub-millivolt measurement accuracy and microsecond fault response times that were previously confined to aerospace-grade specifications.

-

Battery authentication ICs are moving beyond premium consumer electronics into EV battery modules, where counterfeit cell detection and supply chain integrity verification are becoming safety-critical requirements that regulators and OEMs are codifying into procurement standards.

-

Wireless BMS designs using short-range radio to replace the pack wiring harness are entering commercial EV production, creating demand for ICs that integrate RF communication, measurement, and balancing in a single package and increasing per-cell-group IC content.

-

Fast-charging requirements in consumer electronics and EVs are driving adoption of charger ICs capable of multi-protocol input recognition, high-frequency switching, and real-time thermal derating well beyond the capability of catalog charger ICs from five years ago.

-

Solid-state battery development programs are creating a parallel IC development track solid-state cells have different impedance characteristics and tighter voltage windows than liquid-electrolyte lithium-ion, requiring management architectures that existing designs cannot be adapted to support without significant re-design.

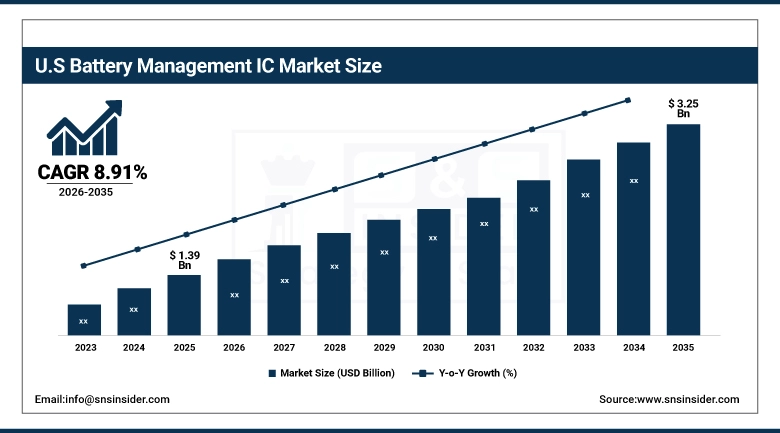

U.S. Battery Management IC Market Size Outlook

The U.S. Battery Management IC Market was valued at USD 1.39 Billion in 2025 and is projected to reach USD 3.25 Billion by 2035, at a CAGR of 8.91% during 2026–2035. Domestic EV assembly by Tesla, GM, and Ford draws on BMS IC supply chains being progressively localized, a technically demanding consumer electronics sector specifies high-accuracy fuel gauge and protection ICs at volume, and grid-scale energy storage tied to renewable buildout across the Southwest and Midwest adds a third demand layer.

Battery Management IC Market Growth Drivers:

-

Electric Vehicle Production Volumes and Energy Storage System Deployment Are Generating Sustained Demand for High-Specification Battery Management ICs Across Both New Architectures and Replacement Cycles

Battery management ICs in automotive applications carry a different design brief than those in consumer electronics. An EV pack operates for a decade across a wide temperature range and must maintain state-of-health estimation accuracy as cells age. The IC needs sub-millivolt measurement resolution across 96 or more series cells and fault detection that responds in microseconds. The global EV ramp is not generating proportional unit demand growth alone it is generating demand for more capable, more expensive ICs as pack voltages move from 400V to 800V architectures. Grid-scale storage adds another dimension utility-scale lithium-ion and flow battery installations require cell balancing and monitoring at a scale that was not commercially relevant five years ago, and even a handful of large battery energy storage system projects generate IC procurement volumes that are meaningful at market scale.

Battery Management IC Market Restraints:

-

Supply Chain Concentration, Long Qualification Cycles in Automotive Applications, and the Technical Complexity of Certifying ICs for High-Voltage Architectures Are Slowing Market Expansion Pace

The 2021–2022 semiconductor supply constraints exposed a structural vulnerability in BMS IC supply chains that has not been fully resolved analog mixed-signal foundry capacity is geographically concentrated in ways that create single-point-of-failure exposure for automotive customers on multi-year production programs. Qualifying a new BMS IC for automotive use is not a short project AEC-Q100 qualification, ISO 26262 functional safety validation, and OEM-specific protocols create high switching costs even when a better-specified alternative exists. The 800V architecture transition introduces isolation requirements and measurement dynamic range demands that existing designs handle with workarounds rather than clean solutions, and the engineering investment to fix that properly is a barrier smaller analog IC supplier with limited design resources find genuinely difficult to clear.

Battery Management IC Market Opportunities:

-

Solid-State Battery Commercialization, Wireless BMS Architectures, and AI-Integrated State Estimation Are Creating Design Win Opportunities for IC Suppliers Who Move Ahead of the Technology Curve

Solid-state battery programs at Toyota, QuantumScape, and Solid Power are not reaching meaningful volumes until the late 2020s, but the automotive IC design cycle means BMS ICs for those cells need to be in development now. Solid-state cells require different voltage windows and impedance-based state estimation than liquid-electrolyte lithium-ion, and suppliers with working silicon for solid-state architectures at qualification time will have a durable advantage. Wireless BMS replacing the pack's wiring harness with short-range radio between cell monitoring ICs and the pack controller has moved from concept to commercial EV production at several European OEMs, increasing per-cell-group IC content. AI-driven state-of-health estimation that trains cell aging models from IC-level telemetry is pulling demand for BMS ICs with higher-frequency, richer data output than current designs provide.

Battery Management IC Market Segment Analysis:

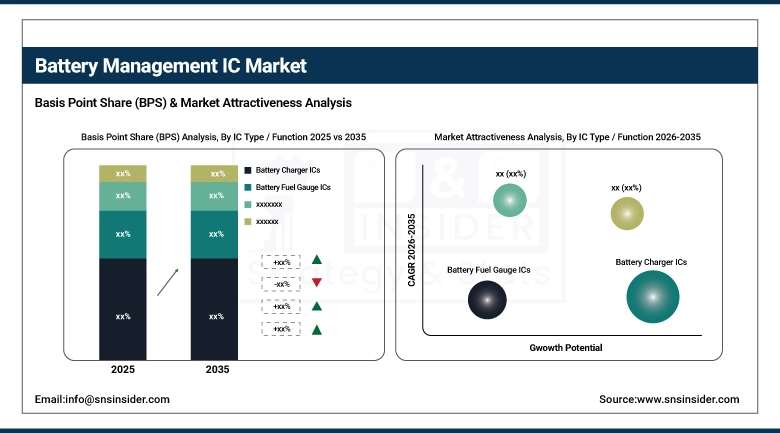

By IC Type / Function: Battery Charger ICs Lead While Battery Authentication ICs Drive Fastest Growth Through 2035

Battery Charger ICs dominated with a 28.36% share in 2025 at USD 1.36 Billion, while Battery Authentication ICs are expected to grow at the fastest CAGR of approximately 12.33% through 2035. Charger ICs hold their leading share because every rechargeable device needs one, the product range spans from simple single-cell linear chargers at fractions of a dollar to multi-phase switching chargers for EV on-board chargers at several dollars per unit, and the total addressable volume across consumer, automotive, and industrial end markets is the broadest of any BMS IC category. Authentication ICs are growing fastest because the counterfeit battery problem has reached a scale at which OEMs in multiple sectors are embedding cryptographic authentication as a standard design requirement rather than an optional feature, and the EV sector's adoption of pack-level and module-level authentication is creating a new high-volume demand channel that the category did not have three years ago.

By Battery Type / Chemistry: Lithium-Ion Leads While Flow Batteries Register Fastest CAGR Through 2035

Lithium-Ion Batteries dominated with a 26.84% share in 2025 at USD 1.29 Billion, while Flow Batteries are expected to grow at the fastest CAGR of approximately 12.69% through 2035. Lithium-ion's leadership simply reflects the installed base reality it is the dominant chemistry across consumer electronics, EVs, and the current generation of grid storage, and the IC content per lithium-ion system is well established and commercially mature. Flow batteries are growing fastest from a smaller base because utility-scale energy storage deployments using vanadium redox and other flow chemistries are scaling commercially, and the management electronics for flow systems which monitor electrolyte state, pump operation, membrane health, and cell voltage simultaneously are more complex and higher-value per unit of storage capacity than those for lithium-ion.

By Application: Automotive Leads While Energy Storage Systems Drive Fastest Growth Through 2035

Automotive (EV & HEV) dominated with a 32.45% share in 2025 at USD 1.56 Billion, while Energy Storage Systems (Renewables) are expected to grow at the fastest CAGR of approximately 12.25% through 2035. Automotive holds the dominant application share because EV battery packs require the highest IC content per system cell monitoring, balancing, protection, authentication, and communication ICs across hundreds of cells per vehicle and because production volumes are scaling rapidly enough to make the segment's growth rate competitive even from a large base. Renewable energy storage systems are growing fastest because the global buildout of utility and commercial-scale battery storage behind solar and wind generation is creating large new procurement volumes where the IC specifications are demanding enough to sustain competitive pricing.

By End-Use Industry: Automotive Industry Leads and Registers Fastest Growth Through 2035

Automotive Industry dominated with a 33.28% share in 2025 at USD 1.60 Billion and is also expected to grow at the fastest CAGR of approximately 11.75% through 2035, holding both positions simultaneously. The concentration of value in automotive BMS IC procurement reflects the combination of high per-vehicle IC content, rapidly rising production volumes, and the above-average ASPs that safety-critical automotive-grade ICs command relative to consumer or industrial specifications. The automotive industry's simultaneous hold on both the dominant share and the fastest growth rate is unusual across semiconductor segments and reflects the specific moment the EV adoption curve is in past early adoption but not yet into the volume maturity phase where market share gain rates typically slow.

Battery Management IC Market Regional Analysis:

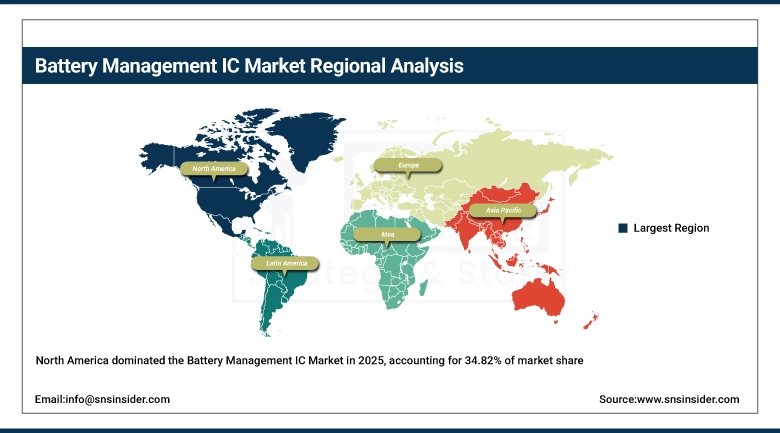

North America Battery Management IC Market Insights

North America dominated in 2025, accounting for 34.82% of market share at USD 1.67 Billion, projected to reach USD 4.09 Billion by 2035 at a CAGR of 9.39%. The United States accounts for 83.1% of regional demand at USD 1.39 Billion in 2025, growing to USD 3.25 Billion by 2035 at 8.91% CAGR, anchored by automotive OEM and battery manufacturer procurement in Michigan, Tennessee, Georgia, and Kentucky, consumer electronics supply chains, and growing energy storage procurement from utilities in California and Texas.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Battery Management IC Market Insights

Europe held a 21.47% share in 2025 at USD 1.03 Billion, expected to reach USD 2.75 Billion by 2035 at a CAGR of 10.33%. Demand is driven by Volkswagen Group, Stellantis, BMW, Mercedes-Benz, and Renault executing multi-year EV platform programs that sustain BMS IC procurement regardless of short-term sales fluctuations. Germany leads as the center of the continent's automotive electronics supply chain, reinforced by EU battery regulation and CO₂ fleet average standards that keep OEM battery investment on schedule.

Asia Pacific Battery Management IC Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 13.49% from 2026 to 2035, rising from USD 1.36 Billion in 2025 to USD 4.82 Billion by 2035. China's EV and battery manufacturing scale CATL, BYD, and the broader cell producer network supplying global customers is the dominant factor, with domestic IC suppliers becoming competitive across non-automotive specifications. Japan and South Korea add volume through their own EV programs and concentrated consumer electronics supply chains.

Latin America and Middle East & Africa Battery Management IC Market Insights

Latin America held 8.15% of global demand in 2025 at USD 391 Million, reaching USD 1.14 Billion by 2035 at a CAGR of 11.35%. Mexico drives procurement through its role as a major automotive assembly base for North American-market vehicles Brazil adds demand through EV adoption and utility-scale storage investment. Middle East & Africa held 7.20% at USD 346 Million in 2025, expected to reach USD 1.01 Billion by 2035 at 11.35% CAGR, led by Gulf state solar-plus-storage programs and EV infrastructure investment in the UAE and Saudi Arabia.

Competitive Landscape for Battery Management IC Market:

Texas Instruments holds one of the broadest BMS IC portfolios in the semiconductor industry, spanning single-cell charger ICs for consumer wearables through multi-cell automotive-grade monitor and balancer ICs rated for ISO 26262 ASIL-D. The BQ series is the reference design choice across consumer, industrial, and automotive applications, and TI's combination of measurement accuracy, protection feature integration, and application support depth gives it a design win rate that smaller suppliers struggle to match at the automotive qualification stage.

-

In March 2025, Texas Instruments announced the BQ79718-Q1, an automotive-qualified battery monitors and balancer IC supporting 800V architectures with ±0.5 mV per-cell accuracy across 18 series cells and ISO 26262 ASIL-D features without external monitoring components, placed immediately into evaluation programs at three European Tier 1 suppliers.

Analog Devices competes in the BMS IC market through its LTC and ADBMS product families, deployed in EV, energy storage, and industrial applications where measurement accuracy and daisy-chain communication reliability under electrically harsh conditions are non-negotiable. ADI's position is strongest at the high-performance end not the lowest-cost option, but frequently the specification-preferred one when the application cannot tolerate the measurement inaccuracies that less expensive alternatives exhibit in real battery environments.

-

In January 2025, Analog Devices launched the ADBMS6948, a 16-cell battery stack monitor IC with integrated open-wire detection, redundant voltage measurement paths for ISO 26262 compliance, and a revised isoSPI interface supporting 4 Mbps data rates for next-generation active cell balancing loop times. The launch included a reference design for 800V EV packs and AEC-Q100 Grade 0 automotive qualification.

Battery Management IC Companies are:

-

Texas Instruments Incorporated

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Infineon Technologies AG

-

Microchip Technology Incorporated

-

ROHM Co., Ltd.

-

ON Semiconductor Corporation (onsemi)

-

Semtech Corporation

-

Diodes Incorporated

-

Skyworks Solutions, Inc

-

Richtek Technology Corporation

-

Vishay Intertechnology, Inc.

-

Nordic Semiconductor ASA

-

Toshiba Electronic Devices & Storage Corporation

-

Silicon Laboratories Inc.

-

Nuvoton Technology Corporation

-

MagnaChip Semiconductor Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.80 Billion |

| Market Size by 2035 | USD 13.81 Billion |

| CAGR | CAGR of 11.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By IC Type / Function (Battery Charger ICs, Battery Fuel Gauge ICs, Battery Protection ICs, Battery Authentication ICs, and Cell Balancing & Monitoring ICs) • By Battery Type / Chemistry (Lithium-Ion Batteries, Lead-Acid Batteries, Nickel-Based Batteries, Flow Batteries, and Others) • By Application (Automotive (Electric Vehicles & Hybrid Vehicles), Consumer Electronics, Industrial Equipment, Energy Storage Systems (Renewables), and Medical Devices) • By End-Use Industry (Automotive Industry, Consumer Electronics Industry, Energy & Utilities, Industrial Sector, and Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Texas Instruments Incorporated; Analog Devices, Inc.; STMicroelectronics N.V.; NXP Semiconductors N.V.; Renesas Electronics Corporation; Infineon Technologies AG; Microchip Technology Incorporated; ROHM Co., Ltd.; ON Semiconductor Corporation (onsemi); Semtech Corporation; Diodes Incorporated; Skyworks Solutions, Inc.; Richtek Technology Corporation; Monolithic Power Systems, Inc.; Vishay Intertechnology, Inc.; Nordic Semiconductor ASA; Toshiba Electronic Devices & Storage Corporation; Silicon Laboratories Inc.; Nuvoton Technology Corporation; MagnaChip Semiconductor Corporation. |

Frequently Asked Questions

North America dominated the Battery Management IC Market in 2025

Battery Charger ICs dominated the Battery Management IC Market

Rapid growth of electric vehicles, rising adoption of energy storage systems, and increasing demand for efficient battery performance and safety in consumer electronics are driving the Battery Management IC market.

The Battery Management IC Market size was USD 4.80 Billion in 2025 and is expected to reach USD 13.81 Billion by 2035.

The Battery Management IC Market is expected to grow at a CAGR of 11.19% from 2026-2035.

Get in Touch