Solid State Battery Market Size & Overview:

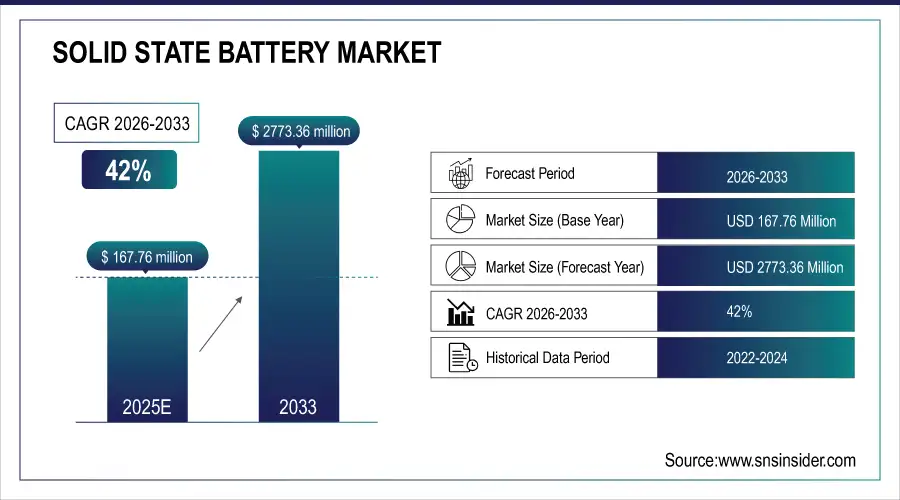

The Solid State Battery Market size is expected to be valued at USD 167.76 Million in 2025. It is estimated to reach USD 5592.06 Million by 2035 with a growing CAGR of 42% over the forecast period 2026-2035.

The Solid-State Battery Market is quickly progressing as a transformative technology in the energy storage industry, due to its ability to surpass the constraints of conventional lithium-ion batteries. Instead of liquid or gel electrolytes, solid-state batteries utilize a solid electrolyte, providing benefits like increased energy density, quicker charging speeds, extended longevity, and improved safety with reduced fire or explosion hazards. These traits make solid-state batteries especially appealing for electric vehicles (EVs) because enhancing range, cutting charging time, and guaranteeing safety are crucial. Major car manufacturers such as Toyota, BMW, and Volkswagen are making substantial investments in solid-state battery research, aiming to incorporate this technology into electric vehicles by the end of the 2020s. Furthermore, the consumer electronics industry is increasing the need for solid-state batteries, which offer smartphones, laptops, and wearables a more reliable and safer power source. In addition, solid-state batteries are becoming more popular in renewable energy storage systems because of their increased energy capacity and resilience, which make them well-suited for grid use.

Market Size and Forecast:

-

Market Size in 2025 USD 167.76 Million

-

Market Size by 2035 USD 5592.06 Million

-

CAGR of 42% From 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026-2035

-

Historical Data 2021-2024

Get More Information on Solid State Battery Market - Request Sample Report

Solid State Battery Market Trends:

• Rising focus on high-energy-density battery chemistries to achieve longer EV ranges and faster charging.

• Acceleration of solid-state battery commercialization timelines, with major automakers targeting deployment before 2030.

• Increased investments and partnerships between automakers, battery manufacturers, and material suppliers.

• Advancements in solid electrolytes, especially sulfide, oxide, and polymer types, to overcome safety and stability challenges.

• Growing push toward cost reduction and large-scale manufacturing to enable mass-market EV adoption.

U.S. Solid State Battery Market Size Outlook:

The U.S. Solid State Battery market is projected to grow from USD 67.10 Million in 2025 to USD 2.24 Billion by 2035. Growth is driven by rising demand for electric vehicles, consumer electronics, and medical devices requiring high energy density and enhanced safety. Increasing investments in U.S.-based battery manufacturing, government incentives for next-generation energy storage, and adoption in aerospace and defense applications further accelerate market expansion, enabling longer cycle life and faster charging solutions across industries.

Solid State Battery Market Growth Drivers: The Importance of Solid-State Batteries in Addressing Increasing EV Needs

The increasing desire from consumers for electric vehicles with greater range and capabilities is a major factor fueling the growth of the solid-state battery industry. With the electric vehicle industry seeing remarkable expansion, as demonstrated by the historic achievement of selling over 1 million battery electric vehicles in a year, the demand for improved battery technology has become more pressing. Consumers prefer vehicles with longer driving ranges and quicker charging times to accommodate their lifestyle of frequent long-distance travel. Solid-state batteries have the ability to offer a solution to these challenges by potentially increasing range by up to 50% compared to traditional lithium-ion batteries. They tackle the main concerns of range anxiety and restrictions on charging infrastructure through allowing vehicles to cover longer distances with one charge, thus increasing the practicality and attractiveness of EVs.

Solid State Battery Market Restraints: Transforming the Range and Weight of Electric Vehicles with Solid-State Batteries

Balancing weight and range in electric vehicles (EVs) has been a major obstacle because of the constraints of conventional lithium-ion batteries. In the United States, where larger vehicles are preferred and long-distance travel is frequent, the current EV battery technology frequently faces challenges in meeting these needs. As an example, the Tesla Model Y Long-Range has a battery that weighs around 1,700 pounds, which is close to 40% of the total weight of the vehicle, and it can travel 330 miles on a single charge. In order to increase the distance it can travel by 200 miles, the electric vehicle's battery would have to be enlarged by 1,000 pounds, resulting in a weight equivalent to that of a big pickup truck. On the other hand, a gas-fueled SUV just requires a slightly bigger gas tank to increase the range by 200 miles, showcasing the effectiveness of liquid fuel versus battery weight. Solid-state batteries offer an innovative resolution to these challenges.

Solid State Battery Market Segment Analysis:

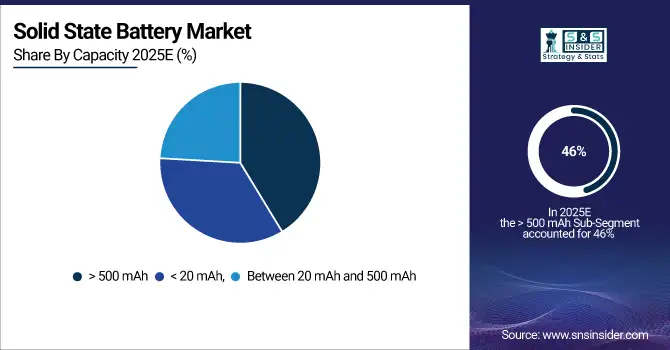

By Capacity

Based on Capacity, > 500 mAh is captured the largest share revenue in Solid State Battery Market with 46% of share in 2025E. Within the solid-state battery sector, the category with capacities exceeding 500 mAh has obtained the highest percentage of revenue, at 46% in 2025E. This supremacy shows the increasing need for high-capacity batteries that can provide longer range and improved performance, particularly in areas such as electric vehicles (EVs), portable electronics, and advanced wearables. Businesses are responding actively to this trend by creating and launching innovative products. An example is QuantumScape, a top player in solid-state battery tech, which has achieved notable progress in its high-capacity battery cells for EVs, offering more than 500 miles of range along with enhanced safety and energy density.

By Application

Based on Application, Consumer & Portable Electronics captured the largest share revenue in 2025E with 38% of share. This strong position highlights the significant need for cutting-edge battery technologies in devices like smartphones, tablets, wearables, and other portable gadgets. Solid-state batteries are well-suited for these tasks because of their higher energy density, safety, and small size when compared to standard lithium-ion batteries.The benefits of solid-state batteries in consumer electronics are significant. They offer increased energy density, resulting in extended battery life and decreased requirement for frequent recharging. Their solid electrolyte also improves safety by reducing the chances of leakage and thermal runaway, issues that arise with liquid electrolytes in standard batteries.

Solid State Battery Market Regional Analysis:

Asia Pacific Solid State Battery Market Insights

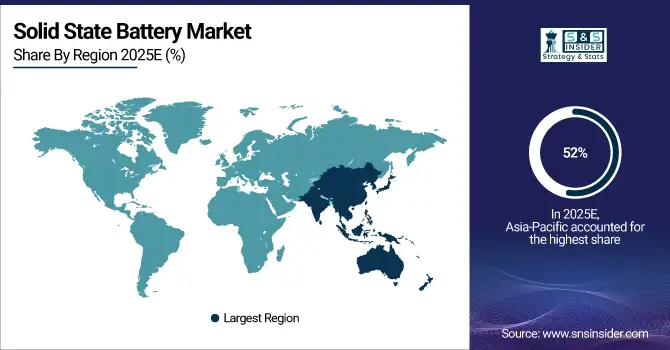

The Asia-Pacific region dominated the global solid-state battery market in 2025E, accounting for 52% of revenue and playing a crucial part in industry expansion. The region's strong presence is a result of its thriving electronic production industry, quick technological progress, and significant funding into energy storage options. Nations such as Japan, South Korea, and China are leading the way in this progress. In Japan, Toyota and Sony have led important advancements with advanced solid-state battery prototypes, with the goal of improving performance and safety for consumer electronics and automotive uses.

Need any Customization as Per Your Business Requirement on Solid State Battery Market - Enquiry Now

Europe Solid State Battery Market Insights

Europe is the second fastest growing region in Solid State Battery Market with largest share revenue in 2025E. grabbing a considerable portion of the revenue and highlighting its important role in advancing battery technology. The area's expansion is driven by its robust dedication to new ideas, strict environmental rules, and a growing need for EVs and sustainable energy storage options.Germany is leading Europe in solid-state battery technology, with companies such as Volkswagen and BMW making significant investments in research and development. Volkswagen has attracted attention for its partnership with QuantumScape to create advanced solid-state batteries that promise to improve electric vehicle range and safety.

North America Solid State Battery Market Insights

North America shows strong growth in the solid-state battery market driven by robust electric vehicle adoption, intensive R&D investment, and support from major automotive and tech companies. Government incentives for clean energy, advancements in battery materials, and the presence of leading innovators boost commercialization. The region focuses on scaling production, improving energy density, and enhancing EV performance and safety.

Latin America (LATAM) and Middle East & Africa (MEA) Solid State Battery Market Insights

LATAM and MEA are emerging markets for solid-state batteries, supported by gradual EV adoption, renewable energy expansion, and government interest in advanced storage technologies. Investments remain moderate but rising, with growing demand for efficient, safe, and long-life batteries for mobility and grid applications. These regions focus on early-stage partnerships, pilot projects, and technology imports to advance electrification and sustainability initiatives.

Solid State Battery Companies are:

-

Altairnano (Lithium Titanate Batteries)

-

Beijing Weilan New Energy Technology Co., Ltd. (Sodium-Ion Solid-State Batteries)

-

BrightVolt Solid State Batteries (Thin-Film Solid-State Batteries)

-

Cymbet (Solid-State Energy Storage Systems)

-

Hitachi Zosen Corporation (Sulfide-Based Solid-State Batteries)

-

Ilika Ltd. (Stereax® Solid-State Batteries)

-

Ion Storage Systems (Solid-State Lithium Batteries)

-

ITEN (Rechargeable Solid-State Batteries)

-

Johnson Energy Storage, Inc. (Lithium Metal Solid-State Batteries)

-

Prieto Battery Inc (3D Solid-State Batteries)

-

QuantumScape Corporation (Solid-State Lithium Metal Batteries)

-

Samsung SDI Co., Ltd. (Solid-State Lithium-Ion Batteries)

-

Solid Power (High-Energy Solid-State Batteries)

-

STMicroelectronics (Solid-State Lithium Batteries for Electronics)

-

Toyota (Solid-State Lithium-Ion Batteries for EVs)

Competitive Landscape for Solid State Battery Market:

Mercedes-Benz is actively advancing solid-state battery development to enhance the performance, range, and safety of its next-generation electric vehicles. The company is collaborating with leading battery innovators to integrate high-energy-density solid-state cells into future models, targeting longer driving ranges and faster charging. Mercedes-Benz’s strategy focuses on premium EV innovation, sustainability, and accelerating commercialization of solid-state technology across its luxury electric lineup.

-

On September 10, 2024, Mercedes-Benz and U.S. battery startup Factorial announced a collaboration to develop the Solstice solid-state battery. This new battery aims to boost EV range by approximately 80% over current averages, with an energy density of 450 Watt-hours per kilogram, and is expected to be ready for production by the end of the decade.

ProLogium Technology is a leading developer of next-generation solid-state batteries, known for its advanced lithium ceramic electrolyte technology offering high safety, long cycle life, and superior energy density. The company collaborates with major global automakers to accelerate mass production and commercialization. ProLogium focuses on scaling manufacturing capacity and delivering reliable solid-state solutions for electric vehicles and energy storage applications.

-

In July 2023, ProLogium Technology Co, Ltd. and MAHLE GmbH agreed to collaborate on creating the initial thermal management system for ProLogium's upcoming solid-state batteries. This deal will facilitate the marketability of solid-state battery solutions with higher energy density, enhanced safety, and longer lifespan.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 167.76 Million |

| Market Size by 2035 | USD 5592.06 Million |

| CAGR | CAGR of 42% From 2026 to 2035 |

| Base Year | 2024 |

| Forecast Period | 2026-2035 |

| Historical Data | 2021-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

|

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Altairnano, Beijing Weilan New Energy Technology Co., Ltd., BrightVolt, Cymbet, Hitachi Zosen Corporation, Ilika Ltd., Ion Storage Systems, ITEN, Johnson Energy Storage, Inc., Prieto Battery Inc, QuantumScape Corporation, Samsung SDI Co., Ltd., Solid Power, STMicroelectronics, Toyota. |

Frequently Asked Questions

Asia-Pacific dominated the Solid State Battery Market in 2025E.

The Consumer & Portable Electronics segment dominated the Solid State Battery Market.

The major growth factor of the Solid State Battery Market is the increasing demand for higher energy density and improved safety in batteries for electric vehicles and portable electronics.

The Solid State Battery Market size was valued at USD 167.76 Million in 2025E and is expected to reach at USD 5592.06 Million and grow at a CAGR of 42% over the forecast period of 2026-2035.

The Solid State Battery Market grow at a CAGR of 42% over the forecast period of 2026-2035.

Get in Touch